A statement of retained earnings is a financial statement that shows how much net income or net profit a company has earned during a certain period of time, usually a quarter or a year; it also shows how much of that net income was kept or retained by the company as opposed to being paid out in dividends.

The purpose of the statement of retained earnings is to show shareholders and investors how profitable the company is and how much money is being reinvested back into the business. It is also used to calculate the company’s earnings per share (EPS).

We’ll take a closer look at what goes on statement of retained earnings, examples, calculations, and the purpose for which it is prepared.

What is the statement of retained earnings?

The statement of retained earnings is also called the statement of changes in equity (SOCE); it is a financial statement that summarizes the changes in a company’s retained earnings over a period of time. Retained earnings are the portion of a company’s profits that are not paid out as dividends, but are instead reinvested back into the business. Other financial statements are the balance sheet (statement of financial position), cash flow statement, and statement of operations (income statement).

The retained earnings statement is known by different other names depending on the nature of the business or entity.

Other names of the statement of retained earnings

- Statement of changes in equity or simply the equity statement.; because it shows the changes in the shareholders’ stake in a business.

- For government agencies, the statement of retained earnings is also called the statement of changes in taxpayers’ equity

- For sole proprietorship, it is also named a statement of changes in owner’s equity.

- Statement of retained earnings is also known as the statement of changes in partners’ equity

- For a corporation, it is also called a statement of changes in shareholders’ equity

Statement of retained earnings explained

The retained earnings statement can be prepared as a separate financial statement or together with the income statement or the balance sheet.

The statement of retained earnings equation can be expressed as Retained earnings (ending balance) = Retained earnings (starting balance) + Net income – Dividends

The starting retained earnings for the current reporting period is the ending retained earnings from the previous reporting period. You can find the ending retained earnings from the equity portion of the balance sheet for the previous accounting period.

For example, when preparing a statement of retained earnings for 2022, the starting balance would be the retained earnings on the balance sheet at the end of 2021.

The net income is obtained from the income statement of the current reporting period; the dividends would be the payout amount that would be distributed to shareholders for the current reporting period.

The retained earnings statement begins with the beginning balance of retained earnings and then lists all of the net income or loss for the period, any dividends that were declared and paid, and then finally the ending balance of retained earnings. The statement of retained earnings is important because it shows how much profit a company is retaining and reinvesting into the business, which can be used to finance future growth.

The statement of retained earnings is a financial statement that provides information on a company’s profits and losses, as well as the shareholders’ equity in the company. The statement can be used to help investors and creditors understand a company’s financial health and performance.

The equity statement can be an important tool for investors when making decisions about whether or not to invest in a company. It can also be helpful for creditors when considering whether or not to extend credit to a company.

Related: Income Statement Ratios

What does the statement of retained earnings show?

The statement of retained earnings shows the changes in the equity of a company over a period of time; it also shows the dividends paid and the money remaining after the dividends are paid (retained earnings). This information is important to investors and creditors because it provides insight into how well a company is retaining its earnings and whether or not it is reinvesting those earnings back into the business. The statement can also be used to determine the dividend payout ratios and trends.

Statement of Retained Earnings Examples and Samples

Below are samples of the equity statements of some companies.

