Equity options are a form of derivative that gets their value from the underlying asset attached to them. They are exclusively used to trade shares of companies as their underlying assets. Here we shall discuss equity options examples and types. We shall also see the equity options formulas used in calculating the potential profits or losses. But before then, let us have a better understanding of what equity options are.

What are equity options?

Equity options are contracts that give their holders the right to either purchase or sell the underlying asset associated with the option at a predetermined price (strike price) on or before a preset date (expiration date). In the case of equity options, the underlying security is the equity shares.

Common terms associated with equity options

- Strike price

- Option premium

- Expiration date

- Option writer

- Option holder

- Underlying asset

- Exercising

- Vesting

- Vesting schedule

Strike price

The strike price is the price at which the underlying asset is bought or sold. This price is usually predetermined in the equity option contract and represents the price per share. Usually, the strike price is listed in increments ranging from 0.5, 1, 2.5, 5, or 10 points. The increments vary based on the equity options’ price level.

Option premium

The option’s premium is the price at which the option trades daily. It is also the price at which the contract is purchased by the holder. The option writer’s potential loss is unlimited and only reduced by this premium that the option holder pays. The premium is not fixed, it fluctuates daily.

Expiration date

The expiration date is the date on or before which the option holder’s right can be exercised. After the expiration date, the contract becomes invalid. Once the contract expires, the equity option holder no longer has the right to either purchase or sell the underlying asset and the option writer is also no longer obligated to sell or buy the underlying asset.

Generally, most options contracts have a validity period of about ten (10) years. However, in recent times, there are short-term options whose expiration dates vary between one week and a month. Equity options that expire in a given month usually expire on that Friday of that month. This third Friday is referred to as the expiration Friday and is the last trading day for equity options that are expiring. When the expiration Friday is an exchange holiday, the last trading day is the preceding Thursday before it.

Option writer

The option writer is the person who is obligated to either sell or purchase the underlying equity option asset.

Option holder

The option holder is the person who has the right to either sell or purchase the underlying equity option asset.

Underlying asset

The underlying asset is the shares that the option writer is obligated to sell or purchase when the option holder exercises their right to either buy or sell the underlying asset of the equity option contract.

Exercising

Exercising equity option is the process whereby the option holders exercise their right to either purchase or sell the shares associated with the option they own. It is only after exercising the stock options you own that you will now have shares or sell them off. Thus, if you do not exercise your equity stock options, you do not own any shares.

Vesting

Vesting is a legal term related to earning the right to own a particular asset. When it comes to the vesting of equity options, it relates specifically to the employee stock options whereby the employee earns the right to purchase the shares associated with their options after they have met the conditions attached to the options.

Vesting schedule

A vesting schedule is that part of the equity option agreement that outlines the specific milestones or timelines or both milestones and timelines that the employee must meet before they can exercise their options. The vesting schedule varies based on the company’s terms but generally, vesting schedules that are time-based have a time frame ranging between four to ten (4 -10) years.

See also: Stock options vs equity differences

Understanding equity options

Essentially, equity options work just like stock options in that they offer the holder the right to purchase or sell the shares associated with them. The holders of either of these options are however not obligated to exercise this right. If the equity options contract gives the holders the right to purchase the underlying shares, they are called a call equity option. When they give the holder the right to sell the underlying shares, they are called a put equity option. We shall discuss each of these equity options further under the types of equity options.

Generally, the equity options contract represents one hundred (100) shares as the underlying assets. The contract is usually between the holder of the contract who is also known as the buyer and the writer of the contract who is also known as the seller. Although the holder of the equity option contract is not obligated to either purchase or sell the underlying assets, the writer on the other hand is obligated to sell or purchase the shares to or from the buyer.

If the buyer’s equity option is a call option, then the seller is obligated to sell the shares to the buyer at the strike price on or before the expiration date. If the buyer’s equity option is a put option, then the seller is obligated to purchase the shares from the buyer at the strike price on or before the expiration date. Once the expiration date has passed, the equity option ceases to exist and becomes null.

Buyers and sellers set equity options prices in the exchange markets. These options are called listed options. Listed options can also be accessed on the New York Stock Exchange American (NYSE American) and New York Stock Exchange Arca (NYSE Arca). These options generally have at least four (4) expiration dates.

