Businesses usually have both tangible and intangible assets that aid them with revenue generation, ease daily operations, and reduce expenses. For all fixed assets apart from land, their worth begins to decline once they have been purchased. This decline in value can either be attributed to the passage of time or the wear and tear of use. As the value of fixed assets reduces over time, due to usage, or both, making an adjusting entry for depreciation becomes necessary.

This adjusting entry for depreciation is made to reflect the decrease in value of the fixed asset in the company’s balance sheet and the expense in the income statement. Here, we shall discuss what is required when making the adjusting entry for depreciation as well as some examples of this adjusting entry.

Read about: Types of adjusting entries with examples

What is the adjusting entry for depreciation?

The adjusting entry for depreciation refers to a journal entry made by a company to track the reduction in the value of a fixed asset over its useful lifespan. This journal entry is usually a debit to the depreciation expense account and a credit to the accumulated depreciation account. The adjusting entry for depreciation affects the company’s income statement and balance sheet as it increases the expenses for the accounting period while reducing the company’s assets.

The reduction in the value of assets is known as depreciation and assets depreciate over time with or without use. If a company were to account for its fixed assets purchase at once, it will affect its financial statements in such a way that its expenses for that particular period when the purchase was made become overstated, and conversely, profits for subsequent periods may be overstated as well. Thus, in order to present a true picture of a company’s income and expenditures, adjusting entries for the depreciation of fixed assets become necessary. These fixed assets often appear on the company’s balance sheet as long-term assets under the property, plant, and equipment (PP&E) line.

In each accounting period, a predetermined portion of a company’s fixed assets is transferred through the adjusting entry for depreciation from the fixed assets to depreciation expense. This adjusting entry for depreciation is usually made at the end of each accounting period which could be monthly or annually so that the cost of an asset can be correctly matched with the revenue generated by utilizing the assets. All fixed assets such as buildings, furniture, machinery, equipment, fixtures, and vehicles depreciate over time with use and therefore, require an adjusting entry for depreciation.

The only fixed asset that does not require an adjusting entry for depreciation is land, this is because, unlike other fixed assets, the land is not liable to wear and tear from use. Instead, the value of land generally increases in value over time.

Read about: Adjusting entry for unearned revenue

Making adjusting entries for depreciation

To effectively make the right adjusting entry for depreciation, one has to take into account the cost of the asset, its salvage value, and its useful life span. The cost of the asset serves as the bedrock for adjusting entries for depreciation. The assets cost normally includes the dollar amount spent for the asset purchase as well as related expenses such as taxes and shipping. The salvage value is the estimated amount at which the asset can be sold at the expiration of its useful life span. The useful life span of an asset is the estimated time within which the asset is expected to be of use to the company.

Different methods exist when accounting for the depreciation of an asset but the most common method used by companies is the straight-line depreciation method which keeps the amount of depreciation constant over the useful life span of the asset. You can make an adjusting entry for depreciation using the straight-line method in the following simple steps.

- Determine the asset’s cost: The first step when making an adjusting entry for depreciation is to determine how much the asset cost. This includes the amount paid for the asset purchase as well as other associated costs such as delivery or shipping fees and taxes. For example, if a company buys a computer for $5,000 and pays $500 as tax for the purchase, then, the cost of the asset will be $5,500.

- Determine the salvage value: It is important to determine the salvage value of an asset right from the time when it is purchased as the salvage value plays an integral role when calculating the amount that will be recorded when making an adjusting entry for depreciation. The salvage value is the price at which the asset may be sold after its useful life span has been exceeded.

- Determine the useful life span: The time during which an asset functions optimally is considered its useful life span. This varies based on the type of asset and the rate at which it gets affected by wear and tear as a result of use. Some assets such as vehicles may have a shorter useful lifespan when compared to other assets such as furniture.

- Subtract the salvage value from the asset’s cost: After determining the asset’s cost and its salvage value, subtract the salvage value of the asset from the cost. For example, if the cost of equipment is $90 and its salvage value is $13, subtract $13 from $90. This will leave you with $77.

- Determine the depreciation amount: When you have subtracted the salvage value from the asset’s cost, divide the result by the useful life span of the asset to arrive at the depreciation amount. For instance, if the useful life span of the equipment we mentioned earlier is 5 years, then we will divide $77 by 5. This will give us $15.4 which is the amount of depreciation that will be recorded annually when making an adjusting entry for depreciation. If the adjusting entry for depreciation will be made monthly, then the result has to be further divided by 12 to account for the 12 months in a year.

- Make the adjusting entry for depreciation: After determining the depreciation amount, the adjusting entry for depreciation can then be made using the double-entry bookkeeping method. This involves a debit to depreciation expense and a credit to accumulated depreciation.

Do you make adjusting entries for depreciation?

Yes, adjusting entries for depreciation is usually made at the end of each accounting cycle which could be either monthly or yearly. Companies make the adjusting entry for depreciation to account for the gradual reduction in the value of the assets they own over time.

Read about: Why are adjusting entries necessary?

How do you record adjusting entry for depreciation?

