Income statement ratios are important when analyzing the income statement of a company. The income statement ratios formulas are created using the numerical values on the income statement and aid business owners and investors alike to get a better understanding of what the numbers say about the company. The numbers found on a company’s statement of operations, balance sheet, and cash flow statement can be used to analyze and assess the growth, profitability, valuation, liquidity, margins, rate of returns, etc. of a company.

In order to use the income statement ratios to understand the profitability of a company, the business owner or investor, or whoever wishes to make the analysis has to understand what numbers to use and which of the income statement ratios is applicable to the particular analysis. Here, we shall discuss the various income statement ratios and their uses. We shall also look at the income statement ratios formulas and examples of how these formulas are used in calculations.

See also: Balance sheet substantiation

What are income statement ratios?

The income statement ratios are also referred to as the profitability ratio. These ratios are useful tools when measuring a company’s ability to generate income compared to its revenue, physical and nonphysical assets, equity, and operating costs.

These ratios aid to analyze the company’s performance in the market within a stipulated time. Although the income statement and balance sheet show the company’s profit and its current financial standing, it does not really tell how well the company performs within the period. Hence the need to understand the income statement ratios because these ratios help both external and internal users to make sense of the numbers on the income statement.

The external user of the income statement ratios include investors, creditors, regulatory authorities, analysts, competitors, industry observers, and tax authorities. The internal users include the company employees, management, owners, and all people that are directly associated with the company.

Additionally, the income statement ratios are very useful when they are used to compare different financial periods within the company or to compare different companies within the same industry. When used in this way, the income statement ratios can tell the user how well the company is doing in comparison to its previous performance or its competitors within the same industry.

Uses of income statement ratios

- Predicting a company’s future performance

- Comparing companies within the same sector

- Tracking the company’s performance

Predicting a company’s future performance

When the income statement ratios are used to find the various values in previous accounting periods of the company and a trend of growth has been discovered, the company or its investors can use these figures to predict what the company’s future performance might be like.

For example, if a company’s assets turnover ratio increased over the years from 0.5 to 2, it means that the company is effectively utilizing its assets and has increased its turnover from fifty cents to two dollars and thus has a good growth prospect.

Comparing companies within the same sector

When a company or investors want to understand if a company is doing well financially or not, the income statement ratios can be used to compare the company’s performance with that of industry leaders or other competitors within the same industry in order to ascertain if they are doing worst or better than the company that was used in the comparison.

For instance, the earnings per share of companies within the same sector can be used as a comparison tool to determine which company is a better investment option due to its having higher earnings per share ratio.

Tracking the company’s performance

When an investor or company owners want to understand their evaluate their financial performance and understand if there is a trend of growth, decline, or stagnation, they can compare the results gotten when the income statement ratios are used to see the trend in their finances through the years.

For instance, the result of a company’s gross profit ratio calculation can indicate how much per dollar the company spends on its cost of goods sold and how much is available for other expenses. When this is checked for different years and compared side by side with that of other companies within the same industry, it gives a better picture of the resources available to the company for various purposes.

Limitations of income statement ratios

Although the income statement ratios are useful metrics when evaluating a company’s profitability, quality, growth, and financial strength. They are limited because they do not take any of the following into account.

- The overall financial health of the industry sector that the company operates in.

- Changes in government regulations.

- Changes in the company leadership or structure

- International trade developments are especially necessary for corporations with a global presence.

- Scandals and other happenings within the company could lead to bad press which can conversely affect the company’s stock price and its public perception.

Additionally, the income statement ratios only look at the finances of the company under review or at best, compare companies within the same sector.

See also: Financial leverage ratios

List of the income statement ratios

- Assets turnover ratio

- Earnings per share (EPS) ratio

- Gross margin ratio

- Net profit margin ratio

- Operating margin ratio

- Price-to-earnings (P/E) ratio

- Return on assets (ROA)

- Return on equity (ROE)

- Times interest earned (TIE)

The income statement ratios are often used to analyze a company’s transactions within a stipulated period and are most meaningful when used to compare the results of these ratios from other years or the planned ratios the company wants to attain or the industry average within the sector in which the company operates or the ratios of its competitors. We shall discuss each of these ratios below.

