The statement of cash flows or cash flow statement is an important financial statement that shows the cash inflows and outflows of a company over a period of time. Every company that sells stocks to the public is required by the securities and exchange commission (SEC) to file its financial statements such as balance sheet, income statement, cash flow statement, and statement of comprehensive income.

What is a statement of cash flows?

The statement of cash flows is a financial statement that shows how much cash a company has on hand, as well as where that cash came from and where it went over a certain period of time. It is also called the cash flow statement. The statement of cash flows provides a snapshot of a company’s cash inflows and outflows over a given period of time (known as the reporting period). It is typically used to assess a company’s financial health and liquidity, as well as its ability to pay its bills and meet its short-term obligations.

Therefore, the statement of cash flows can be used to assess a company’s liquidity, solvency, and ability to generate cash.

The purpose of the cash flow statement is to show investors and creditors whether or not a company has the ability to pay its bills. This type of financial statement also provides insights into how well a company is managed and how efficiently it operates.

What does the cash flow statement show?

The statement of cash flows shows the operating, investing, and financing activities of a company. It shows how much cash a company has generated or used over a certain period of time arising from these activities. The main purpose of a cash flow statement is to help manage the company’s financial affairs and make decisions about investing, financing, and other activities.

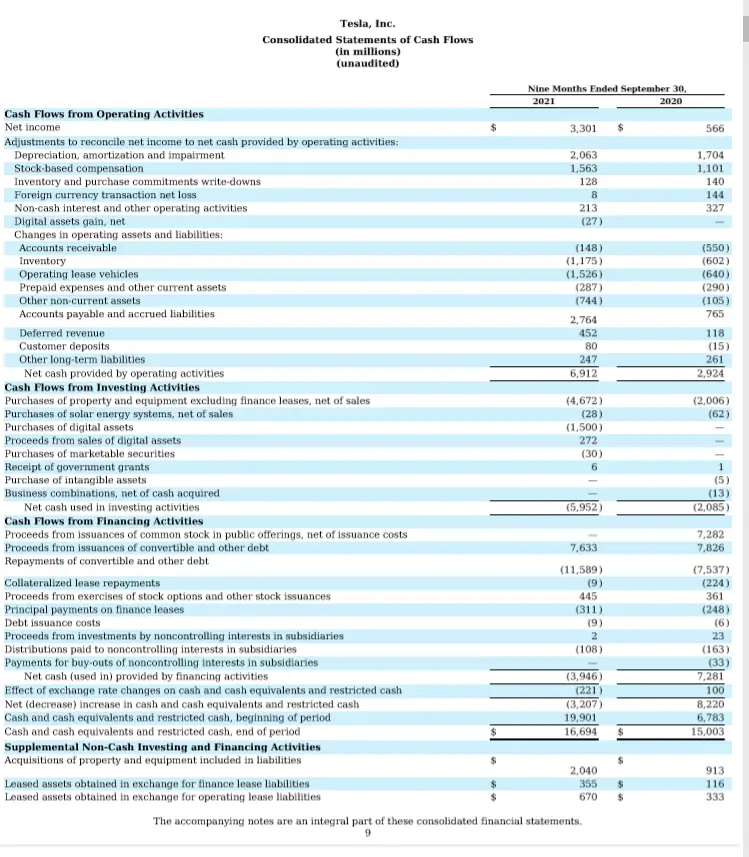

Sample

Statement of cash flows explained

The statement of cash flows has three main sections: operating activities, investing activities, and financing activities. Each of the 3 sections of cash flow statement would be discussed below.

Operating activities in cash flow statement

The statement of cash flows operating activities includes all the cash coming into and going out of the business from its core operations. It involves all the cash inflows and outflows arising from current assets and current liabilities.

The operating section of the cash flow statement shows the cash inflows and outflows from the company’s day-to-day operations. It includes items such as revenue from sales, expenses such as rent and payroll, and other operating income and expenses.

The operating activities of the cash flow statement could include revenue from product sales, as well as money spent on things like inventory, employee salaries, and rent.

