Is notes payable asset or liability? In business, a party may purchase a piece of equipment on credit or borrow money from another party and make a formal promise to pay it back on a predetermined date. This formal promise is made in form of a promissory note which is issued to the lender, by the borrower, assuring him or her of payment on a specific date.

The borrower that issues a promissory note has to record the amount of money received or owed in his accounting books as notes payable. The notes payable account is, therefore, an account on the borrower’s balance sheet that reflects the money owed from an issued promissory note. The lender, on the other hand, that receives the promissory note would record the amount as notes receivable in his accounting book, which is an asset to the lender.

When it comes to notes payable, the borrower borrows from another party, promising to repay with interest, and as such incurs a debt. Hence, notes payable is not an asset but a liability because debt is incurred when a promissory note is issued. This article aims to answer the question ‘is notes payable asset or liability?’ with explanations and examples. We will be discussing notes payable, asset, and liability accounts to understand their features in accounting in order to ascertain why notes payable is not an asset but a liability.

Read also: Is accounts payable a permanent account?

What is notes payable?

Notes payable is an account on the balance sheet that reflects the money that is owed by a note maker under the terms of an issued promissory note. The note maker is the party that issues the promissory note and as such is obligated to pay the amount recorded in the notes payable account to another party. The party, on the other hand, that receives the promissory note is the payee and as such receives payment from the maker under the terms of the promissory note.

The maker or borrower under the agreement of a promissory note receives a specific amount of money from the lender or payee and promises to pay it back with interest. Any promissory note associated with notes payable would therefore have the following:

- Principal amount

- Interest owed

- Maturity date

- Collateral pledged

- Creditor limitations

Now, that we have an understanding of notes payable, is it an asset or liability? Let’s discuss what an asset is.

Related: Is accounts receivable an asset or revenue?

What are Assets?

An asset is anything of economic value that a business owns. Assets are resources that a company owns with the expectation that they will provide an economic benefit in the future. That is, anything that adds value to the company’s business and is used to generate cash flow and reduce expenses is considered an asset. In as much as notes payable are incurred from the purchase of assets or borrowed funds, in order to add value to the company’s business, they are not considered assets.

Typical examples of assets in business would include cash and cash equivalents, accounts receivable, and prepaid expenses such as prepaid rent. They also include merchandise inventory, marketable securities, PPE (Property, Plant, and Equipment), equipment, vehicles, furniture, patents, etc. These assets can be grouped based on liquidity, physicality, and operational activities.

Even though notes payable are incurred in order to add value to the company’s business, they cannot be considered an asset because they are debts that the company will still have to pay for in the future. As you can see, the notes payable account cannot be recognized as an asset account. This is because this account reflects the money that is owed by a note maker under the terms of an issued promissory note.

Since it is evident that notes payable is not an asset, is it a liability? Let’s discuss liability to answer this.

See also: Service Revenue Asset or Liability?

Liability explained

A liability is a debt or financial obligation that a company has to service to another party. Liabilities are the obligations that the company has to pay off either in the near future or in the further future. These liabilities are settled over time through the transfer of economic benefits such as money, goods, or services. A liability can easily be contrasted with an asset; a liability is something that the company owes or has borrowed whereas an asset is something that the company owns or is owed. A liability is characterized by the following:

- Any type of borrowing from individuals or banks for improving a business or personal income that is payable over a short or long time

- A duty or obligation to others that involves settlement by future transfer or use of assets, or provision of goods or services, at a specified date, on the occurrence of a specified event, or on demand

- A duty or obligation that obligates an entity or party to another, leaving it with little or no discretion to avoid settlement

- A transaction or event that obligates an entity that has already occurred

From the characteristics listed above, notes payable fit into the first and second characteristics of liabilities. Hence it is a typical example of a liability. Other examples of liabilities accounts include accounts payable, accrued expenses, loans, mortgages, interest payable, deferred revenues, bonds, wages payable, unearned revenue, and warranties.

