The return on assets formula is an expression used to measure the amount of profit that is generated by a company from its assets. In finance, the ROA calculation is used to measure how efficient a company’s management is in earning a profit from the assets or economic resources on its balance sheet.

This article will discuss the return on assets formula, the ROA calculation, and its uses.

What is the return on assets ratio?

The return on assets ratio (ROA) is a financial ratio that measures the profitability of a company in relation to its total assets. This ratio is commonly expressed as a percentage and is used by analysts, corporate management, and investors to determine how a company efficiently makes use of its assets to generate profit.

The return on assets is most closely related to the debt to assets ratio and profit margin. Calculating return on assets is done by using a company’s net income and its total or average assets. This means that a company that is more efficient and productive at managing its assets to generate profit will have a higher ROA. Whereas, a company having a lower ROA indicates room for improvement.

Related: Tangible assets

Return on assets interpretation

The return on assets measures the profitability of a company in relation to its total assets. Efficiency is very key in business and a company’s profit can be compared to its revenue. The feasibility of the company’s existence can be determined by comparing the company’s profit to the resources used to earn these profits and revenue. Therefore, the return on assets interpretation gives a clearer picture of the earnings generated from a company’s invested assets and capital.

How to analyze return on assets is to compare the ROA of a company to companies in the same industry. This is because the return on assets for public companies can vary substantially depending highly on the industry in which the companies operate. For instance, the ROA for a tech firm won’t necessarily tally with the ROA of a food and beverage firm. Hence, when using the return on assets ratio as a comparative metric, it is best to compare the ROA against another company’s ROA in the same industry or the company’s current ROA should be compared with the previous ROA of the company.

What does return on assets ratio tell us?

The return on assets ratio interpretation tells investors how efficient a company is in converting its invested money into net income. The higher the ROA of a company the better. This is because investors interpret a higher return on assets as the company being able to generate more money with a smaller investment. Therefore, a higher ROA indicates more asset efficiency.

However, it is important to note that the return on assets ratio interpretation is more accurate and useful when comparing companies in the same industry based on the fact that different industries use assets differently. For instance, the return on assets for service-oriented firms, like banks, will be significantly higher than the return on assets ratio for capital-intensive companies, like utility or construction companies.

What does a low return on assets mean?

A company with a low return on assets would likely have more assets involved in generating its profits. Companies having lower ROA compared to the industry average can be a red flag. This is because a low return on assets means that the management might not be deriving the full potential benefits from the assets it owns.

More so, companies with a low ROA tend to have more debt due to the fact that they need to finance the cost of the assets. However, debt financing is not necessarily a bad thing, as far as the management uses it effectively to generate earnings.

Therefore, it is crucial to compare a company’s ROA over multiple accounting periods. A year of a lower ROA may not be a concern if the management team of the company is investing in its future and this investment is forecasted to increase profits over the coming years.

What does a high return on assets mean?

A company with a high ROA would likely have fewer assets involved in generating its profits. The return on assets ratios that are higher than 15% could be an indication that the company has made more profit for each dollar of assets it has employed.

A high return on assets means that the company’s assets are being used to their near full capacity, or at the very least, used more efficiently than its industry peers. This means that companies with consistently higher ROAs can generate more profits using the same amount of assets compared to companies with lower ROAs. Therefore, companies with high ROA are more likely to perform well in the long run. They may even become market leaders with higher profit margins.

However, a higher ROA than average may not always be a good sign of efficiency. It could also mean that the company isn’t investing enough in assets, which cause problems in the future. More so, some companies make it look like the ROA is exceptionally high by finding ways to keep their assets off the books. Additionally, measuring the ROA may not be an effective way to evaluate companies in creative fields. This is because, in such fields, brainpower generates profits rather than equipment.

What does a negative return on assets mean?

A negative return on assets could mean that the company is gravitated towards having more invested capital or earning lower profits. If the net income of a company is in the red, the ROA will be negative as well. A company having a negative net income could be buying up assets that will generate profits in the future or could be losing money.

