Liabilities and assets usually appear together in business terms. These items make up the components of the balance sheet of a company and are the fundamental elements that shape the financial health of a business. A company’s balance sheet is divided into two categories which are assets on the left and liabilities and equity on the right. The difference between liabilities vs assets is that the former decreases the company’s value and equity while the latter adds value to the company and increases its equity.

The assets of a company are the items that are owned by the company which can provide future economic benefit. Liabilities, on the other hand, are what the company owes other parties. This simply means that assets put money into the company’s account, while liabilities take money out. When it comes to business, balancing your books is one of the most important things, and in order to make good decisions and evaluate the health of a business, the owner needs a solid understanding of liabilities and assets.

With a proper understanding of liabilities and assets, the financial reports of a business will start to have more meaning. The more a business’ assets outweigh its liabilities, the stronger the financial health of the business. But if the business finds itself with more liabilities than assets, it may be on the cusp of going out of business. In this article, we will discuss liabilities vs assets differences, similarities, and examples. But, first of all, let’s have a look at what liabilities and assets are.

Related: Differences between assets, liabilities, and equity

What are liabilities?

Liabilities are the debts and financial obligations of a business such as money owing on a loan, unpaid bills, money owing on a mortgage, IOUs, or any other sum of money that the business owes. It is important to note that expenses and liabilities are not the same. Liabilities are the debts and obligations that a business owes whereas expenses are the costs of a company’s operation.

The liabilities of a business are found on the company’s balance sheet (one of the three major financial statements). A company’s liabilities can be short-term or long-term. Generally, the short-term liabilities of a business are known as current liabilities while the long-term liabilities are called noncurrent liabilities. The majority of businesses organize their liabilities under two separate headings on their balance sheet- current liabilities and noncurrent liabilities.

Types of liabilities

- Current liabilities

- Non-current liabilities

Liabilities are grouped into two types- current (short-term) liabilities and noncurrent (long-term) liabilities depending on their maturity. Lenders are mainly concerned with short-term liquidity and the number of current liabilities, whereas long-term investors use noncurrent liabilities to gauge whether a company is using excessive leverage.

Current liabilities

Current liabilities are also known as short-term liabilities. These are the financial obligations that the company or business has to meet within the present accounting year. They are debts that are due in the next year and typically represent money owed for operating expenses such as wages, taxes and accounts payable.

Moreso, the payments on long-term debt owed in the next year will be listed in current liabilities. For instance, if there is a 30-year mortgage on a building, the next year’s worth of payments owed will be listed in the current liabilities section whereas the remaining balance will be listed in the noncurrent liabilities section.

Accounts payable (AP) and accrued expenses are the two main current liabilities. Accounts payable are obtained when a business purchases a product or service from vendors or suppliers without paying for it. The sum of all outstanding amounts that the business owes to the suppliers or vendors is what is shown as the accounts payable balance on the company’s balance sheet.

Accrued expenses, on the other hand, are other liabilities on the balance sheet that must be paid but don’t have a direct invoice. For instance, a company on its balance sheet may have accrued expenses for items such as employee tax withholding that is withheld from paychecks weekly but only paid quarterly to the government.

Current liabilities examples

- Bank overdrafts

- Sales taxes

- Accounts payable (e.g payments to suppliers)

- Payroll taxes

- Wages

- Income taxes

- Short term loans

- Outstanding expenses

Non-current liabilities

Noncurrent liabilities are also known as long-term liabilities. They are the business’s financial obligations listed on the balance sheet that are not due for more than a year. Unlike current liabilities that are due by the next year, noncurrent liabilities are not due until at least a year later. For the majority of small businesses, the only noncurrent liabilities will be loans from banks. This would include every loan owed varying from a three-year loan for a trailer to a 20-year loan for a building.

Nonetheless, deferred revenue, bonds payable, as well as loans and lease obligations, are typical examples of noncurrent liabilities. There are various ratios that implement noncurrent liabilities to assess a company’s leverage, such as debt-to-assets and debt-to-capital. Long-term investors use such ratios to gauge whether a company is using excessive leverage.

Noncurrent liabilities examples

- Bonds payable

- Long-term borrowing

- Capital leases

- Deferred revenues and taxes

- Mortgage debt

- Pension liabilities

- Notes payable

See also: Accumulated depreciation on the balance sheet

What are assets?

Assets are the resources with economic value owned by an individual, corporation, or country with the expectation that they will provide future economic benefit. These resources add value to a business as they are used to generate cash flow and reduce expenses. That is, assets help a business meet its commitments and increase its equity.