Accounts payable, notes payable and loans payable are the most common type of liabilities.

An example on notes payable as a liability and not an asset

An example is a case whereby a wine supplier sells a case of wine to a bar and does not demand payment on delivery. The wine supplier, rather, invoices the bar for the purchase to streamline the drop-off and make paying easier for the bar. Hence, making the transactions between the two businesses more efficient.

The outstanding money that the bar now owes the wine supplier is considered a liability (recorded as accounts payable). Furthermore, in the case whereby the bar is short of cash and decides to issue a note to the wine supplier promising to pay the owed amount with interest on a specific date, the owed amount is also considered a liability (recorded as notes payable). Therefore, it is evident that notes payable is not an asset, but a liability. Let’s discuss this further.

Related: Is accounts receivable a current asset?

Is notes payable asset or liability?

Notes payable is not an asset but a liability. It is a liability account on the maker’s balance sheet that reflects the amount owed under the terms of the promissory note that was issued. Hence, notes payable is an account reported under the liabilities section of the balance sheet. It cannot be considered an asset because it is the money owed for purchase or borrowed funds received under the terms of a promissory note. Hence, notes payable is a liability account on the maker’s balance sheet.

Notes payable is not an asset account but a liability account and as a liability, it can be classified either as a current or long-term liability depending on the maturity date of the note. Most times, notes payable are usually made payable within 12 months. The notes payable that are due within the next 12 months are classified on the balance sheet as current or short-term liabilities. Typical examples of when notes payable are short-term include bulk purchasing of materials from suppliers and manufacturers or bulk licensing of software to cover a company’s large user base.

The notes payable, on the other hand, that are due after one year are classified on the balance sheet as non-current (long-term) liabilities. There are instances whereby companies issue longer-term promissory notes. Typical examples of when notes payable are long-term would be receiving a significant loan from a bank or financial institution or collecting money to build expensive infrastructure, like a manufacturing plant.

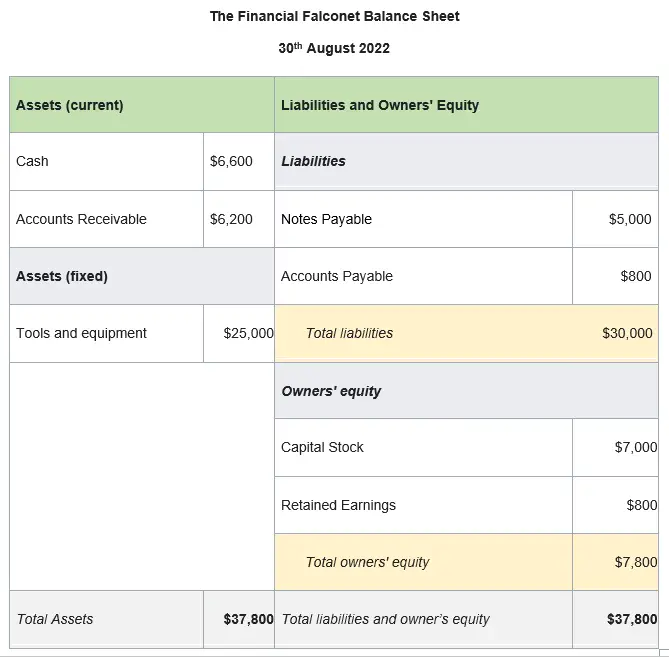

Below is an example of a small business balance sheet, showing notes payable not as an asset account but as a liability account:

In the balance sheet above we can see that notes payable is not listed under the asset section but under the liabilities section. This is an example to show that notes payable is considered a liability account and not an asset account. Furthermore, it is important to note that notes payable and accounts payable are not the same. As shown in the balance sheet above, they are both two different liability accounts. Unlike notes payable, accounts payable (A/P), are not associated with a promissory note and most importantly, don’t require payment of any interest.

