Merchandise inventory is what type of account? Merchandise inventory on the balance sheet includes all goods in stock (finished goods or raw materials) that have been purchased but are yet to be sold. It is named so because wholesalers, retailers, and distributors make money by purchasing goods from suppliers or manufacturers and then merchandising (marketing and selling products) the goods for customers. Hence, merchandise inventory includes goods that are ready to be sold and are intended to be resold to customers.

In this article, we will discuss what type of account merchandise inventory is and how it is recorded. First, let’s have an understanding of the merchandise inventory account.

Related: What type of account is retained earnings?

What is merchandise inventory?

Merchandise inventory includes the range of costs that wholesalers, retailers, or distributors incur in the course of buying products that they intend to sell to customers. That is, the merchandise inventory includes the cost of all goods that have been purchased, from items in warehouses and retail stores to goods that are still in transit from the suppliers. Hence, the merchandise inventory account would include the price paid for the goods, shipping costs paid by the resellers, and any other related expenses, such as packaging and transit insurance.

Therefore, the merchandise inventory refers to any goods that are meant for resale, whether they are in transit from the supplier, in the retailer’s hands, or stored in a warehouse or distribution center ready to be sold. Hence, the merchandise inventory account in accounting is seen as a holding account for inventory that is expected to be sold soon.

The company’s beginning merchandise inventory value, the total amount spent on additional merchandise inventory, and the cost of goods sold COGS (also referred to as the cost of sales) are used to calculate the ending merchandise inventory at the close of an accounting period. The value of inventory at the beginning of the accounting period before any more inventory items are acquired or sold is known as the beginning merchandise inventory. Hence, the beginning inventory for a current period is calculated as the ending merchandise inventory value from the previous accounting period.

Calculating and tracking merchandise inventory

When calculating merchandise inventory, the amount spent on additional inventory during the period is added to the beginning inventory and then the cost of goods sold (COGS) is subtracted. Hence, the formula is expressed as:

Ending merchandise inventory = Beginning inventory + New inventory costs – COGS

In order to explain the calculation of merchandise inventory value and COGS, let us look at an example of a footwear merchandiser who had 10 units of beginning inventory that is worth $1000. He then bought 50 units of shoes from a supplier at $100 a pair and sells 40 pairs at $200 per pair at the end of the accounting cycle. If 20 pairs of footwear out of these are left, in order to calculate the value of merchandise inventory, he will multiply the amount of unsold inventory by the cost of each unit. That is:

Value of merchandise inventory = Amount of unsold inventory x Inventory cost of each unit

= 20 x $100 = $2000

Hence, $2000 is the merchandise inventory value which is considered the same as the ending inventory. This is then entered into the balance sheet in the merchandise inventory account. The next thing would be to calculate the COGS. The cost of goods sold is the direct cost of producing merchandise inventory for sale. The formula for calculating this is:

COGS = (Beginning inventory + Purchased inventory value) – Merchandise inventory value

In the case of the shoe retailer, the COGS would be:

= ($1000 + (50 x $100)) – $2000

= $4000

This means that $4000 is the COGS which can be used to calculate profits:

Profit = Total sales – COGS

= (40 x $200) – $4000

= $4000

This means that $4000 is the profit that the shoe retailer made

See also: Notes payable is what type of account?

Merchandise inventory is what type of account?

Merchandise inventory is a current asset account. A current asset is an asset that the company expects to sell or consume within a year. Current assets are assets that provide economic benefit during a given accounting period, typically a year. Hence, merchandise inventory is reported as a current asset on the company’s balance sheet because it is the unsold goods that are expected to be sold during a fiscal or calendar year.

Merchandise inventory is therefore a current asset because it is the unsold inventory that a company generally expects to sell within a year through normal business operations. As merchandise inventory is represented as an asset on a company’s balance sheet, it indirectly appears on the company’s income statement (that reports expenses, revenue, and profit or loss) during a specific accounting period. That is, during each accounting period, the changes in merchandise inventory are reflected as expenses on the income statement. This is because when merchandise inventory is sold, its cost is reported in the COGS expenses on the income statement for that period.

For instance, a retail store that purchases additional volumes of a product will have to record the cost of the shipment in the merchandise inventory account, as an asset. Until the retailer sells the goods, this cost of shipment is not treated as an expense. Therefore, when the goods are eventually sold, their cost is removed from the merchandise inventory account and then added to the cost of goods sold (COGS) account (which is an expense account) for that accounting period. This will therefore directly affect the gross profit of the company for that period because a company’s gross profit is calculated by subtracting COGS from net sales.

