Notes payable is what type of account? A business owner may purchase a piece of equipment on credit or borrow money from another party and then issue a promissory note to the lender to assure him or her of payment on a predetermined date. When this business owner issues this promissory note, he records the amount of money received or owed on his accounting books as notes payable. This is an account on his balance sheet that reflects the money owed from issued notes. The lender, on the other hand, that receives the promissory note records the amount in his accounting book as notes receivable, which is an asset account on the lender’s balance sheet.

When accounting for notes payable, the party that issues the note incurs debt by borrowing from the other party, promising to repay with interest. Since debt is incurred, notes payable is a liability and as such, it is an account reported under the liabilities section of the balance sheet. This article aims to answer the question ‘notes payable is what type of account?’ with explanations and examples.

Related: What type of account is retained earnings?

What is notes payable?

A note payable is recorded in an accounting book to reflect the money that is owed under the terms of an issued promissory note. The party that issues the promissory note is the maker which is obligated to pay money to another party while the party or lender that receives payment from the maker under the terms of the promissory note is referred to as the payee.

Under the agreement of a promissory note, the maker receives a specific amount of money from the payee and promises to pay it back with interest over a predetermined period of time. The specific amount of money that is received is known as the principal amount while the predetermined time period is the maturity date of the note on which the principal amount has to be paid. Notes payable incur an interest rate that has to be paid. This interest rate may be fixed over the life of the note or vary in accordance with the interest rate charged by the lender such as a prime rate.

The formula used to calculate the interest rate on notes payable is expressed as:

Interest = Principal x Interest rate x Time period

Any promissory note associated with the notes payable account would therefore have the following:

- Principal amount

- Maturity date

- Interest owed

- Collateral pledged

- Creditor limitations

Hence, at the maturity date of the note, the borrower is expected to pay the principal amount plus the interest. The borrower may use the accrual method of accounting to record notes payable, where the notes payable account will be supplemented with an interest payable account. This is done because the promissory note requires the borrower to pay interest, thus, creating an additional interest expense. In the interest payable account, the borrower will then record any interest incurred during the accounting period that has not yet been paid.

Terms and conditions for notes payable

Most times, promissory notes are usually made payable within 12 months. However, the issuer of the note (borrower) and the note holder (lender) are free to agree to a longer maturity period. As a promissory note usually carry a given interest rate, maturity date, etc, it can also have limitations or conditions that are set by the lender.

The note payable agreement may require collateral from the issuer of the note, such as a company-owned building, or a guarantee by an individual or another entity. This is why many notes payable agreements require formal approval by a firm’s board of directors before a lender can issue funds to the issuer of the note.

Also, in several cases, the issuer of the note may be restricted from carrying out stock buybacks or paying dividends until the promissory note has been repaid. Hence, the issuer of the note must have paid back the initial principal amount plus the specified interest rate by the maturity date on the note before being allowed to repurchase shares or pay dividends to their shareholders.

This means that, in some cases, the lender may require restrictive covenants as part of the note payable agreement, which requires the issuer of the note to not pay dividends to investors while still owing any part of the loan. The lender has the right to call the loan should this covenant be breached. However, in most cases, the lender may waive the breach and continue to accept periodic debt payments from the issuer of the note.

Furthermore, according to the terms of the notes payable agreement, the accrued interest on the notes may be paid as a single payment that is made at a particular time when the full amount is due or as regular payments which are done on a monthly or quarterly period. This would depend on the settled terms of the agreement.

See also: Supplies expense is what type of account?

Notes payable is what type of account?

Notes payable is a liability account on the maker’s balance sheet which reflects the amount owed under the terms of the promissory note that was issued. A firm may be short on cash and issue a promissory note to a vendor, bank, or other financial institution to acquire assets or borrow funds. For example, a firm might issue notes to purchase an expensive piece of equipment or a new property. The money owed for purchase or the borrowed funds received under the terms of a promissory note is therefore accounted for in the notes payable account, which is a liability account on the maker’s balance sheet.

Therefore, what type of account is notes payable? Notes payable is a liability account because it is a debt that is owed under the terms of a promissory note. It can be classified as a current or long-term liability depending on the maturity date of the note. The notes payable that are due within the next 12 months are classified under current or short-term liabilities on the balance sheet. Bulk purchasing of materials from suppliers and manufacturers or bulk licensing of software to cover a firm’s large user base are typical examples of when shorter-term promissory notes may be issued.

On the other hand, the notes payable that are due after one year are classified under long-term or non-current liabilities. Companies may issue longer-term promissory notes whereby the maturity date is usually longer than one year. Typical examples would be receiving a significant loan from a bank or financial institution or collecting money to build expensive infrastructure, such as a manufacturing plant.

