A consolidated statement of financial position balance sheet presents the combined balance sheet of a holding or parent company and its subsidiaries as one balance sheet. When a company acquires another company, it can decide to let the company continue operating autonomously, or it could absorb it and control all its operations or have a hybrid of both where it influences some decisions while still letting the company have some level of autonomy.

However, in the case of preparing the balance sheet of a parent company and that of its subsidiaries, there is no middle ground. This is because all parent companies are expected to report their combined assets, liabilities, and equity with that of their subsidiaries as a single entity using the consolidated balance sheet. Public companies that have subsidiaries are expected to make their balance sheet in line with the Financial Accounting Standards Board’s (FASB) Generally Accepted Accounting Principles (GAAP).

Companies that have both local and international subsidiaries must additionally consider the guidelines stipulated by the International Financial Reporting Standards (IFRS) when making a consolidated balance sheet. Some of the guidelines include combining the assets, liabilities, and equity of the parent company with that of its subsidiaries and eliminating intragroup assets, liabilities, and equity in order to mitigate inflating the financial position of the group.

Therefore understanding what a consolidated balance sheet means and how to make one for companies with subsidiaries will go a long way in ensuring that the company’s consolidated balance sheet is not only accurate but also up-to-date and in line with laid down standards. Regardless of a person’s role in a company, whether top management or regular employee and investors seeking companies to invest in, understanding the consolidated balance sheet is a great advantage. Here, we shall discuss what the consolidated balance sheet is as well as the advantages and disadvantages of this statement of financial position. We shall also look at the steps involved in making a consolidated balance sheet.

Read about: Balance sheet substantiation

What is a consolidated statement of financial position?

A consolidated balance sheet is a financial statement of position for a company that has subsidiaries. It is a document that shows the complete financial position of a parent or holding company and all its subsidiaries in a single balance sheet without reporting the balance sheet of the various companies as separate entities. It is also referred to as group accounts.

Companies often use the term, consolidated balance sheet to refer to the aggregated balance sheet of the holding company and all its subsidiaries, but the Financial Accounting Standards Board (FASB) considers a consolidated balance sheet as the balance sheet reporting of a structured entity that has a parent company and subsidiaries.

A consolidated balance sheet is like every other balance sheet due to the fact that it is comprised of three sections which are the assets, liabilities, and equity sections. It is unique from every other balance sheet in the fact that the assets, liabilities, and equity of the parent or holding company and all its subsidiaries are pooled together without distinction and reported as a single entity on one sheet.

A parent or holding company is one that has a controlling interest in another company, meaning that it has control over the composition of the board of directors of a company and has up to fifty-one percent (51%) shareholding in the other company. There are instances where the parent company may own 100% of its subsidiaries. Generally, parent companies have their own business ventures alongside owning other companies (subsidiaries). A holding company, on the other hand, has no business ventures and exists solely for the purpose of overseeing or holding its subsidiaries. A subsidiary company is one whose board of directors is appointed by another company and that company holds at least fifty-one percent (51%) shares of the company.

The consolidated balance sheet is prepared by a company’s accounting department and disclosed by the management team to the company stakeholders and shareholders. It is normally presented as part of the consolidated financial statement of the parent or holding company and its subsidiaries. Inter-company transactions are usually removed from the consolidated balance sheet in order to desist from inflating any account through double counting.

A consolidated balance sheet offers a quick and easy way to examine the financial standing of a parent company and its subsidiaries at a glance and is usually prepared at the end of the accounting year. When the consolidated balance sheet is prepared manually, it is time-consuming and is often riddled with errors, especially for the parent or holding companies that have a considerable number of subsidiaries. In order to save time and minimize errors, there are several softwares that are useful in the preparation of the consolidated balance sheet.

Additionally, a consolidated balance sheet should not be confused with a combined balance sheet. While the former reports the assets, liabilities, and equity of the parent company and its subsidiaries as a single entity, the combined balance sheet reports the assets, liabilities, and equity of the parent company and its subsidiaries as separate entities but in a single document. Hence the former mixes all the assets, liabilities, and equity together to form a new whole while the latter presents each individually but in the same document.

Advantages and disadvantages of using a consolidated balance sheet

When companies use a consolidated balance sheet to report the assets, liabilities, and equity of the parent or holding company and its subsidiaries as a single entity, there are inherent advantages and disadvantages attached to this practice. We shall look at these advantages and disadvantages in the table below and further discuss them later.

| Advantages | Disadvantages |

|---|---|

| Shows assets, liabilities, and equity of the parent company and its subsidiaries at a glance | It might mask companies that are not performing well |

| It aids in promoting transparency | A sector-specific analysis is impossible |

| Gives investors insight into the group of companies | Cross transactions could impact the balance sheet |

| Guides the decisions of management | Takes time and resources |

| Eliminates inflation of accounts | |

| Promotes accountability |

Advantages

- The consolidated balance sheet shows the assets, liabilities, and equity of the parent company and its subsidiaries at a glance.

