Assets, liabilities, and equity are important terms when it comes to operating a company and understanding its financial standing. A company’s balance sheet is its financial statement that summarizes its assets, liabilities, equity, and other activities related to the company’s finance. One equation that shows the relationship between assets, liabilities, and equity is the accounting equation. We shall discuss this hereafter and also look at similarities and differences between assets, liabilities, and equity.

Understanding assets, liabilities, equity and their types

The words assets, liabilities, and equity are used by Accountants a lot, this is because they are the largest classifications in any accounting spreadsheet. Below we shall discuss what assets, liabilities, and equity mean.

What are assets?

Assets are resources that are expected to bring future economic benefits to their owners usually by reducing the owner’s cash outflow while increasing cash inflow. Assets can be tangible or intangible, what is important is being able to use them to obtain a positive economic value. When tangible, they can be seen physically such as cash, land, machinery, buildings, etc. The intangible assets mostly refer to a person’s intellectual property, patents, social media following, trademarks, and all other assets that are not physical.

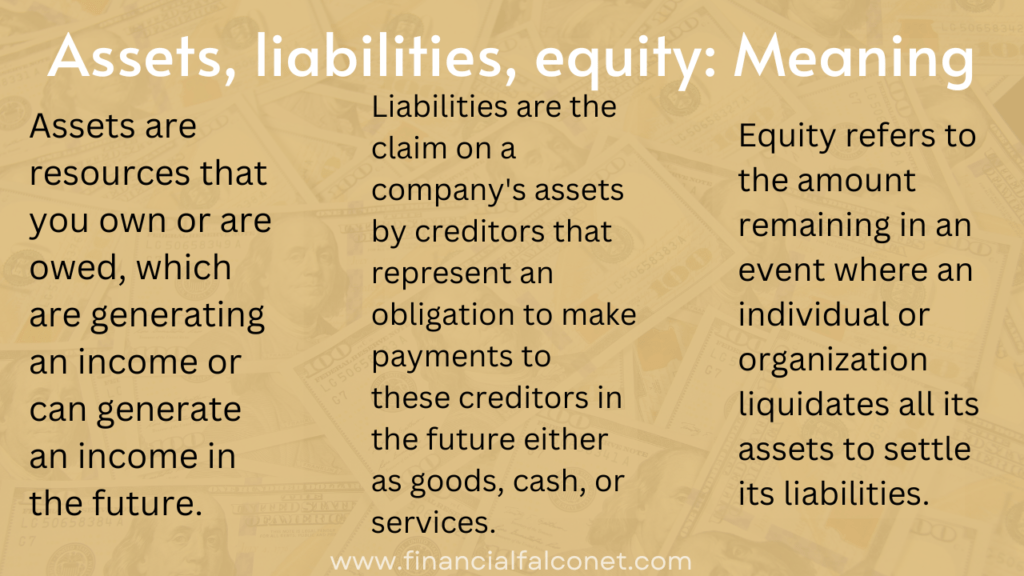

Simply put, assets are anything that brings value to their owners; by this, the owner is said to have a return on their asset. Assets are resources that you own or are owed, which are generating an income or can generate an income in the future. Thus they can be owned by individuals, corporate entities, states, and countries.

Corporate entities keep a record of all their assets, this is usually done on the credit side or the left-hand side of the balance sheet. However, with recent advancements in technology and its use in making the balance sheet, the assets appear on the same side as the liabilities and equity on one page. Assets are usually equal to the company’s liabilities and equity.

For most assets, the main economic benefit that is derived from them is their appreciation in value or market price as time passes and as such, they contribute to the daily business operations and enhance the company’s stability and financial growth.

Types of assets

- Current assets

- Non-current assets

Current assets

These are assets that are easily liquid, which means that can easily be sold for cash within a short period which is usually a fiscal year. These assets bring value to the company within the short time frame of a year. A fiscal year is a period of fifty-two to fifty-three (52 -53) weeks or twelve (12) months which is generally used for accounting and tax purposes. The fiscal year can end on the last day of any month apart from December.

Current assets include prepaid liabilities, accounts receivable, cash, stock inventory, and short-term investments such as government bonds, high-yield savings accounts, and treasury bills. The accounts receivable records any amount that is owed to the company which usually includes payments for goods or services that have already been done.