Adjustment to the equity option contract such as its strike price or size may be made to account for mergers, acquisitions, or stock split that may result in fractional shares. Equity options are one of the types of equity derivative with the others being warrants, equity futures, and swaps.

Equity options simplified

Equity options are a contract that gives their holders the right to either purchase or sell the underlying assets (shares) associated with the option at a specified strike price on or before the expiration date. The equity options are issued as either call or put options. The call option represents the right to sell while the put option represents the right to buy.

The equity option strike price is the price at which each share associated with the option can be either purchased or sold. The strike price which is usually fixed should not be confused with the premium. The premium is the price at which the equity option contract is bought or sold. It fluctuates daily because it is the price at which the equity option contract trades daily on the option’s market.

The expiration date outlines how long the equity option contract will be in effect. Therefore, the holder of the option can purchase or sell the shares anytime within the stipulated period because once the expiration date passes, the contract becomes void.

See also: Different classes of stocks

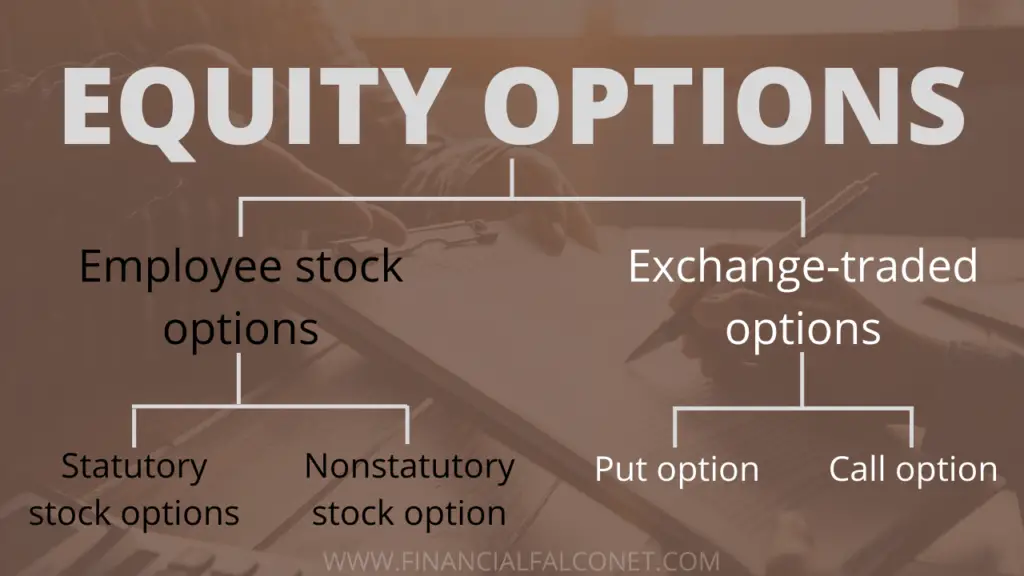

Types of equity options

- Employee stock options

- Exchange-traded options

Employee stock options

Employee stock options are similar to restricted shares. They are a form of equity compensation that companies issue to their employees. These options are mostly part of the employees’ hiring contract or promotion package or issued as an incentive in addition to the regular wages.

Employee stock options are generally in the form of call options in that they give the employees the right to purchase the company’s shares at a future date. Employee stock options are commonly abbreviated as ESOs. The price at which the shares in the ESOs are granted to employees is usually at a discounted rate. The discounted rate is generally cheaper than the current market value of the company’s shares.

Most ESOs have a vesting schedule that is either performance-based, time-based, or a hybrid that is both performance and time-based. Employee stock options give the employee to whom it is granted the right to purchase the company’s shares at a prefixed price known as the exercise price within a stipulated time frame.

Employee stock has a validity period of about ten (10) years before they expire, some companies may however offer a longer or shorter expiration period as enshrined in the ESO agreement. Additionally, when exercising employee stock options, the employee can either pay for the shares in cash or sell part of the shares to cover the cost. This former exercise option is known as a cashless exercise and not all companies offer it.

Types of employee stock options

Statutory stock options

Statutory stock options are often referred to as incentive stock options or abbreviated as ISO. They are also known as qualified stock options because they qualify for certain tax benefits such as:

- Nonpayment of tax when they are exercised provided the difference between their exercise price and fair market value is not up to $73,600 for individuals or $114,600 for married persons filing their tax payments jointly.