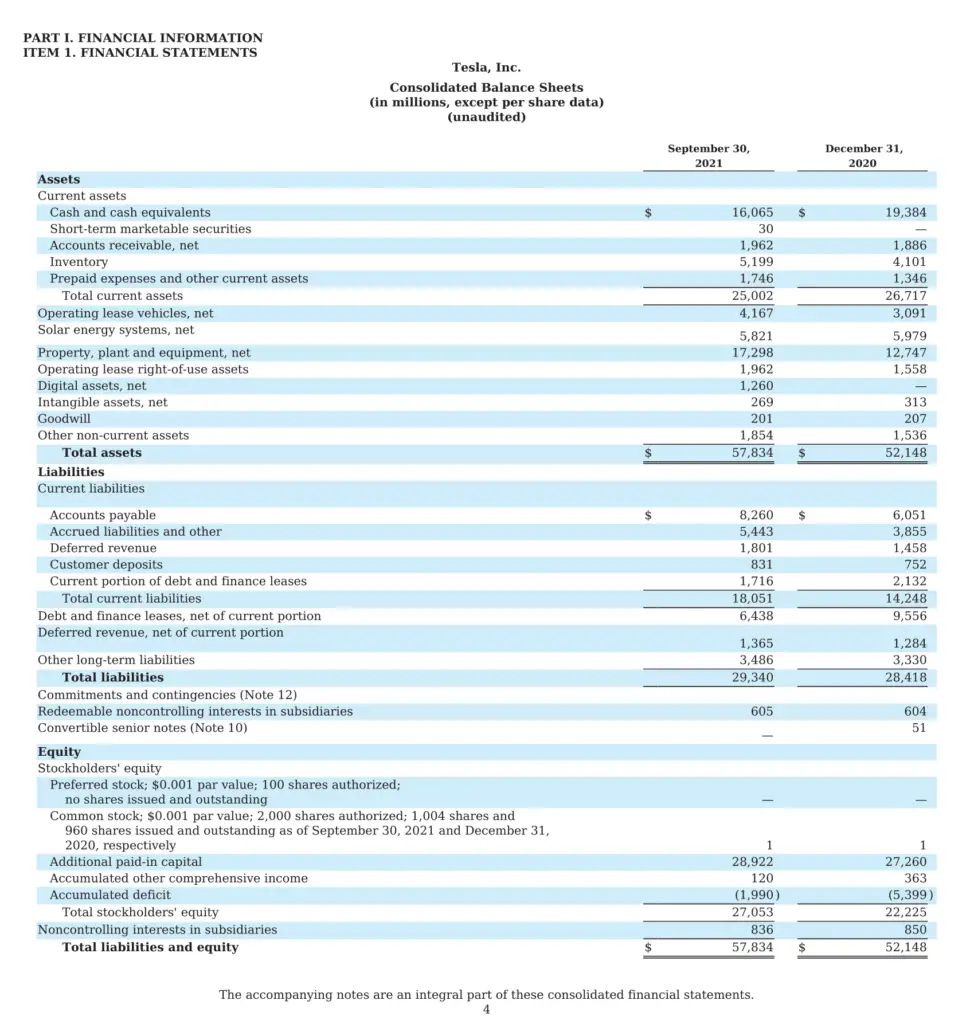

Below is an example of inventory listed as the 4th line item under current assets on the balance sheet:

Source: Tesla

Related: Supplies expense is what type of account?

Recording merchandise inventory as a current asset

So, merchandise inventory is what type of account? Merchandise inventory includes the goods that have been purchased but are yet to be sold and as such is categorized as a current asset on a company’s balance sheet. Hence, merchandise inventory has an impact on a company’s current assets, accounts payable, expenses, and profit, which are all crucial measures of the financial health of a business. Therefore, accurately accounting for merchandise inventory is important.

How is merchandise inventory recorded? Merchandise inventory as an asset will have a normal debit balance, which means that it increases with a debit entry and decreases with a credit entry. This is because according to the debit and credit rules, asset and expense accounts would increase with a debit entry and decrease with a credit entry. When a company purchases goods that it intends to sell to customers, it records the transaction in the Merchandise Inventory account, as a current asset. Recording merchandise inventory can be done using the perpetual inventory procedure or periodic inventory procedures.

A company using the perpetual inventory procedure, will debit the Merchandise Inventory account for each purchase and then credits the Merchandise Inventory account for each sale in order to show the current balance in the account at all times. Whereas, under periodic inventory procedures, the company would not use the Merchandise Inventory account to record each purchase and sale of merchandise. Rather, the company will correct the balance in the Merchandise Inventory account at the end of the accounting period as a result of a physical inventory count carried out.

Conclusively when recording purchases, the cost will be entered as a debit to the merchandise inventory account and as a credit to the Cash or accounts payable account. Then, when these goods are eventually sold, their cost is deducted from the merchandise inventory account and then added to the cost of goods sold (COGS) account for the accounting period.

Example

Assuming, you purchased 10 electronic hardware packages at a cost of $620 each. Say, you had enough cash on hand and therefore paid immediately with cash. This is how you will record this purchase of inventory:

| Account | Debit | Credit |

|---|---|---|

| Merchandise Inventory: Packages | $6,200 | |

| Cash | $6,200 |

As shown in the journal entry above, a debit is made to the Merchandise Inventory account to increase it by $6,200, while a credit entry is made to the Cash account to decrease it by $6,200 because you paid with cash.

Now, let’s assume you didn’t pay cash and purchased the 10 electronic hardware packages on credit. This is how you would record the transaction:

| Account | Debit | Credit |

|---|---|---|

| Merchandise Inventory: Packages | $6,200 | |

| Accounts Payable | $6,200 |

As shown in the journal entry above, a debit is made to the Merchandise Inventory account to increase it by $6,200, while a credit entry is made to increase the Accounts payable account by $6,200 because you made the purchase on credit, hence increasing your liabilities.

Read also: Service revenue is what type of account?

Conclusion

Merchandise inventory is what type of account? Merchandise inventory is goods that have been bought by a wholesaler, retailer, or distributor from suppliers, with the intention of selling the goods to customers. Merchandise inventory is therefore treated as a current asset on the balance sheet of the wholesaler, retailer, or distributor. When these unsold inventories are sold during an accounting period, their cost is charged to the cost of goods sold, and would appear as an expense in the income statement. However, if the inventories are not sold during an accounting period, then their cost is recorded as a current asset in the company’s balance sheet until the time that they are sold.

Related: What type of Account is Sales Returns and Allowances?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.