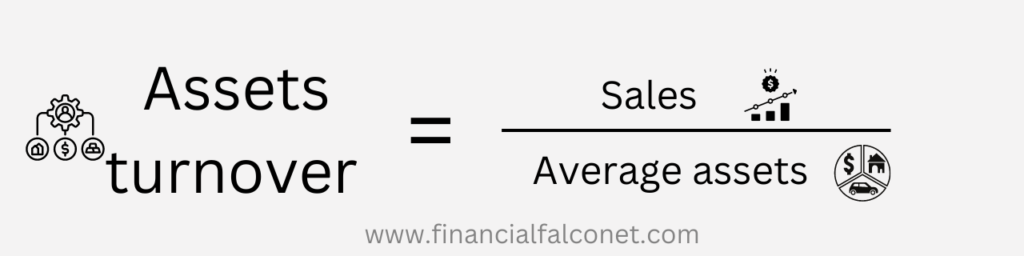

Assets turnover ratio

The assets turnover ratio is one of the income statement ratios, it measures how well a company utilizes its assets to generate sales. This is done by comparing the amount realized from sales and the value of the company’s average total assets. A variation of the assets turnover ratio uses the company’s sales compared to only its fixed assets.

When a company has a high turnover ratio, it means the company is utilizing its assets efficiently in generating sales. On the other hand, a low assets turnover ratio shows that the company’s use of its assets to generate sales is not efficient.

For example, if a company records $600,000 in sales, its beginning assets are valued at $450,000 and its ending assets are valued at $1,000,000 in its income statement. An investor seeking to invest in this company can calculate the company’s assets turnover ratio to determine if they are efficiently using their assets to make sales.

We can calculate the company’s assets turnover ratio using

Assets turnover = Sales ÷ Average assets

Sales = $600,000

Average assets = (Beginning assets + ending assets) ÷ 2 = ($45,000 + $1,000,000) ÷ 2 = $1,045,000 ÷ 2 = $522,500

Assets turnover = $600,000 ÷ $522,500

Assets turnover = 1.15

From the above, the investor can see that the company makes one $1.15 profit from utilizing its assets to make sales.

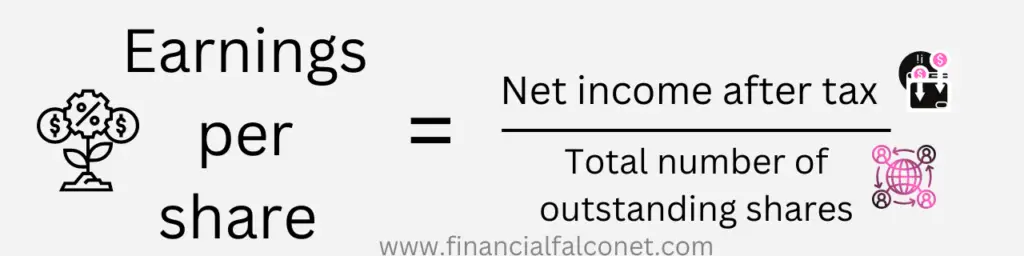

Earnings per share (EPS) ratio

One of the most common income statement ratios is the earnings-per-share ratio. In the world of finance, the earnings-per-share ratio is a very popular metric that is used by investors to determine a company’s ability to generate profits that could be distributed to holders of common stock as dividends for their ownership stake in the company. It combines information gotten from a company’s income statement and its balance sheet.

The EPS ratio uses the difference between a company’s net income or net sales and the dividends paid to holders of a preferred stock divided by the number of common stocks that the company has. The earnings per share of a company is a key determinant of its share price because of its use in calculating the price-to-earnings ratio of a company.

Whether a company’s EPS is good or not depends on its growth rate, goals, stock price stability, and the industry average amongst many other factors. Generally, high earnings per share ratio mean that a company makes enough profits that can cover the distributions paid to its shareholders.

Investors usually use the EPS ratio of a company to have an idea of the earnings they could make by investing in the company as well as predict the company’s future growth. Additionally, EPS is also used by investors to compare share prices, this aids in determining if the share price is undervalued, well-valued, or overvalued.

There are instances when companies buy back some of their common stock, these bought-back shares are referred to as treasury stocks. When this share buyback occurs, it reduces the number of common shares that have been issued, as such, the company’s earnings per share will increase. This is because its net income will be divided by a smaller number of common stock which will in turn make the market value of the company’s common stock increase.