- Liable to be taxed at the capital gains rate when the employee decides to sell the shares they had earlier purchased provided they are held for up to one year after they were granted and up to two years after vesting.

- The profit on these stock options is not liable to Social Security and Medicare taxes.

Statutory stock options are granted to employees as part of the corporate benefits they get for working in the issuing company. They give the employees to whom they are granted the right to purchase the shares of the issuing company, otherwise known as the granting entity, at a fixed price within a stipulated period. The fixed price is usually discounted and is also referred to as the grant price or exercise price or strike price. The stipulated period is usually ten years after which if the employee does not exercise their right to purchase the shares, they can no longer use the ISO as it would have already expired.

ISOs are generally granted to motivate employees to keep working in the issuing company, retain top talents and reward exceptional work ethics. They may also be used as part of a promotion package especially when the company does not want to outrightly give a cash bonus or a hiring plan in order to attract top talents who might otherwise not agree to work at the company due to the relatively low base wages they offer. Oftentimes, statutory stock options are granted to employees alongside their regular wages.

Furthermore, the vesting schedule of statutory stock options is either time-based or performance-based, or a mix of the two. In an event of job termination, the employee has a maximum of three months within which they must exercise their stock option; this is known as the post-termination exercise period (PTEP). However, for some companies, once an employee’s appointment is terminated, their previously granted ISO becomes automatically forfeited.

Since employees will benefit from a higher share price, especially if the difference is considerably higher than when they exercised. It encourages employees to give their best to the company thereby having a direct impact on the success of the company. A major drawback of statutory stock options is that they are nontransferable except in an event of the death of the holder or in the case of lunacy or other disabilities.

Nonstatutory stock option

Nonstatutory stock options are often referred to as nonqualified stock options because they do not qualify for most of those tax benefits that statutory stock options enjoy; They are taxed both at exercise and at sale at the higher ordinary income tax rate and are also subject to payroll taxes which include Social Security and Medicare.

Unlike statutory stock options that can only be granted to employees, these stock options can be granted to nonemployees of the company as well. Thus making them a more readily available compensation type. They also have a wider range of entities that can grant them. They are often abbreviated as NSO or NQSO.

Nonqualified stock options also have a vesting schedule which is either graded or cliff. It is graded if a certain percentage of the shares are vested per time and it is cliff if all the shares vest at once. It is only after vesting and when the employees have exercised their NSOs that they now own shares in the company. After the exercise, the employee can either hold their shares or sell them off.

Just like statutory stock options, nonqualified stock options give the employees whom they are granted, the right to purchase a preset number of shares of the issuing company at a predetermined price per share within a stipulated time frame. Typically, the expiration date for nonstatutory stock options varies from one company to the next, it is therefore pertinent that employees who have been granted this stock option keep the specific expiration date of their stock option in mind because once this date has passed, they can no longer exercise their right to purchase the shares.

The post-termination exercise period for NSOs is varied depending on the agreement terms. Some companies also put clawback provisions that allow them to recall previously granted NSOs for several reasons such as the employee leaving the company, selling the NSO shares to a competitor, insolvency of the company, etc.

Statutory stock options vs nonstatutory stock options

Both statutory stock options and nonstatutory stock options are often used as part of compensation plans of companies, there are however marked differences between these two stock options types which we shall outline within the table below

| Statutory stock options | Nonstatutory stock options |

|---|---|

| They are generally not subject to taxation at the time of exercise | They are subject to ordinary income tax at exercise |

| ISOs can only be granted to employees | NSOs can be granted to both employees and nonemployees |

| The Internal Revenue Code section that regulates these stock options is section 422 | The Internal Revenue Code section that regulates these stock options is section 409a which imposes a 20% excise tax rate if the holder violates some rules in the section. |

| They are not subject to payroll taxes | They are subject to payroll taxes |

| Statutory stock options can only be issued by corporations | Nonstatutory stock options can be issued by corporations, limited liability companies, and partnerships |

| They cannot be transferred unless in the event of the death of the holder | They are usually transferable |

| The amount of ISO that can be exercised yearly is $100,000 | There is no yearly exercise limit with NSO |

| These stock options generally expire 10 years after they were granted | The expiration date of these stock options is varied based on the agreement terms |

| Already vested statutory stock options must be exercised within 3 months after the termination of employment | Already vested nonstatutory stock options may be exercised anytime after the termination of employment before their expiration date |

Related: ISO vs NSO – which is better?