See also: Is Dividends an Asset?

Why notes payable is not an asset but a liability

Let’s discuss reasons why notes payable is not an asset but a liability. In financial accounting, a liability is characterized as the future sacrifices of economic benefits that a party is obliged to make to other parties as a result of past transactions or other past events. This is applicable to notes payable which is recorded as the amount a party reports when a purchase is made on credit or money is borrowed from another party from issuing a promissory note, to pay back the stated amount on a specific date.

Also, the settlement of liabilities may result in the transfer or use of assets, or the provision of services or goods (as in the case of unearned revenue). In the case of notes payable, the settlement is usually done with cash (which is an asset). Hence, notes payable is a liability and not an asset.

Notes payable is not an asset because it is not a resource of economic value that the business owns. Assets are resources that a company owns with the expectation that they will provide an economic benefit in the future. Even though notes payable are incurred in order to add value to the company’s business, they cannot be considered an asset because they are debts that the company will still have to pay for in the future.

Hence, a notes payable account is not recognized as an asset but as a liability. This is because this account reflects the money that is owed by a note maker under the terms of an issued promissory note.

Related: Is accumulated depreciation an asset?

Notes Payable Transaction Example

Let’s look at an example to show how notes payable is treated not as an asset but as a liability account:

Cindy’s Apparel sells some items of clothing worth $15,000 to Anne’s Online Store, with payment due in 30 days. After 60 days of nonpayment, the two parties agree that Anne will issue a promissory note to Cindy for $15,000, at an interest rate of 10%, which will be due in the next three months. Hence, Anne issues a promissory note with the following terms:

- Payee: Cindy’s Apparel

- Maker: Anne’s Online Store

- Principal amount: $15,000

- Maturity date: 3 months due at maturity

- Interest rate: 10% per year

Initially, Anne’s Online Store recorded the transaction as accounts payable. So after the agreement, she makes an entry to convert the account payable to a note payable. After Anne’s Online Store has issued the promissory note to Cindy’s Apparel, she will now record the $15,000 owed, to her notes payable account as a current liability. This transaction is treated as a current liability because the due date is in 3 months which is less than a year (12 months).

Hence, the journal entry for this transaction would be entering $15,000 as a debit to the Cash account and as a credit to the Notes payable account. That is:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash A/c | $15,000 | |

| Notes payable A/c | $15,000 |

In double-entry bookkeeping, a debit entry either increases an asset or decreases a liability while a credit entry either decreases an asset or increases a liability. Hence, in accordance with this debit and credit rule, notes payable is recorded as a credit as seen in the journal entry above. This means that, as a liability, notes payable would increase with a credit entry and decrease with a debit entry. Therefore, as Anne issued a note to Cindy, the Notes Payable account had to be credited to increase the account by $15,000, and a debit entry of $15,000 had to be made to the Cash account to increase the account.

Also, recall that with notes payable, interest is accrued. Hence, Anne will record the accrued interest as:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Interest Expense A/c | $375 | |

| Interest Payable A/c | $375 |

Interest = Principal x Interest rate x Time period

= $15,000 x 10% x (3 months/12 months)

= $375

As Anne pays the accrued interest, the journal entry will be as follows:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Interest Payable A/c | $375 | |

| Cash A/c | $375 |

Then, when Anne has made payment of the note, the Notes Payable account is debited by $15,000 to reduce the account, and the Cash account is credited by the $15,000 paid to Cindy to reduce the Cash account:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Notes payable A/c | $15,000 | |

| Cash A/c | $15,000 |

In conclusion, is notes payable asset or liability? Notes payable is not an asset but a liability account on the balance sheet that reflects an amount that is owed under the terms of an issued promissory note. The notes payable that are due within the next 12 months are current (short-term) liabilities while the notes payable that are due after one year are non-current (long-term) liabilities.

See also: Are expenses assets, liabilities, or equity?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.