Are expenses assets, liabilities, or equity? For accounting purposes, expenses are recorded on a company’s income statement rather than on the balance sheet where assets, liabilities and equity are recorded. Therefore, expenses are not assets, liabilities, or equity, rather they decrease assets, increase liabilities and decrease equity.

In this article, we will discuss, expenses, assets, liabilities and equity and the reasons why expenses are not assets, liabilities or equity.

Related: Is accumulated depreciation an asset?

What are expenses, assets, liabilities and equity in accounting?

Expenses, assets, liabilities, equity and revenue are the five major types of accounts in financial statements. Revenue and expenses are reported on a company’s income statement whereas assets, liabilities and equity make up the major accounts on a company’s balance sheet.

Expenses

Expenses are the operational costs that a company incurs in order to generate revenue. These are the expenditures that allow a company to operate. It involves the cost that a company needs to spend on the day-to-day operation of its business. Examples of expenses examples include payments to suppliers, employee wages, entertainment, advertisement, equipment depreciation, factory leases, etc. Expenses and revenues are usually broken down in the company’s income statements. Hence, the net profit of a company will be the total revenue made minus its expenses.

In order to calculate the profitability of a business, the expense is deducted from revenue. Revenue and expenses are both reported on the income statement (profit and loss report). Expenses are recorded on the debit side of the profit and loss report and measure a business’s profit and losses.

In a company, the management teams aim to maximize profits which is achieved by boosting revenues while keeping expenses in check. Cutting down costs and expenses can help companies make more money from sales. Nevertheless, it is important to note that even though costs and expenses may seem similar, there are not the same when it comes to accounting. Costs are the finances used to purchase an asset while expenses are the cost incurred in the use and consumption of these assets.

Expenses in accounting are recorded through cash basis or accrual basis accounting methods. In cash basis accounting, expenses are only recorded when they are paid. While, in the accrual accounting method, they are only recorded when they are incurred. Expenses can be grouped into two main types in business such as operating and nonoperating expenses.

The expenses that are incurred in relation to the main operations of the business are known as operating expenses. They include expenses such as the cost of goods sold, direct labor, administrative fees, office supplies and rent; that are incurred from the normal day-to-day running of the company’s business.

Non-operating expenses, on the other hand, are not directly related to the main operations of the business. Hence, they are incurred outside of a company’s day-to-day activities such as interest charges and other costs associated with borrowing money or costs on obsolete inventory. From an accounting perspective, non-operating expenses and operating expenses are separated so that the company will be able to determine how much it earns from its core operations.

When an expense is recorded, it appears within a line item in the income statement and appears indirectly on the balance sheet. As an amount of expense is recorded, the Retained Earnings line item within the equity section of the balance sheet will decline by the same amount. Also, either the asset side of the balance sheet will decrease or the liabilities side will increase by the recorded amount of the expense. Hence, ensuring the balance sheet is in balance.

An example of how expenses appear directly in the income statement and indirectly in the balance sheet is when an expense item is paid in cash, the Cash account in the assets section will decline or if some inventory were written off, Inventory will decline. Another example would be when a depreciation charge is made, this will cause the accumulated depreciation (contra asset account) on the balance sheet to increase. Moreso, accrued expenses increase when an expense accrual is created and accounts payable on the balance sheet would increase when a supplier invoice that has not yet been paid is recorded.

Now that we have an idea of what expenses entail; are expenses assets, liabilities or equity? Let’s look at what are considered assets and if expenses can be considered as one.

Assets

Assets are things of value or resource that an individual, corporation, or country owns with the expectation that they will yield future benefits. They are listed on the balance sheet of a company and are classified as fixed, current, financial, and intangible assets. These items are created or purchased to increase the value of a business and benefit its operations. Therefore, anything of economic value that the company uses to generate cash flow, improve sales or reduce expenses is an asset.

Expenses are not basically used to generate cash flow rather they are the operational costs incurred from the use of assets to generate cash flow. Therefore, expenses can’t be considered assets. An asset has the ability to generate cash inflows or decrease cash outflows in order to produce economic benefit. Assets will therefore provide a current, future, or potential economic benefit for the company.