Personal assets are the assets owned by an individual, whereas business assets are those owned by a corporation or company. They contain economic value and can benefit a company’s operations, increase the value of a business, or raise an individual’s net worth. A high proportion of assets to liabilities is an indicator of a successful business because this indicates a higher degree of liquidity. Nevertheless, there is some overlap between liabilities and assets because businesses can use liabilities to purchase assets.

There are different types of assets based on physicality such as tangible and intangible assets. They can be currently available to sell or available for long-term sale, or used for the daily operation of a business. Assets can also be grouped into current and fixed assets based on liquidity. Moreso, they can be grouped into operating and non-operating assets based on operational activities. Furthermore, a company’s equity, solvency, or financial health can simply be calculated by subtracting its liabilities from the value of its total assets.

Types of assets

- Current assets

- Fixed assets

- Tangible assets

- Intangible assets

- Operating assets

- Non-operating assets

- Financial assets

The different types of assets listed above appear on a company’s balance sheet. They are created or bought to increase the value of a business or benefit the business’s operations.

Current assets

These are assets that are highly liquid because they can be sold and converted into cash easily. Financial assets such as cash, mutual funds, bonds, stocks, and other marketable securities are considered the most liquid current assets. This is because they can be sold easily and quickly without their price being affected. Current assets examples for businesses include cash, inventory, accounts receivable, and prepaid expenses.

Fixed assets

Fixed assets are also known as noncurrent assets, hard assets or long-term assets. These assets are generally considered to have low liquidity. This is because they may take a long period of time to earn cash value.

Fixed assets provide long-term, continual value to a business. However, they usually cannot be converted into cash within one year or be sold at their desired value quickly. Some fixed asset examples include buildings, land, furniture, or any other type of asset that is not intended for sale within the year. Apart from land, most long-term assets usually depreciate in value over time.

Tangible assets

Tangible assets are physical and real property such as real estate, inventory, cash, machinery, equipment, bonds, furniture, etc. They are physically tangible and are usually in the owner’s possession. The majority of tangible assets are considered current assets. This is because they are easily converted to cash.

Intangible assets

Intangible assets are items or goods that do not exist physically but exist theoretically. These assets have their value boosted through successful use and cannot easily convert to cash. Typical examples of intangible assets include logos, intellectual property, permits, business licenses, brand reputation, patents, and trademarks.

Operating assets

These are assets that generate revenue through day-to-day business operations. Operating assets help maintain workflow. Some examples of operating assets are licenses, copyrights, inventory, or machinery.

Non-operating assets

Non-operating assets are business-owned items that generate revenue though they are not necessarily needed for day-to-day business operations. A typical example of non-operating assets includes vacant land or short-term investments.

Financial assets

These are liquid assets that get their value from a contractual right or ownership claim. They represent investments in the assets and securities of other institutions. Financial assets include preferred equity, stocks, sovereign bonds, corporate bonds, mutual funds, and other hybrid securities. These assets are valued according to the underlying security market supply and demand.

Related: Return on assets formula and calculation

Liabilities vs assets examples

Let’s look at some real-life situations as an example to highlight liabilities vs assets comparison.

Getting supplies on credit

Assume Company A does well in their new location and lands a bunch of new clients. However, the company doesn’t have enough inventory to start a new project. So the company contacts their suppliers, and they agree to give the company supplies on credit, which must be paid back within two months.

Now, the inventory that the company receives is an asset that will help the company make money from the new projects whereas the amount that the company needs to pay back to the suppliers is a short-term liability.

Buying property

Let’s assume Mr. Peter owns a painting company, and for the past years, he has been operating out of his garage. Say, he wants to move into a proper office space and decides to take out a mortgage and buy a small office.

The office space acquired is an asset because he can now have a proper business address that may attract more customers. Also, if the need arises he can sell the office space. On the other hand, he has taken out a mortgage- that’s a non-current liability. So, he will need to make extra money to pay off this long-term debt.

Leasing or buying a vehicle

Assume you have a business that continues its smooth sailing, but you want to add a car to your pickup truck. You will either have to lease a car for a long period of time, take out a vehicle loan and buy a car, or buy a car in cash if your business can afford it.

Now, if you choose to buy the car with cash, the car will be an asset and you won’t owe anything to it. You can even choose to sell it if you need to make some money quickly. But say, you take out a vehicle loan or lease, that becomes a significant liability. The upside of taking the loan is that after you pay back the loan, the car becomes yours- an asset. However, if you lease, after a lease ends, you will turn the car in, thus, you won’t have an asset.

Whichever way, one will need to evaluate whether leasing or buying a car will put them in a better financial position.

