When investors put their money into a company by purchasing the stocks of that company, they often do so with the hope of either getting paid dividends, capital gains, or both. In order for companies to declare distributions and pay dividends to their investors, they have to first make use of the invested funds to make a profit. The return on equity (ROE) is a measure of financial performance that is used to gauge how efficient a company is in generating profits and its profitability.

ROE alone might not give in-depth details on the company’s profitability. Hence, the Dupont formula further breaks it down to aid with an easier understanding of how a company’s ROE changes with any change in the formula’s components.

See also: Income Statement Ratios Formulas and Examples

Return on equity (ROE)

As mentioned earlier. ROE is a measure of financial performance. It is a two-part ratio that brings together the items on the income statement and balance sheet of a company. This is done by dividing a company’s net income, which is found on the income statement by shareholder’s equity, which is found on the balance sheet. ROE is normally expressed as a percentage by multiplying the result gotten from the previous division by 100.

What is the formula for calculating ROE?

ROE can be calculated by dividing a company’s net income by its shareholder’s equity and then expressed as a percentage. This is expressed as ROE = (Net income ÷ Shareholders equity) x 100

Return on equity is generally useful when comparing the performance of companies that are operating within the same sector. It is also used by analysts and investors along with other financial ratios when carrying out a stock valuation. ROE measures the profits a company makes for every dollar that has been invested by its shareholders. It shows the company’s ability to turn equity investments into profits and represents the total return on shareholder’s equity.

ROE varies from one sector to another, hence a high ROE in one sector might be considered low in another. This is why ROE can only be used to compare companies within the same sector. When using a company’s ROE to gauge its management’s efficiency in utilizing shareholders’ equity to make profits, one should consider the industry average which is made available by indexes such as the S&P 500. ROE lower than this average is usually considered low while those above it are considered high.

See also: Debt to EBITDA ratio formula and calculation

Dupont formula

The DuPont formula is an expression that breaks return on equity down into three parts: net profit margin, asset turnover, and financial leverage. This equation was developed by Frank Donaldson Brown in 1914 while he was working for the Dupont Corporation. He called the formula return on investment (ROI). The formula incorporated investment, working capital, and earnings into a single figure. It was adopted and used in the business operations of the company. The Dupont formula is also known as the Dupont method, Dupont identity, Dupont model, strategic profit model, or Dupont analysis.

By using the Dupont formula, the company’s operating efficiency, asset use efficiency, and financial leverage are weighed. This aids companies, analysts, and investors in easily understanding the changes that occur in a company’s ROE over time. There are two variations of the Dupont formula. The first one has three parts while the second one has five parts. We shall look at each of these variations below:

3-part Dupont formula

- Net profit margin

- Asset turnover

- Equity multiplier

The 3-part Dupont formula is gotten by multiplying net profit margin, asset turnover, and equity multiplier. It is expressed as Dupont formula = Net profit margin x Asset turnover x Equity multiplier

Net profit margin

The net profit margin is a profitability ratio that measures how much income or profits a company makes compared to its revenue or sales. It is an indicator of how well a company controls cost as well as its goods and services pricing strategies. It further reveals how much of the revenue generated by a company is actually converted to profit. This ratio can be expressed as a decimal although it is generally multiplied by 100 and expressed as a percentage.

As a part of the Dupont formula, when the profit margin of a company increases, its ROE will also increase. The net profit margin is also referred to as net margin and is expressed as Net profit margin = (Net income ÷ Revenue) x 100

Asset turnover

Asset turnover is an efficiency ratio that measures how efficiently a company uses its assets to generate income by comparing its net sales or revenue to its average total assets. Generally, companies with high asset turnover tend to have low net profit margins while those with low asset turnover tend to have high net profit margins. As a component of the Dupont formula, when the asset turnover increases, it positively affects the Dupont equation, thus, increasing the ROE.