List of operating activities on cash flow statement

- Sales revenue: from products or services rendered

- Sales of Inventory

- Purchase of Inventory

- Salaries expense

- Rent expense

Investing activities in cash flow statement

This section shows the cash inflows and outflows from the company’s investments. The cash flow statement investing activities include items such as the purchase or sale of investments, proceeds from the sale of property or equipment, and any other investing income or expenses.

In general, investing activities in cash flow statement are all the cash flows related to the purchase or sale of long-term assets, such as property or equipment. The cash flow from the investing section is important in identifying the changes in capital expenditures (CapEx).

Examples of investing activities in cash flow statement

- Sale of property

- Purchase of property

- Sale of plant

- Purchase of Plant

- Sale of equipment

- Purchase of equipment

Financing activities of the statement of cash flows

Financing activities are all the cash flows related to a company’s borrowings and repayments of debt, as well as any dividends or other distributions to shareholders.

This section shows the cash inflows and outflows from the company’s financing activities. It includes items such as loans taken out or repaid, issuance of new equity or debt, dividends paid to shareholders, and any other financing income or expenses.

Examples of financing activities in cash flow statement

- Loans taken

- Loan repayment

- Issuance of new equity

- Payment of dividends to shareholders.

- Buyback of shares (Treasury stock)

In general, financing activities on a statement of cash flows relate to the raising or repayment of capital.

Looking at a statement of cash flows can give you valuable insights into a company’s overall financial health. For example, if a company is consistently spending more cash than it is generating from operating activities, that could be a sign that it is in trouble and may not be able to sustain itself in the long run.

Statement of cash flows purpose

The purpose of the statement of cash flows is to give investors and creditors an idea of the company’s financial health and liquidity. For investors who are interested in growth stocks, a company with high capital expenditure shows the company is investing in growth and the company would be their choice; this means investors interested in growth stocks would look for positive cash flows from investing activities whereas investors interested in income stocks would look for a positive cash flow from operating activities.

This means the operating section of cash flow statement is important for income stock investors while the investing section of cash flow statement is important for growth stock investors.

For creditors, they are interested in the financing section of cash flow statement because it shows whether a company is actively paying back debt. The financing section of cash flow statement also shows if a company is paying dividends or buying back shares (treasury stocks).

