I will cover in detail how to build a cash flow statement from a balance sheet and an income statement using the indirect method, it is one of the common accounting questions often asked at job interviews and accounting examinations. You really need to take your time to follow it to understand this topic clearly, I take it step by step so that you have a better grasp of the topic.

A cash flow statement is one of the most important financial statements for a business. It shows how much cash is coming in and going out of the business, and thus provides insight into the company’s liquidity and its ability to pay bills and make profits.

The balance sheet shows all of the company’s assets and liabilities as well as the shareholders’ equity, while the income statement shows all of the company’s revenues and expenses.

What is a cash flow statement?

The cash flow statement is a financial statement that provides information about a company’s cash inflows and outflows over a given period of time. It is divided into three sections: operating activities, investing activities, and financing activities.

Before we begin making a cash flow statement from balance sheet and income statement, take note of these tips, they are very important. I will list them and then explain more about them.

Examples would be given as each point is explained, after that, we take an example of a comparative balance sheet and an income statement and then use these financial statements to create a statement of cash flows.

Important points to note when building cash flow statement from balance sheet and income statement

- Take note of the negative and positive signs

- Understand that in a cash flow statement, we are only interested in the movement of cash, that is, cash inflow and cash outflow.

- Adjustments must be made to cancel the effect of non cash transactions that were used to calculate the net profit.

Examples and calculations would be shown while explaining the above points; after that, we will pick 1 question and use it to make a cash flow statement from a balance sheet and income statement.

Understanding the importance of cash and cash equivalents in preparing a cash flow statement from the balance sheet and an income statement

Cash and cash equivalents are the most important items of the cash flow statement because whatever you are calculating and recording in the statement of cash flows is simply the movements in the Cash and cash equivalents occurring during the fiscal year or during the reporting period.

Cash equivalents can be defined as assets that can easily be converted to cash within 6 months.

What are examples of cash equivalents?

A good example of a cash equivalent is cash in the bank account. Other examples of cash equivalents include short-term investments such as short-term treasury bills or investments in buying shares of another company.

This shows that after preparing your cash flow statement using the balance sheet and income statement, the net change in Cash and cash equivalents for the current reporting period should be equal to the difference between the Cash and cash equivalents of the previous reporting period and the current reporting period; if they are not equal, then it shows you have prepared your cash flow statement wrongly.

Therefore, the Cash and cash equivalents help in the substantiation of the statement of cash flows to prove that it was prepared correctly.

Having known the importance of the Cash and cash equivalents, it is necessary to calculate the net increase or decrease in the Cash and cash equivalents even before building the cash flow statement from the balance sheet.

Example of how to calculate the net increase or decrease in cash and cash equivalents

Below is an excerpt from a comparative balance sheet showing the cash and cash equivalents, use it to calculate the net increase or decrease in Cash and cash equivalents.

| 2019 | 2020 | |

|---|---|---|

| Short term investments | 10 | 40 |

| Cash in hand | 60 | 90 |

| Cash in the bank | 40 | 30 |

From the table above, the total Cash and cash equivalents for the fiscal year 2019 is 10+60+40 = 110 whereas the total Cash and cash equivalents for the fiscal year 2020 is 40+90+30 = 160

This example shows that as the company moves from one year to another, there is an increase in the cash and cash equivalents from 110 to 160. It means there is a net increase of +50 of the cash and cash equivalents. If there was a decrease in the cash and cash equivalents as we move to this current year, it means cash is being spent, this would have been negative. So it is important that you specify the negative and positive signs.

Example 2

Below is an excerpt from a comparative balance sheet showing the cash and cash equivalents, use it to calculate the net increase or decrease in Cash and cash equivalents.

| Current Assets | 2019 | 2020 |

|---|---|---|

| Short term investments | 10 | 40 |

| Cash in hand | 40 | 30 |

| Cash in the bank | 60 | – |

| Current Liabilities | ||

| Trade Payables | – | – |

| Bank | – | 10 |

The above table has cash and cash equivalents listed under the liabilities section. What you will do when there is a cash and cash equivalent under the liability section is to subtract any liability that is a cash and cash equivalent from the current assets that are part of the cash and cash equivalents.