Non-current assets

Non-current assets are the company’s long-term assets. Generally, these assets are those that the company does not intend to sell. However, if the need to sell them arises, they mostly require more than a year to be sold because most of these assets are not readily liquid. Therefore, these assets are said to bring value over a period that is generally longer than one year. Non-current assets include real estate, machinery, vehicles, furniture, etc, and nonphysical assets such as copyrights, goodwill, patents, trademarks, etc.

What are liabilities?

In accounting, liabilities are the financial obligations or debts of a company. They are the claim on a company’s assets by creditors that represent an obligation to make payments to these creditors in the future either as goods, cash, or services. These creditors could be the company’s clients, partners, institutions, service providers, or investors. In simple terms, it is anything you owe or have borrowed.

Just like assets, individuals, corporate entities, states, and countries can have liabilities. Corporate entities record their liabilities on the right-hand side of the balance sheet.

Liabilities are the difference between a company’s assets and equity. The working capital available to the company is the difference between its current assets and liabilities.

Types of liabilities

- Short-term liabilities

- Contingent liabilities

- Long-term liabilities

Short-term liabilities

Short-term liabilities are liabilities that must be settled within a fiscal year, these are also known as current liabilities and consist of accounts payable, recurring operational costs like electricity, utility, and wages, short-term debt repayment, notes payable, and taxes. Short-term liabilities are usually settled using current assets. The accounts payable is any amount that has to be paid for goods or services that have been offered to the company and is mostly paid within a month.

Contingent liabilities

Contingent liabilities are obligations that may result due to the outcome of a future event such as honoring product warranties or pending lawsuits.

Long-term liabilities

These are liabilities whose repayment period is more than one fiscal year, meaning that they can be paid off in years to come. They are also known as non-current liabilities. Long-term liabilities include deferred taxes, mortgages, debentures, bonds payable, retirement payments, etc.

See also: Common stock – asset or liability?

What is equity?

Equity refers to the amount remaining in an event where an individual or organization liquidates all its assets to settle its liabilities. It is also the amount that shareholders of a company may get paid in exchange for their investment thus, it is also referred to as shareholders’ equity. Equity is additionally referred to as net assets or net worth.

Equity comprises share capital, paid-in capital, and retained earnings. Share capital is the amount a company gets from the sale of common and preferred stocks. Paid-in capital is the capital obtained from the sale of shares that is above their par value. Retained earnings comprise all the company’s income earned through the sale of products or rendering of services.

Equity is a combination of all monies directly invested into the company by its founders, the company’s income since its inception, reinvested income, and income from equity shares. Investors who own the shares of a company known as dividend shares receive a return on their equity in the form of dividend payment.

See also: What is negative equity?

Assets, liabilities, equity and the accounting equation

The accounting equation comprises assets, liabilities, and equity. It represents a company’s finances at a glance; showing the amount that assets, liabilities, and equity each have. Accountants of a company use the accounting equation when completing a company’s balance sheet, this is done because it is important that a company’s assets, liabilities, and equity align.

The accounting equation shows the relationship between a company’s assets, liabilities, and equity and is expressed as Assets = Liabilities + Equity

In order for a company’s accounts to balance, its assets are supposed to be equal to the sum of its liabilities and equity as shown by the equation above. If this is not so, it means the company’s balance sheet is not balanced. When this happens, it shows that the company does not have a good financial standing, it is, therefore, important to check the calculation done and ensure that everything balances.

For instance, if a fast food chain such as MacDonald’s has 90 billion in assets, then the sum of their liabilities and equity should also be 90 billion in order for their account to balance out. The need for MacDonald’s assets to be equal to its liabilities and equity is because everything it owns has a source which could be the company founders, investors, or creditors. This means that every dollar of the business can be classified as either assets, liabilities, or equity.

The accounting equation is important in order to run a financially stable company since it is a foundational component of ensuring that you have an accurate balance sheet that shows you your assets, liabilities, and equity at a glance.

Furthermore, the accounting equation may be alternated to either calculate a company’s liabilities or equity. When calculating liabilities, it is expressed as Liabilities = Assets – Equity. When calculating equity, it is expressed as Equity = Assets – Liabilities.

Calculating assets, liabilities, and equity

Example 1

For instance, If a publishing company has $5 million in current assets and $30 million in long-term assets. It realized an income of $13 million from the sale of common shares and $5 million from the sale of preferred shares. If its short-term liabilities amount to $6 million and its long-term liabilities are $11 million. We can use the information given to find out the total assets, liabilities, and equity of the company.