Publicly traded companies usually report their net income after they have paid income tax as earnings per share on their income statement. Additionally, the calculation to find out a company’s EPS is dependent on if the company issued only common stocks or has issued both common and preferred stock and other securities that could be converted to common stock in the future such as convertible preferred stock or has issued more common stocks within the accounting period in view.

Assuming Walmart has 1,000 preferred shareholders who receive annual dividend payments of $50,000 and they have 120,000 common shareholders. If they do not issue additional share throughout the year in view and reports a net income after tax of $1,000,000. We can calculate Walmart’s earnings per share after determining the earnings that will be available to the common shareholder using

Earnings available to common stockholders = Net income after tax – Dividend to preferred stockholder

Earnings available to common stockholders = $1,000,000 – $50,000

Earnings available to common stockholders = $950,000

We can now find out the earnings per share of Walmart using

Earnings per share ratio = Earnings available to common stockholders ÷ Total number of outstanding common stock

Earnings per share ratio = $950,000 ÷ 120,000

Earnings per share ratio = $7.92

This means that the holders of common stock in Walmart could get dividends of up to $7.92

Gross margin ratio

Another income statement ratio is the gross margin ratio that compares a company’s gross profit to its net sales or its net sales to the cost of goods sold (COGS) to determine how much profit the company makes after paying its cost of goods sold. This is the same as finding the gross profit of a company as a percentage of its net sale. The gross margin ratio is also referred to as the gross margin profit ratio.

The gross margin ratio of a company is often used by financial analyst to determine if a company was able to maintain its gross margin, especially during periods of increasing competition in the sector in which they operate, or if they were able to increase the selling price of their products when there is an increase in costs and other factors of production. For companies that sell goods, their COGS and net sales are two of the largest amounts found on their income statement.

It should however be noted that when using the gross margin ratio to compare companies, there might be some differences in results even with companies operating in the same sector. The difference may arise due to differences in marketing strategy, periods of deflation or inflation, and the accounting principles the company applies when calculating various items on its income statement such as its cost of goods sold, stock repurchase, etc.

Most US companies use the last in, first out (LIFO) method where the most recently produced goods are recorded as first sold. The use of LIFO generally reduces the amount of income tax a company is liable to pay in times of inflation but the company has to meet up with certain standards set by the Internal Revenue Service (IRS) especially when they have branches outside the US. The other accounting standard used by most companies in other countries and some US companies since the ban of the LIFO method by the International Financial Reporting Standards Foundation (IFRS Foundation) in 2003 is the first in, first out (FIFO) method where the older goods are recorded as first sold.

For example, if a company records a revenue of $150,890 and the cost of goods sold is $50,890. We can calculate the gross profit margin of the company using

Gross margin ratio = Gross profit ÷ Revenue

Gross profit = Revenue – Cost of goods sold = $150,890 – $50,890 = $100,000

Revenue = $150,890

Gross margin ratio = $100,000 ÷ $150,890

Gross margin ratio = 0.66

This means that for every dollar the company makes in revenue, $0.66 could be used for other operational expenses of the company while $0.34 is spent on the cost of goods sold.

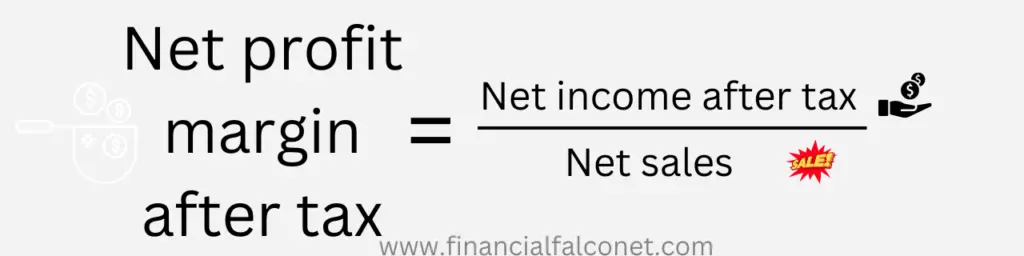

Net profit margin ratio

One of the most common income statement ratios is the profit margin ratio, this ratio is used to measure a company’s profitability by showing how much a company makes in profit for a dollar of sale. The net profit margin is also referred to as the profit margin ratio.

The profit indicated per sale is usually after all expenses have been deducted from the net sales. The expenses subtracted from the net sales include the cost of goods sold (COGS), income tax, interest expenses, selling, general and administrative (SG&A) expenses. In addition to the expenses already mentioned, salaries and fringe benefits are also included, and there is also compensation earned by stockholders who work in the company.

