Claiming bonus depreciation can be a beneficial tax break option for business taxpayers that purchase equipment, furniture, and other fixed assets. Nonetheless, depreciation laws and limits are always changing, thus, before you decide to claim bonus depreciation, it is always advisable to talk to your tax professional to ensure you are taking the right strategy for your business.

For taxpayers seeking ways to minimize short-term tax liabilities, electing to claim bonus depreciation is usually favorable. However, there are some instances whereby electing out of this incentive makes more sense than claiming it. Therefore, it is advisable to consult your tax advisor to know whether it strategically makes sense to take a bonus depreciation and if the property in question qualifies for it. In this article, we will discuss how to claim bonus depreciation and what assets are eligible for this special depreciation allowance.

Related: Can you take bonus depreciation on rental property?

Bonus depreciation explained

In business, you depreciate an asset over its useful life in order to reflect the time that is expected of the asset to generate revenue and be of use to the business. Usually, the entire depreciation expense of a fixed asset is not reported in the year of purchase, it is usually customary to break up the expense over a period of years. However, Congress’ Job Creation and Worker Assistance Act of 2002 enacted bonus depreciation which allows a business to expense the entire cost or a large percentage of most fixed assets in the year that it was purchased and put in service.

Bonus depreciation is, therefore, a tax incentive that allows taxpayers or business owners to report a larger percentage of depreciation in the year that the asset was purchased and placed in service. That is if for instance, say a coffee shop purchased an espresso machine for $10,000. By claiming bonus depreciation, the shop will report the entire $10,000 on its income statement and business tax return in the year that it purchased the machine and put it into service; instead of reporting $1,000 in depreciation annually for 10 years.

From 2017 to 2022, you can deduct up to 100% of the cost of an asset in the year of purchase on your business taxes. The deductible amount was increased in 2017 from 50% to 100% of an eligible asset’s cost by the Tax Cuts and Jobs Act of 2017 (TCJA). However, after 2022, the 100% decreases by 20 percentage points until it reaches 0% in 2027. This means that unless Congress extends the bonus depreciation rate, any asset purchased after September 27, 2017, and January 1, 2023, is subject to the 100% bonus depreciation; then starting in 2023, bonus depreciation drops down to 80%, and will continue to reduce over the years. That is 80% for 2023, 60% for 2024, 40% for 2025, 20% for 2026, and 0% for 2027.

When you claim bonus depreciation, you can deduct the cost of your fixed assets in the year that you purchased them and put them to work. Nonetheless, not all assets are eligible for this special depreciation allowance and there are certain restrictions. Let’s further discuss how to claim bonus depreciation and what assets are eligible for this special depreciation deduction.

See also: Adjusting Entry for Depreciation

How to claim bonus depreciation

Once you purchase a depreciable property for your business, depreciating the property is very much required. However, claiming bonus depreciation is optional. If you purchase a property that qualifies for bonus depreciation, and for certain reasons don’t want to write off a large percentage of the cost, you can elect not to take bonus depreciation and use the applicable MACRS depreciation method instead. However, if you want to claim bonus depreciation, let’s look at the necessary steps of how to take bonus depreciation:

Purchase a qualified business asset

First of all, in order to claim bonus depreciation, you have to buy a qualified business property. What property is eligible for bonus depreciation? The majority of fixed assets that you purchase for your business are eligible for bonus depreciation in the year that you purchase them and put them in service. The only major exceptions are lands, buildings, and intangible assets. You are allowed to claim bonus depreciation for tangible assets that have an IRS-dictated useful life of 20 years or less. Hence, assets eligible for bonus depreciation would include furniture, vehicles, machinery, appliances, equipment, and computers.

Intangible assets such as patents and email lists acquired from third parties aren’t eligible for bonus depreciation. Also, you cannot claim this special depreciation allowance on buildings because they get depreciated over 27.5 years under the modified accelerated cost recovery system (MACRS). Nonetheless, bonus depreciation can be claimed on qualified improvement property such as improvements made to the interior of rental property as far as the improvement is made after the building is open for business.

Some listed properties that are used for both business and personal use, such as cameras and vehicles can qualify for bonus depreciation if the asset has been used for business at least 50% of the time. Before only new assets were eligible for bonus depreciation but the TCJA expanded the definition of qualified property to include used property. Hence, in summary, to be able to claim bonus depreciation on a property, the property should not be used by the taxpayer at any time before acquiring it, the property should not be acquired from a related party, and the property should not be acquired as part of a tax-free transaction, such as a like-kind exchange.

Place the property into service

You can’t just claim bonus depreciation by just purchasing an eligible property, you have to place the property in service. This means you have to start using the property in your business before you can take bonus depreciation for the property. For instance, if you bought a piece of equipment in November of 2022, but don’t start using it until January of 2023, you would have no option but to wait until you file your 2023 tax return to be able to claim bonus depreciation on the machinery.

When can you take bonus depreciation? In order to claim bonus depreciation you have to be using the asset. The depreciation clock does not start when you purchase the property but when you place it in service. Hence, the bonus depreciation calculation would depend on the year you placed the property in service. For instance, if you purchased a $10,000 machine in 2022 and put it into service in the same year, you can claim 100% bonus depreciation which means you can deduct the entire purchase with bonus depreciation. However, if you put the said machine into service in 2024, you can’t claim the 100% bonus depreciation for 2022, rather you will depreciate $6,000 ($10,000 purchase x 60% bonus depreciation rate). Then, the remaining $4,000 will be depreciated in future years under MACRS.

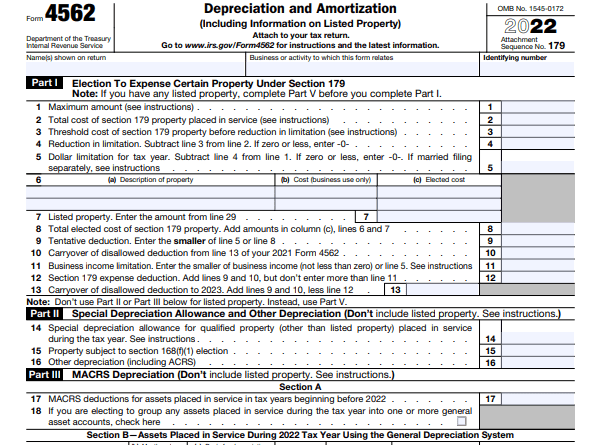

Report bonus depreciation on Form 4562

Lastly, you claim bonus depreciation on your tax return. That is, you write off the bonus depreciation percentage of the cost of the asset on Form 4562, which gets filed along with your business tax return. Basically, how to take bonus depreciation is to report the calculated bonus depreciation on IRS Form 4562, where businesses report depreciation and amortization. This is done under Part II, Line 14 on Form 4562. Also, if you are reporting bonus depreciation for multiple assets, you have to report the total cost.

Read also: Is Accumulated Depreciation an Expense?

Last Updated on November 2, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.