The quick ratio formula is among the most aggressive liquidity ratios in determining the short-term liquidity capabilities of companies. This quick ratio calculation is a more conservative assessment of the liquidity status of firms, though it is similar to the current ratio. But unlike the current ratio, the quick ratio excludes inventory as it doesn’t consider it sufficiently liquid.

Companies can’t survive without cash flow and being able to take care of their bills when due. Hence, calculating the quick ratio of a company helps to tell what resources the company have in the very short term should in case there will be a need to liquidate current assets.

Even though there are other liquidity ratios for the measurement of the company’s ability to be solvent in the short term, the quick ratio happens to be among the most aggressive ratio used in determining short-term liquidity capabilities.

What is the quick ratio?

The quick ratio is a type of liquidity ratio that measures the ability of a company to meet its short-term liabilities with its near cash or most liquid assets. This ratio is also known as the acid-test ratio because it indicates the ability of the company to quickly use its near-cash assets (assets that can be converted quickly to cash) to settle its current liabilities. The slang ‘acid test’ is a term for a quick test created to produce instant results.

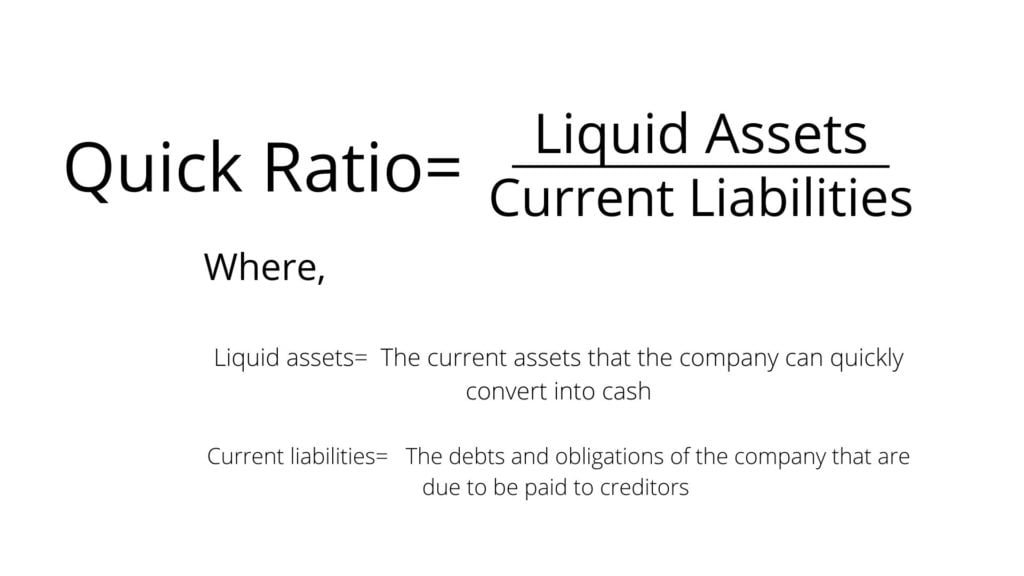

The quick ratio is the ratio between liquid assets or quickly available assets and current liabilities. This ratio is called a quick ratio because it only looks at the most liquid assets that are available in a company to service short-term debts and obligations.

These liquid/quick assets are the current assets of the company that can apparently be quickly converted to cash at close to the book value of the company.

In simple terms, quick ratios evaluate whether a company has enough liquid assets that can be converted into cash to pay its bills. The key component of liquid assets that are included in the quick ratio are cash, cash equivalent, marketable securities, and accounts receivable.

The quick ratio is similar to the current ratio but only considers assets that can be converted to cash in a short period of time. Hence, it excludes inventory and prepaid expense assets. Even though prepaid expenses are an asset they cannot be used to retire current liabilities and that is why it is omitted from the quick ratio formula. More so, inventory is omitted too because in most companies it takes time to liquidate. Selling off inventory in the short term is quite difficult and possibly at a loss. However, very few rare companies can turn their inventory quickly to consider it a quick asset.

