Credit risk assessment helps in the prediction of potential risks that are faced by banks and other lenders. It is an essential factor in determining if a customer is at risk of defaulting on payments. Carrying too many high-risk customers or even just a few significant transaction customers who are a potential default risk can be greatly detrimental to the health of a business.

Also, each time one invoices clients after the provision of goods and services, it is exposing its business to late payment risks which are capable of disrupting cash flow. Credit risk, therefore, is not only applicable to banks and other lenders, it is also applicable to businesses that offer credit sales of goods and services to customers.

The effective assessment of credit risk allows one to determine the creditworthiness of a customer and reduce his financial risk. Conversely, risk decisions that are overly conservative can cost the company in the form of opportunity costs. In this article, we see what is credit risk, the types of credit risks, what credit risk assessment implies, and ways to assess them.

What is credit risk?

Credit risk is the possibility of loss that results from a borrower’s failure to repay a loan or meet contractual obligations. It is traditionally the risk that a lender may not receive the principal and interest owed which brings about an interruption in cash flows as well as an increased collection cost.

Excess cash flows may be written to provide additional cover for credit risk. When a lender is faced with heightened credit risk, it can be mitigated via a higher rate of coupon which provides for greater cash flows.

Although it is not possible to know exactly who will default on financial obligations, properly assessing and managing credit risks can go a long way in reducing the severity of a loss. Interest payments made by borrowers or the issuer of a debt obligation are the reward that lenders or investors get for assuming credit risk.

When lenders offer mortgages, credit cards, and other types of loans, there is the risk that the borrower may not repay the loan. The case is similar to a company that offers credit to a customer, there is a risk that the customer may not pay their invoices. Credit risk can also describe the risk that an issuer of bonds may fail to make payment when requested or that an insurance company will not be able to make a claim payment to its policyholder.

Credit risk explained

Credit risks are calculated on the basis of the borrower’s overall ability to repay a loan according to its original terms. Usually, to assess credit risk on a consumer loan, lenders take a look at the five Cs which are credit history, capacity to repay, capital, the loan’s conditions, and associated collateral.

There are companies that have established departments that are solely responsible for the credit risk assessment of their current and potential customers. Technology has afforded businesses the ability to swiftly analyze data used in assessing the risk profile of a customer.

An investor who considers buying a bond will always review the credit rating of the bond. If it has a low rating, less than BBB, then the issuer has a relatively high default risk. On the other hand, if it has a stronger rating, BBB, A, AA, or AAA, the risk default is progressively diminished. In this case, bond credit-rating agencies evaluate the credit risk of thousands of corporate bond issuers and municipalities continuously. For example, an investor that is risk-averse may opt for an AAA-rated municipal bond while a risk-preferred investor may buy a bond with a lower rating in exchange for returns that are potentially high.

Credit risks check a borrower’s creditworthiness and in calculating it, lenders measure how they will recover all the principal and interest while making a loan. In essence, lenders judge the borrower’s ability to pay off his debt while determining the credit risks involved in making loans. A number of factors go into the assessment of credit risk including credit history and credit score, debt-to-income ratio, and collateral.

Risks are expected to be a part of banking operations, however, this does not mean that it is impossible to mitigate risks. Commercial banks as well as private lenders usually reduce the risk of fraud and cyber security threats to protect the financial information of their clients as well as protect their treasury from unreliable borrowers.

Each time a borrower misses a monthly payment or in worse situations, defaults on a loan altogether, the lender suffers a loss. Even if the collateral is taken, the time and money that is spent to turn it into funds can still bring about negative returns to the lender. It is for this reason that financial institutions evaluate each borrower’s credit risk thoroughly. The borrower will also look out for their reserves and environmental factors before signing off on loans.

With this, financial institutions analyze the credit risk that has to do with each borrower to reduce losses and fraudulent activities. As earlier stated, the term can be extended to other similar risks such as bonds where a bond issuer may not be able to make payment at the time of its maturity or an insurance company may not be able to make claims payment.

Related: Capital Market Instruments Examples, and Types

Types of credit risks

- Default risk

- Concentration risk

- Country risk

- Downgrade risk

- Institutional risk

Default risk

Default risk is a situation whereby the borrower is either unable to pay the amount in full or is already 90 days past the due date of the loan repayment. Default risk has an impact on almost all credit transactions such as securities, bonds, loans, and derivatives. Because of the uncertainty that exists, borrowers undergo thorough background checks.