Calculating assets

From our earlier discussion on assets, we know that a company’s total assets comprise its current and long-term assets. We can express this as, Total assets = Current assets + Long-term assets. Therefore we can use the values given above to calculate the assets of the publishing company.

Current assets = $5 million

Long-term assets = $30 million

Total assets = $5 million + $30 million

Total assets = $35 million

Calculating liabilities

When we discussed liabilities, we saw that a company’s liabilities are the sum of its long-term and short-term liabilities. We can express this as Total liabilities = Short-term liabilities + Long-term liabilities

From the information given earlier, Short-term liabilities = $6 million

Long-term liabilities = $11 million

Total liabilities = $6 million + $11 million

Total liabilities = $17 million

Calculating equity

In order to find out the publishing company’s equity, we will add the income realized from its sales of common stock and preferred stock. This can be expressed as Equity = Income from the sale of common stock + Income from the sale of preferred stock

Income from the sale of common stock = $13 million

Income from the sale of preferred stock = $5 million

Equity = $13 million + $5 million

Equity = $18 million

Balancing assets, liabilities, and equity

Now that we know the publishing company’s assets, liabilities, and equity, we can use the accounting equation to find out if the company’s finances are balanced.

Assets = Liabilities + Equity

Assets = $35 million

Liabilities = $17 million

Equity = $18 million

Inputting the values into the accounting equation

$35 million = $17 million + $18 million

$35 million = $35 million

From this calculation, we can deduce that the publishing company has a good financial standing since its assets are equal to the sum of its liabilities and equity.

Example 2

Assuming Mark owns a recording studio that has the information in the table below and he wants to know if his studio’s books of account will balance.

| Item | Amount |

|---|---|

| Cash | $500,000 |

| Accounts receivable | $200,000 |

| Studio land and building | $15,000,000 |

| Furniture and equipment | $5,000,000 |

| Employee wages | $600,000 |

| The loan from the bank | $8,000,000 |

| Utilities | $600,000 |

| Marks investment in the studio | $10,000,000 |

| Money from Mark’s family | $1,500,000 |

With the information above, we can calculate Mark’s assets, liabilities, and equity which will in turn help us understand if the studio’s books of account will balance.

Calculating assets

Assets comprise cash, accounts receivable, and fixed assets such as land, building, furniture, and equipment. Therefore, in order to know Mark’s total assets, we will sum all these together.

Cash = $500,000

Accounts receivable = $200,000

Land and building = $15,000,000

Furniture and equipment = $5,000,000

Total assets = Cash + Accounts receivable + Land and building + Furniture and equipment

Total assets = $500,000 + $200,000 + $15,000,000 + $5,000,000

Total assets = $20,7000,000

Calculating liabilities

The studio’s liabilities are the wages paid to employees, the loan from the bank, and money spent on utilities. We shall sum them up to get the total liabilities of the studio.

Employee wages = $600,000

Loan from bank = $8,000,000

Utilities = $600,000

Total liabilities = Employee wages + Loan from bank + Utilities

Total liabilities = $600,000 + $8,000,000 + $600,000

Total liabilities = $9,200,000

Calculating equity

The equity comprises the money which Mark invested as well as that which was invested into the business by his family.

Marks investment in the studio = $10,000,000

Money from Mark’s family = $1,500,000

Total equity = Mark’s investment in the studio + Money from Mark’s family

Total equity = $10,000,000 + $1,500,000

Total equity = $11,500,000

Balancing assets, liabilities, and equity

So far, we have calculated the assets, liabilities, and equity of Mark’s studio. Now, we shall input all the values in the accounting equation in order to gauge if the studio’s finances are stable and if its books of account are balanced.

Assets = Liabilitie + Equity

Assets = $20,7000,000

Liabilities = $9,200,000

Equity = $11,500,000

$20,7000,000 = $9,200,000 + $11,500,000

$20,7000,000 = $20,7000,000

From the calculation of the studio’s assets, liabilities and equity, we can conclude that the studio has a good financial standing and its books of accounts are balanced since its assets are equal to the sum of its liabilities and equity.

Assets, liabilities, equity: differences and similarities

So far, we have seen that assets, liabilities, and equity are important parts of the balance sheets and very useful in understanding a company’s financial standing. However, there are some intrinsic differences between these three accounting equation components which we shall look at below

Similarities between assets, liabilities, and equity

- Assets, liabilities, and equity are all part of a company’s balance sheet.

- They are all useful components that aid in understanding the financial stability of a company.