Take, for instance, a company that has equipment worth $100,000 and a profit of $20,000 earned from cash and accounts payable with a ROA of 20 percent. Now, supposing this company lost money or gained assets in excess of their profits, the ROA will become negative. For example, the company purchasing a large piece of equipment for $50,000, will warrant the company using its $20,000 in profit with an additional $30,000 gotten as a loan. This definitely results in net profits of -$30,000 with assets of $150,000. Therefore, resulting in a ROA of -20 per cent (i.e -$30,000 / $150,000).

Looking at this example, the negative return on assets ratio doesn’t necessarily mean a bad thing as the piece of equipment bought could generate profits for the company in the future. Therefore, a lower or negative ROA isn’t necessarily always bad. For instance, it is possible for a company to have a positive cash flow but write off a lot of revenue because of depreciation. In addition, even major companies can have a negative return on assets.

What is a good ROA?

A ROA of over 5% is generally considered a good return on assets. It is considered excellent when the ROA is even over 20%. Nevertheless, whether a company’s ROA is a good return on assets or not would depend on the average ratio in the industry. This means that to get a reliable result, it is better to always compare ROAs amongst companies in the same sector.

Take, for instance, a software company that has far fewer assets on the balance sheet. Comparing this firm with a car manufacturing company is futile because the software maker has lesser assets than the car maker. Therefore, the assets of the software company will be understated and its ROA may get a questionable boost.

Furthermore, a rising ROA tends to be a good sign, indicating that the company is increasing its profits with each dollar invested in the total assets of the company. A declining ROA, on the other hand, can be an indication that the company may have made poor capital investment decisions and is not deriving enough profit to justify the cost of purchasing those assets. It could also be a signal that the company’s profits are shrinking due to declining sales or revenue.

Related: Return on equity ratio

Return on assets formula

The formula for the return on assets is computed by dividing the net income of a company by its total assets. The numerator of the ROA formula can be found at the bottom of a company’s income statement while the denominator of the return on assets ratio formula can be found on the company’s balance sheet.

What is the formula for return on assets?

The formula for the return on assets ratio is expressed as:

ROA= Net income / Total assets

Where,

Net income= The sales made by the company minus the cost of goods sold, general expenses, interests, and taxes.

Total assets= The total amount of assets owned by the company

Alternatively, the ROA calculation can be done by dividing the company’s net income by the average of its total assets. The average total assets can be used in the formula for return on assets ratio because a company’s total assets can vary over time due to seasonal sales fluctuation, the purchase or sale of land, vehicles, equipment, or inventory changes. Due to this, calculating the return on assets using the average total assets for the period in question is more accurate than using the total assets for one period.

This gives us a more sophisticated return on assets formula, which is expressed as:

ROA= Net income / Average total assets

This ROA formula takes into account the fact that the value of a company’s assets changes over time. Therefore, during the ROA calculation, the average value of assets that a company owns in a given year is used instead of the total value of the company’s assets at year-end. After dividing the net profit by average assets, multiply the value by 100 to get the ROA percentage.

ROA calculation

The ROA calculation can be very helpful in comparing the profitability of a company over multiple quarters and years. The return on assets calculation can also be helpful to compare a company’s profitability to similar companies. Nevertheless, the return on assets formula should be used with other financial ratios to determine a company’s financial performance.

How do you calculate return on assets?

The return on assets ratio is calculated by dividing the net income of a company by its total assets or average total assets. Here are some examples of how to calculate the return on assets ratio:

Calculation for return on assets: Example 1

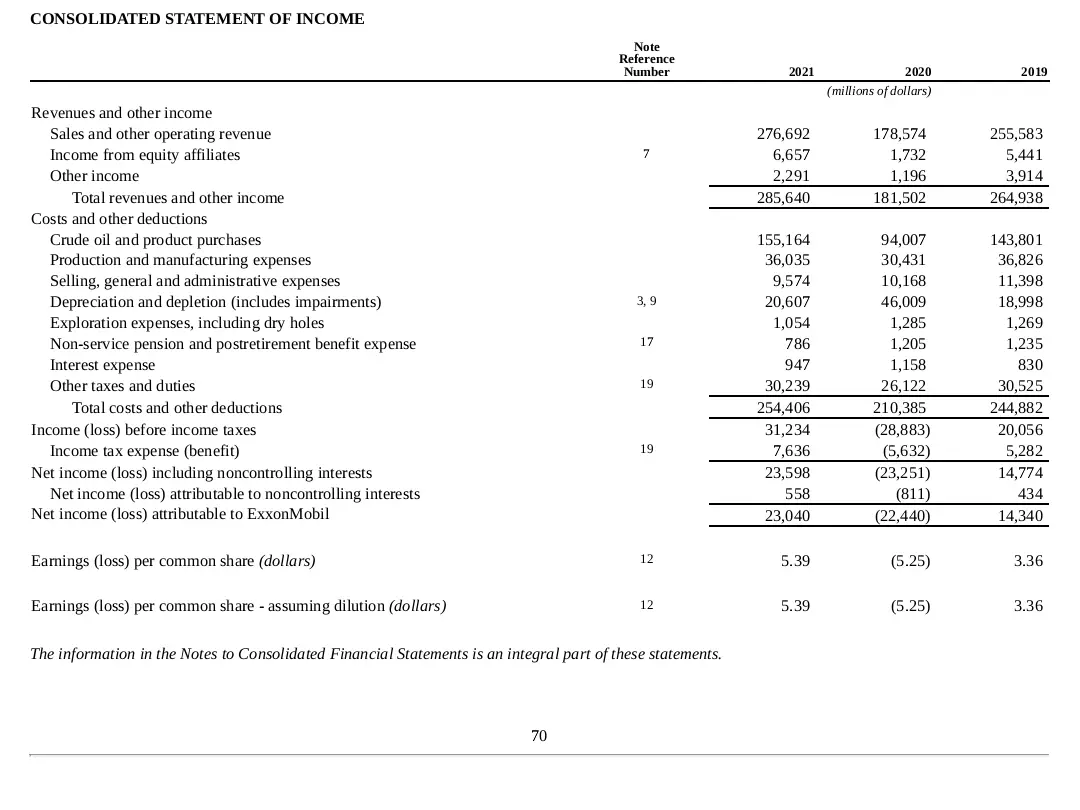

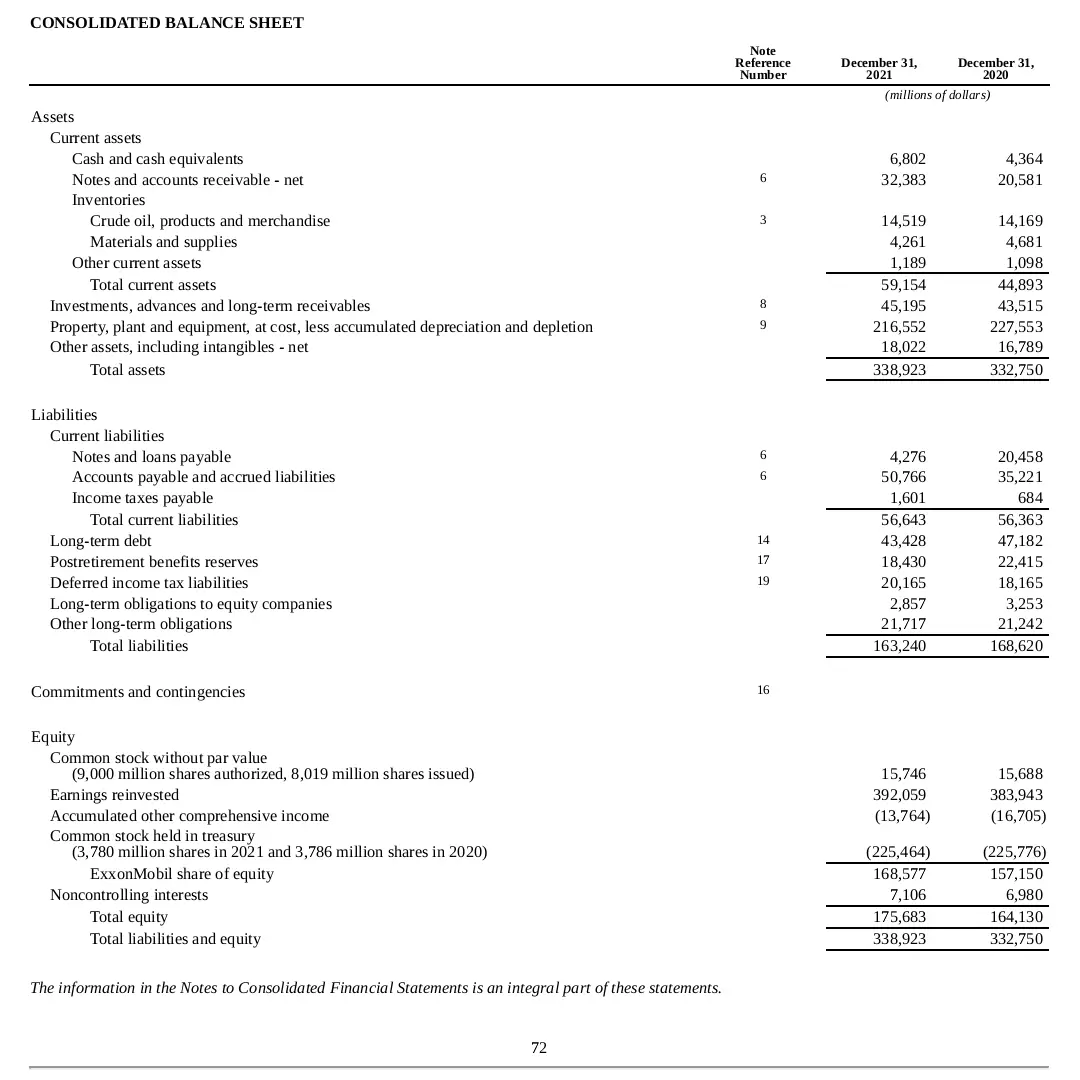

We are going to look at an example of how to find return on assets from the balance sheet. Using the Exxon Mobil Corporation (XOM) as an example, below is an excerpt of Exxon’s income statement and balance sheet from its 10K statement (pages 72 & 74) for 2020 and 2021.

We are going to compare the company’s ROA for 2020 with its ROA for 2021. From the excerpt, we can see the following data:

For 2020

Net income= $22,440 million

Total assets= $332,750 million

For 2021

Net income= $23,040 million

Total assets= 338,923 million

Solution

How to compute return on assets for Exxon (2020)

Using the return on assets formula: ROA= Net income / Total assets

ROA= $22,440 million/ $332,750 million

ROA= 0.0674

Therefore, for 2020, the return on assets is equal to 6.74%

Calculating for 2021

ROA= $23,040 million / $338,923 million

ROA= 0.0679

Therefore, for 2021, the return on assets is equal to 6.79%

Return on assets interpretation: Comparing the ROA of Exxon Mobil Corporation in 2020 to that in 2021 shows a slight increase (from 6.74% to 6.79%). A rising ROA tends to be a good sign, indicating that Exxon is increasing its profits with each dollar invested in the total assets of the company. More so, a ROA of over 5% is generally considered a good return on assets ratio.

How to calculate return on assets example 2

