The formula of interest coverage ratio is a simple equation like the debt to equity ratio formula, used in the financial industry by lenders to determine if a borrower can pay the interest on their debt. Knowing this is important in corporate finance.

This article will discuss ICR meaning and the formula of interest coverage ratio in detail.

What is interest coverage ratio?

The interest coverage ratio is a financial metric that assesses a company’s capacity to timely pay the interest on its debt. The word “coverage” refers to the frequency, typically quarters or fiscal years a business or company can pay back its interest from its current earnings.

This financial metric is used by creditors to determine whether a business can support more debt. Because a business won’t be able to afford the principal payments if it can’t afford to pay the interest on its debt. As a result, creditors use the formula of interest coverage ratio to determine the lending risk.

In other words, the majority of businesses simultaneously borrow money from several different sources. Therefore, the lending institutions require a guarantee that they will periodically receive payment, particularly interest. They can determine the likelihood of borrowers missing interest payments with the aid of the interest coverage ratio formula.

The findings from the calculation of the interest coverage ratio, make it simpler for creditors and lenders to determine whether or not to trust the finance seekers with a sizeable loan plus interest.

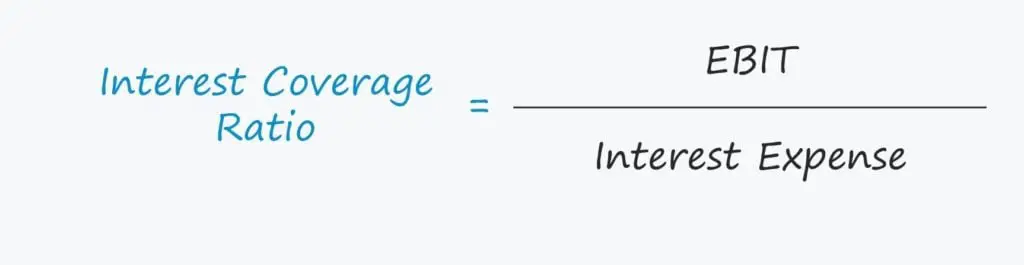

Formula of interest coverage ratio

The formula for interest coverage ratio is given as the earnings before interest and taxes (EBIT) divided by the interest expense. The interest coverage equation is represented in the following manner.

Where:

EBIT, also known as operating profit, is calculated by deducting total revenue from the amount a business owes in taxes and interest, and the amount owing on borrowings like bonds, loans, and credit lines is known as the interest expense.

You can see that the equation substitutes EBIT for net income. In essence, earnings before interest and taxes are net income with interest and tax expenses subtracted. Because we want a true representation of how much the company can afford to pay in interest, we use EBIT rather than net income in the calculation. The calculation would be flawed if we used net income because interest expenses would be double counted and tax expenses would change depending on the amount of interest being deducted.

Interpretation of interest coverage ratio

- Higher interest coverage ratio

- Lower interest coverage ratio

Higher interest coverage ratio

A ratio higher than one indicates that a business can cover its debts out of earnings and the business can maintain steady revenue growth. Additionally, a ratio of 1.5 might be thought to be adequate. Although, analysts and investors typically favor two or higher. Until it is significantly above three, it may not be considered favorable for businesses whose revenues have historically been more erratic.

Lower interest coverage ratio

A negative interest coverage ratio is one with a value below one. This shows that the business’s current revenues are insufficient to pay off its debt. The likelihood that a company will be able to pay its interest expenses continuously is still in doubt if it is less than 1.5. It is dubious, particularly if the business is subject to cyclical or seasonal revenue fluctuations.

According to the interpretation of the interest coverage ratio, default risks (ability to miss loan payments) are reduced as ICR increases. In order to prevent being dropped during the loan term, lenders seek a high ratio. When this ratio is high, the business is in good financial shape, which guarantees lenders low-interest costs for the duration of the loan. On the other hand, a low ICR indicates that the companies’ finances are not in the best shape. As a result, lenders are less likely to trust entities with lower ICR.