For partnerships and sole proprietorships where the business owners do not have regular salaries or get paid other compensations, their profit margins cannot be compared to companies whose owners earn salaries and other compensations. This is because the profit margins of the prior mentioned type of partnership or sole proprietorship will likely have lesser expenses accruing from salaries and compensations since the owners get draws that are not listed as expenses.

When comparing the profit margins of companies, whether the company is a corporation, limited liability company, partnership or sole proprietorship should be considered. Generally, corporations and limited liability companies report income tax for their businesses in their income statement while partnerships and sole proprietorships, do not report income tax as a business, instead, the owners file personal income tax returns. Hence, salaries, fringe benefits, and income tax do not appear on the income statement report of partnerships and sole proprietorships.

Determining whether a company’s profit margin is good or bad depends on the company’s previous profit margin figures, the profit margin figures in the sector in which the company operates, the planned profit margin figures the company hopes to attain, etc.

In order to calculate a company’s profit margin, it can be calculated before tax payment or after-tax payment. For calculating the profit margin before tax, the company’s net income before tax is divided by its net sales. For calculating the profit margin after tax, the company’s net income after tax is divided by its net sales.

For example, if a company has $10,000,000 in net sales after the deduction of sales discounts, allowances, and returns. If its cost of goods sold and interest expenses were $7,000,000 and $60,000 respectively, while its income tax and selling, general, and administrative expenses totaled $2,200,000. The profit margin of the company can be calculated using

Net profit margin after tax = Net income after tax ÷ Net sales

Net income after tax = Net sales – (Cost of goods sold + interest expenses + Income tax + Selling, general and administrative expenses) = $10,000,000 – ($7,000,000 + $600,000 + $2,200,000) = $10,000,000 – $9,800,000 = $200,000

Net sales = $10,000,000

Net profit margin after tax = $200,000 ÷ $10,000,000

Net profit margin after tax = 0.02

Our calculation shows that the company was able to make 0.02 or 2% in profits from sales after the deduction of all expenses and taxes.

Operating margin ratio

The operating margin ratio is one of the income statement ratios that is used to gauge the profits a company makes from its operations before the payment of taxes and interest charges and how well they manage this profit. It additionally ascertains the operating efficiency of a company as it shows how much revenue the company has after taking care of variable costs such as raw materials and wages.

When the operating margin of a company keeps fluctuating through the years, with variable high and low figures, it serves as an indicator of high risk in the business. Hence investors mostly consider the profit margin of companies they wish to invest in. This aids them to understand how much profit the company is making compared to its total revenues and how well the company margins have improved over the years.

The operating margin of a company can be calculated by dividing its operating income by its net sales. The operating margin of a company can improve through improved product pricing, efficient use of resources, effective marketing of products, and better management of operations. The operating margin ratio is also referred to as the earnings before interest and tax (EBIT) margin or the return on sales or the operating profit margin.

For example, if a business reports $450,000 as its gross revenue and has operating expenses totaling $225,000. We can calculate its operating margin using

Operating margin ratio = Operating income ÷ Net sales

Operating income = Gross revenue – Operating expenses = $450,000 – $225,000 = $225,000

Net sales = Gross revenue = $450,000

Operating margin ratio = $225,000 ÷ $450,000

Operating margin ratio = 0.5

From the above, it means that for every dollar of sale made by the company, they make a profit of 50 cents.

Price-to-earnings ratio

The price to earnings ratio which is also referred to as P/E ratio or pe ratio or PER is an income statement ratio that is widely used for stock valuations. This income statement ratio shows the amount that an investor needs to put into a business through a share purchase in order to receive a dollar from the company’s earnings. It is, therefore, the part of a company’s net earnings that could be earned per share if all profits were distributed to shareholders.

Investors and analysts use the earnings per share value to understand the financial strength of a company. A high P/E ratio indicates that the share price is high compared to the company’s earnings while a low P/E ratio indicates that the share price is low compared to earnings. The earnings power share can be calculated by dividing the company’s market capitalization by its net income.

For example, if a manufacturing company has a market capitalization of $4,000,000 and its net income is $1,500,000 we can calculate its price-to-earning ratio using

Price to earnings ratio = Market capitalization ÷ Net income

Price to earnings ratio = $4,000,000 ÷ $1,500,000

Price to earnings ratio = 2.67

Hence, the above translates to investing $2.67 for every $1 dollar earned annually.