- It saves time and resources that would have otherwise been spent if the parent company and all its subsidiaries were to prepare individual balance sheets.

- It grants investors and other stakeholders easy access to the financial standing of the parent or holding company and its subsidiaries.

- The consolidated balance sheet aid the company’s management to properly plan ahead and guides them when deciding on the purchase of additional assets and which liabilities to take care of. Hence, it is useful in making informed managerial decisions.

- It aids investors to have an understanding of the overall financial standing of the parent company and its subsidiaries. Thus, it promotes transparency between the company and its investors.

- It aids in promoting transparency and accountability from the company management to stakeholders and shareholders.

- The consolidated balance sheet ensures that there is no double counting which could result in the inflation of accounts through the elimination of cross-sales.

Disadvantages

- The true picture of the financial standing of the parent company and the subsidiaries is not given. This is because the consolidated balance sheet combines all as one entity. It is therefore difficult to pinpoint the companies that are doing well and those that are failing.

- If the cross transactions between the subsidiaries and the parent company are not eliminated, it will present higher assets or liabilities which is inaccurate.

- It takes a lot of time and resources to prepare. This is so because the individual financial transactions of the patent and its subsidiaries have to be compiled and then combined as one.

- Since the assets, liabilities, and equity of the parent company and its subsidiaries are combined as one, it makes it impossible to use the various market prospect ratios in marking sector-specific comparisons and analysis.