The current ratio, on the other hand, considers prepaid expense assets and inventory. Compared to this ratio, the quick ratio is a better indicator of the company’s ability to meet its immediate obligations. This ratio comes in very handy when a company is facing a financial crisis and needs to pay off a substantial amount of liabilities in the near term.

A ratio of 1:1 is said to be a normal liquid ratio. Therefore, a company that has a quick ratio less than 1 can’t fully settle its current liabilities. In quarterly financial reports, publicly traded companies usually report the quick ratio figure of the company under the heading- Liquidity/Financial Health, in the Key Ratios section.

Interpretation

A quick ratio analysis interpretation tells us whether a company has enough liquid assets that can be converted into cash to settle its current liabilities. The ratio would measure the dollar amount of available liquid assets of the company against the dollar amount of the company’s current liabilities.

The current assets that the company can quickly convert into cash with minimal impact on the price received in the open market are what amounts to the dollar amount of available liquid assets. While the debts and obligations of the company that are due to be paid to creditors within one year are the current liabilities.

Hence, the quick ratio interpretation would ascertain the short-term liquidity capabilities of companies. Calculating the quick ratio is a more conservative assessment of the liquidity status of companies. For example, a quick ratio of 1.8 can be interpreted as a business having $1.8 of liquid assets that are available to pay off each $1 of its current liabilities.

However, in as much as this ratio is a good test for the viability of business entities, it may not give a complete insight into the overall health of the business. For instance, a company may have essential business expenses and accounts payable due for immediate payment and have large amounts in accounts receivable that are due for payment after a long period. Now, in such a scenario, the quick ratio may look healthy when the company is actually about to run out of cash.

Conversely, if the company has negotiated fast payment or cash from customers as well as long terms from suppliers, the company may have a very low quick ratio but still, be very healthy. Therefore, adjusting input data accordingly and a more detailed analysis of all major payables and receivables in relation to market sentiments tend to give a more sensible result for actionable insights. In essence, it is crucial to look at other associated measures to assess the actual picture of a company’s financial health.

What is a good quick ratio?

Whether a company has a good quick ratio or not may depend on several factors such as industry, growth, risk, economic conditions, accounts receivable, and inventories (the company might have a type of inventory that was easy to quickly liquidate). Notwithstanding, an ideal quick ratio is considered to be 1, which indicates that the company is fully equipped with the needed liquid assets to settle current liabilities.

A quick ratio less than 1 can indicate that the business may not be capable of fully paying off its current liabilities in the short term. Whereas, a business with a quick ratio higher than 1 can immediately get rid of its current liabilities.

Generally, an ideal quick ratio should be 1:1 or higher. However, this varies widely by industry and the rule of thumb is that the higher the ratio, the greater the company’s liquidity (i.e the ability to settle current liabilities with liquid assets). A higher quick ratio tends to be better because the numerator (liquid asset) of the quick ratio formula will be higher than the denominator which is the current liabilities of the company.

A higher quick ratio tells us that a business can be more liquid and can generate cash quickly in cases of emergency. Nevertheless, it is important to note that a very high quick ratio may not be better. For instance, a business may be sitting on a very large cash balance. The business can use this capital to invest in new markets or to generate company growth. Hence, there is usually a fine line between balancing short-term cash needs and spending capital for long-term potential.

