Is sales discount an expense? Trade discounts and sales discounts are the two main types of discounts in accounting that might occur in businesses. Trade discounts take place when the seller reduces the sales price for a wholesale customer, such as on bulk orders. A sales discount, on the other hand, occurs when a seller offers a sales price reduction to a customer as an incentive to pay an invoice within a certain time.

Hence, sales discount is recorded in a separate account from the sales revenue account. It is reported on the income statement as a reduction of the sales revenue. Therefore, when reporting sales discounts in accounting, the amount of total sales discounts for an accounting period is reported on a line item called ‘Less: Sales Discounts’. For example, if a small business had $500 in sales discounts during an accounting period, it will be reported on the income statement as ‘Less: Sales discounts $500.’ It is usually listed below the sales revenue line on the income statement.

This means that the sales discount that was issued during the accounting period cost the business $500. This might sound like an expense for the business. However, in accounting a sales discount is not treated as an expense account but as a contra-revenue account. This article aims to answer the question ‘is sales discount an expense?’. Hence, we will discuss sales discount, expense, and why sales discount is not an expense.

Related: Is accumulated depreciation a fixed asset?

What is sales discount?

A sales discount also known as a cash discount or early payment discount is the reduction that a seller gives to a customer on the invoiced price of goods or services in order to incentivize early payment. That is, the seller gives the customer an opportunity to pay a lesser amount for the goods or services that are purchased when the customer pays within the stated discount periods. The seller usually states the standard condition (terms of sales discount) at which the discount may be taken by the customer in the header bar of the invoices issued.

A common example of the terms of sales discount is the ‘2/10 net 30‘ which means that the seller has offered the customer an opportunity to take a 2 percent discount if he or she pays the invoice within 10 days of the invoice date. Therefore, if the customer doesn’t pay within 10 days, the customer doesn’t get the discount and pays the full price of the goods or services within 30 days after the invoice date. Another common example is the ‘1/10 net 30‘, whereby the customer takes a 1 percent discount in exchange for paying within 10 days of the invoice date. Hence, if not met, the customer makes the full-price payment within 30 days after the invoice date.

Businesses offer a sales discount in order to incentivize their buyers or customers to pay invoices in a timely manner. This is because when a company’s invoices are settled early, the amount of time that the business is extending credit will be reduced which in turn improves cash flow and also reduces the risk of invoice aging and bad debt.

Therefore, companies that offer small discounts for a 10-day payment return are able to clear their accounts quickly. However, as customers take advantage of the sales discount, the overall revenue figures for the business tend to reduce. This sacrifice is, nonetheless, done by businesses in order to encourage early payments and reduce bad debt. In addition, early payments support the liquidity position of the company and reduce the company’s outstanding accounts receivable.

Example of sales discount

Let’s look at an example to understand sales discounts. Assume, Company ABC sold $100 worth of goods to a customer who will pay the invoice at a later date. Company ABC will record this transaction as a debit of $100 to accounts receivable and a credit of $100 will be made to the sales revenue account.

Let’s say Company ABC offered the customer a sales discount term of ‘2/10 net 30’. If the customer eventually makes an early payment for the goods within 10 days and takes advantage of the sales discount, the amount of the sales discount would be subtracted from the full invoice amount to determine the amount of cash that Company ABC will receive from the customer as payment for the invoice.

The customer received a 2 percent discount on the $100 for paying early, and as such will pay $98 instead of $100 (i.e $2 discount is subtracted from $100). In order to record this transaction, Company ABC’s Cash account would be debited by the amount of $98 cash received from the customer and the Sales discount account would be debited by the amount of $2 discount. That is debit cash by $98 and debit sales discounts by $2.

These debit entries would increase the cash and sales discount accounts. While a credit entry of the full invoice amount of $100 would be made to the accounts receivable account in order to remove the invoice amount from the accounts receivable.

Now, that we have an understanding of sales discount, is sales discount an expense? Let’s look at what is considered an expense in accounting in order to answer this.

See also: Is the capital stock a debit or credit?