Concentration risk

In situations whereby a financial institution relies heavily on a particular industry, it is prone to the risk that is associated with that industry. If that industry suffers an economic setback, the financial institution will incur massive losses.

Country risk

The term, country risk, denotes the likelihood of a foreign government or country defaulting on its financial obligations as a result of economic downturn or political unrest. Even a little rumor or revelation can make a country become less attractive to investors. The sovereign risk is mainly dependent on a country’s macroeconomic performance.

Downgrade risk

Downgrade risk is the loss that results from falling credit ratings. When market analysts look at credit ratings, they assume operational inefficiency and a lower scope for growth. It is a vicious cycle and the speculation makes it even more difficult for the borrower to repay.

Institutional risk

This implies a scenario where borrowers fail to comply with regulations as well as contractual negligence that may be caused by intermediaries between the lenders and borrowers.

Credit risk assessment defined

Credit risk assessment is defined as analyzing the possibility of the borrower’s payment failure and the loss caused to the financer when the borrower fails to repay the contractual loan obligations for any reason. Interest for credit-risk assumption forms the earnings and rewards from such debt obligations and risks. This is a vital as well as the basic aspect of credit risk management.

There is an impact on the financer’s cash flow when the interest accrued and the principal amounts are not paid. This further brings about an increase in collection costs. Though there is no clarity in guessing who and when will default on borrowings, it is the process of intelligent analysis of credit that can help in reducing the severity of complete loss of the borrowings and its recovery.

In assessing credit risks, banks, financial institutions, and NBFCs offer mortgages, loans, credit cards, etc., need to exercise utmost caution. In the same way, companies that offer credit, bond issuers, insurance companies, and even investors need to know the techniques for effectively assessing risks.

With this, risk analysis of the credit or obligation being offered is very important to be prepared for risk management, mitigation, and recovery of the loans/financial obligations. Borrowers, on the other hand, need to monitor their credit ratings in order to be eligible for a lower interest rate and loan eligibility. Improving credit scores on part of the borrower ensures access to unsecured or collateral-free loans at low-interest rates.

In cases where lenders offer mortgages, credit cards as well as other types of loans, a risk that the borrower may not repay the loan is usually in place. In assessing the credit risk of a customer, smart businesses make use of a series of strategies to unveil the full picture of the customer’s creditworthiness. This means first assessing the client’s financial performance using big-data tools that quickly capture trade data.

Running a business credit report which depicts a customer’s ability to pay invoices based on the history of payment and public records is also a critical next step. Making requests for trade references from the customer’s bank and other lenders, as well as businesses or suppliers that already extend credit facilities to that customer is also a good practice.

While these practices are helpful in mitigating risks, it is important to note that potential clients are likely to provide companies they pay on time as references and omit companies with which they tend to have an unfavorable payment record.

Companies like credit insurers that are specialized in payment risk can remove this uncertainty since they have unique visibility over millions of buyer relationships and covered transactions rather than just a select few. Calculating a client’s debt-to-income ratio shows the portion of the company’s debts that make up its earnings. The lower this number, the higher its creditworthiness.

In assessing an international client, it is important to review any credit risk that is country-specific, which can be affected or impacted by fluctuations in currency exchange rates, economic or political instability, the possibility of trade sanctions or embargo, and other issues.

Related: Loan to Value Calculation: LTV Ratio Formula

5Cs in the assessment of credit risks

- Capital

- Capacity to repay

- Credit history

- Conditions of the loan

- Collateral

It has been seen that credit risks are assessed depending on the borrower’s overall ability to adhere to the original contractual terms of loan payment. The important 5Cs that lenders look out for are:

Capital

Capital in business or the own contribution of borrowers is an important factor. Higher cash flows and equity capital lower one’s financial leverage and make the loan terms better. This rule essentially says that more is better.

Capacity to repay

Capacity to repay takes into consideration the borrower’s cash flow, ability to repay, and the terms of repayment.

Credit history

Credit history reveals how reliable and trustworthy the borrower’s credit handling has been and lenders will evaluate foreclosures, bankruptcies, court cases, and judgments revealed in his credit history.