Quick ratio formula

The formula for quick ratio can be expressed as:

Quick ratio (Acid-test ratio)= Liquid assets / Current liabilities

However, there are variants of the quick ratio formula in accounting depending on how the numerator (liquid assets) is calculated. Hence, the quick ratio equation can also be expressed as:

Quick ratio= (Cash and cash equivalent + Marketable securities + Accounts receivable) / Current liabilities

or

Quick ratio= (Current assets – Inventory – Prepaid expenses) / Current liabilities

Components of the quick ratio formula

- Quick assets

- Cash

- Cash equivalents

- Marketable securities

- Net accounts receivable

- Current liabilities

Listed above are the components of the quick ratio calculation formula. The figure of these elements is used when calculating the quick ratio:

Quick assets

Quick assets are the assets that the company can quickly convert into cash with minimal impact on the price received in the open market. For an item to be called a quick asset, it should be quickly converted to cash without significant value loss. Hence, the companies shouldn’t incur a lot of time and cost to liquidate the asset. Inventory, for example, is excluded from quick assets because it incurs lots of time to be converted into cash.

Therefore, the most liquid items in a company include cash, cash equivalents, marketable securities and accounts receivable. The majority of the quick assets of companies are mostly kept in form of cash and short-term investments (marketable securities) to pay off their immediate financial obligations that are due in one year.

Cash

Among the more straightforward component of the quick ratio is cash. This cash component may include cash from foreign countries that has been translated to a single denomination.

Cash equivalents

Cash equivalents are usually an extension of cash. This usually accounts for house investments with very low risk and high liquidity. Cash equivalents as a component of quick ratio usually include certificates of deposits, treasury bills, bankers’ acceptances, corporate commercial paper, or other money market instruments.

However, cash equivalents may not necessarily be limited to the equivalents listed. Moreso, according to a publication by the American Institute of Certified Public Accountants (AICPA), digital assets e.g digital tokens or cryptocurrency, may not be reported as cash or cash equivalent.

Marketable securities

Marketable securities are usually free from time-bound dependencies. Nevertheless, in order to maintain precision in the calculation, only the amount to be actually received in 90 days or less under normal terms should be considered. Therefore, early liquidation or premature withdrawal of assets such as interest-bearing securities may result in discounted book value or penalties.

Net accounts receivable

It’s still debatable whether accounts receivable is a quick asset. This is because this component depends on the credit terms that the company extends to its customers. For instance, a business that needs advance payments or only gives 30 days to the customers for payment will be in a better liquidity position compared to a business that allows 90 days.

Companies could negotiate rapid receipt of payments from their customers and secure longer terms of payment from their suppliers, which would keep liabilities on the books longer. These companies may have a healthier quick ratio and be fully equipped to pay off their current liabilities by converting accounts receivable to cash faster.

Furthermore, the estimated amount of uncollectible receivables should be deducted from the total accounts receivable balance. Most importantly, the quick ratio formula should not include any receivables a company does not expect to receive since the ratio only wants to reflect the cash that could be on hand.

Current liabilities

The current liabilities of a company are the short-term debts that are due within one year or one operating cycle. The quick ratio calculation pulls all current liabilities from the balance sheet of the company. It doesn’t attempt to distinguish between when payments may be due. Hence, the quick ratio formula assumes that all current liabilities have a near-term due date.

The total current liabilities are usually calculated as the sum of various accounts such as wages payable, accounts payable, taxes payable, notes payable, short-term debts, dividends owed, and current portions of long-term debt. Accounts payable, however, is one of the most common current liabilities in a company’s balance sheet.

Quick ratio calculation

How to find the quick ratio is to add the most liquid assets and divide the total by the current liabilities. The most common approach to calculating quick ratio is using the formula:

Quick ratio= Liquid assets / Current liabilities

However, depending on the type of current assets a company has on its balance sheet, the quick assets of a company can be calculated as:

Quick Assets = Cash + Cash equivalents + Marketable securities + Net accounts receivable

The quick assets of a company can also be calculated by deducting illiquid current assets from the balance sheet. For instance, considering that prepaid expenses and inventory may not be easily or quickly converted to cash, the quick assets can be calculated as:

Quick Assets = Total current assets – Inventory – Prepaid expenses

In the quick ratio calculation, no matter the method used to calculate the quick assets, the calculation for current liabilities is calculated the same (i.e all current liabilities are included in the formula).