Calculate and compare the return on assets ratio of the three companies given in the table below. The data in the table is for the trailing 12 months (TTM) and shows the net income and total assets for Company A, B, and C in the retail industry.

| Company A | Company B | Company C | |

| Net income | $1.7 billion | $996 million | $243 million |

| Total assets | $20.4 billion | $14.1 billion | $3.9 billion |

Here is how to find return on assets for Company A, B and C

Using the return on assets equation: ROA= Net income / Total assets

For Company A

ROA= $1.7 billion/ $20.4 billion

ROA= 0.083

Therefore, the ROA calculation for Company A is 8.3%

For Company B

ROA= $996 million/ $14.1 billion

ROA= 0.0706

Therefore, the return on assets is equal to 7.06%

For Company C

ROA= $243 million/ $3.9 billion

ROA= 0.0623

Therefore, the ROA calculation for Company C is 6.23%

Return on assets interpretation: From the ROA calculation done, it is seen that every dollar that Company A invested in assets generated 8.3 cents of net income. From the differences in the return on assets ratio, Company A was better at converting its investment into profits, compared with Company B and Company C. Nevertheless, the return on assets ratio of Company B and Company C is fair and good enough for its industry.

See also: Intangible assets

How to increase return on assets

- Increasing the net income of a company will help increase the ROA.