Assets vs liabilities list

| Assets | Liabilities |

|---|---|

| Cash and cash equivalents (e.g checking accounts) Investments Inventory Office equipment Machinery Real estate Company-owned vehicles Accounts receivable (unpaid invoices from customers) Property (e.g buildings or cars) Patents or trademarks | Long term debt Notes and loans payable Accrued liabilities Income taxes payable Mortgage debt Accounts payable Wages owed Bonds payable Capital leases Deferred revenues and taxes Pension liabilities |

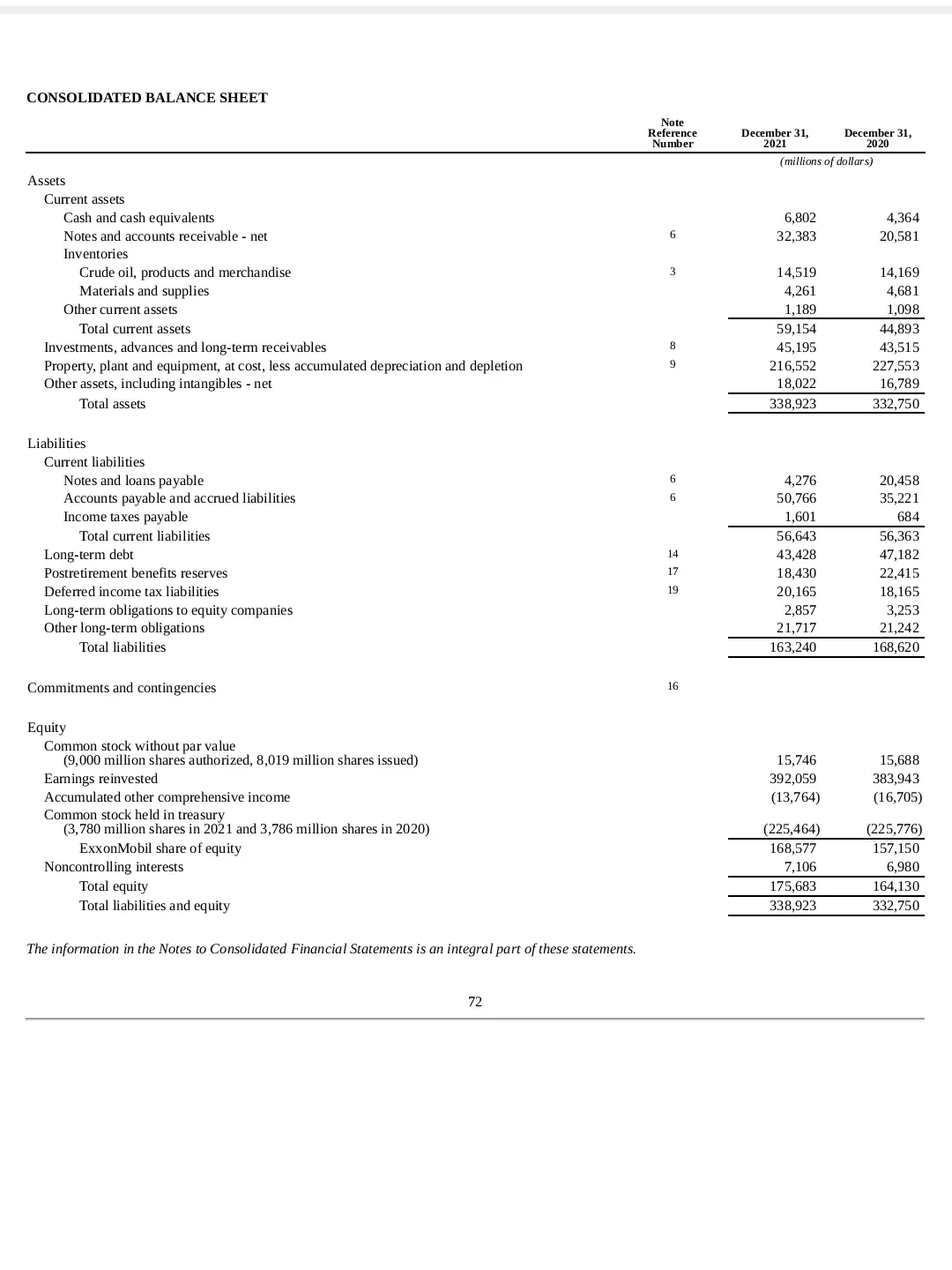

The image below is an excerpt of Exxon Mobil Corporation’s (XOM) balance sheet from its 10K statement (pages 72 & 74) for 2020 and 2021 to show an exemplary list of assets and liabilities in balance sheet:

From the image above we can see items such as cash and cash equivalents, notes and account receivable, inventories, investments, advances, long-term receivables, property, plant and equipment all listed as assets. Whereas, under the liabilities section we have listed items like long-term debt, notes and loans payable, accrued liabilities, income taxes payable, long-term debt, post-retirement benefit reserves, deferred income tax liabilities, and long-term obligations to equity companies.