Exchange-traded options

Exchange-traded options are equity options that are listed on exchanges such as New York Stock Exchange American (NYSE American) and New York Stock Exchange Arca (NYSE Arca). They are also referred to as listed options and are regulated by the Securities and Exchange Commission (SEC).

Just like employee stock options, owning these options does not mean that you actually own shares, rather, they confer on their holders the right to purchase or sell the shares associated with the option at a predetermined strike price within a designated period. Exchange-traded options are guaranteed by the Options Clearing Corporation (OCC). The OCC handles options transactions in order to mitigate the risks of companies failing to meet the settlement obligations associated with these options.

When the strike price of an exchange-traded option is below the current market value of the underlying shares, the option is referred to as an in-the-money option. This presents a gain to the option holder. When the current market price of the underlying shares is equal to the strike price, the option is referred to as an at-the-money option. When the strike price is greater than the current market value of the underlying shares, the option is referred to as an out-of-the-money option or an underwater option.

With exchange-traded options, investors can still profit without necessarily exercising their equity options. They can instead sell off the equity options when the options are in-the-money to another investor and make a profit before the expiration date. This is commonly done by investors who purchase uncovered options. Selling the equity option also mitigates higher transaction costs, waste of time, and other marginal requirements

Uncovered options are options for which the investors do not have any prior existing shares. Covered options are options for which the investors have prior existing shares. Most investors with covered options purchase these options as a means of hedging against a fall in share price.

Investors who want to invest in exchange-traded options may do so by predicting if the price of a particular share will either decrease below or increase above the strike price at the expiration date. If the investor’s prediction turns out right, they can make a profit from the equity options they have. The potential profits or losses incurred from exchange-traded options might also be subject to taxes. Additionally, commissions and some other fees could also be charged.

Types of exchange-traded options

- Call option

- Put option

Call option

A call option is a derivative contract that confers on its holder the right to purchase the underlying assets at the specified strike price anytime before its expiration date. The option writer is obligated to sell the underlying assets to the call option holder once they exercise their right to make the purchase. These underlying assets are the shares and each call option typically contains one hundred (100) shares as its underlying assets. The expiration date for a call option varies between three (3) months to one (1) year; although some may be longer.

The call option price is usually based on how unlikely or likely, it is that the option holder will make a profit when they decide to exercise their option before the expiration date. Most investors that buy call options do so with the hope that the underlying share price will increase above the strike price before the expiration date.

If the market price of the underlying shares increases, the option holder is guaranteed the shares at the cheaper strike price and they can sell the shares after they have exercised their options. The difference between the strike price and its higher market value becomes their gain. If the investor however decides not to exercise their rights either because the market price of the underlying shares is the same as or below the strike price; then they will lose their initial investment which was used to purchase the call option otherwise known as the option premium.

While the option holder hopes for an increase above the strike price, the option writer conversely hopes that the price does not reach the strike price or even decreases far below it within the stipulated period because if either of the aforementioned happens, the money which the option writer received for the call option sale becomes a profit. Since the option holder is not likely to exercise their call option in any of those scenarios.

If however, the price increases beyond the strike price and the call option holder exercise their right, then the option writer incurs a loss which is equivalent to the difference between the strike price and the current market value of the shares multiplied by the number of shares in the call option contract.

A call option can function either as a short call option or a long call option. A long call option is a contract that gives the option holder the right to purchase the underlying shares in the option contract at the strike price on or before the expiration date. By purchasing the long call option, investors use it either to speculate or to plan ahead.

When a long call option is used to speculate, the investor predicts that the underlying share price will increase within the stipulated period. When used to plan ahead, investors who do not have the needed money to purchase shares that they feel will increase in market price purchase the long call option for it instead. These investors do so in the hope that when the share price rises, they will still be able to purchase it at the lower strike price preset in the option contract.