Examples of companies with consolidated financial statements

- Alphabet

- Apple

- Amazon

- AmerisourceBergen

- AT&T

- Berkshire Hathaway

- Coca-cola

- Costco

- CVS Health

- Disney

- Exxon Mobil

- General Electric

- IBM

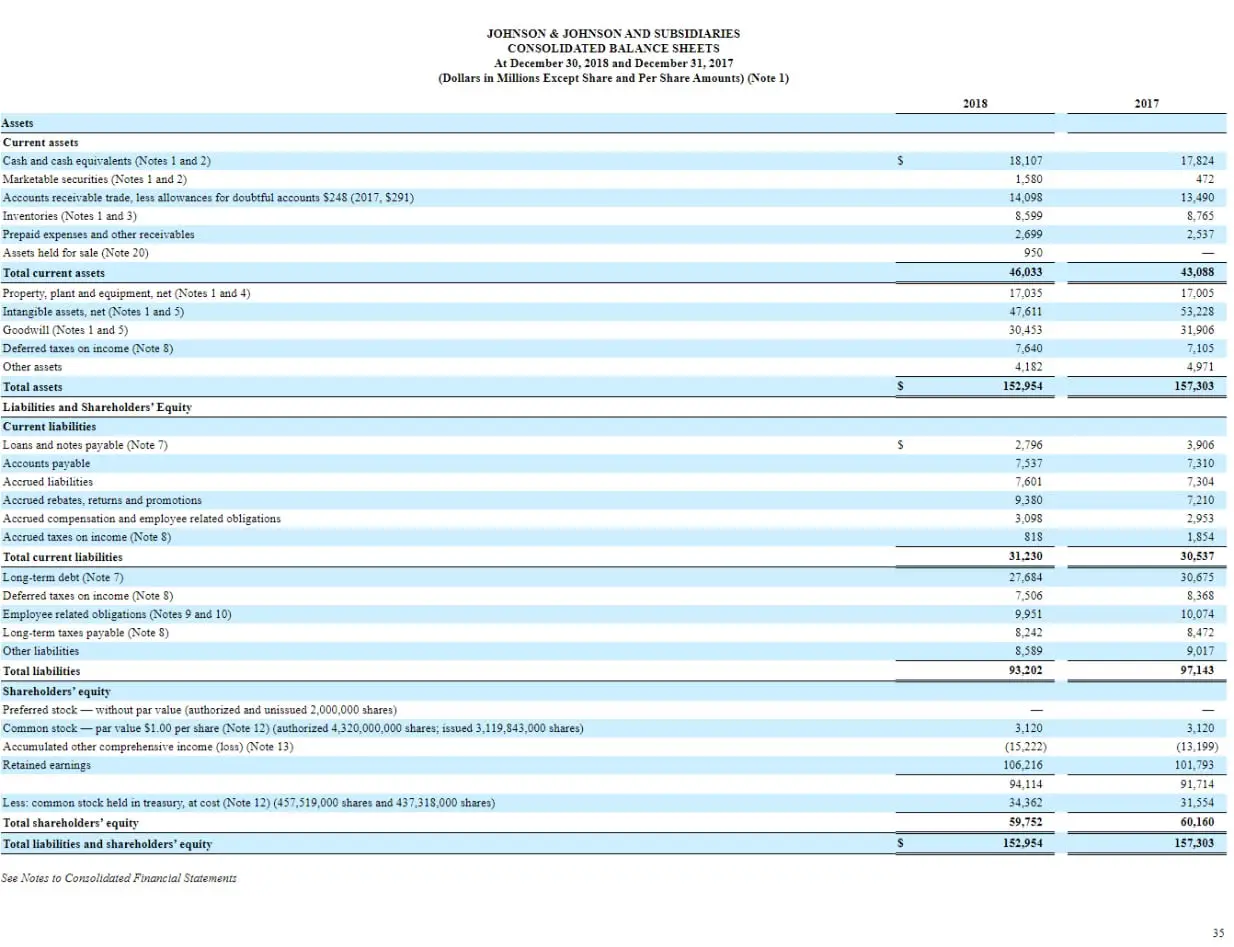

- Johnson & Johnson

- McKesson Corporation

- Microsoft

- Meta

- Starbucks

- Tesla

- Walmart

Any company that has subsidiaries be it a parent company or a holding company will have consolidated financial statements. The consolidated financial statement is a broad term that includes the consolidated balance sheet, consolidated statement of cash flows, and consolidated income statement. Listed above are some companies that have consolidated balance sheets.

Example of a consolidated balance sheet

Read about: Are Expenses Liabilities on a Balance Sheet?

Consolidated balance sheet vs standalone balance sheet

Both the consolidated balance sheet and the standalone balance sheet are financial reports that show the financial position of a company, they, however, share more similarities and differences. We shall outline some of the differences in the table below:

| Consolidated balance sheet | Standalone Balance sheet |

|---|---|

| Has an added entry known as minority interest | Does not contain minority interest. |

| Reported by the parent company | Reported by a single company |

| Preparation is very tasking and time-consuming | Less tasking and takes a shorter time to prepare |

| Reports the assets, liabilities, and equity of the parent company and its subsidiaries. | Reports the assets, liabilities, and equity of a particular company |

Similarities

- Both have sections for assets, liabilities, and equity.

- Both give information about the assets, liabilities, and equity of companies.

- Both give a picture of the financial position of the company that has them.

- Both are prepared based on the balance sheet equation where the assets reported must be equal to the sum of the liabilities and equity reported.

- Both are balance sheets.

Differences

- The consolidated balance sheet has an added entry known as a minority interest. The minority interest is used in a situation where the parent company has shared ownership of a subsidiary. This indicates a situation whereby the parent company does not own 100% of the subsidiary, instead, it owns the controlling interest (over 50%) while the remaining portion is owned by others.

- While the balance sheet reports the assets, liabilities, and equity of a single company, the consolidated balance sheet reports the combined assets, liabilities, and equity of several companies but combines them together as a single entity.

- Any kind of company irrespective of being a startup or a well-established company can have a balance sheet but only holding or parent companies have a consolidated balance sheet to report their combined assets, liabilities, and equity with that of the subsidiaries they own.

- Preparing a consolidated balance sheet is more tasking than preparing a balance sheet. This is because in preparing a consolidated balance sheet, duplicate data has to be eliminated, cross sales have to be removed and all information from the various subsidiaries has to be combined as one with that of the parent or holding company.

Read about: Where is accumulated depreciation on the balance sheet?

How to prepare a consolidated balance sheet

- Gather all information

- Make necessary adjustments for cross sales

- Remove duplicated data

- Create a worksheet

- Make the consolidated trial balance

- Make the actual consolidated balance sheet

The major step in preparing a consolidated balance sheet is to ensure that all the subsidiary companies have accurate data on their assets, liabilities, and equity, This is important because any inaccuracy in their reporting will affect the overall outcome of the consolidated balance sheet. Additionally, the information of the parent company has to also be up-to-date and precise before the consolidation begins. Let us look at the various other steps necessary in preparing a consolidated balance sheet.

Gather all information

In preparing a balance sheet, the major information required is the assets, liabilities, and equity of a company. In the case of the consolidated balance sheet, these have to be gotten for the parent company and all its subsidiaries before any other thing can be done.