Examples of such items include properties, cash, inventory, vehicles, long-term investments, accounts receivable (unpaid invoices from customers), furniture, real estate, equipment, patents, trademarks, etc. Moreso, money loaned out is considered an asset because the company is owed that amount.

Expenses are therefore the cost incurred in the use and consumption of these assets to generate cash flow. That is, owning an asset enables a business to meet its financial commitments and increase its equity. Therefore, a company that has a high proportion of assets compared to its liabilities is an indicator of good financial health because more assets to liabilities indicate a higher degree of liquidity.

Why expenses are not assets

In as much as assets and expenses are both incurred when goods or services are purchased for the business, they’re not considered the same thing. Expenses are not assets and are reported differently in the financial statements of a business.

Resources owned by the business that can help the business produce goods and services are considered an asset. Such an item can be long-term or short-term and usually decreases in value over time. These assets are reported on the balance sheet together with liabilities and equity. An expense, on the other hand, is a cost related to the day-to-day running of a business.

Assets and expenses represent very different things and that is why the way an expense is accounted for on a business’s financial statements is very different from the way an asset is accounted for. According to the principles of double-entry bookkeeping, when an expense is recorded as a debit, a credit entry has to be created also in another account which is usually an asset account or a liability account.

At least for a fact, we now know that expenses are not assets, but are they liabilities or equity? Let’s look at what liabilities are in a company’s financial statements.

Liabilities

Liabilities are debts or financial obligations that a company owes other parties. They are the obligations that the company has to settle either in the near future or in further future. These debts or financial obligations are settled over time through the transfer of economic benefits such as money, goods, or services.

Liabilities can easily be contrasted with assets because they are the things that the company owes or has borrowed whereas assets are the things that the company owns or is owed. They are recorded on the right side of the balance sheet and include items such as accrued expenses, accounts payable, loans, mortgages, interest payable, deferred revenues, bonds, wages payable, unearned revenue, and warranties. Accounts payable and loans payable are the most common types of liabilities.

Why expenses are not liabilities

Expenses are not liabilities even though they may seem as though they’re interchangeable terms. What the company spends on a monthly basis to fund the business operations are expenses whereas liabilities are the debts and financial obligations that the company owes to other parties. Liabilities are reported in a company’s balance sheet and some expenses can be a subset of the company’s liabilities but are recorded differently to track the financial health of the business.

Expenses are more immediate in nature and are paid on a regular basis, compared to liabilities that are owed for a period of time. This is why expenses are shown on the monthly income statement to determine the company’s net income. However, expenses can become liabilities when they are not paid for. For example, a company can’t afford to pay cash to purchase its monthly office supplies and decides to take out a loan to pay for these expenses. The loan then becomes a liability.

Conclusively, expenses are not liabilities, thus, they differ in accounting. Expenses are shown on the income statement whereas liabilities are reported on the balance sheet. Paying expenses immediately keeps the company’s business afloat and the balance sheet can reflect business expenses by drawing down the cash account or increasing accounts payable. More so, liabilities and expenses diverge when it comes to the payment and accrual of each.

Knowing that expenses are neither assets nor liabilities; are they equity? Let’s look at what equity is in a company’s financial statements.

Equity

The equity of a company represents ownership of a company’s shares in proportion. This can be thought of as a degree of residual ownership in an asset or company, after subtracting all the debts associated with the asset or company. It is usually referred to as shareholders’ equity for public companies or owners’ equity for privately held companies. This equity is found on a company’s balance sheet and can represent a company’s book value. It is one of the most common pieces of data that analysts use in several key financial ratios such as return on equity (ROE) to assess the financial health of a company.

Equity, in the case of liquidation, represents the amount of money that would be returned to the shareholders of a company, if all the assets of the company were liquidated and all debts paid off. In the case of acquisition, the equity is the value of the company sales minus any liabilities that the company owes, that are not transferred with the sale of the company. It is simply the portion of the company’s total assets that the owner fully owns which may be in cash or assets.

Equity is found on a company’s balance sheet together with assets and liabilities. It represents the owners’ or shareholders’ stake in the company which is calculated as the total asset of the company minus its total liabilities. Hence, equity is paid lots of attention by business owners or shareholders because it is their financial share of the company. Therefore, equity can also be referred to as net worth.