Expense in accounting

An expense is an operational cost that a business incurs in order to generate revenue. Expenses are the expenditures that allow a company to operate, which involve the cost that a company needs to spend on the daily operation of its business. Examples of expenses include equipment depreciation, employee wages, depreciation expense, payments to suppliers, cost of goods sold, entertainment, advertisement, office supplies expense, etc.

Expenses and revenues are usually reported in a company’s income statements. Hence, a company’s net profit is the total revenue generated minus its expenses. That is, in order to calculate the profitability of a business, expenses are deducted from revenue. Revenue is reported on the credit side while expenses are recorded on the debit side of the profit and loss report in order to measure a business’s profit and losses.

From our understanding of sales discount, it is evident that sales discount is associated with revenue rather than expenses. When a customer takes advantage of a sales discount, the amount that the customer was supposed to be paid is reduced by a certain percentage which literally means that the customer bought the goods at slightly lower prices.

This means that the revenue that the business earned is reduced by a certain percentage. The disadvantage of this is to the seller as the seller bears the brunt of lower revenue due to sales discounts. Hence, offering a sales discount is like an extra cost for the seller which may seem like an expense that the seller expends. However, that is not the case, offering a sales discount reduces revenue and so is treated as a contra revenue rather than an expense. This means that a sales discount is not an expense but a contra-sales account. Let’s discuss this further.

Related: What type of account is retained earnings?

Is sales discount an expense?

No, a sales discount is not an expense but a contra-revenue account. That is, a sales discount as a contra-revenue account takes into account the value of price reductions that are granted to buyers or customers in order to incentivize early payments. Sales discounts together with other contra revenue accounts like sales returns and sales allowances are deducted from a company’s gross sales in order to arrive at the company’s net sales. Hence, a sales discount is not an expense but a contra-revenue account.

Sales discount is reported on the income statement to offset a company’s gross sales, which in turn results in a smaller net sales figure. As a contra revenue account, a sales discount has a debit balance that reduces gross sales revenue which has a credit balance on an income statement. Contra revenue accounts are expected to have a debit balance that is contrary to the normal credit balance of revenue. Hence, sales discounts as well as sales returns and allowances offset sales revenue in order to report the net sales that are generated by a business for an accounting period. Therefore, their debit balance will be the deductions from sales (gross sales) which reports the net sales.

On the income statement, contra-revenue accounts are reported separately from the gross sales revenue to show the discounts, allowances, and returns that reduced the original total value of the sale to the net amount. This is more informative for the reader of the financial statements rather than when only the company’s net balance is reported on the income statement. With the use of a contra-revenue account, the reader of the income statement will be able to differentiate between the original amount of sales revenue generated, the sales reduction, and the resulting net amount.