In the above example, the cash and cash equivalents is a bank draft of $10. This means our net change in cash and cash equivalents would be calculated as 10+40+60 = 110 – (40+30) – 10 (from the liability section); this gives net cash and cash equivalents of +30.

Once you know how to calculate the net increase or decrease of the cash and cash equivalents; you can begin calculating the values for all the 3 major sections of the cash flow statement (i.e, cash flows from operations, investing and financing).

Building a cash flow statement from balance sheet

The statement of cash flows prepared using the indirect method adjusts net income for the changes in balance sheet accounts to calculate the cash from operating activities. In other words, changes in asset and liability accounts that affect cash balances throughout the year are added to or subtracted from net income at the end of the period to arrive at the operating cash flow.

In order to build a cash flow statement from balance sheet and income statement, you will need the following: a copy of the company’s balance sheet for two accounting periods (previous year and current year) and a copy of the company’s income statement for the current accounting period. Additional information may have to be given to have a complete picture.

The balance sheet shows the financial position at a point in time, hence, you need the previous accounting date and the current accounting date in order to determine the changes that have occurred over this period (this means you need the comparative balance sheet of the previous fiscal year and the current fiscal year). Once you have these financial statements, you can begin building your cash flow statement from scratch.

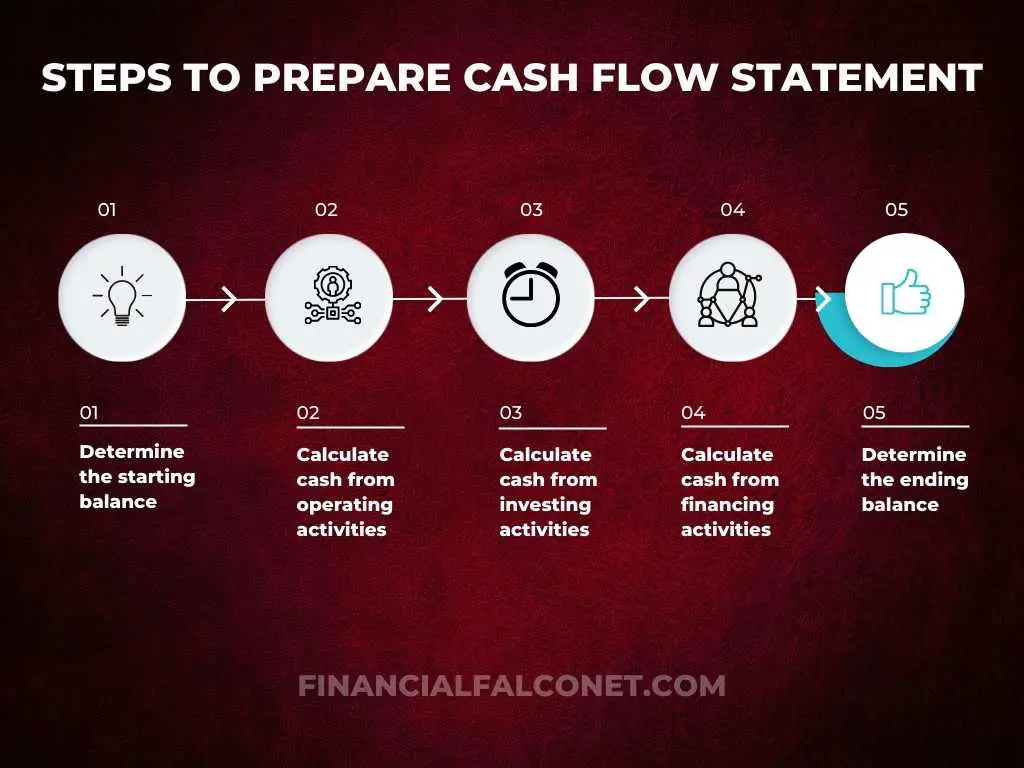

Steps on how to prepare cash flow statement from balance sheet

- Find the net income or net profit from the profit and loss statement

- Make adjustments for non cash transactions

- Calculate the changes in working capital

- Calculate the cash flows from investing activities

- Calculate the cash flows from financing activities

Find the net income or net profit from the profit and loss statement

The net profit is easy to find on the income statement, it is located at the bottom. In some cases, the examiner may not give you the net income directly; the profit after tax may just be what will be given.