Why expenses are not equity

Expenses are not equity rather they cause the owner’s equity to reduce. The major accounts that influence owner’s equity are expenses, losses, revenues, and gains. When there are revenues and gains, the owner’s equity increases but when there are expenses and losses, the owner’s equity decreases.

The normal balance of owner’s equity is a credit balance, and as such, expenses must be recorded as a debit. The debit balance in the expense accounts at the end of the accounting year will be closed and transferred to the owner’s equity account, thus, reducing the owner’s equity. For corporations, the debit balance will be closed and transferred to Retained Earnings which is a stockholders’ equity account.

Related: Is the common stock a current asset?

Are expenses assets liabilities or equity?

No, expenses are neither assets, liabilities or equity. Expenses are shown on the income statement to offset revenue whereas, assets, liabilities and equity are shown on the balance sheet. Liabilities on the balance sheet usually offset assets; that is assets= liabilities + equity.

The income statement on which expenses are reported shows the company’s financial performance for a given period of time, usually over the span of one quarter. It shows the profit and loss of the company and calculates its net income. Therefore, expenses, together with revenue, gains and losses, determine the net income for that period.

On the balance sheet of a company, expenses are reflected in two ways; they can increase a liability account such as accounts payable or draw down an asset account such as cash. Expenses are not assets but can fund daily business operations and contribute to turning a profit, just like assets. Also, expenses are not liabilities but can become a liability on the balance sheet when it is not paid off immediately. Moreso, expenses are not equity; they rather cause a decrease in owner’s equity.

Furthermore, in double-entry bookkeeping, expenses would be reported as a debit to an expense account and a credit to either an asset account or a liability account, which are balance sheet accounts. Therefore, expenses decrease assets or increase liabilities.