What investors look for in ICR

Investors should also take a look at which direction a company’s ICR is trending over a period of time. If the interest coverage ratio rises, the company is becoming more capable of covering itself in the event of a revenue disruption. If the interest coverage ratio falls, the company may be on the verge of insolvency.

Examples and Calculations

The following examples will be on how to calculate the interest coverage ratio using the formula that has been stated previously.

Example 1

Company A reported COGS (costs of goods sold) of $500,000 and total revenues of $10,000,000. Additionally, operating costs for the most recent reporting period included $100,000 in depreciation, $120,000 in salaries, and $500,000 in rent. For the time period, interest costs total $3,000,000. Calculate the interest coverage ratio of company A.

Solution

In order to calculate the interest coverage ratio: we have to determine the EBIT

EBIT = Revenue – COGS – Operating Expenses

EBIT = $10,000,000 – $500,000 – $120,000 – $500,000 – $200,000 – $100,000 = $8,580,000

Therefore:

Interest Coverage Ratio = EBIT/ Interest expense

ICR= $8,580,000 / $3,000,000 = 2.86x

Hence, with its operating profit, Company A can cover its interest payments 2.86 times over.

Example 2

Calculate the interest coverage ratio if a company earns $750,000 in earnings before interest and taxes per quarter and owes $240,000 in debt every six months.

Solution

Since six months equals two quarters, the debt figure would need to be divided by two in order to calculate the company’s interest coverage ratio. The EBIT would then need to be divided by the resulting figure.

Where, EBIT = $750,000, and interest expense = $240,000 / 2 = $120,000.

Therefore:

Interest Coverage Ratio = EBIT/ Interest expense

ICR = $750,000 / $120,000

ICR = 6.25x

This is a respectable interest coverage ratio for a company of this size.

Example 3

Company X submitted a loan request. The lenders discovered the ICR first to make the decision regarding whether or not to approve the loan amount because it had multiple borrowings to manage concurrently. The lenders discovered that the interest costs were $1700, $1500, and $2000 and that the EBIT was $15,000.

Solution

The following formula is used by the company to determine ICR:

ICR = Earnings Before Interest and Taxes (EBIT) / Interest Expense

Where EBIT = $15,000, and interest expense = $1,700 + $1,500 + $2,000 = $5,200

Therefore:

ICR = $15,000 / $5,200

ICR = 2.88x

The lenders were relieved by the calculation because they had no doubt that the borrower would pay interest on time.

Example 4

Preservatives are canned and shipped across the nation by Jane’s Jam Company, a company that makes jelly and jam jars. In order to grow her business, Jane needs canning machines, but she lacks the money to buy them. So, in an effort to obtain the funding she needs, she visits several banks armed with her financial records. Before interest and taxes, Jane made $50,000, while her interest and taxes came to $15,000 and $5,000, respectively.

Solution

The following is how the bank would determine Jane’s interest coverage ratio:

ICR = Earnings Before Interest and Taxes (EBIT) / Interest Expense

Where EBIT = $50,000, and interest expense = $15,000

Therefore:

ICR = $50,000 / $15,000

ICR = 3.33x

You can see that Jane’s ratio is 3.33. This indicates that she has earned 3.33 times more than she is currently paying in interest. She has no trouble paying both the interest and principal on her current debt. This is a positive indication that the risk to her business is low and that her operations are generating enough revenue to cover her expenses.

Example 5

In the most recent reporting month, ABC Company earned $5,000,000 before interest and taxes. That month’s interest expense is $2,500,000. Determine the interest coverage ratio.

Solution

The interest coverage ratio of the company is calculated as:

ICR = Earnings Before Interest and Taxes (EBIT) / Interest Expense

Where EBIT = $5,000,000, and interest expense = $2,500,000

Therefore:

ICR = $5,000,000 / $2,500,000

ICR = 2.1x

According to the ratio, ABC’s earnings should be sufficient to cover the interest expense.