Examples of statement of cash flows

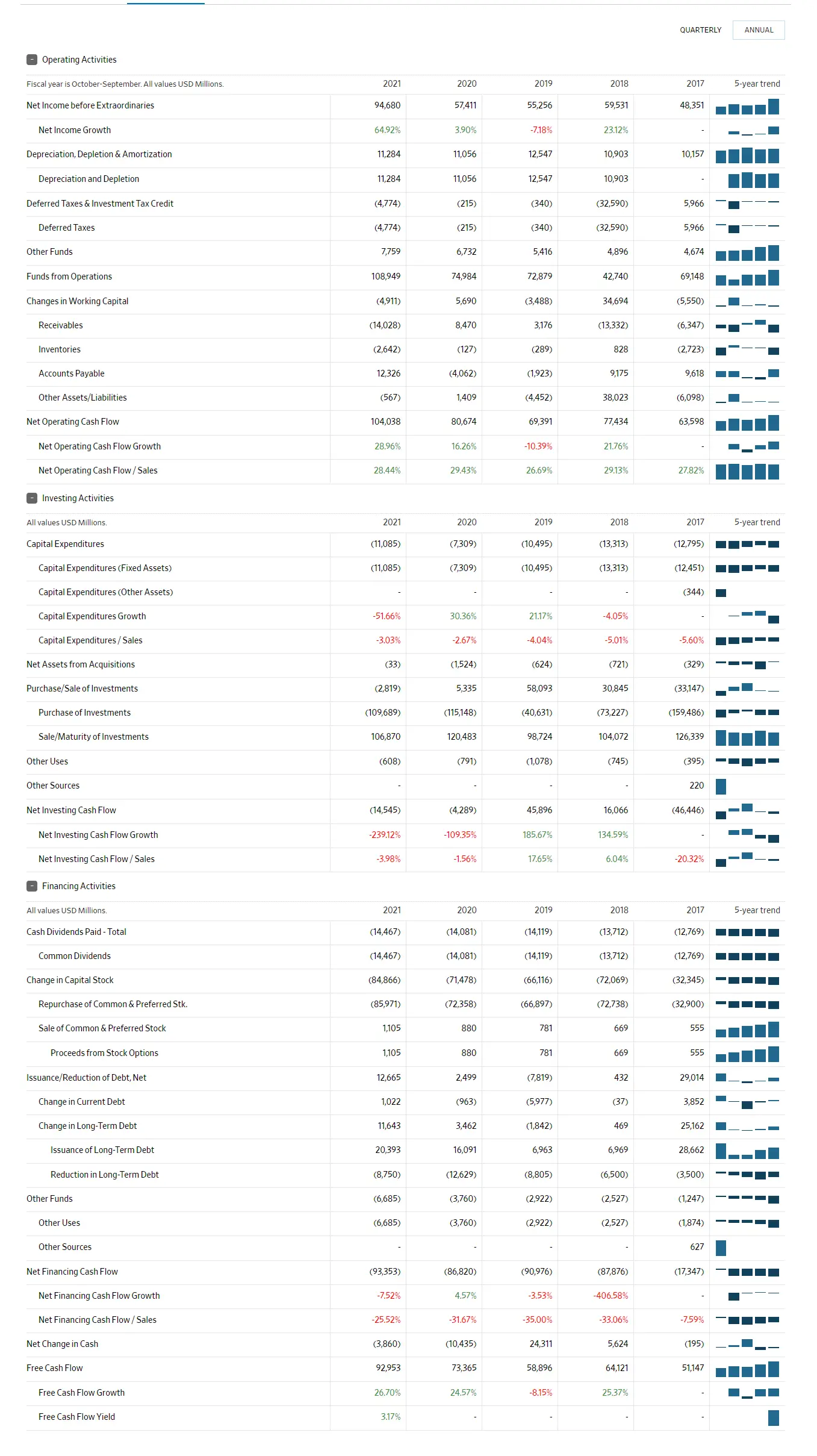

Apple’s statement of cash flows 5-year trend 2017 to 2021

Source: WSJ.com

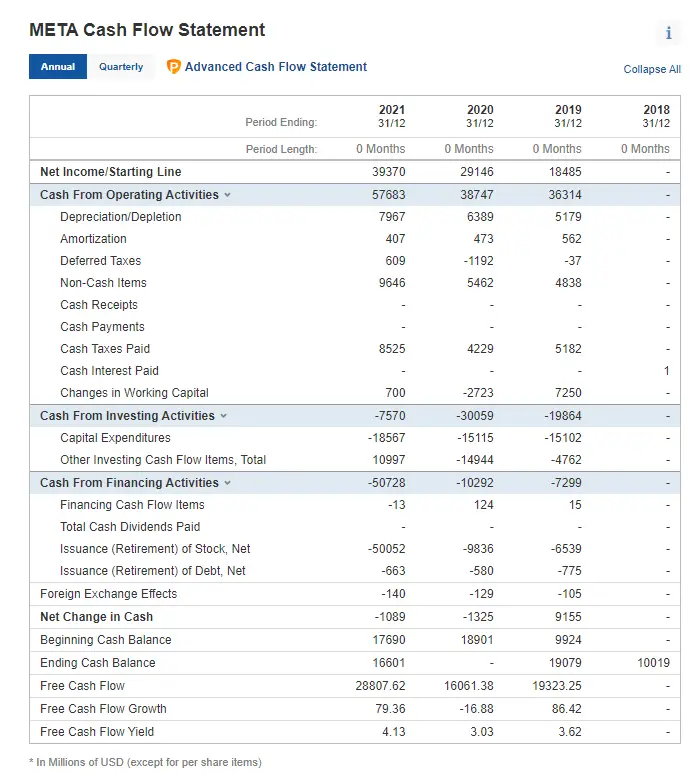

(META) Facebook statement of cash flows

Source: Investing.com

Preparation of cash flow statement

The preparation of a cash flow statement requires careful consideration of all of the company’s activities that could impact its cash position. There are two methods of preparing a statement of cash flows: the indirect and direct methods. We will see how each of these two methods is used for preparing cash flow statements with their differences and similarities.