Return on assets (ROA)

Another important income statement ratio is the return on assets ratio. This ratio measures the profitability of a company compared to its total assets which include both current and noncurrent assets. The current assets include all resources that can be converted into cash within a fiscal year such as prepaid liabilities and accounts receivable. The noncurrent assets include all resources that cannot be easily converted into cash within one fiscal year such as land, plant, and property.

The ROA ratio shows the efficiency of a company in using its assets to make a profit. The return on assets varies from one company to the next based on its industry sector, hence the need to compare only companies within the same sector or the previous year’s return on assets figure of the company in question when using return on assets as a comparison tool.

Investors use the return on assets ratio to ascertain the efficiency of a company in converting invested capital in the form of assets into profit. A low return on assets shows that the company is not efficiently utilizing its resources while a high return on assets shows that a company is making good use of its assets.

The return on assets can be calculated by dividing the net income of the company by its total assets.

For example, if the net income of a logistics company is $15,000,000. It had only two delivery trucks at the beginning of the year valued at $2,500,000 but by the end of the year, the company purchased more trucks raising the value of its assets to $8,900,000 at the end of the year. We can calculate the return on assets using

Return on assets ratio = Net income ÷ Average total assets

Net income = $15,000,000

Average total assets = (Begining assets + Ending assets) ÷ 2 = ($2,500,000 + $8,900,000) ÷ 2 = $11,400,000 ÷ 2 = $5,700,000

Return on assets ratio = 15,000,000 ÷ $5,7000,000

Return on assets ratio = 2.63

The above result shows that the logistics company made 2.63 x 100% or 26.3% as its return on assets for the year in view

Return on equity (ROE)

Return on equity (ROE) is one of the key valuation metrics shareholders and potential investors use to gauge the percentage of profit a corporation makes after taxes from utilizing the equity of its shareholders otherwise known as the shareholder’s equity. Based on the balance sheet equation, equity is equal to the difference between a company’s assets and its liabilities, hence return on equity is considered the returns realized from a company’s net assets.

In order to calculate the return on equity of a company, its net income is divided by the total number of outstanding common shares. Before calculating a company’s return on equity, if the company has preferred shareholders, their dividends are subtracted from the net income. For companies that have only common shareholders, the net income is directly divided by its total equity without making any subtractions.

For example, if the net income after tax of a clothing company is $200,000 and its total equity is $700,000. We can calculate the company’s return on equity using

Return on equity = Net income ÷ Shareholder’s equity

Net income = $200,000

Shareholders equity -= $700,000

Return on equity = $200,000 ÷ $700,000

Return on equity = 0.2857

The return on equity for the clothing company is thus 0.2857 x 100% or 28.57%

Times interest earned (TIE)

The time interest earned (TIE) ratio is an income statement ratio that measures the ability of a company to meet up with the interest payments on its debt such as bonds payable and loans payable based on the company’s current operating income. The time interest earned ratio is also referred to as the interest coverage ratio.

This ratio measures the credit health of a company; a high times interest earned ratio (from 3 and above) signifies a company that has a high chance of paying off its interest expense in good time while a low times interest earned ratio (below 2) indicates a company that might not be able to meet up with its interest expense payment obligations. Thus lenders generally consider the times interest earned ratio of a company before leading to them in order to ascertain if they can keep up with the interest expense payments for the loan they seek. However, the high and low range of the interest coverage ratio may differ based on the industry sector of a company.

When a company has a high time interest earned ratio, it means the company has adequate cash to service its debt interest payments and still has enough cash to reinvest into the business operations in order to make profits. This high times interest earned ratio value indicates that the company is capable of paying off its interest expense on time thereby signifying its creditworthiness. A low times interest earned ratio shows that the company could be at risk of defaulting on its interest expense payment and hence has little or no room for error in its business operations. This could also mean that the company took on more debt than its cash flow can handle.

In order to calculate the times interest earned ratio of a company, its net income or earnings before income taxes and interest expense (EBIT) is divided by the total annual interest expense for the year in view.