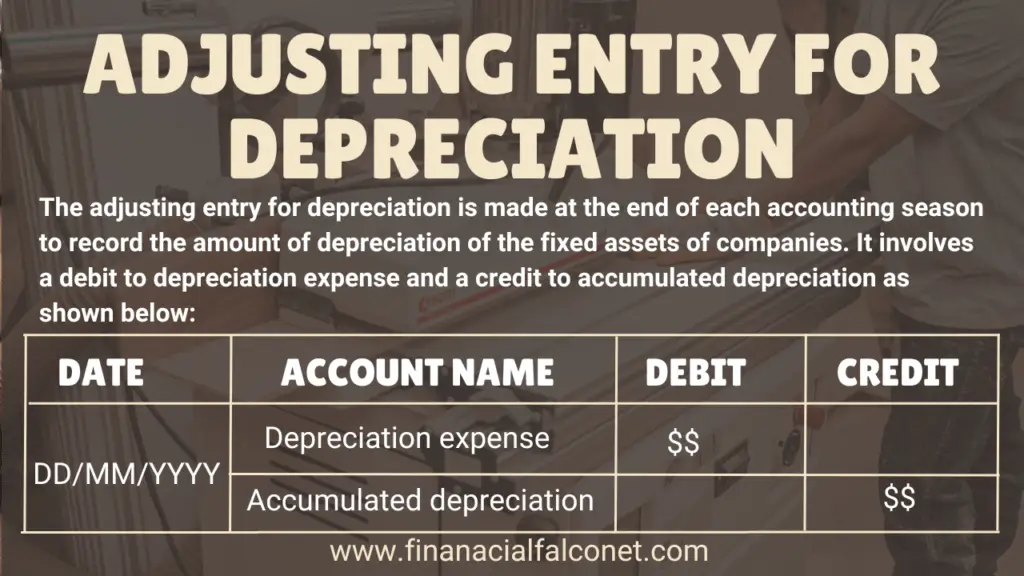

In order to record the adjusting entry for depreciation, companies make journal entries that involve the depreciation expense account and the accumulated depreciation account. These accounts are debited and credited respectively to account for the gradual decrease in value for the particular asset for which the adjusting entry for depreciation is made for. This adjusting entry will be as shown in the table below:

| Date | Account name | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Depreciation expense | $$ | |

| Accumulated depreciation | $$ |

This adjusting entry for depreciation is made at the end of each accounting period and records the amount that is depreciated for the asset within that period in the depreciation expense account. Previous depreciation expense is added to the accumulated depreciation account such that the depreciation expense account becomes empty at the beginning of every accounting period. The debit to depreciation expense and the credit to accumulated depreciation indicate an increase in both accounts.

Examples of adjusting entries for depreciation

Example 1

Suppose a logistics company bought a delivery van worth $60,000in January 2023. If the van’s salvage value is $10,000 and its useful life is 5 years. We can calculate the amount that will be recorded as its annual depreciation using the depreciation formula;

Depreciation = Cost of an asset – Salvage value ÷ Asset’s useful life span

Depreciation = ($60,000 – $10,000) ÷ 5

Depreciation = 50,000 ÷ 5

= $10,000

Now that we have determined the yearly depreciable amount, The company can make the adjusting entry for depreciation the following year as shown below:

| Date | Account name | Debit | Credit |

|---|---|---|---|

| 01/01/2024 | Depreciation expense | $10,000 | |

| Accumulated depreciation | $10,000 |

Example 2

Suppose a laundry mart bought a new washing machine that costs $8,000 and it has a useful life span of 3 years. If the machine was bought in March 2023 and its salvage value is $1,000, we can determine its yearly depreciation using

Depreciation = Cost of an asset – Salvage value ÷ Asset’s useful life span

Depreciation = ($8,000 – $1,000) ÷ 3

Depreciation = $7,000 ÷ 3

Depreciation = $2,333.33

Thus, the yearly journal adjusting entry for the depreciation of the washing machine will be as shown in the table below:

| Date | Account name | Debit | Credit |

|---|---|---|---|

| 01/03/2024 | Depreciation expense | $2,333.33 | |

| Accumulated depreciation | $2,333.33 |

If the laundry mart wants to make monthly adjusting entries for depreciation, they will have to divide the yearly depreciation by 12 to arrive at the monthly depreciation amount.

Hence, monthly depreciation = $2,333.33 ÷ 12

Monthly depreciation = $194.44

In this instance, the adjusting entry for depreciation will be made monthly and the first entry will be as follows:

| Date | Account name | Debit | Credit |

|---|---|---|---|

| 01/04/2023 | Depreciation expense | $194.44 | |

| Accumulated depreciation | $194.44 |

Read about: Adjusting entries for supplies

Conclusion

The adjusting entry for depreciation is made at the end of each accounting season to record the amount of depreciation of the fixed assets of companies. It involves a debit to depreciation expense and a credit to accumulated depreciation. This adjusting entry impacts the company’s financial statements and equally affects the taxes paid by the company annually. In the United States, the Internal Revenue Service (IRS) has specified guidelines concerning the depreciation of various fixed assets as well as the methods of depreciation to use.

The method currently in use is the Modified Accelerated Cost Recovery System (MACRS) which uses either the straight-line depreciation method that we used in the examples above or the double-decline method whereby the rate of depreciation varies with the first year normally being higher than subsequent years. The double-decline depreciation method is often used for assets that have a rapid rate of depreciation, especially in their first year of use. Irrespective of the depreciation method a company uses, it is important to make timely adjusting entries for depreciation to ensure that the financial records are correct and up-to-date.

Last Updated on November 3, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.