Statement of cash flows indirect method

The indirect method of preparing a cash flow statement involves starting with the net income for the period and then adjusting it for non-cash items that affected net income. These items include depreciation, amortization, deferred taxes, and other non-cash items. This results in the cash provided by operating activities. It uses the accrual method of accounting which records sales when earned and not necessarily when the cash is received.

This means the indirect statement of cash flows adjusts net income for the changes in balance sheet accounts to calculate the cash flow from operating activities. Regulatory boards generally accept this method because it provides more information about a company’s operating cash flows than the direct method.

How to prepare a statement of cash flows using the indirect method

The first step in calculating operating cash flows using the indirect method is to adjust net income for items that do not affect cash. These non-cash items include depreciation and amortization. Adding back these expenses provides us with the company’s operating profit before interest and taxes (EBIT).

Next, we need to adjust EBIT for changes in other working capital items on the balance sheet. These items include accounts receivable, inventory, and accounts payable. Adjusting for these changes tells us how much cash was generated (or used) by a company’s operations during the period.

Finally, we add any interest and tax payments made during the period to arrive at the total cash flow from operating activities.

The goal of the indirect statement of cash flows is to ultimately arrive at the same cash flows that would be reported using the direct method.

There are three main types of adjustments that need to be made: operating, investing, and financing.

Operating activities involve generating revenue and incurring expenses. Adjustments for operating activities typically include items like accounts receivable, inventory, and accounts payable.

Investing activities involve acquiring or disposing of long-term assets. Adjustments for investing activities might include items like depreciation or changes in the value of investments.

Financing activities involve raising or repaying capital. Adjustments for financing activities could include items like debt issuance or stock buybacks.

Statement of cash flows direct method

The direct method of preparing a cash flow statement is the preferred method by businesses and investors. The direct method is simple, easy to understand, and provides straight forward detailed information about a company’s cash flow than the indirect method. It uses the cash method of accounting where the actual cash received is recorded.

The difference between the indirect method and the direct method of cash flow statement lies in how the operating activities are reported. Other sections such as investing and financing activities are reported the same way in both the direct and indirect methods.

How to prepare a statement of cash flows using the indirect method

To prepare a cash flow statement using the direct method, businesses list all major cash receipts and payments for the period under consideration. These items are then categorized as operating activities, investing activities, or financing activities.

Operating activities include items such as cash collected from customers, cash paid to suppliers, and cash paid to employees.

Investing activities include items such as cash received from the sale of investments and cash paid for the purchase of new investments.

Financing activities include items such as cash received from issuing new debt, and cash paid to repay outstanding debt.

Once all major cash inflows and outflows have been accounted for, the net change in cash for the period is calculated; which is the difference between the cash inflows from operating activities and the cash outflows from the operating activities.

The direct method is the most straightforward way to prepare a cash flow statement because it simply lists all of the cash inflows and outflows for the period in question. This information can be gleaned from a company’s accounting records.

Cash Flow Statement Positive and Negative

A cash flow statement could be positive or negative, depending on the difference between the cash inflows and outflows; the difference between the two determines whether a company can operate in the short or long term. A positive cash flow shows the company is solvent and can grow its operations.

Positive cash flows

A positive cash flow simply means there is an inflow of cash than an outflow.

Positive cash flow from operations

Positive cash flow from operating activities simply means the core activities of the business are generating more cash than it is spending. This is good and investors would prefer such companies. However, you should also note that a business can still have a positive cash flow from operations and still not be profitable. Cash flow statements do not report profitability but rather the movement of CASH in and out of the business over a period of time (accounting period).

Positive cash flow from investing activities

A positive investing cash flow means the company is generating cash from investments (gains) or cash is received from the sale of property, plant, or equipment.