If you are given profit after tax in a job interview question or in an exam, you must look for the tax expense from the income statement and add it back to the profit after tax in order to get the profit before tax. This is important due to the fact that tax expense is regarded as a non cash transaction because companies record the tax expense while preparing an income statement but that does not necessarily mean that the actual cash has been paid to the government agency in charge of tax (IRS); it may be paid at a later date, hence, tax expense is not regarded as a cash transaction in preparing a cash flow statement.

Make adjustments for non-cash transactions

Please note that the statement of cash flows deals only with transactions that are paid with cash or cash equivalents. It doesn’t record transactions purchased on credit. This is important to note because whatever we are going to use from the balance sheet and income statement must be cash transactions. Any non-cash transaction from the income statement must be subtracted from the net income or added to the net income, depending on whether the non-cash transaction was an expense or gain.

The net income used in building the cash flow statement from the balance sheet is gotten from the income statement, but you have to understand that such net income is derived by calculating the difference between the Total Revenues and the Total Expenses (i.e Total Revenues – Total Expenses). This means the total revenue also includes both cash and non-cash revenues; the same applies to the total expenses – it also includes both cash and non-cash expenses.

Since the statement of cash flows is only concerned with the cash movements, it means starting the cash flow statement with the net income will require you to remove the effects or impact of the non-cash transactions associated with the net income. I will give some examples of how you can make these non-cash adjustments to the net income below.

How to make adjustments for non cash transactions

If a non cash transaction was added when calculating the net income on the income statement, then it will be subtracted from the net income on the cash flow statement when using the indirect method. But if a non cash transaction was subtracted when calculating the net income on the income statement, then it will be added to the net income on the cash flow statement when using the indirect method. These 2 rules are very important when preparing a cash flow statement from a balance sheet and income statement.

First, we add back the depreciation. Please note that you will only add back depreciation if it was used to calculate the net profit of the income statement.

Example: making adjustments for depreciation

For example, you purchased a machine for $600; we need to calculate the depreciation. Before calculating the depreciation, you have to give it an estimated useful life.

So let’s assume you gave it an estimated useful life of 10 years. Your depreciation would now be calculated using the formula: (purchased price/estimated useful life); this gives a depreciation of 600/10 = $60. What this means is that every year, you will deduct $60 from the Selling, General and Administrative (SGA) expenses section of the balance sheet.

Assuming you used the machine for 4 years, at the end of the fourth year, the accumulated depreciation would be 4X60 = $240. This means your net book value at the end of the 4th year would be 600 – 240 = $360; that means the net book value is the value of an asset that remains after it has been depreciated.

You have to remember that our net book value was calculated from an estimated useful life, which means at the end of the 4th year, the true value of our machine may be more than the net book value, it may be less, or equal.

Now, since you used the estimated useful life in calculating the depreciation and also deducting the depreciation in order to arrive at the net income; what this means is that you didn’t actually pay any cash as depreciation, it was just an estimate; and because it is an estimate, the IAS 7 guideline for preparing a statement of cash flows does not permit it to be included in the cash flow statement; therefore, its effect has to be canceled and because you deducted it in order to arrive at the net income, we have to add it back to the net income when using the indirect method of preparing a cash flow statement from the balance sheet and income statement.

Still on the machine, assuming you sell it at the end of the 4th year for $400, it means you have made a profit of 400 – 360 = $40 (that is, selling price – estimated value). You see, this $40 cannot be recorded in the cash flow statement because it was derived using an estimate from a non cash transaction.

Other non-cash transactions are adjusted in the same way that depreciation is adjusted when building a cash flow statement using the indirect method. That means if one noncash transaction was added to the items on the balance sheet in order to arrive at the net income, such a transaction must be subtracted from the net income when preparing a cash flow statement using the indirect method.

If another noncash transaction was subtracted from the items on the profit and loss statement in order to arrive at the net income, the transaction must be added to the net income when preparing a cash flow statement (this is done in order the cancel the effects of the non cash transactions.