Investors who use the short call option mainly do so as a means of boosting their income. The short call is an obligation to sell the underlying shares for which they have already received the option premium. Here, the investor hopes the strike price does not rise to the strike price before the expiration date.

Investing in call options enables option holders to make a potentially large return on investment (ROI) from a relatively small amount of investment; by doing so, they limit their risk while generating a capital gain. Institutional and corporate investors also use these options as a means of increasing their marginal revenue and hedging their stock portfolios. Some other investors also use it as a means of hedging from positional risks and also generating income from the option premium.

Put option

The put option is the opposite of the call option. It gives the option holder the right to sell the underlying shares to the option writer at the strike price before the expiration date. The option writer on the other hand is obligated to purchase the underlying shares. The option writer sets the contract terms and the option buyer must pay the writer the premium to purchase the put option contract.

Since the option holder is not obligated to sell the shares, there are no consequences if they choose not to exercise the option. They will only lose the money they spent to purchase the options plus any other fees that had been spent. If the price of the underlying shares decreases below the strike price, the put option holder gains from it as the option is in-the-money.

While the put option holder gets a maximum profit if the underlying share price falls to zero, the option writer gets the maximum loss if this happens. The maximum gain of the put option writer is limited to the premium collected, as well as any other related fees, that is if the option holder does not exercise their put option.

Put options are especially used to hedge against a future fall in share price, they are also used to speculate that the price of the underlying shares will fall below the strike price before the expiration date. The relationship between the value of a put option and the underlying share price is the opposite, this means that the value of a put option decreases when the market price of the underlying share increases, and it increases when the market price of the underlying share decreases.

If you purchase a put option, you are betting that the price of the underlying shares will reduce before the expiration date of the option. Conversely, if you sell a put option, you are betting that the price of the underlying shares will either remain the same or increase before the expiration of the contract.

Put options can either be covered or uncovered. Covered put options are those which the option holder has prior existing shares for. Uncovered options are those which the investors do not have any prior existing shares for.

Call options vs put options

Although both call options and put options have similarities in the fact that they are both listed equity options and are regulated by SEC, there are some intrinsic features that differentiate them which we shall outline within the table below

| Call options | Put options |

|---|---|

| Call options give their holders the right to buy the underlying shares | Put options give their holders the right to sell the underlying shares |

| The option writers are obligated to sell the underlying shares | The option writers are obligated to buy the underlying shares |

| Holders of these options bet that the underlying share price will increase above the strike price | Holders of these options bet that the underlying share price will decrease below the strike price |

| Writers of these options bet that the underlying share price will decrease below the strike price | Writers of these options bet that the underlying share price will increase above the strike price |

| The option holder gets a maximum profit if the underlying share price rises far above the strike price and they exercise their option. | The option holder gets a maximum profit if the underlying share price falls to zero and they exercise their option. |

| The option writer gets the maximum loss if the underlying share price rises far above the strike price and the option holder exercises their right to buy. | The option writer gets the maximum loss if the underlying share price falls to zero and the option holder exercises their right to sell. |

See also: Dividend stocks

Equity options formulas

The equity options formulas are useful when an employee or investor wants to find out if they are making a profit, breaking even, or losing on the equity options they own when they exercise. When making a profit or breaking even, the result will be positive, meaning that your option is in-the-money in a case of a profit or at-the-money if you are breaking even. When you are going to experience a loss if you exercise your result will be negative which means that your option is out-of-the-money.

Employee stock options profit

Since employee stock options are usually granted to employees as compensation, it is generally rare to experience a loss or break even with these stock options. The profit on ESOs is gotten by subtracting the exercise price from the fair market value of the shares. It can be expressed as

Employee stock option profit = Fair market value of underlying shares – Exercise price

Exchange-traded option formulas

Unlike employee stock options (statutory and nonstatutory stock options) whose profit, breakeven, or loss can be calculated using the same formula, exchange-traded options (call and put options) have different formulas. We shall look at each of these formulas below

Call option profit or loss formula

In order to calculate the profit or loss of exercising a call option, the difference between the price at which the underlying shares are currently trading and the sum of its strike price and the premium paid needs to be gotten. This will show if exercising the option will be a gain or not. It can be simply expressed as

Call option profit/loss = Current market value of the shares – (Strike price + Premium)