Variations of interest coverage ratio

- EBIT- Earning Before Interest and Taxes

- EBITDA- Earning Before Interest, Taxes, Depreciation, and Amortisation

- EBIAT- Earning Before Interest and After Taxes

EBIT- Earning Before Interest and Taxes

Earning Before Interest and Taxes (EBIT) is the organization’s operating revenue, which represents the income from sales and operating-related expenses. EBIT can be calculated using one of two methods. One method is to add the interest liabilities and taxes due to the net operating income. Since they were initially subtracted, the interest and taxes are added back. The second strategy is to just focus on the profit and loss account’s operating income line item. That is EBIT = Revenue – Cost of Goods Sold – Operating Expenses.

EBITDA- Earning Before Interest, Taxes, Depreciation, and Amortisation

Instead of EBIT, one version of the interest coverage ratio (EBITDA) uses profits before interest, taxes, depreciation, and amortization. Depreciation and amortization are not included in EBITDA. EBITDA is usually worth more than EBIT. Because interest expense is the same in both cases, EBITDA calculations yield a higher interest coverage ratio than EBIT calculations.

For example, if a company’s EBITDA is $100 million and its annual interest expense is $20 million, the EBITDA interest coverage ratio is 5.0x (EBITDA Interest Coverage Ratio = $100m ÷ $20m = 5.0x)

The company’s EBITDA can service the $20 million in interest expense five times, implying that the company’s operating earnings can cover the current interest payment for five “turns.”

However, if the EBITDA coverage ratio was much lower, say only 1.0x, a slight drop in performance for the company could result in default due to a missed interest expense payment.

EBIAT- Earning Before Interest and After Taxes

Earnings before interest and taxes (EBIAT) rather than EBIT are also used in the interest coverage ratio. EBIAT necessitates deducting tax liabilities from the numerator. As a result, the EBIAT approach is a better representation of a company’s ability to pay interest expenses. Tax obligations are both mandatory and obligatory. Because of their tax structure, many companies’ tax liabilities are quite high. As a result, it makes sense to deduct it. EBIAT, rather than EBIT, can be used to calculate interest coverage ratios using this method. EBIAT, like EBITDA, provides a more accurate picture of a company’s ability to cover its interest costs.

Uses of Interest coverage ratio

- The ICR is used to assess a company’s ability to pay interest on outstanding debt.

- Lenders, creditors, and investors use ICR to assess the risk of lending money to a company.

- The ICR is used to assess a company’s stability; a falling ICR indicates that the company may be unable to meet its debt obligations in the future.

- ICR is used to assess a company’s short-term financial health.

- ICR trend analysis provides a clear picture of a company’s interest payment stability.

ICR Importance

- A single interest coverage ratio can reveal a great deal about a company’s current financial situation. However, looking at it over time can show a company’s position and direction.

- It is recommended to examine the company’s interest coverage ratios on a regular basis over the last few years. An examination of the ratio over a number of fiscal years would reveal whether it is improving, declining, or stable. It also gives an indication of the company’s short-term financial health.

- Furthermore, the analyst’s decision plays some role in whether a particular level of this ratio is acceptable. A lower ratio might be acceptable to some banks, investors, and lenders in exchange for a higher interest rate on the company’s debt.

- It is a common accounting metric used to assess the risk of lending funds.

- It is also used by investors to determine whether or not a company is profitable.

- Borrowing does not imply inefficiency or a lack of resources. A company must use this borrowing as efficiently as possible to build assets, expand their business, acquire new businesses, and so on. Profitability is affected by interest payments. As a result, a company should be confident that it can handle them on a regular basis. This ratio can be used to determine a company’s ability or financial strength to pay debt interest.

- Many businesses face the challenge of continuously covering interest liabilities. When a company is unable to meet its obligations, it may be forced to borrow more if it has a good interest coverage ratio.