Making adjustment for profit on sale of a non current asset

If there is a profit on the sale of a noncurrent asset that has been added to “Other income” and therefore used in arriving at the net income, then you have to subtract it from the net income while preparing your cash flow statement using the indirect method.

Making adjustment for loss on sale of a non current asset

But, if there is a loss on the sale of a non-current asset that has been subtracted from “Other income” and therefore used in arriving at the net income on the income statement, then you have to add it back to the net income on your cash flow statement while preparing it using the indirect method.

Remember, these adjustments are made because we are only interested in cash transactions in a statement of cash flows.

Calculate the changes in working capital

The working capital includes transactions affecting inventories, cash receivables, and cash payables. Cash and cash equivalents are part of the working capital, but since the whole essence of a cash flow statement is to show the inflow and outflow of cash and cash equivalents, it is not included under this section of the cash flow statement.

Negative and positive signs before the values in your cash flow statement are very important because they show the movement of cash. An outflow of cash is a reduction in your cash whereas an inflow of cash is an increase of cash. This rule is very important in recording your transactions.

Please note also that the cash flow statement does not care about the ITEMS being transacted but ONLY the CASH; so always ask yourself in any transaction whether it is causing a reduction in cash (outflow) or an increase in cash (inflow) and then use the appropriate sign needed. Examples of the use of these cash movements and the positive and negative signs are shown in calculating the working capital changes below.

Inventories

Inventories are found on the balance sheet. To calculate the changes in the inventories, you check if there is an increase or decrease in inventories from the previous reporting period to this current reporting period.

An increase in inventories as you move from the previous accounting period to the current accounting period means you spent more cash in order to add the inventories; this means your cash is reduced (outflow of cash) in order to buy more inventories. On your cash flow statement, it is indicated as “Increase in inventories” with a negative sign.

A decrease in inventories as you move from the previous accounting period to the current accounting period means you sold out your products, leading to a reduction in the inventories; this means your cash is increased (inflow of cash). On your cash flow statement, it is indicated as “Decrease in inventories” with a positive sign.

Example 1:

| January 2022 | January 2023 | |

|---|---|---|

| Inventories | $40 | $60 |

From the table above, we can see that there is an increase in inventories from $40 to $60. This means there is an outflow of cash (that is, cash is spent in order to buy more inventories). The cash flow statement would look like the sample below:

| Cash Flows from Operating activities | |

| Profit before tax | XYZ |

| Adjustment for: | |

| Depreciation | X2Y |

| Loss on sale of a non current asset | -1X2Y |

| Profit on sale of a non current asset | XY |

| Increase in Inventories | -20 |

Example 2:

| January 2022 | January 2023 | |

|---|---|---|

| Inventories | $60 | $40 |

From the table above, we can see that there is a decrease in inventories from $60 to $40. This means there is an inflow of cash (that is, cash is earned as products are being sold leading to a decrease in inventories). The cash flow statement would look like the sample below:

| Cash Flows from Operating activities | |

| Profit before tax | XYZ |

| Adjustment for: | |

| Depreciation | X2Y |

| Loss on sale of a non current asset | -1X2Y |

| Profit on sale of a non current asset | XY |

| Decrease in Inventories | 20 |

Account receivables

Account receivable is an account that records your money that is yet to be paid by customers.

An increase in account receivables means more of your money is in the hands of customers which is a reduction of the cash available to you. On your cash flow statement, it is indicated as “Increase in receivables” with a negative sign.

A decrease in account receivables means some customers paid the money they owed you which means you had more cash (your cash is increased or there is an inflow of cash). On your cash flow statement, it is indicated as “Decrease in receivables” with a positive sign.

Example

| January 2022 | January 2023 | |

|---|---|---|

| Receivables | $40 | $60 |

From the table above, we can see that there is an increase in receivables from $40 to $60. This means there is a reduction in your cash because more people owed you money. The cash flow statement would look like the sample below:

| $ | |

| Cash Flows from Operating activities | |

| Working capital changes | |

| Decrease in inventories | 20 |

| Increase in inventroies | -20 |

| Increase in trade receivables | -20 |

| Decrease in trade receivables | 20 |

PLEASE NOTE: I have shown both the increase and decrease in the cash flow statement just for the purpose of illustration; when preparing your cash flow statement just indicate only the type of changes occurring; that is, if it is an increase, only indicate the increase (don’t add an extra row for the decrease when the change occurring from one reporting period to the current is only an increase.) – the same applies with gain or loss on sales.