Put options profit or loss formula

Calculating the profit or loss that will be incurred when a put option is exercised is gotten by finding the difference between the strike price of the underlying shares and the sum of the option premium and its current market price. This can simply be expressed as:

Put options profit/loss = Strike price – (Premium + Current market price of shares)

Equity options examples

Using the various equity options formulas, we shall use them to calculate the profits or losses incurred by option holders when they choose to exercise their option. These hypothetical situations will give us a clearer understanding of how the various equity option types work

Employee stock options example

Example 1

Suppose Mr. John works as an assistant secretary in a publishing firm and recently got promoted to be the firm’s secretary. As part of his promotion package, he was granted 200 shares at an exercise price of $5 per share and a 6-year expiration date. If the statutory stock option has a graded vesting schedule with 25% of the share vesting yearly, and he exercises in the fifth year before the expiration date when the company’s shares are trading at $15 per share. It means that his options are in-the-money and we can calculate his profit using:

Employee stock option profit = Fair market value of underlying shares – Exercise price

Fair market value of underlying shares = Fair market value per share x Total number of shares = $15 x 200 = $3,000

Exercise price = Exercise price per share x Total number of shares = $5 x 200 = $1,000

Employee stock option profit = $3,000 – $1,000

Employee stock option profit = $2,000

Example 2

Assuming you are a sales agent for a furniture company and you were granted 100 shares of that company which will vest once you are able to sell a thousand pieces of furniture. If the expiration date of the nonstatutory stock option is four years after it was granted and the strike price is $20 per share. It means that your stock option is a performance-based option that has a cliff vesting schedule. This means that if you are able to meet the target of selling the furniture within the first year, you can exercise your option right away.

However, if the price per share at that time is below or equal to the $20 strike price, it is best to wait because exercising at that point will make your option either underwater or at-the-money.

If in three years the price appreciates to $23 per share, you can now exercise your option as it will be in-the-money

Call option examples

Example 1

Assuming Mrs. Gray paid a premium of $400 to purchase a call option that has 200 underlying shares, with a strike price per share of $15 and the option expires in one year. If the market price per share when she bought the option is $12, but it rises to $20 per share before the option expires; she can exercise her right to buy the shares. If she does, her profit will be the difference between the current market price and the sum of the premium and the strike price.

We can calculate the profit using: Call option profit = Current market value of the shares – (Strike price + Premium)

Current market value of shares = Market value per share x Total number of shares = $20 x 200 =$4,000

Strike price = Strike price per share x Total number of underlying shares = $15 x 200 =$3,000

Premium = $400

Profit = $4,000 – ($3,000 + $400)

Profit = $4,000 – $3,400

Profit = $600

This means that Mrs. Gray will make a profit of $600 when she exercises her call option. If on the other hand, the price of the underlying shares does not increase above the strike price, she can decide not to exercise her right to purchase. In this case, her loss will be the premium she paid and any other related fees.

Example 2

Suppose Mr. Harry bought a call option with a strike price of $10 per share and a 6 months expiration date. If the option contains 100 underlying shares and he paid a premium of 50 cents per share, then he stands to lose if the share price does not increase from $8 per share at which it is currently trading before the expiration date. The loss he will incur if he exercises despite the non-increase in share price can be calculated using: Call option loss = Current market value of the shares – (Strike price + Premium)

Current market value of shares =Market value per share x Total number of shares = $8 x 100 =$800

Strike price = Strike price per share x Total number of underlying shares = $10 x 100 =$1,000

Premium = Premium per share x Total number of underlying shares = $0.5 x 100 = $50

Call option loss = $800 – ($1,000 + $50)

Call option loss = $800 – $1,050

Call option loss = -$250

This means that Mr. Harry stands to lose $250 if he decides to still exercise his call option. In this case, it is the option writer that will benefit from the premium Mr. Harry paid since it is unlikely that he will want to exercise his option. However, if the price of the underlying shares increases above the strike price, he can make a profit when he exercises the option.

Related: Put Options Examples and Problems

Put option examples

Example 1

Suppose you own 100 shares in a car manufacturing company, but due to the phasing out of cars that use fuel, you predict that the company’s share price will fall in a few months’ time when more electric cars are released into the market. You can purchase a put option to hedge against this suspected decrease in share price.