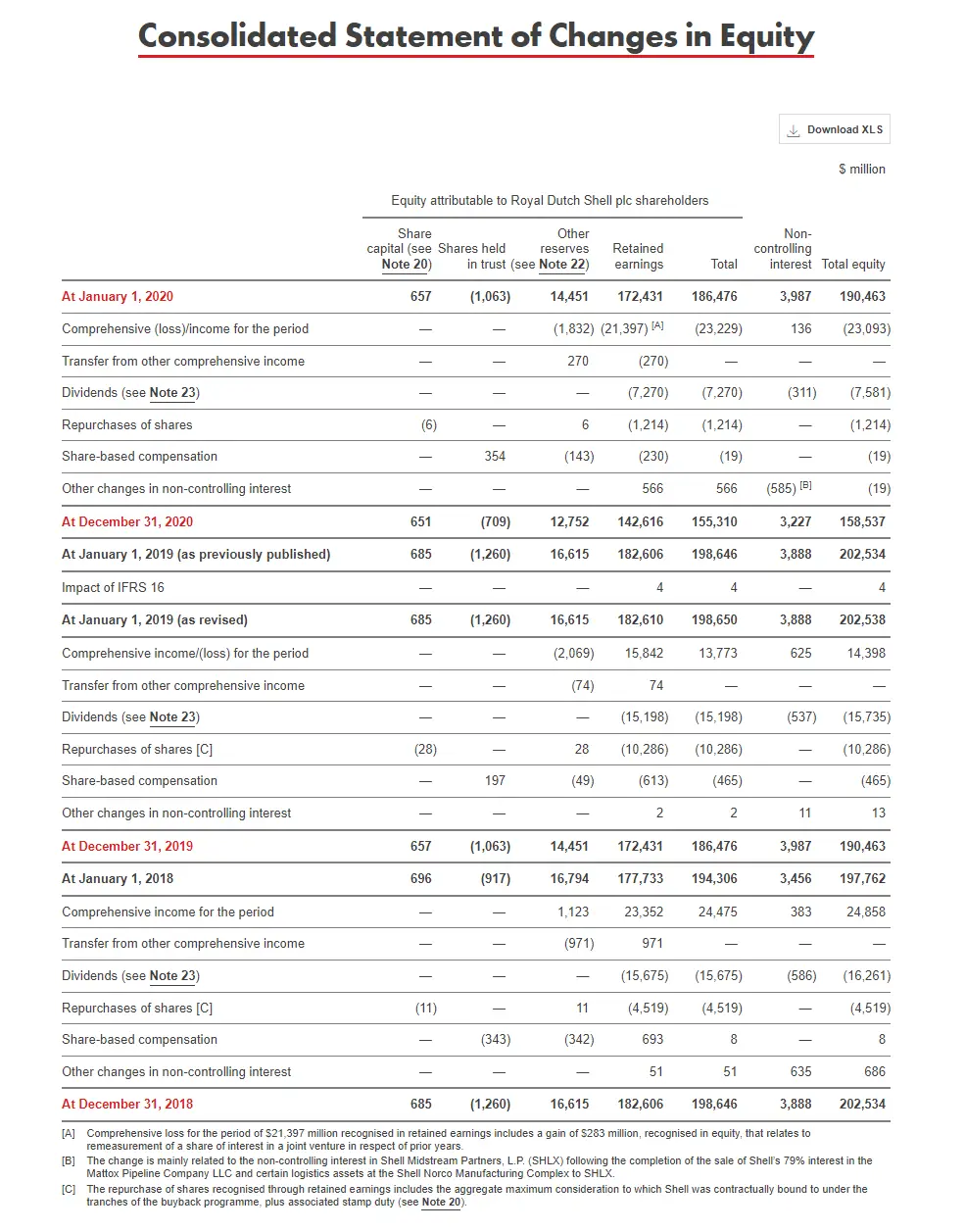

Shell 2019 and 2022 Consolidated Statement of Changes in Equity

You can download the Shell Statement of Changes in Equity here (Excel format)

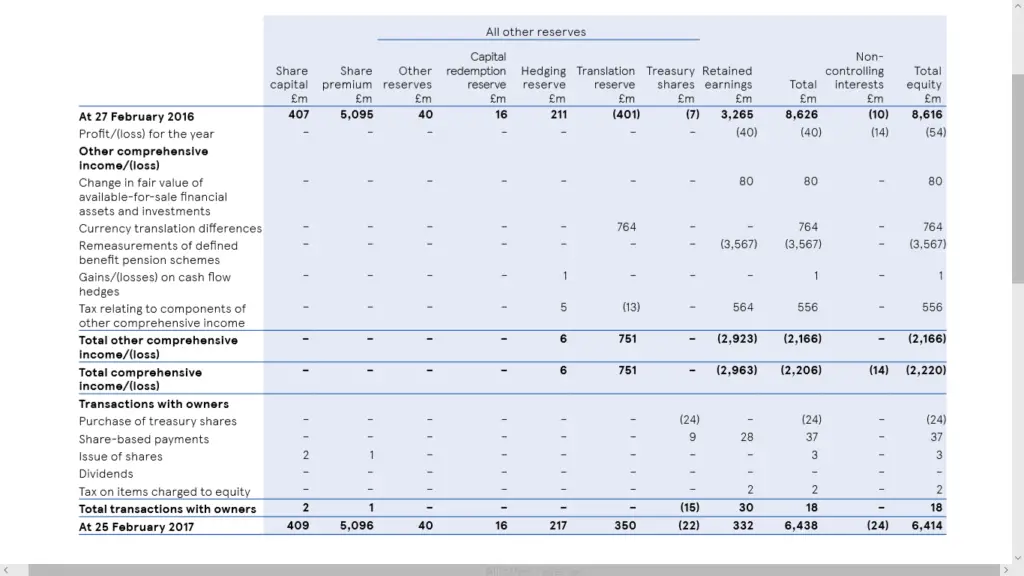

Tesco 2016 Statement of Changes in Equity Example

Source: Tesco (PDF)

Statement of Retained Earnings Examples and Calculations

In the following examples, we would be given some information from the balance sheet that we are going to use in preparing a statement of equity changes.