Accounts payable

Accounts payable is an account on the balance sheet that records the money you owed your suppliers. An increase in accounts payable means you have borrowed more from your suppliers which means you now have more cash; this increases cash (inflow of cash). There is an increase in debt we know but we are interested in cash inflow and outflow when it comes to the cash flow statement; so when you borrow from your suppliers, you increase your inflow. On your cash flow statement, it is indicated as “Increase in accounts payable” with a positive sign.

A decrease in accounts payable as you move from the previous accounting period to the current accounting period means you paid back your suppliers, which will cause a decrease in cash (outflow of cash). On your cash flow statement, it is indicated as “Decrease in accounts payable” with a negative sign.

Example

| January 2022 | January 2023 | |

|---|---|---|

| Accounts payable | $40 | $60 |

From the table above, we can see that there is an increase in accounts payable from $40 to $60. This means there is an inflow of cash (that is, cash is increased as you borrow more from suppliers). The cash flow statement would look like the sample below:

| $ | |

| Cash Flows from Operating activities | |

| Working capital changes | |

| Decrease in inventories | 20 |

| Increase in inventroies | -20 |

| Increase in trade receivables | -20 |

| Decrease in trade receivables | 20 |

| Increase in accounts payable | 20 |

| Decrease in accounts payable | -20 |

The last items to be added to the cash flows from operating activities are the tax paid and interest paid. These are all outflows of cash and are therefore negative.

You can now add up all the cash inflow and outflow arising from the operating activities to arrive at the net value known as the Net cash from operating activities.

Our cash flow statement from the balance sheet and income statement will now look like the sample below:

| $ | |

| Cash Flows from Operating activities | |

| Profit before tax | |

| Adjustment for: | |

| Depreciation | |

| Loss on sale of a non current asset | |

| Profit on sale of a non current asset | |

| Decrease in inventories | 20 |

| Increase in inventroies | -20 |

| Increase in trade receivables | -20 |

| Decrease in trade receivables | 20 |

| Increase in accounts payable | 20 |

| Decrease in accounts payable | -20 |

| Interest paid | |

| Income taxes paid | |

| Net cash from operating activities |

According to the IAS 7 guidelines, Dividends paid can appear under the operating section or financing section, but must only appear once in a cash flow statement.

Calculate the cash flows from investing activities

Calculating and recording cash transactions involving investing activities is easier compared to operating activities. This is because the investing activities involve 2 major things: the purchase and sale of non current assets.

In the investing activities and the financing activities, there is no difference when using the direct and indirect methods of preparing a cash flow statement from the balance sheet and income statement; their difference is in the operating activities.

The purchase of any non current asset means cash is reduced while proceeds from the sale of non current assets mean cash is increased. Therefore, any purchase is a reduction to cash and would be recorded on the cash flow statement with a negative sign; whereas proceeds from the sale of non current assets would be recorded with a positive sign because it is a cash inflow.

Noncurrent assets are assets that cannot be converted to cash within 1 year.; they are usually long-term investments. Examples of non current assets are property, plant, and equipment (PPE). Other examples of non current assets are mutual funds, commercial paper, long-term government bonds, and long term stocks, notes, etc.

Also, proceeds received from long-term investments from other companies are also included in this section.

Calculate the cash flows from financing activities

Financing activities involve sources of funding for a business or paying back loans or paying out dividends.

Any source of funding that increases the cash of the business is an inflow and would be recorded on the cash flow statement with a positive sign.

Paying back loans or any repayment of debt will cause a decrease in cash and therefore is represented on the cash flow statement as a negative sign.

Examples include the issuance of shares would increase the cash and therefore would be positive whereas the buyback of shares (treasury stock) reduces cash (it is a cash outflow) and therefore will be indicated with a negative sign.