Asset turnover is expressed as Asset turnover = Net sales ÷ Average total assets

Where average total assets = (Beginning assets + Ending assets) ÷ 2

Beginning assets are the company’s assets at the start of the year while ending assets are its assets at the end of the year

Equity multiplier

The equity multiplier measures the portion of a company’s assets that is financed by shareholder’s equity rather than debt. It attempts to understand a company’s ownership weight through the analysis of how its assets are financed. Companies with a low equity multiplier usually have a large portion of their assets financed by shareholder’s equity which also means that the company is not highly leveraged. Just as an increase in net profit margin and asset turnover increases a company’s ROE, an increase in a company’s equity multiplier also has the same effect.

The formula for equity multiplier is expressed as Equity multiplier = Average total assets ÷ Average shareholder’s equity

5-part Dupont formula

- Tax burden

- Interest burden

- Operating margin

- Asset turnover

- Equity multiplier

The 5-part Dupont formula is an elaboration of the 3-part Dupont formula. It is basically an expansion of the net profit margin into tax burden, interest burden, and operating margin. This is then multiplied by the asset turnover and equity multiplier. The expansion further gives more in-depth details for anyone seeking to better understand a company’s ROE. This formula is expressed as Dupont analysis = Tax burden x Interest burden x Operating margin x Asset turnover x Equity multiplier

Since we have already looked at the asset turnover and equity multiplier formulas earlier, let us look at the formulas for the remaining part of the formula.

Tax burden

The tax burden ratio measures the tax liability of a company. It does this by dividing the company’s net income by its pre-tax income. The result represents the portion of the company’s profits that is left after they had made tax payments. This is expressed as Tax burden = Net income ÷ Pre-tax income

Interest burden

The fact that a lot of businesses are financed by debts makes the interest burden an important component to be considered when analyzing a company’s ROE hence its incorporation into the 5-part Dupont analysis. It measures the extent to which interest expense impacts profits by dividing a company’s pre-tax income by its operating income. This is expressed as Interest burden = Pre-tax income ÷ Operating income

Operating margin

The operating margin otherwise known as operating profit (EBIT) measures the profits made by a company per dollar of sales after deducting the cost of goods sold (COGS) and operating expenses. It is calculated by dividing the company’s operating income by net sales or revenue. As with other components of the Dupont formula, a high operating margin increases a company’s ROE.

Companies whose operating margin is high indicate that they are good at turning their sales into profit and are efficient in their operations. The formula is expressed as Operating margin = Operating income ÷ Revenue