Differences between assets, liabilities, and equity

- Assets are sources of present or future income for the company. Liabilities are what the company owes and needs to pay back either within a short or long period. Equity is mainly investors’ contributions to the company.

- A company’s assets are liable to wear and tear, this leads to a depreciation in their value and lifespan over the years. Liabilities do not depreciate in value or lifespan, instead, they can reduce when the company pays them off. Equity remains constant especially that gotten from the sales of the company shares. It can only get reduced when it is used to finance the company’s projects or other kinds of reinvestments.

- Assets are mainly acquired by companies with the aim of growing the business. Liabilities are taken in order to aid in the acquisition of more assets with the hope of these assets netting in enough income to take care of the liabilities in the future. Equity is a source of financing for the company.

- Assets are a means of increasing cash inflow since they are resources of economic value that can generate income. Liabilities increase cash outflows since they are obligations that have to be repaid. Equity adds to the company’s cash inflow.

- Assets comprise current and long-term assets. Liabilities consist of short-term and long-term liabilities. Equity comprises shareholder equity and retained earnings.

- When there is an increase in the company’s assets, it will be debited from the asset side of the balance sheet. When there is an increase in a company’s liabilities or equity, it would be credited to the liabilities or equity side of the balance sheet.

- When there is a decrease in the company’s assets, it will be credited from the asset side of the balance sheet. When there is an increase in liabilities or equity, it will be debited from the liabilities or equity side of the balance sheet.

Assets, liabilities, equity: tabular comparison

Within the table below, we shall outline the differences between assets, liabilities, and equity.

| Comparison criteria | Assets | Liabilities | Equity |

|---|---|---|---|

| Meaning | Assets are resources that are expected to bring future economic benefits to their owners usually by reducing the owner’s cash outflow while increasing cash inflow. | Liabilities are the financial obligations or debts of a company. | Equity is a combination of all monies directly invested into the company by its founders, the company’s income since its inception, reinvested income, and income from the sale of shares |

| Components | Current and long-term assets | Short-term and long-term liabilities | Share capital, paid-in capital, and retained earnings |

| Cash flow | Increases inflow and reduces cash outflows | Increases cash outflows | Increases cash inflow |

| Depreciation | Depreciates with time | Does not depreciate | Does not depreciate |

| Equation | Assets = Liabilities + Equity | Liabilities = Assets – Equity | Equity = Assets – Liabilities |

| Position in the balance sheet | Placed on the left-hand side traditionally. It comes first in recent balance sheets. | Placed on the right-hand side traditionally. It comes after assets in recent balance sheets. | Placed on the right-hand side traditionally. It comes after liabilities in recent balance sheets. |

| Impact | Contributes to the company’s growth | Could finance projects or purchase assets | Useful in business expansions and reinvestment |

| Increase in account | When there is an increase in assets, the assets account will be debited | When there is an increase in liabilities, the liabilities account will be credited | When there is an increase in equity, the equity account will be credited |

| Decrease in account | When there is a decrease in assets, the assets account will be credited | When there is a decrease in liabilities, the liabilities account will be debited | When there is a decrease in equity, the equity account will be debited |

Conclusion

Looking at assets, liabilities, and equity, we have seen what each of these terms means, their components, similarities, and differences. Assets are resources owned by the company. Liabilities are what the company owes. Equity is what the company owners have invested in it. We have also seen practical examples of how the accounting equation is used in checking if a company’s assets are the same as the sum of its liabilities and equity.

A company’s assets, liabilities, and equity are important components in its books of account or balance sheet. The accounting equation helps to simplify the relationship between these three terms as it is fundamental in keeping a record of the company’s finances. The equation uses the double entry accounting system principle whereby every financial transaction undertaken by the company has an equal and opposite effect. Hence in order for a company’s books of account to balance, its total assets must be equal to the sum of its liabilities and equity.

Ensuring that a company’s balance sheet is balanced is key irrespective of the company’s size or period of operation as it shows the financial stability of the company. Investors who want to invest in a company also find it useful to look at its balance sheet to see the relationship between its assets, liabilities, and equity. This is because companies with a high amount of liabilities especially liabilities which do not add to the company’s growth or successes are considered risky investments. Another aspect that may indicate the poor financial standing of a company is when its balance sheet is not balanced, this means that the company’s total assets when calculated do not equal the sum of its liabilities and equity.

Video on: the differences between assets, liabilities, equity and their meaning

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.