The total of both the positive and negative changes in cash arising from the financing activities gives the Net cash flows from financing activities.

Calculate the TOTAL of the changes in the operating, investing, and financing activities

We are almost done building a cash flow statement from balance sheet and income statement. What remains now is to calculate the net effect of all the 3 sections; that is, the addition of the (Net cash from operating activities) + (Net cash from investing activities) + (Net cash from financing activities). The summation of the 3 sections of the cash flow statement gives the net.

It is important to know that any positive or negative sign of the Net cash from operating activities, Net cash from investing activities, and the Net cash from financing activities must be taken into consideration; and if their net effect is positive, then it is recorded as Net increase in cash and cash equivalents but when their net calculation gives a negative value, then it is recorded as Net decrease in cash and cash equivalents.

Finally, we will conclude the building of our cash flow statement from balance sheet and income statement by recording the cash and cash equivalents at the beginning of the period as well as the cash and cash equivalents at the end of the period.

Example and Calculation

Below is the Comparative Balance sheet and Income statement of Financial Falconet with additional information provided. Use the information given to prepare a cash flow statement for Financial Falconet.

| REVENUE | 60,000 |

| Cost of Sales | -17,500 |

| GROSS PROFIT | 42,500 |

| General and Admin Expenses | -13,200 |

| Selling and Marketing Expenses | -18,000 |

| Depreciation and Amortisation | -850 |

| OPERATING PROFIT | 10,450 |

| Interest Expense | -50 |

| Tax Expense | -750 |

| NET PROFIT | 9,650 |

| Comparative Balance Sheet ACCOUNT | January 2022 | January 2023 |

|---|---|---|

| Cash | 17,000 | 13,895 |

| Accounts receivable | 12,500 | 7,850 |

| Other receivables | 550 | 500 |

| Prepaid Expenses | 1,000 | 500 |

| Property, Plant and Equipment | 4,000 | 3,750 |

| Intangible Assets | 1,300 | 1,500 |

| TOTAL ASSETS | 36,350 | 27,995 |

| Accounts Payable | 8,125 | 10,000 |

| Taxes Payable | 3,200 | 2,800 |

| Accrued Expenses | 75 | 50 |

| Deferred Revenue | 3,000 | 2,000 |

| Long Term Loans | 1,200 | 1,100 |

| Capital Contributions | 1,050 | 1,000 |

| Retained Earnings | 19,700 | 11,045 |

| TOTAL LIABILITIES AND EQUITY | 36,350 | 27,995 |

Additional Information

| SALE OF FURNITURE | |

| Original Cost | 20 |

| Accumulated Depreciation | 5 |

| Sale Price | 10 |

| PURCHASED OF NON-CURRENT ASSET | |

| Computer Equipment | 910 |

| RAISING/REPAYING FUNDS | |

| Long Term Debt Raised | 100 |

| Long Term Debt Repayment | – |

| Common Stock Issued | 50 |

| Dividends Paid | 1,000 |

From the above information, we will create a cash flow statement from the comparative balance sheet and the income statement.

Step 1: Find the net profit from the income statement

We begin creating the cash flow statement using the indirect method by finding the net income (or the net profit); this is found on the last line of the income statement, hence the net profit is also known as the “Bottom line“. From our income statement, the net profit is 9,650.

Our basic cash flow statement will now look like the sample below:

| CASH FLOW FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| CASH FLOW FROM INVESTING ACTIVITIES | |

| CASH FLOW FROM FINANCING ACTIVITIES |

Step 2: Find the cash and cash equivalent at the beginning and end of the reporting period

As earlier stated, before creating the cash flow statement, check for the opening and closing balance of the cash and cash equivalents from the comparative balance sheet.

The cash and cash equivalent for the beginning of this current reporting period will be the cash balance at the end of the previous reporting period. In this case, it is 13,895; while the closing balance for cash will be the cash balance of this current reporting period, which is 17,000. The difference between the opening and closing cash balances gives 3,105(which is positive, and forms the NET INCREASE IN CASH).

One thing to note is that the difference between the cash and cash equivalent at the beginning and the end should be equal to our net cash and cash equivalent when we finish preparing our cash flow statement, if not, then we are wrong.