Make necessary adjustments for cross sales

When preparing the consolidated balance sheet double counting is avoided. Double counting occurs when the same transaction is reported differently by the parent company and the subsidiary. In most instances, sales between the parent company and a subsidiary will appear in the financial transactions of both companies with one recording a revenue from the sale and the other reporting an expense. For instance, if the parent company realizes revenue that is recognized as an expense for the subsidiary, such a transaction is eliminated from the balance sheet. This step is known as eliminating cross-sales and aids in reporting the right amount of assets and liabilities.

Remove duplicated data

All assets and liabilities that appear in both the parent company’s balance sheet and that of its subsidiaries have to be removed to avoid duplication of data. Hence any asset or liability that appears in more than one balance sheet will be reported only once. This is to ensure that the consolidated balance sheet is accurate and does not give an incorrect impression about the financial standing of the parent company and its subsidiaries. For instance, if two subsidiaries use one printing machine, it should not be listed twice, as that would be an inaccurate picture of the asset since there is actually just one printing machine. Therefore, only one printing machine should be reported.

Create a worksheet

A lot of companies use Excel as their worksheet although some others use various other types of software to create a worksheet. After confirming that the information you have about the parent company and its subsidiaries’ assets, liabilities, and equity are accurate, and you have eliminated all cross-sales, creating a worksheet is the next step. List all the asset and liabilities accounts and their exact values, adding all the assets and liabilities of the parent company and the subsidiaries into one account. Ensure that there are no errors when making the compilation.

Make the consolidated trial balance

A consolidated trial balance is a sum of all the debits and credits that have been recorded by the parent company and all its subsidiaries. Each subsidiary is listed in the columns with all its debits and credits and a grand total at the end. The consolidated trial balance should have a total of zero if all calculations are done accurately as it shows that the assets, liabilities, and equity of the parent company and its subsidiaries are in sync and accurately represented. If the total is not equal to zero, it means there is an error in the trial balance reporting.

Hence this step is used to checkmate and ensure that the data reported by the various subsidiaries and the parent company are accurate. It also serves as a quick reference whenever there is a need to check any underlying transaction that was carried out by the parent company or its subsidiaries. Additionally, the fair market value of the assets owned by the parent company and all its subsidiaries have to be correctly estimated to avoid overvaluation or undervaluation of the business.

Make the actual consolidated balance sheet

Now that all the information from the parent company and all its subsidiaries has been checked to ensure they are all balanced, the consolidated balance sheet can be made. The date for the period for which the balance sheet covers and the names of all the companies involved are listed at the top of the balance sheet. Sections are then added for assets, liabilities, and equity, and the prior information from the consolidated trial balance is inputted. Furthermore, the assets reported should be equal to the sum of the liabilities and equity based on the balance sheet equation where Assets = Liabilities + Equity.

Summary: Preparing a consolidated balance sheet in 3 steps

The 6 steps listed above on how to prepare a consolidated balance sheet can be summarized into the three steps viz:

- Combine the assets, liabilities, and equity of the parent company with that of all its subsidiaries.

- Offset the parent company’s investment in the various subsidiaries, the portion of equity it owns in each subsidiary, and input the minority interest to represent the portion owned by other shareholders (the portion of the company not owned by the parent company)

- Eliminate all intragroup transactions that could impact the assets or liabilities that will be reported on the consolidated balance sheet. Report what is left as the consolidated balance sheet of the group.

Read about: Accumulated Depreciation on Balance Sheet

Conclusion

Parent companies generally prepare the consolidated balance sheet for reporting purposes and also to show the connection between the assets, liabilities, and equity of the parent company and its subsidiaries. It is seen as an extension of the regular balance sheet that single companies use to report their financial standing. Although the process of preparing a consolidated statement of financial position is tasking and time-consuming, the outcome gives a picture of the parent company and its subsidiaries at a glance.

The information gotten on the consolidated balance sheet is also useful to auditors, investors, and stakeholders as it gives a more vivid picture of the financial standing of the group. This is especially true since assets and liabilities that are common to the parent company and its subsidiaries are eliminated from the consolidated statement of financial position to avoid duplication of data that could lead to distorting the balance sheet.

Additionally, when the parent company and its subsidiaries use the same template for their balance sheet reporting, it makes the consolidation process easier and less time-consuming. This is because the similar template aids in reducing the time taken when creating a worksheet to compile the various assets, liabilities, and equity of the parent and its subsidiaries. Furthermore, the consolidated balance sheet is part of the reporting requirements when companies file their financial statements, hence preparing it is compulsory for all parent companies.

When a consolidated balance sheet is made, it might be necessary to substantiate it. The substantiation process ensures that all the data presented therein are not only accurate but that they are true and in balance with each other.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.