Limitations

The interest coverage ratio, like any other metric used to assess the efficiency of a business, has limitations that any investor should be aware of before employing it.

- For starters, it is important to note that interest coverage varies greatly between industries and even between companies within the same industry. An interest coverage ratio of two is often an acceptable standard for established companies in certain industries, such as utility companies.

- Because of government regulations, a well-established utility will likely have consistent production and revenue, so even with a relatively low-interest coverage ratio, it may be able to reliably cover its interest payments.

- Manufacturing industries, for example, are much more volatile and frequently have a minimum acceptable interest coverage ratio of three or higher. These businesses typically experience greater business fluctuations. For example, during the 2008 recession, car sales plummeted, harming the auto manufacturing industry.

- Another example of an unexpected event that could harm interest coverage ratios is a workers’ strike. Because these industries are more susceptible to these fluctuations, they must rely on a greater ability to cover their interest to compensate for periods of low earnings.

- In addition, while all debt must be considered when calculating the interest coverage ratio, businesses may choose to isolate or exclude certain types of debt from their calculations. As a result, when evaluating a company’s self-published interest coverage ratio, it’s critical to determine whether all debts were included.

FAQs

An interest coverage ratio of 6 indicates what?

If the interest coverage ratio is 6, it means that the debt can be paid off 6 times in a fiscal year.

What does a bad interest coverage ratio indicate?

A negative interest coverage ratio is one or less, indicating that the company’s current earnings are insufficient to service its outstanding debt. Even with an interest coverage ratio below 1.5, the chances of a company continuing to meet its interest expenses on an ongoing basis are still bleak, especially if the company is susceptible to seasonal or cyclical revenue dips.

How do we calculate interest coverage ratio?

The ratio is calculated by dividing EBIT (or some variation thereof) by interest on debt expenses (the cost of borrowed funds) over a specific time period, usually a year.

How to improve the interest coverage ratio?

There are two ways to raise the ICR. One method is to increase earnings before interest and tax, or EBIT, which can be accomplished as revenue grows. Another method is to reduce finance costs or interest expenses.

What is the formula for interest coverage Class 12?

The interest coverage ratio is also known as the debt service coverage ratio or debt service ratio. It is calculated by dividing the earnings before interest and taxes (EBIT) by the interest expenses incurred by the company during the same period.

Is an interest coverage ratio a liquidity ratio?

Yes, the interest coverage ratio is a liquidity ratio that compares a company’s earnings over a period (before interest and taxes) to the interest payable on its debts at the same time. The interest coverage ratio of a company reflects its ability to make interest payments from available earnings.

Is a high-interest cover ratio good?

Generally speaking, a minimum acceptable level is an interest coverage ratio of at least two. The majority of the time, investors and analysts will be looking for interest coverage ratios of at least three, which show that the company’s revenues are steady and reliable.

What if the interest coverage ratio is negative?

A negative interest coverage ratio is one with a value below one. This shows that the business’s current revenues are insufficient to pay off its debt. The likelihood that a company will be able to pay its interest expenses continuously is still in doubt if it is less than 1.5.

What is EBITDA interest coverage ratio?

The EBITDA-to-interest coverage ratio, also known as EBITDA coverage, measures how easily a company can pay the interest on its outstanding debt. The formula divides total interest payments by earnings before interest, taxes, depreciation, and amortization, making it more inclusive than the standard interest coverage ratio.

How is EBITDA ratio calculated?

Here’s how it works: EBITDA is calculated as net sales minus raw material costs minus employee costs minus other operating expenses. Net sales are the total of all products sold by the company during a given time period.

What is a good interest coverage ratio?

An ideal ratio is one with an ICR greater than 1.5. Many lenders prefer businesses with an ICR of 3, which is not a lenient figure. They are, however, limited to only lending to entities with an ICR greater than 2 to 3.

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.