How to calculate quick ratio example 1

Company A and Company B are two leading competitors operating in the personal care industrial sector. Calculate the quick ratio of Company A and Company B based on the figures given as appeared on their balance sheets for the fiscal year ending in 2021.

| Company A | Company B | |

| Quick Assets | $15,013 | $46,891 |

| Current Liabilities | $33,132 | $45,226 |

Solution

Calculating the quick ratio of Company A using the formula:

Quick ratio= Liquid assets / Current liabilities

Quick ratio (company A)= $15,013 / $33,132= $0.453

Calculating the quick ratio of Company B

Quick ratio (company B)= $46,891 / $45,226= $1.036

The quick ratio analysis interpretation: From the quick ratio calculation done, company A has a ratio of 0.45 whereas, Company B has a ratio of 1.04. Therefore, company B with a quick ratio higher than 1, seems to be in a better position to pay off its current liabilities being that its current assets are greater than its total current liabilities. Company A, on the other hand, with a quick ratio of less than 1 may not be able to settle its current financial obligations using only quick assets. Comparing these two companies may indicate that Company B appears to be in better short-term financial health with respect to liquidity.

How to calculate quick ratio example 2

Mr Johnson owns and runs Company XYZ which has $15 million in cash and cash equivalents, marketable securities of $35 million, $27 million of current liabilities, and accounts receivable of $20 million. What will be the quick ratio of Company XYZ?

Solution

Here is how to find the quick ratio of Company XYZ:

Calculating the quick ratio of Company XYZ using the formula:

Quick ratio= (Cash and cash equivalent + Marketable securities + Accounts receivable) / Current liabilities

First, let’s solve to get the numerator (quick asset) in the quick ratio formula above:

Cash and cash equivalent + Marketable securities + Accounts receivable= $15 million + $35 million + $20 million= $70 million

Quick ratio= $70 million / $27 million= $2.6

The quick ratio analysis interpretation: From the quick ratio calculation done, company XYZ has a ratio of 2.6. Having a quick ratio higher than 1 indicates that the company has more than enough capital to cover its short-term debts. It means that the company has $2.6 of liquid assets that are available to pay off each $1 of its current liabilities.

Example 3: How to calculate quick ratio from a balance sheet

Calculate the quick ratio assuming a company with a current liabilities of $170,000 has the following balance sheet data:

| Assets | Amount |

| CURRENT ASSETS | |

| Cash on hand | $35,000 |

| Cash in bank | $25,000 |

| Short-term investments | $40,000 |

| Inventory | $60,000 |

| Accounts receivable | $85,000 |

| Prepaid insurance | $15,000 |

| TOTAL CURRENT ASSETS | $260,000 |

| NON-CURRENT ASSETS | |

| Fixed assets | $90,000 |

| Goodwill | $30,000 |

| TOTAL NON-CURRENT ASSETS | $120,000 |

Solution

Here is how to calculate the quick ratio from the balance sheet:

Using the formula:

Quick ratio= (Current assets – Inventory – Prepaid expenses) / Current liabilities

First, let’s solve to get the numerator (quick asset) in the quick ratio formula above:

(Current assets – Inventory – Prepaid expenses)= $260,000 – $60,000 – $15,000= $185,000

Quick ratio= $185,000 / $170,000= $1.08

The quick ratio analysis interpretation: From the quick ratio calculation done, the company has a ratio of 1.08. Having a quick ratio of 1 indicates that the company has the needed liquid assets to settle its current liabilities.

Why is the quick ratio important?

The quick ratio is important because it can be used to analyze a single company over a period of time or to compare similar companies. This ratio tells us how well a business will be able to take care of its short-term debts using only the most liquid of assets. It is also important because it serves as an indicator to internal management and external investors whether the business will run out of cash.

This ratio holds more value than other liquidity ratios like the current ratio. This is because it happens to have the most conservative approach to reflecting how liquid a company is. It is a better actual indicator of short-term cash capabilities compared to other calculations that usually include potentially illiquid assets.

