Adjusting entries are the changes made to the journal entries that were already made at the end of an accounting period. These entries adjust the business’s income and expenses to reflect its financial situation more accurately. Knowing how to do adjusting entries is necessary to make your accounting ledger as accurate as possible without having to make any illegal tampering with the numbers.

Adjusting journal entries are recorded at the end of an accounting period after a trial balance is prepared. After journal entries are entered, the initial trial balance is created, then, after making adjusting entries, you will have the adjusted trial balance. Then, these entries are posted into the general ledger in the same way as other accounting journal entries. They are done under accrual accounting which is based on the revenue recognition and matching principle.

Hence, the essence of knowing how to adjust journal entries is to show when money changed hands and to convert real-time journal entries to entries that reflect accrual accounting. These accounting adjustments are usually associated with accruals, deferrals, and estimates. In this article, we will be discussing how to make adjusting entries.

Related: Adjusting entry for inventory

How to do adjusting entries

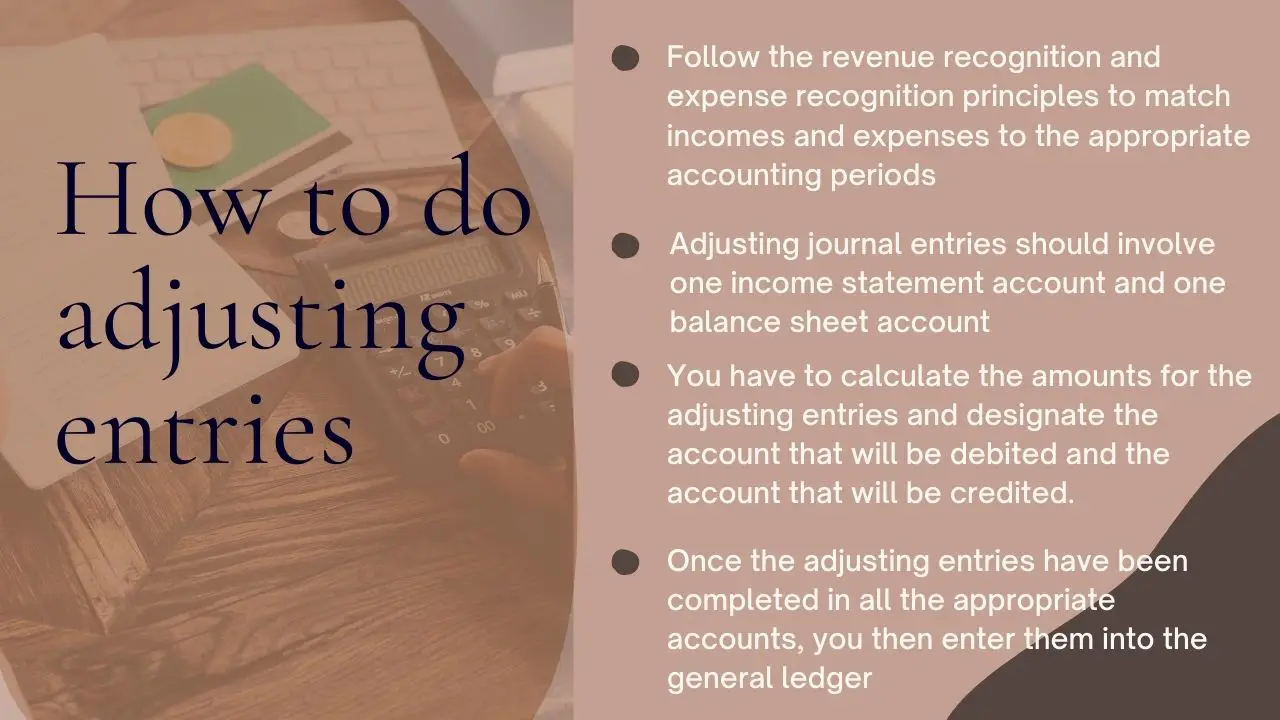

When learning how to do adjusting entries it is important to ensure you follow the revenue recognition and expense recognition principles. This is to match incomes and expenses to the appropriate accounting periods. Hence, adjusting journal entries would involve one income statement account and one balance sheet account. You have to determine the amounts for the adjusting entries and designate the account that should be credited and the account that should be debited. Once the adjusting entries have been completed in all the appropriate accounts, you then enter them into the general ledger. Here are when and how to do adjusting entries:

Make an original entry to record accruals and then make adjustments in the next accounting period