Conditions of the loan

Conditions of the loan are dependent on economic policies, current market rates, taxes, economic conditions that are relevant to industries, size of the loan, intended use, and market impact on the loan.

Collateral

Collateral associated with the loan covers the risks that have to do with non-repayment. Adequacy, acceptability of the asset, and market values can be gainfully leveraged when applying for loans.

Assessing the credit risk can be carried out in several ways like point-based systems, personal appraisals by risk assessors, or by departments for credit risk assessment of loan customers. Investors look into the credit rating of bonds. Bonds that have a B or C low rating have a higher probability of offering higher returns and defaulting on payments.

Additional factors to be considered in credit risk assessment

- Probability to default

- Debt-to-income ratio

Probability to default

In the assessment of credit risks, one most important factors for lenders to consider is the borrower’s probability of default. This describes the likelihood of a borrower not paying back the loan. This calculation helps the lenders assess the information contained in a credit report and the pieces of information that most predict the occurrence of a default.

Debt-to-income ratio

A lender should consider this important calculation, the borrower’s debt-to-income ratio. Once they have collected a substantial amount of debt, their credit risk increases rapidly. This shows that they are a high-risk borrower because they are spreading their finances too thin.

At the end of the day, a lender needs to do what is best for the company and determine the level of risk it is willing to take. It is also of relevance for the lender to decide how much of a break on interest and down payment it is going to give low-risk clients. Once there is a baseline and maximum associated with risk management, it will be much easier to assess individual cases.

Ways to assess credit risks

Analyze the borrower’s financial statements

Analyzing the borrower or firm’s financial statements is a good starting point. This is to see if it has enough liquidity to remain in business, is well-funded, and has a history of consistent profitability.

Review gross margin

This is a further financial investigation that should be carried out, the gross profit margin is reviewed on a trend line to see if the borrower is able to maintain a reasonable profit on a consistent basis. This can be derived from being able to establish and hold reasonable price points as well as maintaining significant efficiencies in production.

Review senior management team history

Reviewing a borrower’s senior management team is another way of assessing credit risk. This is applicable to a borrower that has such. Ideally, this group should have a record of solid financial performance in the places they have worked and preferably have avoided situations of bankruptcy. Any evidence in the business press of having made poor management decisions is to be reviewed in detail.

Related: Income Statement Ratios Formulas and Examples

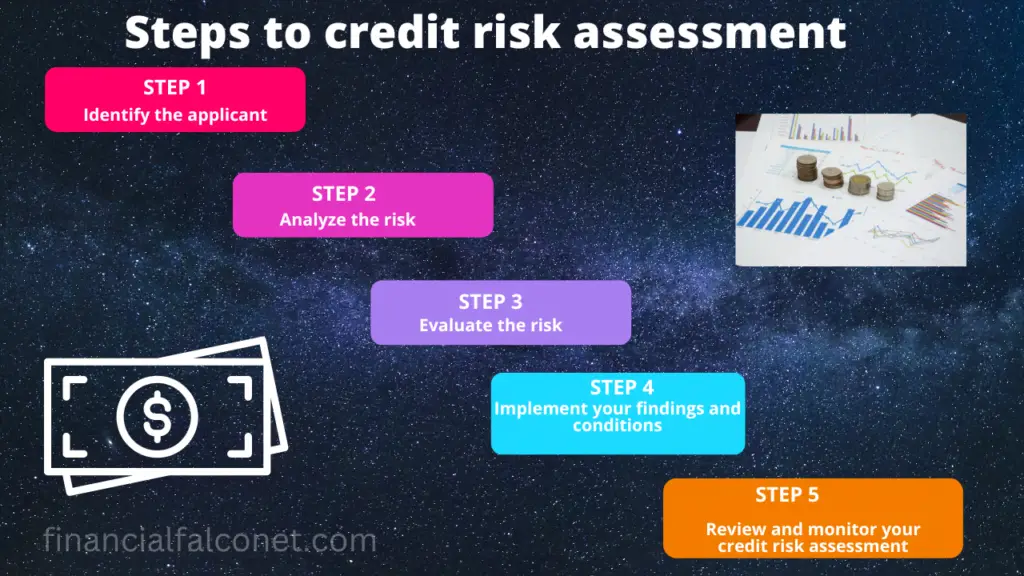

Steps to credit risk assessment

- Identify the applicant

- Analyze the risk

- Evaluate the risk

- Implement your findings and conditions

- Review and monitor your credit risk assessment

Identify the applicant

The first step that is usually taken in credit risk assessment is to gather all the necessary information to determine the characteristics of the applicant. In assessing the sources for traditional credit information, one will need to collect their personally identifiable number (PII). Alternative credit information may require other information other than PII such as banking, payroll, or even tax information.