Assuming Amazon’s net income after tax is $20 million and its interest expense and income tax are $5 million and $8 million respectively. We can calculate Amazon’s times interest earned using

Times interest earned = Earnings before interest expenses and income taxes ÷ Interest expense

Earnings before interest expenses and income taxes = Net income after tax + Interst expense + Income tax = $20 million + $5 million + $8million = $33 million

Interest expense = $5 million

Times interest earned = $33 million ÷ $5 million

Times interest earned = 6.6

Since Amazon has a times interest of 6.6 which is within the high range, it means they are a credit-worthy company and can comfortably meet its obligations to make interest expense payments.

Income statement ratios simplified

All the income statement ratios are useful financial metrics that could be used in understanding the profitability of a business hence they are also referred to as profitability ratios. When all these ratios are used side by side, they give a better picture of how well a company is doing per time.

The assets turnover ratio is a metric that is useful when measuring the efficiency of a company in using its assets to generate sales.

The earnings per share (EPS) ratio is commonly used by shareholders to determine the ability of a particular company to generate profits that it could distribute to them as dividends.

The gross margin ratio is useful in understanding how much profit a company makes after it has paid its cost of goods sold.

The net profit margin ratio is a metric that measures how much a company makes in profit per dollar of sale after all expenses have been subtracted from the company’s net sales.

The operating margin ratio can be used to gauge how well a company manages its profits and how much profit they make before the payment of interest expenses and taxes.

Price-to-earnings (P/E) ratio informs investors about the amount they need to invest in a business in order to have a share in its profits.

Return on assets (ROA) is a metric that measures how well a company were able to utilize its assets in order to realize a profit.

The return on equity (ROE) ratio shows company owners and investors alike, the profit a company makes through the effective utilization of its equity. The profit here is usually the one made after the company has taken care of its taxes.

Times interest earned (TIE) ratio measures the creditworthiness of a company by determining if it would be able to meet up with its interest expense payments with its current operating income.

See also: What type of Account is Sales Returns and Allowances?

Income statement ratios formulas

- Assets turnover formula

- Earnings per share (EPS) formula

- Gross margin ratio formula

- Net profit margin ratio formula

- Operating margin ratio formula

- Price to earnings ratio formula

- Return on assets (ROA) formula

- Return on equity (ROE) formula

- Times interest earned (TIE) formula

The income statement ratios formulas are expressions of the various income statement ratios that are useful tools in determining the profitability of a company within a stipulated time frame. They are also useful in determining a company’s quality, efficiency, growth, and financial strength.

The income statement ratios formulas can be used by analysts, company owners, auditors, investors, or any individual or corporate organization to understand how well a company is performing in various aspects. They provide insight into a company’s profitability, operating expenses, cost of debt, and income amongst many other things.

For the Net profit income ratio, return on assets ratio and return on equity ratio, the results gotten after calculations are generally multiplied by 100 in order to get the percentage. Let us take a look at the various income statement ratios formulas below

Assets turnover formula

In order to calculate the assets turnover ratio of a company, its total sales are divided by the average of the sum of its assets at the beginning of the year and its assets at the end of the year.

This is expressed as Assets turnover = Sales ÷ Average assets

Where Average assets = (Beginning assets + ending assets) ÷ 2

Earnings per share (EPS) formula

When it comes to calculating the earnings per share of a company, the formula varies depending on whether:

- The company issued only common shares and did not make additional issues within the period.

- The company in question has both preferred and common stockholders and has issued more common shares within the period under review as well as if they have issued other securities that are convertible to common stock within the period.

Companies that issue only common shares and did not make additional issues within the period thereby having the same number of outstanding shares through the period will have their earnings per share calculated by dividing the company’s net income after the payment of taxes by the total number of shares outstanding.

This is expressed as Earnings per share = Net income after tax ÷ Total number of outstanding shares

For companies that issue both common and preferred stock or other securities that are convertible to common stock, the earnings per share are calculated by first determining the earnings that will be available to the common stockholders. This is because the issuing of preferred stocks affects the amount of distributions that will be available to the common shareholders while the issuing of other securities that are convertible to common stock can lead to stock dilution through the increase in the number of shares outstanding. The earnings per share in such an instance can be calculated by first subtracting the dividend payment that the preferred stockholders will receive if the company declares distributions. This can be expressed

Earnings available to common stockholders = Net income after tax – Dividend to preferred stockholders

The result obtained is then divided by the total number of common stock outstanding as expressed below

Earnings per share ratio = Earnings available to common stockholders ÷ Total number of outstanding common stock