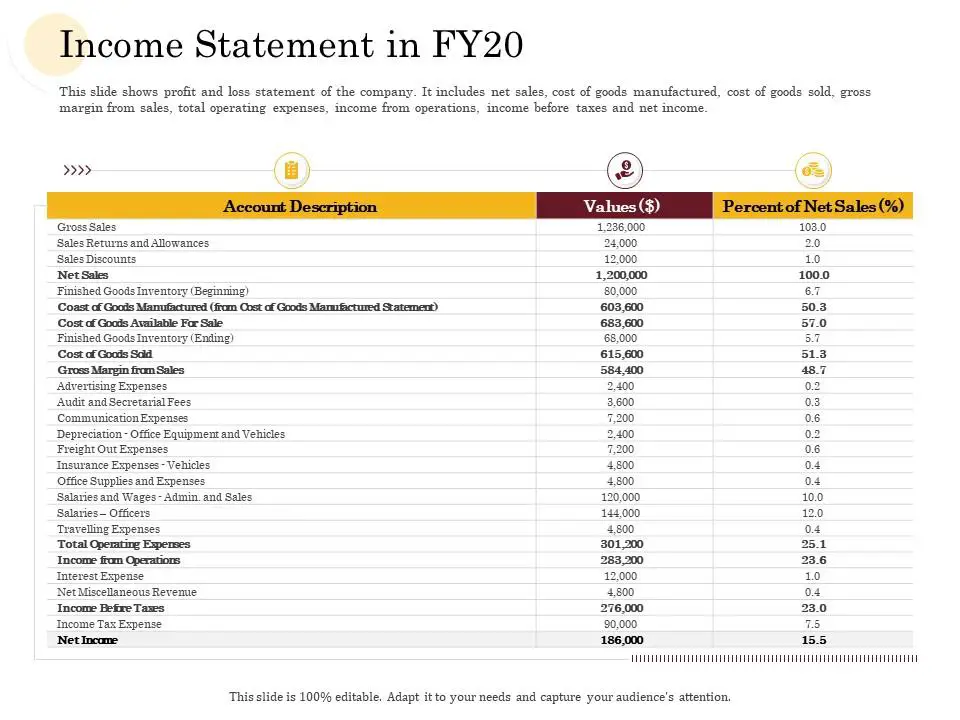

Below is an example of a sales discount on an income statement as a contra-sales account that reduces the gross sale to give the net sales amount:

Source: www.slideteam.net

As seen in the income statement above, sales discount comes under Gross sales which is in the revenue section, and not in the expenses section. It is usually advisable to use a sales account and a contra-sales account when recording sales. The sale account will report the value of an original sale while the contra-sale account will report the details of any sales discounts, returns, and allowance that reduces the value of the original sale.

Hence, reporting a sales discount not as an expense but as a contra-revenue account allows the company to see the original amount of sales as well as the items that reduced the sales to the net sales amount. This is why Sales Returns and Allowances, as well as Sales Discounts, are reported separately from the gross sale as contra-sale accounts on the income statement above.

However, a company may decide to just simply record its net sales in its income statement, rather than reporting the sales discount and gross sales separately. This is normally common when the amount of sales discount is so small that a separate line item presentation does not yield any material additional information for the reader of the financial statement.

See also: Service revenue is what type of account?

Sales discount as a contra revenue account

So ‘is sales discount an expense?’ No, a sales discount is not an expense but a type of contra account that offsets revenue. Sales discounts are reported on the income statement just like with expenses. However, sales discount is on the income statement not as an expense or revenue but as a contra account. Contra accounts are normally presented on the same financial statement as the associated account. This is why sales discount is presented as a line item called ‘Less: Sales Discounts’ below the sales revenue line on the income statement.

Therefore, the sales discount account would appear on an income statement as this:

| Gross sales | 00 |

| Less: sales discounts | 00 |

| Net sales | 00 |

On the income statement, the net revenue/sales balance is calculated as gross sales minus all contra-revenue accounts (Sales discounts, sales returns and allowance). This means that:

Contra revenue = Gross revenue – Net revenue

Furthermore, in a general ledger, contra accounts are used to reduce the value of the associated account when the two are netted together. As a result, the natural balance of a contra account is always contrary to the associated account. Hence, if the natural balance recorded for the related account is a credit, the contra account will record a debit balance. This is why sales discounts as a contra account have a debit balance because revenue has a natural credit balance.

Expenses, on the other hand, also have a natural debit balance; as explained before this is not in any way the reason for sales discount being recorded as a debit. Sales discount is debited as a contra revenue account and not as an expense. Hence, a sales discount is a contra-revenue account and not an expense.

Examples of sales discount as a contra revenue account and not an expense

Let’s look at some examples of how sales discount is treated not as an expense account but as a contra revenue account. In these examples, we will see how sales discount as a contra revenue account is recorded as a debit which is contrary to the natural credit balance of revenue.

Example 1

ABC Ltd sold merchandise to Company RST for a total sales price of $100,000. Say, Company RST is given 30 days to pay the amount and will be granted a 5% discount if it pays within 10 days.