See also: Debt to capital ratio formula and interpretation

ROE with Dupont Formula Example

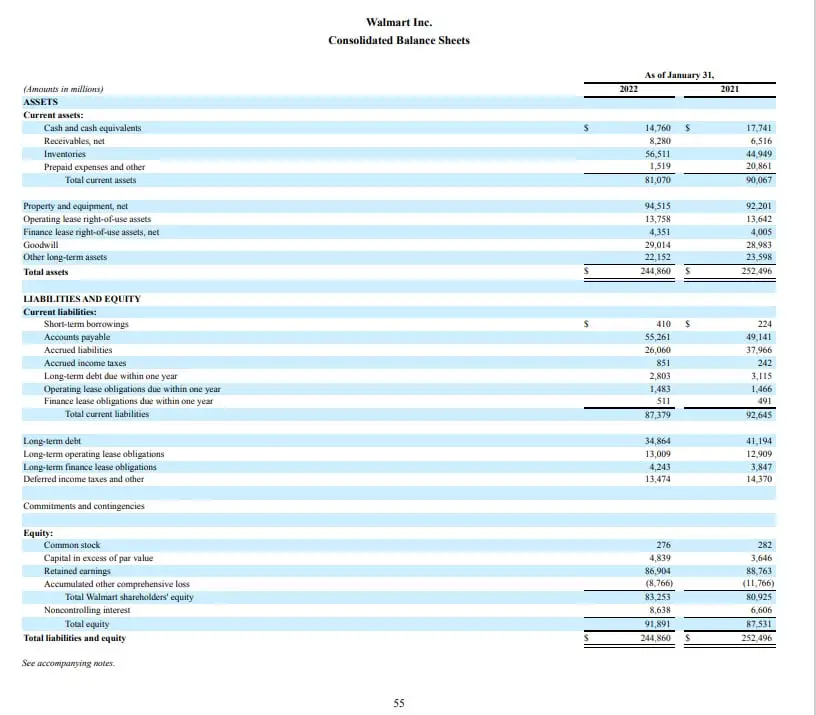

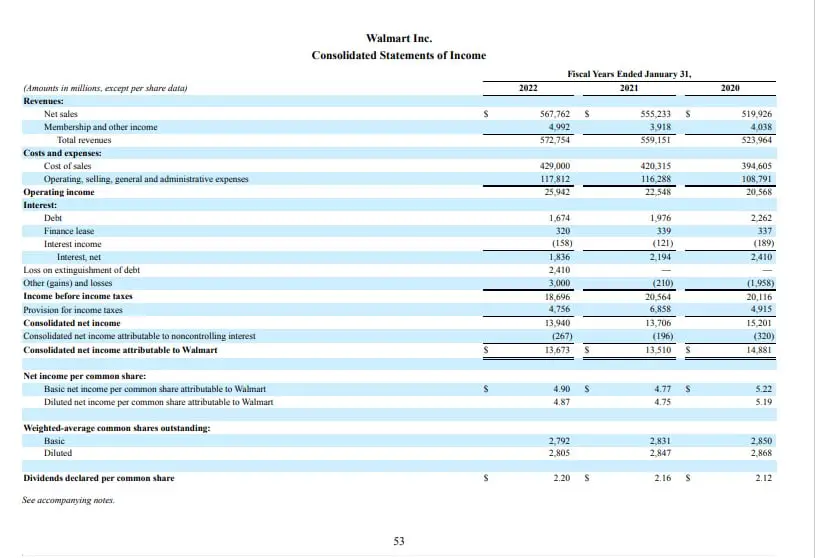

Using the information from Walmart’s balance sheet and income statement above, let us calculate their ROE for the fiscal year 2022 using the 3-part Dupont formula.

Dupont formula = Net profit margin x Asset turnover x Equity multiplier

Before we can make use of the Dupont analysis, let us first calculate the components.

Net profit margin = (Net income ÷ Revenue) x 100

Net income = $13,673,000

Revenue = Net sales = $567,762,000

Net profit margin = ($13,673,000 ÷ $567,762,000) x 100

Net profit margin = 0.024082 x 100

Net profit margin = 2.4082

Asset turnover = Net sales ÷ Average total assets

Net sales = $567,762,000

Average total assets = $244,860,000

Asset turnover = $567,762,000 ÷ $244,860,000

Asset turnover = 2.3187

Equity multiplier = Average total assets ÷ Average shareholder’s equity

Average total assets = $244,860,000

Average shareholder’s equity = $83,253,000

Equity multiplier = $244,860,000 ÷ $83,253,000

Equity multiplier = 2.9412

Now that we have found the various components, we can input them into the Dupont formula and find Walmart’s return on equity for the year 2022.

Dupont formula = Net profit margin x Asset turnover x Equity multiplier

Dupont formula = 2.4082 x 2.3187 x 2.9412

Dupont formula = 16.42

From our calculation, we have ascertained that the ROE for Walmart in the year 2022 was 16.42%

See also: Cash ratio formula, interpretation, and examples

Conclusion

By splitting ROE using the Dupont formula into three or five parts, companies, investors and analysts can more easily understand the changes that occur in their return on equity over time. As the value of a company’s net profit margin, asset turnover, and equity multiplier increases, it translates into an increase in its ROE. This means that the component parts of the Dupont analysis contribute to the outcome of a company’s ROE.

Additionally, breaking down ROE with the Dupont formula makes it easier to trace the particular component of the equation that is a dominant factor in determining a company’s ROE. For instance, while asset turnover is the dominant factor in industries in sectors with a high turnover such as retail stores, high-margin industries such as haute couture and luxury brands have profit margin as their dominant determinant of ROE. Industries in the financial sector such as banks have equity multipliers as their dominant determinant of ROE.

When comparing the ROE of companies within the same industry, the Dupont formula can be employed to ascertain how the companies compare to each other in the various aspects that make up the equation.

Last Updated on November 3, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.