Gross margin ratio formula

The gross margin ratio of a company can be calculated either by dividing its gross profit by its net sale or subtracting the cost of goods sold from its net sale and dividing the result by the net sales. These two formulas can be expressed as

Gross margin ratio = Gross profit ÷ Revenue

where Gross profit = Revenue – Cost of goods sold (COGS)

Gross margin ratio = [Net sales – Cost of goods sold (COGS)] ÷ Net sales

Where Net sale = Gross sales – Sales discounts – Sales returns – Sales allowances

Net profit margin ratio formula

When calculating the net profit margin ratio of a company there are two available formulas; one is the net profit margin before tax which divided the net income of the company before the payment of taxes by its net sales. The other formula divides the company’s net income after its tax obligations have been taken care of by its net sales. These formulas can be expressed as

- Net profit margin after tax = Net income after tax ÷ Net sales

- Net profit margin before tax = Net income before tax ÷ Net sales

Operating margin ratio formula

The operating margin ratio formula divides the company’s operating income by its net sales. This is expressed as

Operating margin ratio = Operating income ÷ Net sales

Where Operating income = Gross revenue – Operating expenses

Net sales = Gross revenue

Price to earnings ratio formula

When it comes to calculating the price-to-earnings ratio of a company, two variants are available. One divides the company’s market capitalization by its total net earnings while the other divides the company’s stock price by the earnings per share. The formulas are expressed as

Price to earnings ratio = Market capitalization ÷ Total net earnings

Where Market capitalization = Current share price x Total number of outstanding shares

Price to earnings ratio = Current share price per share ÷ Earnings per share

Where Earnings per share = Net income after tax ÷ Total number of outstanding shares

Return on assets (ROA) formula

In order to calculate the return on assets of a company, its net income is divided by its average total assets. This is expressed as

Return on assets ratio = Net income ÷ Average total assets

Where Net income = Total revenue – Total expenses

Average total assets = (Begining assets + Ending assets) ÷ 2

Return on equity (ROE) formula

The formula for calculating the return on equity for a company depends on whether or not the company has preferred stockholders or not. For companies that have preferred stockholders, the dividend payments to these stockholders are subtracted from the company’s net income before dividing the result by the common shareholder’s equity. For companies that issued only common shares, the company’s net income is divided by its total equity. These two variations are expressed as

Return on equity = Net income ÷ Shareholder’s equity

Where Net income = Net income – Preferred dividends

Shareholders equity = Total equity – Preferred equity

Return on equity = Net income ÷ Shareholder’s equity

Where Net income = Total revenue – Total expenses

Times interest earned (TIE) formula

The times interest earned by a company can be calculated by dividing its earnings before interest and taxes by its interest expense. This is expressed as

Times interest earned = EBIT ÷ Interest expense

Where EBIT = Earnings before interest expenses and income taxes

See also: Market Prospect Ratios

Income statement ratios calculations and examples

Assuming a liquor-producing company has the following income statement and balance sheet