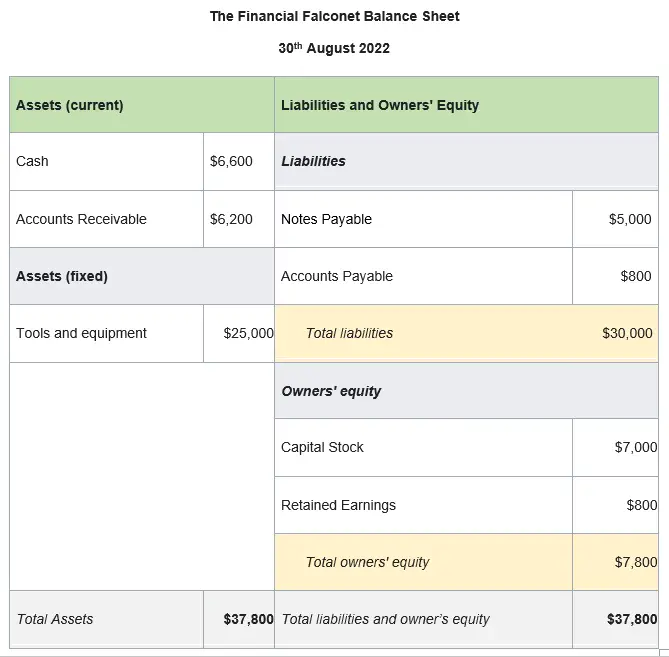

Below is an example of a small business balance sheet. In the balance sheet below we can see that notes payable are not listed under the assets nor the equity section but under liabilities. Hence, notes payable is a liability account and not an asset or equity account.

Furthermore, it is important to note that notes payable are not accounts payable. These two liabilities are different. As shown in the balance sheet above, they are both different accounts in the liability sections. A lot of people mistake the two for each other, which is wrong.

Accounts payable (A/P), are not associated with a promissory note and most importantly, there is no interest rate to be paid; although a penalty may be incurred if payment is made after a designated due date. A/P is a liability account in the business’s book that reflects the amount of money owed to its creditors or suppliers, that has not yet been paid. Notes payable, on the other hand, is a liability account in a company’s books that reflects the business’s promises to pay specific amounts of money within a predetermined period.

Related: Service revenue is what type of account?

Example of notes payable as a liability account

In order to understand notes payable as a liability account, let’s look at an example:

ABC Construction Company purchases a truck worth $100,000 on credit from the manufacturer- XYZ Motors. ABC receives an invoice from XYZ Motors that is due in 30 days, but unfortunately, ABC is unable to make prompt payment. Hence, ABC negotiates and issues a promissory note with the following terms:

- Payee: XYZ Motors

- Maker: ABC Construction Company

- Principal: $100,000

- Maturity date: 6 months due at maturity

- Interest rate: 6% per year

After ABC Company has issued the promissory note to XYZ Motors, it will now record the $100,000 owed to its notes payable account as a current liability. It is a current liability because the due date is within the next 12 months.

Let’s look at the journal entry for this transaction. ABC will enter the $100,000 as a debit to the cash account and as a credit to the notes payable account:

| Account | Debit | Credit |

|---|---|---|

| Cash A/c | $100,000 | |

| Notes payable A/c | $100,000 |

As seen in the journal entry shown, notes payable is recorded as a credit. This is because it is a liability and as such would increase with a credit entry and decrease with a debit entry. As ABC issued a note to XYZ Motors, the Notes Payable account has to be credited to increase the account by $100,000, and the debit entry of $100,000 is made to the Cash account to increase the account.

Also, recall that interest is accrued with notes payable. Hence, this is how ABC will record this:

| Account | Debit | Credit |

|---|---|---|

| Interest Expense A/c | $3000 | |

| Interest Payable A/c | $3000 |

Interest = Principal x Interest rate x Time period

= $100,000 x 6% x (6 months/12 months)

= $3000

As ABC pays the accrued interest, the journal entry will be as follows:

| Account | Debit | Credit |

|---|---|---|

| Interest Payable A/c | $3000 | |

| Cash A/c | $3000 |

Then, when ABC Company has made payment of the note, the Notes Payable account is debited to reduce the account and the Cash account is credited to reduce the account by the $100,000 paid to XYZ Motors:

| Account | Debit | Credit |

|---|---|---|

| Notes payable A/c | $100,000 | |

| Cash A/c | $100,000 |

What type of account is notes payable? In conclusion, notes payable is a type of liability account that reflects a debt that is owed under the terms of an issued promissory note.

Related: What type of Account is Sales Returns and Allowances?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.