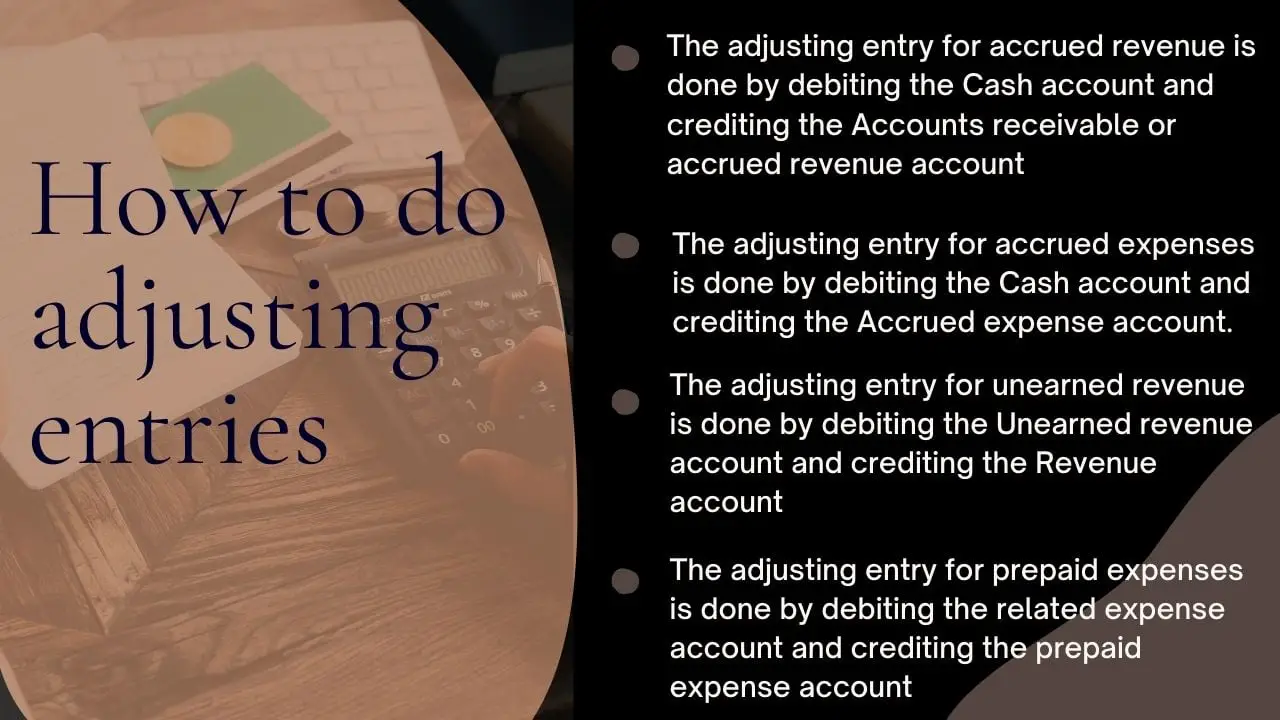

Accruals are transactions that involve unbilled revenues that have not been received or unbilled expenses that have not yet been paid for. You have to make adjusting entries any time sales are conducted in a current accounting period and the customers pay for them in the next accounting period. This is recorded as accrued revenue and an initial journal entry is made to report this, which is a debit to the Accrued revenue account and a credit to the Revenue account. Then, when the customer has been billed, an adjusting entry is made which is a debit to the Cash account and a credit to the Accounts receivable or accrued revenue account.

You have to also make adjusting entries any time an expense is incurred in one accounting period but you are billed in the next accounting period. This is recorded as an accrued expense and an initial journal entry is made to report this, which is a debit to the Accrued expense account and a credit to the related expense account. Then, how to adjust journal entries when you have been billed and make the payment, is to debit the Cash account and credit the Accrued expense account.

Make an original entry to record deferrals and then make adjustments in the next accounting period

Deferrals are transactions that involve revenues that have been received but have not yet been earned or expenses that have been paid in advance but have not yet been used. That is, you have to make adjusting entries when you pay for an expense in advance (deferred or prepaid expenses) or when a client pays for a product or service in advance (unearned or deferred revenue).

You make an original entry to record deferred expenses by debiting the prepaid expense account and crediting the cash account. Then make adjustments in the next accounting period when the prepaid expenses have been used up by debiting the related expense account and crediting the prepaid expense account. For deferred revenue, the initial journal entry for unearned revenue is a debit to the Cash account and a credit to the Unearned revenue account. Then, when the revenue has been earned you make an adjusting entry for unearned revenue which would be a debit to the Unearned revenue account and a credit to the Revenue account.