See also: Debt financing examples and types

Debits and credits Journal Entry for Liabilities and Assets

Every financial transaction, according to the principle of double-entry, corresponds to both a debit and a credit. A debit would either increase an asset or decrease a liability. Conversely, credit either decreases an asset or increases a liability.

For instance, when cash is deposited in a bank, the bank is said to debit its cash account, on the asset side, and credit its deposits account, on the liabilities side. In this instance, the bank is debiting an asset and crediting a liability, meaning that both increase.

On the other hand, when cash is withdrawn from a bank, the bank credits its cash account and debits its deposit account. In this instance, the bank is crediting an asset and debiting a liability, meaning that both decrease.

Liabilities vs assets differences

- Liabilities are existing debts that a business owes to another business, employee, vendor, lender, organization, or government agency whereas assets are items or resources of value that the business owns.

- The main difference between liabilities vs assets is that liabilities present a future obligation while assets provide a future economic benefit.

- Liabilities (e.g loans) can help owners finance their companies creating a future obligation whereas assets (e.g property) can generate revenue and provide long-term benefits to the owner.

- In terms of value, liabilities represent a net loss whereas assets represent a net gain in value.

- Total assets are listed on the left side of a standard balance sheet, whereas the different types of liabilities are listed on the right side of the page.

- Liabilities make the business obligated for a short or long period of time whereas assets pay off the business for a short/long period of time.

- All fixed assets are depreciated except for land (non-current asset) that doesn’t depreciate; whereas liabilities can’t be depreciated, though they are paid off within a short/long period.

- Liabilities are credited when increased and debited when decreased whereas assets are credited when decreased and debited when increased.

- A company acquires assets with the intention of expanding the business whereas liabilities are taken to acquire more assets in order to make the business free of most liabilities in the future.

- Liabilities are one of the reasons for cash outflow because they must be paid off whereas assets help to generate cash flow for the business.

What is the difference between assets and liabilities?

The assets of a company are the items that are owned by the company which can provide future economic benefit. Liabilities, on the other hand, are what the company owes other parties. The table below summarizes the difference between liabilities vs assets:

| Criteria for comparison | Liabilities | Assets |

|---|---|---|

| Value/burden | These are debts that the business owes to another entity. They are an expense for the business. Nevertheless, they can be used to purchase assets | These are items of value owned by the business. They provide long-term benefits to the business |

| Placement in the balance sheet | Liabilities are placed on the balance sheet after total assets are computed | Assets are placed first on the balance sheet |

| Side of balance sheet | Total assets are listed on the left side of a standard balance sheet | Total liabilities are listed on the right side of a standard balance sheet |

| Increase in account | Liability would be credited if it is increased | An asset would be debited if it is increased |

| Decrease in account | If decreased, liability would be debited | If decreased, an asset would be credited |

| Uses | They may be used to finance business operations | It is used to generate revenue for the business |

| Depreciation | Liabilities are non-depreciable | Assets are depreciable |

| Value | They represent a net loss in value | They represent a net gain in value |

| Cash flow | Liabilities are one of the reasons for cash outflow in the business | Assets help to generate cash flow for the business |

| Types | Types of liabilities include current and non-current liabilities | Types of assets include current, fixed, tangible, intangible, operating, non-operating and financial assets |

| Equation | Liabilities= Assets – Shareholders equity | Assets= Liabilities + Shareholders’ equity |

| Examples | Bank overdrafts, sales taxes, accounts payable, payroll taxes, wages, income taxes, short term, loans, outstanding expenses | Cash, motor vehicles, buildings, machinery, equipment, and accounts receivable |

See also: Financial leverage ratios

Liabilities vs Assets Similarities

- Liabilities and assets are both reported on the balance sheet.

- They can both be debited.

- They can both be credited.

- Assets and liabilities are two essential parts of any business.

- Liabilities and assets both help in the growth of a business (businesses can’t operate and grow with no assets or zero liabilities).

Conclusion

Liabilities and assets are two essential parts of any business. Therefore, balancing your assets and liabilities is good for a healthy business. They both play a role in the growth of a business. Even though liabilities seem daunting, no business can operate and grow with zero liabilities. They may need to take a loan to get inventory on credit or buy necessary equipment.

Assets contribute to the smooth running of a business even when the earnings aren’t as high as expected. The main difference between liabilities vs assets is that liabilities present a future obligation while assets provide a future economic benefit. That is why a standard accounting equation compares a company’s total assets against its total liabilities, and investors use the comparison factor of liabilities vs assets to place a valuation on the company.

The more a business’ assets outweigh its liabilities, the stronger the financial health of the business. But when a business finds itself with more liabilities than assets, it may be on the cusp of going out of business.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.