Though a positive cash flow from investing activities is good, it is not the main activity of the business and should not be the major source of cash; investors would prefer a company to generate cash through the main activities (operating section of the cash flow statement).

Positive cash flow from financing activities

Positive financing cash flow means cash is generated from the sale of equity (shares), taking loans, or the company may not have paid dividends during the accounting period or does not pay dividends at all.

The reason for a positive cash flow from financing activities will determine whether it is good or bad. For an investor looking for income stocks, a positive cash flow from financing activities arising as a result of a lack of dividends payment shows it is the right company.

Negative cash flow

A negative cash flow means there is more cash being spent than cash being received. It is not a measure of profitability, hence a company can have a negative cash flow during an accounting period and still be profitable.

Negative cash flow from operations

A negative cash flow from operating activities means more cash is spent on the core activities of a business than the cash received from the same activities. It doesn’t mean that the company is not generating sales from its products because the accounts receivable may be high (which shows sales were made but cash has not been received); this is the reason why the indirect method of preparing cash flow statement deducts account receivables and other non-cash items from the net income in other to arrive at the operating cash flow.

Therefore, a negative cash flow from operations could mean:

- more cash is used for paying salaries than cash received from other operational activities

- more cash is used for purchasing inventory than cash received from other operational activities

- sales are made but cash is yet to be received (high accounts receivable)

- low sales but more spending arising from other operating activities.

Negative cash flow from investing activities

A negative cash flow from investing activities of the cash flow statement means the business is spending more on investments or in the acquisition of property, plant, or equipment. This shows the firm is investing in growth. A negative investing cash flow could also mean that there are more losses from investments than gains. It is good that an investor checks for the reason of the negative cash flow.

Negative cash flow from financing activities

A negative financing cash flow means more money is spent on repaying debts, paying dividends, or buying back shares (stock buybacks).

A negative cash flow statement is not always bad because a company may be investing in research and development or may be spending money on growth. It is good to check multiple statements of cash flows to have a better understanding of the overall spending of a company.

It is also important to note that a negative cash flow does not mean the absence of profits.

Statement of cash flows importance

- To the company, the purpose of a statement of cash flow is to track the amount of cash that is coming into the company and the amount of cash leaving the company. That way, decisions can be made for improvement.

- The statement of cash flows is important in identifying any potential red flags that may be indicative of future financial problems.

- Investors can know if a company generates more revenue than its expenses. A company with more cash inflows than outflows would be attractive to investors. This is because a company may generate revenue but may not know how to manage it well (that is, it may have poor financial management). Hence the statement of cash flow shows how the cash is generated and how it is spent, to know if the finances were managed properly.

- Capital expenditures (CapEx), which is the fund used for purchasing, maintaining, and upgrading fixed assets such as property, equipment, land, etc. can be tracked using the cash flow statement.

- The value of the stocks of a company can be determined from the statement of cash flows.

- The cash flow statement shows the amount of money paid out as dividends. A company that is paying dividends would have a negative cash flow from financing.

- Creditors can check the cash flows from financing activities, if it is negative, one reason could be that the company is repaying loans.

- Another purpose of the statement of cash flow to investors is to show the money used for share buybacks. This shows the purchase of treasury stock.

Statement of Cash Flows vs Income Statement

There are a few key differences between a statement of cash flows and an income statement. The statement of cash flows focuses on cash inflows and outflows, while the income statement focuses on net income.

Another difference is that the statement of cash flows includes information on investments and financing activities, while the income statement does not.

The major difference between income statement and statement of cash flow is that the cash flow statement provides insights into a company’s liquidity and solvency, while the income statement provides insights into profitability.

Statement of Cash Flows vs Balance Sheet

The statement of cash flows reports on a company’s inflows and outflows of cash over a given period of time, while the balance sheet reports on a company’s assets, liabilities, and shareholder equity as of a given point in time.

The balance sheet focuses on assets and liabilities, while the cash flow statement focuses on actual cash movement. This means a statement of cash flows shows how cash has moved in and out of a company over a period of time, while a balance sheet shows what a company owns and owes at a specific point in time.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.