- In order to increase return on assets, companies should manage their current assets effectively.

- Companies properly managing their fixed assets will have an impact on the company’s net income and total assets, thus boosting the ROA.

- The companies that have investments in other companies in form of financial assets, associates, or other types of investments can manage them well to generate returns different from the main business operating activities in order to increase ROA.

- Decreasing the total asset of a company while the net profit remains the same can help increase the return on assets ratio of a company.

Advantages and use of the ROA calculation

Investors can use the return on assets ratio to find stock opportunities. The ratio is relevant in finding stock opportunities as it shows the efficiency of a company at using its assets to generate profits. A ROA that rises over time shows that the company is doing well at increasing its profits with each investment dollar it spends. Whereas, a declining ROA may indicate a company that might have over-invested in assets that have failed to produce revenue growth. This could be a red flag for investors to buy the company’s stock.

The ROA calculation can be used to make comparisons across companies in the same sector or industry. The ratio is an indicator of performance that incorporates the company’s asset base. Calculating the ROA of a company gives information about the relationship between the company’s income and assets employed.

The major advantage of the return on assets ratio is that it takes into consideration all types of assets, such as the company’s property, working capital, equipment, and investments in securities. This ratio serves as a good measure of management performance as it focuses on the assets being used to generate earnings for shareholders and investors.

Limitations of the return on assets formula

One of the biggest limitations of the return on assets formula is that it can’t be used across industries. This is because companies in one industry have different asset bases than others in another industry. For instance, the asset bases of companies within the retail industry are not the same as companies in the oil and gas industry.

Also, some analysts are of the opinion that the basic return on assets formula is limited in its applications, as the formula is most suitable for banks. Bank balance sheets represent the real value of their assets and liabilities better because they’re carried at market value through mark-to-market accounting versus historical cost. Therefore, interest income and interest expense are both already factored into the equation.

But for non-financial companies, this is not the case as debt and equity capital are strictly segregated, as are the returns to each. The interest expense is the return for debt providers and the net income is the return for equity investors. Therefore, the basic ROA formula mixes things up by comparing returns to equity investors (net income) with assets funded by both debt and equity investors (total assets).

Due to these concerns, there are two variations on the return on assets formula used by analysts to fix the inconsistency with the numerator and denominator by putting interest expense (net of taxes) back into the numerator. So the ROA formula is expressed as:

Variation 1: ROA= Net Income + [Interest Expense x (1 – Tax Rate)] / Total Assets

or

Variation 2: ROA= Operating Income x (1 – Tax Rate) / Total Assets

Related: Debt ratio

FAQs

What is ROA?

ROA means a return on assets. This is a ratio that shows a company’s net income as a percentage of total assets. The return on assets shows how efficient a company is in converting its invested money into net income.

What is a good return on assets for a company?

A ROA of over 5% is generally considered a good return on assets for a company. Nevertheless, whether a company’s ROA is a good return on assets or not would depend on the average ratio in the industry. This means that to get a reliable result, it is better to always compare ROAs amongst companies in the same sector.

Can return on assets be negative?

Yes, it is possible to get a negative return on assets. If the net income of a company is in the red, the ROA will be negative as well. A company having a negative net income could be buying up assets that will generate profits in the future or could be losing money.

Is a high return on assets good?

A high return on assets means that the company’s assets are being used to their near full capacity, or at the very least, used more efficiently than its industry peers. Is a higher return on assets better? Yes, the higher the ROA, the better. However, a higher ROA than the industry average may not always be a good sign of efficiency. It could mean that the company isn’t investing enough in assets, which could cause problems in the future.

What causes a rise in the return on assets?

Increasing the net income or decreasing the total asset of a company can cause a rise in the return on assets.

How does supply management affect return on assets?

Efficient supply management affects the return on assets positively. It increases the net profit of the company which is the numerator of the ROA formula and reduces the total assets (denominator) as well. The combined effect increases the return on assets.

Is return on assets the same as return on investment?

Return on assets (ROA) and return on investment (ROI) are two vital ratios used to measure returns derived proportionate to assets and investment respectively. They are not the same. The former (ROA) calculates how much income is generated as a percentage of total assets while the latter (ROI) measures the income generated as opposed to investment.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.