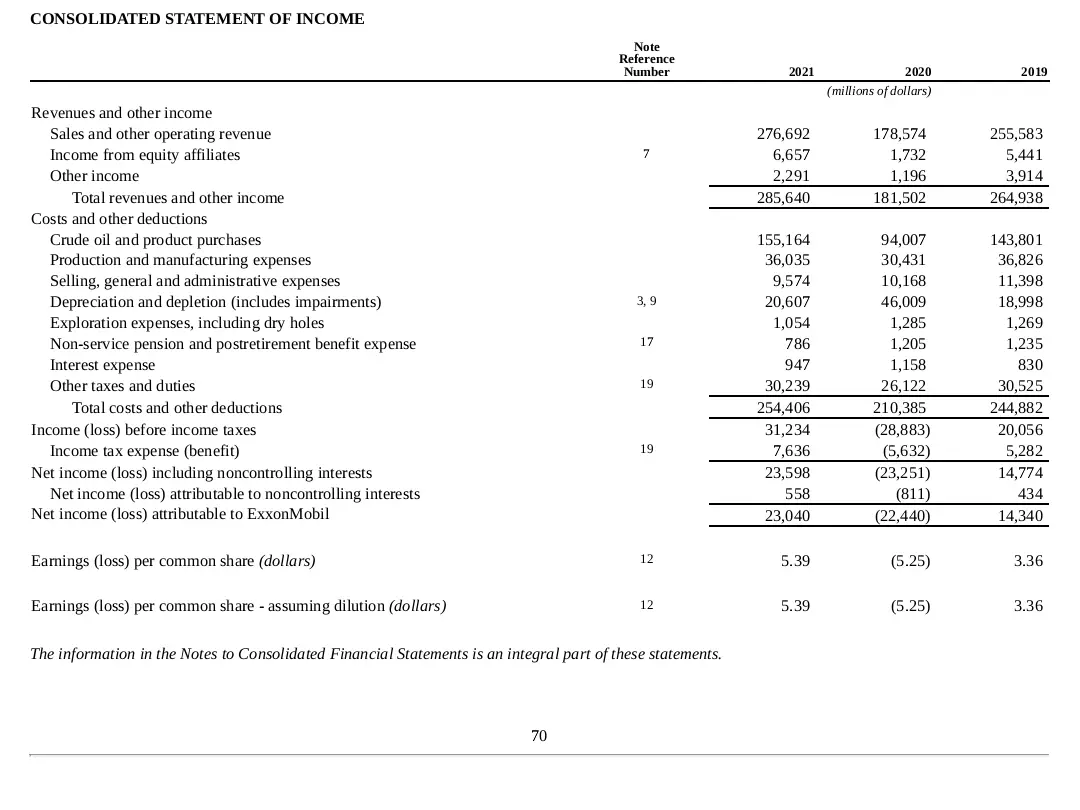

Let’s look at how expenses, assets, liabilities and equity are accounted for in a company’s financial statements. We will be using the excerpt of Exxon’s income statement and balance sheet from its 10K statement (pages 72 & 74) for 2019, 2020 and 2021 as an illustration:

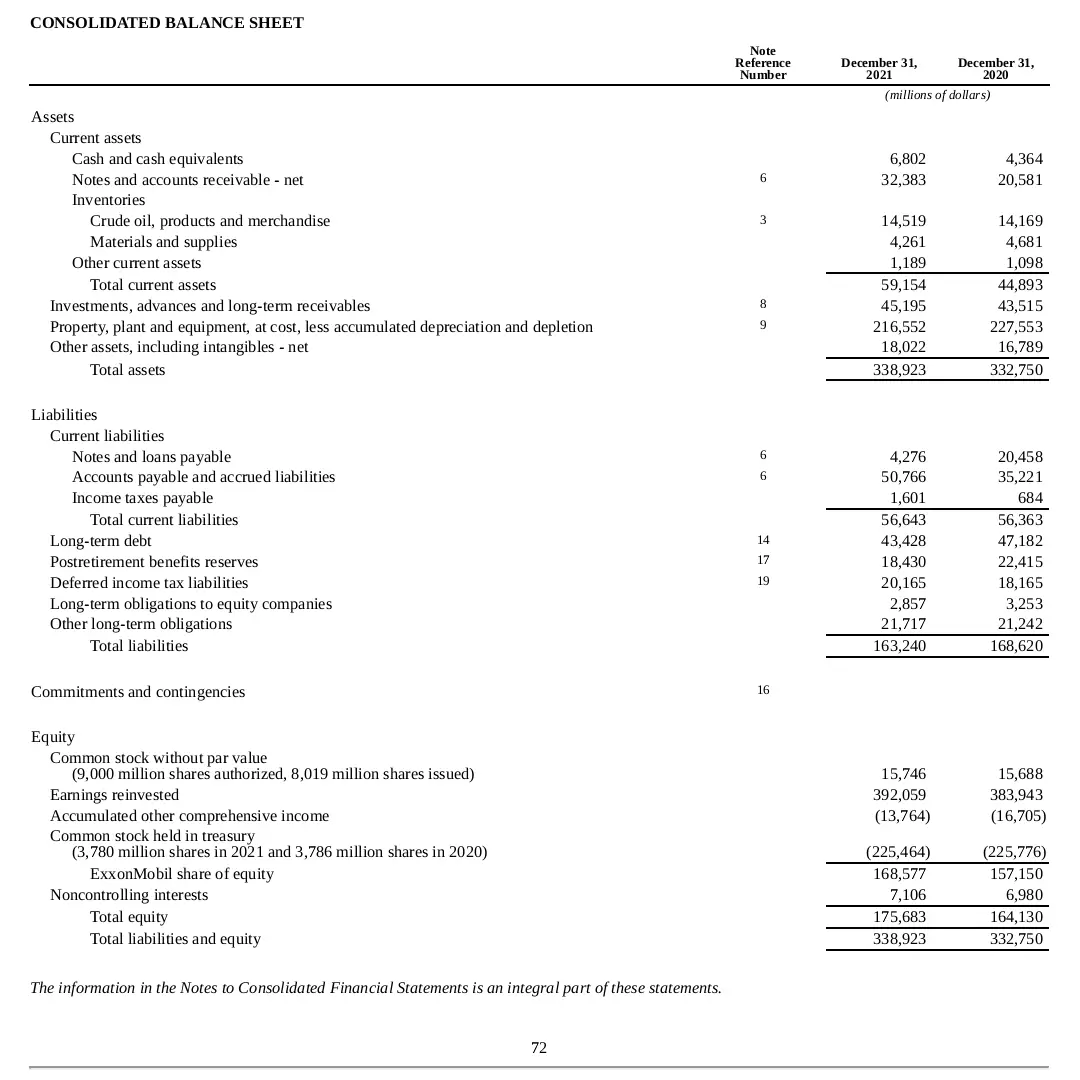

As seen in the image above, the company’s expenses usually appear on the income statement after the top-line figure (revenue). We can see that expenses appear in the company’s income statement and not on the balance sheet below, where assets, liabilities and equity appear:

As seen in the image above expenses are not on the balance sheet compared to assets, liabilities and equity that are listed on the company’s balance sheet. Nevertheless, even though expenses usually appear on the income statement, they can cause an increase in liabilities like accounts payable or a decrease in an asset account like cash.

See also: Is preferred stock an asset?

If expenses are not assets, liabilities or equity; what are they?

Just like revenue accounts, expenses are a separate account on the income statement. The expense account and revenue account are temporary accounts that collect data for one accounting period and are reset to zero at the beginning of the next accounting period. They are zeroed at the end of the year in order to make room for the recordation of a new set of expenses and revenues in the next fiscal year.

That is, expense accounts and revenue accounts only exist for a set period of time- a month, quarter, or year, and then new accounts are created for each new period. This is why they are considered temporary accounts.

An expense account report all the decreases in the owners’ equity that arise from the use of assets and all increasing liabilities in delivering goods or services to a customer. It is one of the major charts of accounts. It takes account of the costs of doing business, which entails all expenses incurred by a business during an accounting period such as expense accounts for bad debts, water, telephone, fuel, salaries, electricity, repairs, wages, depreciation, interest, stationery, entertainment, honorarium, rent, utility, etc.

The expenses account on the income statement helps the company oversee and organize the various expenses of its business over a certain duration of time. This account is broken into sub-accounts so that the company can clearly see where money is going and organize the finances accordingly. Such expense sub-accounts include Wages expenses, Salary expenses, Supplies expenses, Rent expenses, and Interest expenses.

The expense account increases when a company makes use of funds (a debit) and decreases when funds are credited from another account into the expense account. Therefore, the expense account stores information about different types of expenditures in a company’s accounting records. Thus, appearing on the business’s profit and loss account.

Conclusively, because in accounting, expenses are not considered as assets, liabilities or equity, when it comes to bookkeeping, expenses are reported as a separate account from the asset, liabilities and equity accounts. There are basically five types of accounts that show up on both a balance sheet and an income statement. The table below shows the 5 major accounts in a company’s Charts of Accounts (COA):

| Types of account | Definition | Examples (sub-accounts) | Debit | Credit | |

|---|---|---|---|---|---|

| 1 | Expense Account | Expenses are the operational costs that a company incurs in order to generate revenue. It involves the cost that a company needs to spend on the day-to-day operation of its business | Advertising, utilities, rent, travel, salaries, payments to suppliers, employee wages, entertainment, equipment depreciation, factory leases, etc | Increase | Decrease |

| 2 | Asset account | Assets are items of economic value that provide future economic benefits to a company | Cash, accounts receivable, inventory, prepaid expenses, savings account, petty cash balance, vehicles, buildings, undeposited funds, property and equipment | Increase | Decrease |

| 3 | Liability account | Liabilities are debts or financial obligations that a company owes other parties that the company has to settle either in the near future or in further future | Accounts payable, income tax payable, loans payable, bank fees, accrued liabilities, payroll liabilities, notes payable | Decrease | Increase |

| 4 | Equity account | The equity account is an account recording the owners’ or shareholders’ stake in the company which is calculated as the company’s total assets minus its total liabilities | Available-for-sale securities, stocks (common stock and preferred stock, treasury stock), bonds, mutual funds, real estate, pension and retirement plans, derivative instruments, debt security | Decrease | Increase |

| 5 | Revenue account | The revenue account is the financial account that contains the receipts of the income or interest from investments that the company receives through its business transactions | Sales revenue, service revenue, interest income, investment Income | Decrease | Increase |

See also: Common stock: asset or liability?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.