The journal entry to record the merchandise that ABC Ltd sold on credit would be:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Accounts receivable | $100,000 | |

| Sales | $100,000 |

If Company RST is able to take advantage of the discount and pays within the discount period of 10 days, ABC Ltd will record this as:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash ($100,000 – $5,000) | $95,000 | |

| Sales discount ($100,000 x 5%) | $5,000 | |

| Accounts receivable | $100,000 |

As seen in the journal entry made above, the sales discount was recorded as a debit because it has a natural balance that is opposite to the natural credit balance of revenue. Expenses too are debits but in this case, the sales discount is recorded as a debit because it is a contra-revenue account and not an expense.

Furthermore, if this transaction were the only invoice issued by ABC Ltd during the reporting period, and Company RST paid for the merchandise within the reporting period, then the revenue section of ABC’s income statement would look like this:

ABC Ltd Income Statement

| Gross sales | $100,000 |

| Less: sales discounts | $5,000 |

| Net sales | $95,000 |

As seen in the income statement above, the sales discount is a contra-revenue account and not an expense. As a contra revenue account, the sales discount appears on the income statement as a $5,000 reduction from the gross revenue of $100,000 that ABC Ltd reported, which results in net revenue of $95,000.

Example 2

Jenny’s organics sold some skincare products on credit to Miss Mary on the 1st of May, 2022 and the total amount on the invoice was $30,000 which she has to pay on or before the 1st of June 2022. The invoice stated that if Miss Marry makes full payment before 15th May 2022, a 5% discount will be given to her.

Jenny’s organics would record the sale of products to Miss Mary as:

| DATE | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| 1/05/2022 | Accounts receivable | $30,000 | |

| Sales | $30,000 |

Let’s assume, Miss Mary paid the full amount of $30,000 on 10th May 2022 and as such benefited from the discount. Jenny’s organics will enter the following to record this payment on discount:

| DATE | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| 10/05/2022 | Cash ($30,000 – $1,500) | $28,500 | |

| Sales discount ($30,000 x 5%) | $1,500 | ||

| Accounts receivable | $30,000 |

Now, when reporting this on Jenny’s organic’s income statement, the revenue section would look like this:

Jenny’s Organics Income Statement

| Gross sales | $30,000 |

| Less: sales discounts | $1,500 |

| Net sales | $28,500 |

As seen in the income statement report above, the sales discount as a contra revenue account appears as a $1,500 reduction from the gross revenue of $30,000 that Jenny’s organics recorded. This will result in net revenue of $28,500.

Example 3

A manufacturer sells $1000 worth of products to its customer with credit terms of 1/10, n/30.

| DATE | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| 3/11/2022 | Accounts receivable | $1,000 | |

| Sales | $1,000 |

The sale discount terms given mean that the customer can settle the $1000 obligation if he pays $990 ($1000 – $10 of sales discount) within 10 days. The other alternative is for the customer to pay the full $1000 within 30 days. Now, if the customer pays the $990 within 10 days, the manufacturer will record this transaction as follows:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash ($1,000 – $10) | $990 | |

| Sales discount ($1000 x 1%) | $10 | |

| Accounts receivable | $1,000 |

When reporting this, the revenue section on the income statement would look like this:

| Gross sales | $1,000 |

| Less: sales discounts | $10 |

| Net sales | $990 |

As seen, the sales discount is a contra-revenue account that appears as a $10 reduction from the gross revenue of $1000 that the manufacturer reported, resulting in net revenue of $990.

Related: Unearned revenue is what type of account?

Conclusion

Is sales discount an expense? A sales discount is the reduction that a seller gives to a customer on the invoiced price of goods or services in order to incentivize early payment. Hence, a sales discount is not an expense but a contra-revenue account that offsets revenue. Therefore, the natural balance of a sales discount is opposite to the natural credit balance of a revenue account.

Sales discount as a contra revenue account, on the income statement, is reported as a line called ‘Less: Sales Discounts’ below the sales revenue line. It is not considered to be an expense but rather a contra account that appears near the top of the income statement, as a reduction from gross revenue. Hence, the debit balance of the sales discount will be a deduction from sales (gross sales) in order to report the net sales of a company. Hence, in conclusion, a sales discount is not an expense account but a contra-revenue account.

See also: Accumulated depreciation is what type of account?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.