One of the advantages of a quick ratio is that it is fairly easy and straightforward to calculate. The quick ratio calculation is relatively easy to understand, particularly when comparing a company’s liquidity against a target figure of 1.0.

Limitations of the quick ratio formula

There are some drawbacks to the quick ratio formula. One of them is that the ratio doesn’t give any indication about the future cash flow activity of a company. For instance, a company may be sitting on $2 million today and may not be selling a profitable good. Hence, the company may struggle to maintain its cash balance in the future. There are also considerations to make in the quick ratio formula in regard to the true liquidity of accounts receivable and marketable securities in some situations.

Quick ratio vs current ratio

The current and quick ratios are both types of liquidity ratios. However, there is a significant difference between the current and quick ratio. The quick ratio is more conservative than the current ratio. This is because it excludes inventory and other current assets that are more difficult to turn into cash. The quick ratio only considers the most liquid assets on the balance sheet of the company. Whereas, the current ratio, considers inventory and prepaid expense assets. Therefore, a quick ratio much smaller than the current ratio reflects that a large portion of current assets is in inventory.

Cash ratio vs quick ratio

The cash ratio, quick ratio, and current ratios are all types of liquidity ratios. Nevertheless, they all vary and are calculated differently. The difference between the cash ratio vs quick ratio is that the quick ratio measures the company’s ability to settle its short-term liabilities using its most liquid assets while the cash ratio measures the company’s ability to settle its short-term liabilities using only cash and cash equivalents.

FAQs

What are quick ratios?

Quick ratios are a type of liquidity ratio that measures the ability of a company to meet its short-term liabilities with its near cash or most liquid assets. This ratio is also known as the acid-test ratio because it indicates the ability of the company to quickly use its near-cash assets (assets that can be converted quickly to cash) to settle its current liabilities.

What does quick ratio mean?

The quick ratio means a company may have or may not have enough liquid assets that can be converted into cash to settle its current liabilities. A quick ratio of less than 1 can indicate that the business may not be capable of fully paying off its current liabilities in the short term. Whereas, a business with a quick ratio higher than 1 can immediately get rid of its current liabilities.

What is the quick ratio definition?

We can define quick ratio as a liquidity ratio that tells us whether a company has enough liquid assets that can be converted into cash to settle its current liabilities. This ratio is called a quick ratio because it only looks at the most liquid assets that are available in a company to service short-term debts and obligations.

What is the quick ratio formula in accounting?

The formula for a quick ratio can be expressed as:

Quick ratio (Acid-test ratio)= Liquid assets / Current liabilities

What does the quick ratio inform you about a company?

A quick ratio analysis interpretation informs you of a company’s ability to settle its current liabilities using its liquid assets that can be converted into cash. The ratio would measure the dollar amount of available liquid assets of the company against the dollar amount of the company’s current liabilities.

What is a good quick ratio for a company?

Whether a company has a good quick ratio or not may depend on several factors such as industry, growth, risk, economic conditions, accounts receivable, and inventories (the company might have a type of inventory that was easy to quickly liquidate). Notwithstanding, an ideal quick ratio is considered to be 1, which indicates that the company is fully equipped with the needed liquid assets to settle current liabilities.

A quick ratio of less than 1 can indicate that the company may not be capable of fully paying off its current liabilities in the short term.

What does quick ratio measure?

The quick ratio measures whether a company has enough liquid assets that can be converted into cash to pay its bills.

What is current ratio and quick ratio?

The current ratio is a liquidity ratio that measures a company’s ability to settle its short-term liabilities. Whereas, the quick ratio is a liquidity ratio that measures a company’s ability to settle its short-term liabilities using its liquid assets. The quick ratio only considers the most liquid assets on the balance sheet of the company. Whereas, the current ratio, considers inventory and prepaid expense assets.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.