In identifying the applicant, the lender needs to check potential credit scores which is one of the 5Cs to be considered. Looking out for credit scores will help a business evaluate its business and supplier risk or potential loss, increase collections, and reduce fraud. The ability to make the right decisions is only as good as the data that drives those decisions. It is important to be sure to get current information.

Analyze the risk

The next step to take in assessing credit risk is to evaluate the applicant’s ability to repay or capacity to repay (another element of the 5Cs to be considered). This should not be ignored. They may have good intentions to repay but situations, whereby they are unemployed with no job prospects or have a negative bank account balance, may not make them a viable prospect for the lender’s service. While evaluating approvals based on the willingness of the applicant to repay their loans and their intentions, one is most likely lending based on their ability to pay back.

Evaluate the risk

Evaluating or assessing the credit risk properly can be a complex task. Most financial institutions make use of data science, build credit models, and incorporate artificial intelligence (AI) and machine learning (ML) to automate credit risk evaluation. Whatever method is applied, variables from the credit data are usually weighed for their contribution to the desired outcome and predictive strength.

Implement your findings and conditions

Once the risk has been evaluated, the conditions of the loan are to be determined which includes the interest rate and the duration of the loan. The aim of this step is to build an extra layer of security as well as accountability into the loan. There is a need to cover all the potential weak spots to reduce the risk of the loan. However, the credit risk assessment does not stop here, it continues even after the loan facilities have been extended to the borrower.

Review and monitor your credit risk assessment

It is important for a lender to continuously assess its customer’s risk. The fact that their credit was good when they applied does not necessarily imply that their credit will remain the same. There is a need to monitor and review a customer’s credit on a regular basis. The monitoring and reviewing process will help the lender find customers that may be eligible for additional financial services.

Impact of credit risk assessment on interest rates

Since all investments look out for a higher interest rate, it is a thumb-rule that the higher the credit risk perceived, the higher the interest rate for capital will be. In cases whereby the risks are too high, the creditors, banks, or financers, may decline to offer loans or invest. Banks will prefer a good credit rating borrower and offer low-interest rates to them.

In the same way, bonds with low ratings will normally offer better returns and are for risk-preferred investors. This means that better credit ratings for borrowers attract lower interest rates. Thus, credit risk assessment is a method used in assessing the creditworthiness of the borrower, organization, business, or bond issuer. As stated earlier, it implies the ability and evaluation of the borrower or company to honor repayments of its financial obligations. The contents of the audited financial statements of bigger companies are used for rating creditworthiness and bond issues.

Importance of credit risk assessment

The basic importance of credit risk assessment is that it is a step to mitigating economic risks that result from a borrower’s default. It is an aspect or one of the processes of credit risk management which means that without assessing credit risks, risk management cannot be effectively carried out. In turn, credit risk management brings about a competitive advantage to commercial banks and private lenders by improving their decision-making.

Also, credit risk assessment is a stepping stone to ensuring increased financial security for lenders. here, lenders can then grant borrowers the loans needed to build their credit.

It provides the basis for remaining compliant in this highly regulated environment and if done correctly, it can offer an advantage in the business.

Companies and financial institutions are increasingly investing in high amounts in credit risk assessment. It is carried out with many significant levels of capital to create in-house teams that focus solely on the development of credit risk management processes and tools for better assessment of credit risks.

With the rise of fintech over time, new technology has empowered businesses to be better at analyzing the data and assessing the risk profile of different investment products and individual customers. It is critical to note that it becomes impossible for any lender to have a full understanding of whether a borrower will default on a loan or not. However, through relevant risk modeling techniques and the latest credit risk assessment technology, it is possible to keep the default rates low and reduce the severity of losses.

Related: Types of Profitability Ratios and Formulas

Last Updated on November 2, 2023 by Nansel Nanzip Bongdap

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.