Since we have our opening and closing cash balance, let us include it in the cash flow statement that we are building from balance sheet and income statement.

| CASH FLOW FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| CASH FLOW FROM INVESTING ACTIVITIES | |

| CASH FLOW FROM FINANCING ACTIVITIES | |

| Beginning Cash Balance | 13,895 |

| Ending Cash Balance | 17,000 |

| NET INCREASE IN CASH | 3,105 |

Step 3: Make adjustments for non cash transactions

We now make adjustment for non cash transactions. We have stated the common examples of non-cash transactions such as depreciation, loss on sale of a non current asset, profit on the sale of a non current asset, etc.

In this example, our depreciation is 850.

There was a sale of furniture that was given in the additional information; we have to calculate the loss or profit on it.

Purchased price = $20

Accumulated depreciation = $5

Carrying value will be 20 – 5 = $15

Selling price = $10

Since the accountant expected the furniture to be $15, according to the carrying value but ended up selling it at $10, then there is a loss of 15 – 10 = $5.

This loss of $5 was charged to the general and admin expenses and since it contributed to the calculation of the net income, we have to cancel its effect on the net income because it was not a cash transaction; to do this, we add it back.

Therefore, the depreciation of $850 and loss on sale of furniture of $5 would be added back in order to adjust for these 2 non cash transactions.

This is shown on the cash flow statement below:

| CASH FLOW FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| Adjustment for: | |

| Depreciation and Amortisation | 850 |

| Loss on Sale of Non Current Asset | 5 |

| CASH FLOW FROM INVESTING ACTIVITIES | |

| CASH FLOW FROM FINANCING ACTIVITIES | |

| Beginning Cash Balance | 13,895 |

| Ending Cash Balance | 17,000 |

| NET INCREASE IN CASH | 3,105 |

Step 4: Make adjustments for movement in working capital

The working capital is the difference between the current assets and current liabilities.

Current assets can be defined as items that can easily be converted to cash within a short period of time, typically, within a year. Examples of current assets are cash, short term investments, inventories, prepaid expenses, and receivables.

Since our aim is to resolve the cash movements in a statement of cash flows, cash is not included as one of the current assets when calculating the working capital changes.

Current liabilities have to be paid within a year. Examples of current liabilities are payables (accounts payable, taxes payable, etc), accrued expenses, and deferred revenue.

Working Capital Calculations

From the comparative balance sheet given, our current assets (accounts payable, other receivables, and prepaid expenses) for this year add up to 12,500 + 550 + 1,000 = 14,050 while the previous year adds up to 7,850 +500 + 500 = 8,850.

This shows the receivables increased from 8,850 to 14,050; an increment of 14,050 – 8,850 = 5,200; and since there is an increase in receivables, the value becomes negative (-5,200). This has been explained in the preceding section.

From the balance sheet provided, the current liabilities (accounts payable, taxes payable, accrued expenses, and deferred revenue) add up to 8,125 + 3,200 + 75 + 3,000 = 14,400 whereas the previous year’s current liabilities add up to 10,000 + 2,800 + 50 + 2,000 = 14,850.

This shows the payables decreased from 14,850 to 14,400; a reduction 450; and since there is a decrease in payables, the value becomes negative (-450). This also has been explained in the preceding section.

There are no inventories in the balance sheet, this can be included in the cash flow statement (but will be left empty) or you simply omit it.

Let’s include these changes in the working capital in the cash flow statement, as shown below:

Add up everything under the operating activities to arrive at the net change in operating activities. In our example, we are going to add the net profit, adjustment for a non-cash transaction, and working capital changes (including their negative and positive signs): 9,650 + 850 + 5 – 5,200 – 450 = 4,850; this is shown below.

| CASH FLOW FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| Adjustment for: | |

| Depreciation and Amortisation | 850 |

| Loss on Sale of Non Current Asset | 5 |

| Changes in Working Capital | |

| Increase in Receivables | -5,200 |

| Decrease in Payables | -450 |

| NET CASH FLOWS FROM OPERATING ACTIVITIES | 4,855 |

| CASH FLOW FROM INVESTING ACTIVITIES | |

| CASH FLOW FROM FINANCING ACTIVITIES | |

| Beginning Cash Balance | 13,895 |

| Ending Cash Balance | 17,000 |

| NET INCREASE IN CASH | 3,105 |

Step 6: Calculate the cash flows from investing activities

In investing activities, we are dealing with loss or gain from the sale of non current assets. These non current assets include property, plant, and equipment (PPE) as well as long-term investments.