Record estimates and make adjustments in the next accounting period

Estimates are adjusting entries that are made to record non-cash items, such as allowance for doubtful accounts, depreciation expense, or inventory obsolescence reserve. For depreciation, the adjusting entries are a little bit different than with other accounts. Accumulated depreciation which is a contra-asset account is put into consideration and is used to track depreciation expenses. When accounting for depreciable assets, you make an adjusting entry which is a debit to the depreciation expense account and credit accumulated depreciation.

In business, there is a possibility that you may not collect some debts, so you make use of allowance for doubtful accounts to offset the account. This is used when you offer credit to customers and anticipate that they may miss payments. Hence, you make a debit entry to the bad expense account and a credit to Allowance for doubtful accounts. However, how to make adjusting entries when the customer later pays the debt, is to make a debit entry to the allowance for doubtful accounts and a credit entry to the accounts receivable account.

See also: Types of adjusting entries with examples

Examples of how to do adjusting entries

Here are a few examples of how to do adjusting journal entries:

Example 1: how to make adjusting entries for accrued revenue

In February, Mr. John sells $3,000 worth of goods to a client and sends the invoices. However, the client pays the invoice on March 10. In order to accurately reflect the income for the month, he needs to show the revenue he generated in his books. Hence, he would debit the accrued revenue account and credit the revenue account. Then, on March 7, when the customer pays Mr. John for the goods, this is how to do adjusting entries to record the payment of the accrued revenue:

| Date | Account | Debit | Credit |

|---|---|---|---|

| March 7 | Cash | $2,400 | |

| Accrued revenue | $2,400 |

Example 2: how to do adjusting entries for accrued expenses

The amount of electricity that ABC company used amounted to $10,000 for the month of October but is yet to be billed. On October 31st, the company records this expense by making a debit entry of $10,000 to the electricity expense account and a credit entry of the same amount to the Accrued expense account. On November 1, the company received the electricity bill and wrote a check to the electric company on November 2. This is how to make adjusting entries to record the payment of the accrued utility expense:

| Date | Account | Debit | Credit |

|---|---|---|---|

| November 2 | Accrued revenue | $10,000 | |

| Cash | $10,000 |

Example 3: how to do adjusting journal entries for deferred expenses

A common example of a prepaid expense is prepaid rent, prepaid insurance, or a company buying and paying for office supplies. Assume you buy office supplies for your business worth $5000. To record this you make a debit entry of $5,000 to the Office supplies account and a credit entry to the Cash account. As these office supplies are used they become an expense. If at the end of the month, $1,500 worth of office supplies have been used, this is how to do adjusting entries to record the supplies expense:

| Account | Debit | Credit |

|---|---|---|

| Supplies expense | $1,500 | |

| Office Supplies | $1,500 |

Example 4: how to do adjusting entries for unearned revenue

Let’s assume you’re paid $3,000 in January to carry out home renovations and makeover services for a client. You’ve received payment for your services but haven’t yet earned it. Thus, you will record the income on the books for January as a debit to the Cash account and a credit entry to the Unearned revenue account. Let’s say you deliver the service in March and eventually earned the revenue, this is how to do adjusting entries to record the earned revenue:

| Date | Account | Debit | Credit |

|---|---|---|---|

| March | Unearned Revenue | $3,000 | |

| Service Revenue | $3,000 |

Example 5: how to adjust journal entries for allowance for doubtful accounts

A business delivers products to a client for $6,000 and the customer made a deposit of $2,000 at first and the business offered credit payments for the remaining $4,000. This is how to adjust journal entries if the business anticipates the customer may not pay:

| Account | Debit | Credit |

|---|---|---|

| Bad debts expenses | $4,000 | |

| Allowance for doubtful accounts | $4,000 |

However, if the customer later pays the debt, the journal entry will be a debit to the allowance for doubtful accounts and a credit to the accounts receivable account.

Example 6: how to do adjusting entries for depreciation

A delivery company purchased a new truck for $35,000. After a year of delivering and using the truck, its value decreases by $5,000. When filing their taxes, the company pays a one-time $5,000 fee; this is how to do adjusting entries for depreciable assets:

| Account | Debit | Credit |

|---|---|---|

| Depreciation expenses | $5,000 | |

| Accumulated depreciation | $5,000 |

Read also: Adjusting Entry for Prepaid Insurance

Last Updated on November 3, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.