If you purchased a put option on February 13, 2023, that contains 100 underlying shares at a premium of $170, with a strike price of $350 per share and an expiration date of 60 days. If the shares were trading at $365 per share but fall to $340 on April 3, 2023. Your put option is said to be at-the-money and you can exercise it to make a profit. The put option has also protected you from incurring a loss on the shares you own. This is also known as a covered put option since you already own the shares for which you purchased a put option.

Your profit can be calculated using: Strike price – (Premium + Current market price of shares)

Strike price = Strike price per share x Total number of underlying = $350 x 100 = $35,000

Premium = $170

Current market price of shares = Current market price of shares x Total number of shares = $340 x 100 = $34,000

Put option profit = $35,000 – ($170 + $34,000)

Put option profit = $35,000 – $34,170

Put option profit = $830

From the above example, we can see that instead of losing $2,500 dollars when the share price declines from $365 to $340 per share and you sell your shares, you end up selling for $350 per share thereby reducing the loss you would have incurred if you had not purchased the put option.

Example 2

Assuming Miss. Pauline paid a premium of $90 for 3 put options with a three-month expiration date and a strike price of $11 per share but she does not own prior shares for which she bought this option. If the shares were trading at $10 per share when she bought the option and the price of the shares increases to $12 per share before the expiration date. She will lose if she decides to exercise her option especially since it is an uncovered option.

The loss she will likely incur can be calculated using Strike price – (Premium + Current market price of shares)

Strike price = Strike price per share x Total number of underlying= $11 x 300 = $3,300

Premium= $90

Current market price of shares = Current market price of shares x Total number of shares = $12 x 300 = $3,600

Put option loss = $3,300 – ($90 + $3,600)

Put option loss = $3,300 – $3,690

Put option loss = -$390

Miss. Pauline’s put options are said to be underwater as it will result in a loss to her if she decides to exercise her option.

See also: Stocks vs real estate

Pros and cons of equity options

Equity options are a risky investment and are therefore not suitable for some investors. However, for investors who are willing to take the risks, equity options provide the flexibility that other financial investment instruments may not offer. This is because unlike investments such as preferred stocks that have a fixed price, equity options are tailored to whatever position the investor wants to take based on their financial ability and risk appetite.

Below, we shall discuss the pros and cons of investing in equity options

Equity options pros

- Equity options serve as a hedge from a decline in the fair market value of the underlying shares, this is known as hedging. They can also be used to assume some level of risk in hopes of a reward; this is known as speculation.

- They aid investors in purchasing shares at lower prices

- Equity options can be a means of increasing the investor’s income against their current shareholding.

- They help investors position themselves for a major market move even when they do not know with certainty the way that the share prices will move.

- Equity options serve as a means through which investors can benefit from either the rise or fall of a share’s price without having to outrightly purchase the shares.

- Investors can combine both long and short equity options with varying expiration dates and strike prices to profit from a favorable market change at a minimal investment. This minimal investment is usually the option premium.

Equity options cons

- Unlike holders of common stock who have the right to vote in the share’s issuing company and may also get paid dividends, holders of equity stock options do not enjoy any of these. In order to get these benefits, the call equity option holder has to first exercise their right to purchase the underlying shares. It is only after the purchase that they may enjoy shareholder benefits.

- The option holder losses the premium paid on the equity option contract if they do not exercise their right to either buy or sell the underlying asset.

- Equity options are a risky investment since no one can predict with 100% efficiency how the fair market value of a share will move in the future.

See also: Shares vs stocks

Conclusion

Equity options generally had a validity period of 10 years but recently, options with an expiration date that varies between a week or a month are available. Exchange-traded options are considered more suitable for investors who have a good knowledge of how these options work and are also willing to bear the risks associated with owning them. The risk indicator of a specific option, contract specifications, and underlying shares can be found on the exchanges website or the Key Investor Document (KID) which is usually a 3 paged document.

For employees who have been granted equity options, it is important to take note of their vesting schedule, exercise price, expiration date, and any other related conditions attached to the options. This information will guide your decision on when best to exercise your options.

Furthermore, holders of equity options should note that they do not own the underlying shares unless they exercise their option to either buy or sell the underlying shares. The formulas above will also be useful in calculating your potential profits or losses when you choose to exercise your options.

Last Updated on November 8, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.