In this example of building a cash flow statement from balance sheet and income statement, we can see there is a purchase of computer equipment for $910 and a sale of furniture for $10.

The purchase is a cash outflow (which will be negative) while the sale of furniture is a cash inflow (which will be positive). We will include this in the cash flow statement as a purchase or proceed on the sale of property, plant and equipment.

The Net cash flows from investing activities would be -910 + 10 = -900

This is shown below:

| CASH FLOW FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| Adjustment for: | |

| Depreciation and Amortisation | 850 |

| Loss on Sale of Non Current Asset | 5 |

| Changes in Working Capital | |

| Increase in Trade Receivables | -5,200 |

| Decrease in Payables | -450 |

| NET CASH FLOWS FROM OPERATING ACTIVITIES | 4,855 |

| CASH FLOW FROM INVESTING ACTIVITIES | |

| Purchase of Property, Plant and Equipment | -910 |

| Proceeds from the Sale of Property, Plant and Equipment | 10 |

| NET CASH FLOWS FROM INVESTING ACTIVITIES | – 900 |

| CASH FLOW FROM FINANCING ACTIVITIES | |

| Beginning Cash Balance | 13,895 |

| Ending Cash Balance | 17,000 |

| NET INCREASE IN CASH | 3,105 |

Step 7: Calculate the cash flows from financing activities

Financing activities involve the raising of funds or repayment of debt. Examples of financing activities include payment of dividends, repaying a loan, issuing of shares, etc.

From the additional information provided in the example, there is:

- a long term debt that was raised of $100; this is a cash inflow, hence it will carry a positive sign

- $50 was realized from the issuance of common stock; this also is a cash inflow and therefore will be a positive value in the cash flow statement

- $1,000 was paid as dividends; this is a cash outflow and would have a negative sign on the cash flow statement.

From the above, the net cash flows from financing activities would be 100 + 50 – 1,000 = -850.

A total of the net cash flows from operating, investing, and financing activities gives 4,855 – 900 – 850 = 3,105 (this is a positive value), hence, there was an increase in cash over the reporting period.

Since this value matches the difference between the balances of the cash and cash equivalent of the opening balance and closing balance, it shows we are correct.

This is shown in the statement of cash flows below:

| Financial Falconet Cash Flow Statement FY January 31 2022 | $ (in thousands) |

|---|---|

| CASH FLOWS FROM OPERATING ACTIVITIES | |

| Net Profit | 9,650 |

| Adjustment for: | |

| Depreciation and Amortisation | 850 |

| Loss on Sale of Non Current Asset | 5 |

| Changes in Working Capital | |

| Increase in Trade Receivables | -5,200 |

| Decrease in Payables | -450 |

| NET CASH FLOWS FROM OPERATING ACTIVITIES | 4,855 |

| CASH FLOWS FROM INVESTING ACTIVITIES | |

| Purchase of Property, Plant and Equipment | -910 |

| Proceeds from Sale of Property, Plant and Equipment | 10 |

| NET CASH FLOWS FROM INVESTING ACTIVITIES | – 900 |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| Long Term Debt | 100 |

| Common Stock Issued | 50 |

| Dividends Paid | -1,000 |

| NET CASH FLOWS FROM FINANCING ACTIVITIES | -850 |

| NET INCREASE IN CASH AND CASH EQUIVALENTS | 3,105 |

| Beginning Cash Balance | 13,895 |

| Ending Cash Balance | 17,000 |

| NET INCREASE IN CASH | 3,105 |

With this, you can now prepare a cash flow statement from balance sheet and income statement when given the necessary information.

Last Updated on November 3, 2023 by Nansel Nanzip Bongdap

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.