| Income statement | 2022 |

|---|---|

| Revenue | $ |

| Cash sales | 90,000 |

| Credit sales | 57,800 |

| Total Revenue | 147,800 |

| Cost of goods sold | 75,900 |

| Gross profit | 71,900 |

| Operating expenses | |

| Salaries | 30,000 |

| Advertising | 4,600 |

| Office rent | 10,120 |

| Utilities | 2,670 |

| Office Supplies | 800 |

| Depreciation | 3,490 |

| Other expenses | 3,600 |

| Total operating expenses | 55,280 |

| Operating profit | 16,620 |

| Operating income | |

| Interest Income | 2,000 |

| Interest expenses | 2,400 |

| Net Income before Tax | 16,220 |

| Income tax expenses | 4,540 |

| Net Income after Tax | 14,680 |

| Balance sheet | 2022 | 2021 |

|---|---|---|

| Current assets | $ | $ |

| Cash and cash equivalents | 15,217 | 13,580 |

| Receivables | 4,000 | 3,220 |

| Inventories | 11,060 | 8,800 |

| Other current assets | 3,250 | 2,850 |

| 33,527 | 28,450 | |

| Non-current assets | ||

| Equipment | 70,780 | 70,780 |

| Vehicles | 87,500 | 87,500 |

| Accumulated depreciation | (19,700) | (19,700) |

| 138,580 | 138,580 | |

| Total assets | 172,107 | 167,030 |

| Current liabilities | ||

| Interest payables | 900 | 878 |

| Account payables | 9,600 | 3,700 |

| Accruals | 3,760 | 2,150 |

| Other current liabilities | 4,455 | 3,729 |

| 18,715 | 10,457 | |

| Non-current liabilities | ||

| Note payables | 30,000 | 43,000 |

| 30,000 | 43,000 | |

| Total liabilities | 48,715 | 53,457 |

| Equity | ||

| Share capital | 80,000 | 80,000 |

| Retained earnings | 29,072 | 20,500 |

| Profit/(Loss) current year | 14,340 | 13,073 |

| Total Equity | 123,392 | 113,573 |

| Total liabilities and equity | 172,107 | 167,030 |

Let us assume that the total number of outstanding shares is 70,000; the market value per share is $2 and the company has no preferred shares.

Using the above information, we can calculate the values of its various income statement ratios as follows

Assets turnover = Sales ÷ Average assets

Sales = $147,800

Average assets = (Assets form 2021 + Aaaset from 2022) ÷ 2 = ($167,030 + $172,107) ÷ 2 = $339,137 ÷ 2 = $169,568.5

Assets turnover = $147,800 ÷ $169,568.5

Assets turnover = 0.872

Earnings per share = Net income after tax ÷ Total number of outstanding shares

Net income after tax = $14,680

Total number of outstanding shares = 70,000

Earnings per share = $14,680 ÷ 70,000

Earnings per share = $0.209

Gross margin ratio = Gross profit ÷ Revenue

Gross profit = $71,900

Revenue = $147,800

Gross margin ratio = $71,900 ÷ $147,800

Gross margin ratio = 0.486

Net profit margin after tax = Net income after tax ÷ Net sales

Net income after tax = $14,680

Net sales = Gross sales – Sales returns – Allowances – Discounts

but since the liquor company did not report sales returns, allowances or discounts, the net sales will be the same as the total revenue of $147,800

Net profit margin after tax = $14,680 ÷ $147,800

Net profit margin after tax = 0.099

Net profit margin before tax = Net income before tax ÷ Net sales

Net income before tax = $16,220

Net sales = $147,800

Net profit margin before tax = $16,220 ÷ $147,800

Net profit margin before tax = 0.109

Operating margin ratio = Operating income ÷ Net sales

Operating income = Gross revenue – Operating expenses = $147,800 – $55,280 = $92,520

Net sales = Gross revenue = $147,800

Operating margin ratio = $92,520 ÷ $147,800

Operating margin ratio = 0.626

Price to earnings ratio = Current share price per share ÷ Earnings per share

Current share price per share = $2

Earnings per share = $0.209

Price to earnings ratio = $2 ÷ $0.209

Price to earnings ratio = 9.569

Return on assets ratio = Net income ÷ Average total assets

Net income = Total revenue – Total expenses = $147,800 – $55,280 = $92,520

Average total assets = (Assets form 2021 + Assets from 2022) ÷ 2 = ($167,030 + $172,107) ÷ 2 = $339,137 ÷ 2 = $169,568.5

Return on assets ratio = $92,520 ÷ $169,568.5

Return on assets ratio = 0.546

Return on equity = Net income ÷ Shareholder’s equity

Net income = Total revenue – Total expenses = $147,800 – $55,280 = $92,520

Shareholder’s equity = $80,000

Return on equity = $92,520 ÷ $80,000

Return on equity = 1.157

Times interest earned = EBIT ÷ Interest expense

EBIT = Earnings before interest expenses and income taxes = $16,620

Interest expense = $2,400

Times interest earned = $16,620 ÷ $2,400

Times interest earned = 2.621

See also: Treasury stock debit or credit?

Conclusion

The income statement ratios are key performance indicators that are used to ascertain the performance of a particular corporation in comparison to its competitors over time or to its previous records. Thes ratios aid investors, business owners, analysts, and all other corporate organizations or individuals that use them to better understand the figures found on the income statement of companies.

They are also useful in comparing companies within the same industry sector, understanding a company’s performance trend, and gaining insight into a business operation. Thus, they aid in determining the profitability, growth, efficiency, strength, and quality of a business.

The various income statement formulas when used also provide insight into the revenue, cost of debt, operating expense, and equity and assets utilization by businesses. It is however best to use the income statement ratios along with other company evaluation metrics in order to have a full picture of the financial stability of a company.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.