Statement of Retained Earnings Example 1

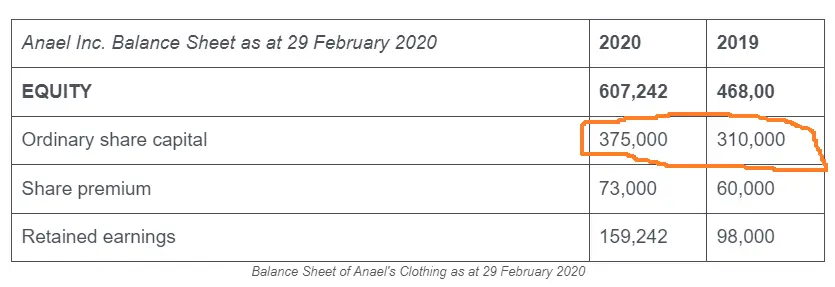

Below is a table showing the 2019 and 2020 Equity section of the Balance sheet of Anael Inc. as at 29 February 2020. Prepare a statement of changes in equity for the company for the year ended 29 February 2020; assume the profit for the year is $81,242 and ordinary dividends declared was $20,000.

| Anael Inc. Balance Sheet as at 29 February 2020 | 2020 | 2019 |

| EQUITY | 607,242 | 468,00 |

| Ordinary share capital | 375,000 | 310,000 |

| Share premium | 73,000 | 60,000 |

| Retained earnings | 159,242 | 98,000 |

From the information given, the current fiscal year ended 29 February 2020. That means it started 1st of March 2019.

The ending balances at 29 February 2019 (in the equity section of the balance sheet) become our balances at the beginning of the current reporting period (in our equity statement), 01 March 2019.

Before we can prepare the statement of changes in equity, we need to calculate the balances for the items that were not given in the question. After that, we will create the statement.

Calculation for the balances in the statement of equity

The profit for the year is given in the question, which is $81,242. If there was a loss for the year, the balance of the profit for the year would be negative. This would be reported under the retained earnings column in the statement of changes in equity.

Profits increase the retained earnings balance while losses decrease the retained earnings balance. Dividends paid also decrease the retained earnings balance.

Since we are given the dividends declared, this would be recorded under the retained earnings because dividends reduce the balance of the retained earnings. Therefore, the dividends declared would be – $20,000; we would add the dividends in brackets to show that it is negative or that it is reducing the retained earnings. Dividends are negative because paying dividends takes money out of the account of a company.

Ending balance for retained earnings would be = retained earnings balance at beginning + profit for the year – dividends paid – losses during the reporting period = 98,000 + 81,242 – 20,000 = $159,242.

How to calculate the shares issued

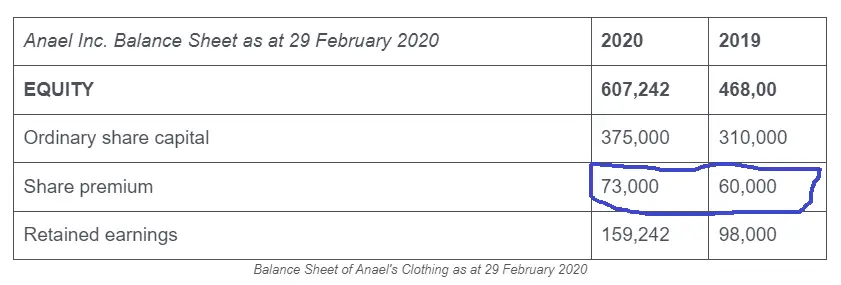

From the question, we were not given the shares issued during the current reporting period. But you can notice that the ordinary share capital increased from $310,000 to $375,000.

The ordinary shares for the reporting period will be 375,00 – 310,00 = 65,000

Therefore, the ordinary shares = $65,000

Ending balance for ordinary shares would be = ordinary shares balance at beginning + ordinary shares during the reporting period = 310,000 + 65,000 = $375,000

How to calculate the share premium

The share premium was not given in the question, so if it is available in the statement of financial position (balance sheet) we will calculate it.

The share premium moved from $60,000 to $73,000 during the current reporting period. The difference would be our share premium for our current reporting period.

Therefore, the share premium as at 29 February 2020 would be 73,000 – 60,000 = $13,000; in the statement of retained earnings, the share premium is added to the row of the shares issued because a premium is charged on shares that are issued.

Ending balance for share premium would be = share premium balance at beginning + share premium during the reporting period = 60,000 + 13,000 = $73,000

We were not given shares repurchased from the balance sheet nor in the question; the shares repurchased would still appear in our equity statement but will have an empty balance.

When you sum up all the balances at the end of the reporting period of the statement of retained earnings, it gives the total equity at the end of the accounting period. In this statement of retained earnings example, the total equity at the end of the reporting period is $607,242. This way, the statement of retained earnings shows the changes that occurred in the equity of a company during a reporting period, hence it is also called the statement of changes in equity or the equity statement.

The total equity at the end of the reporting period should be the same amount of equity reported in the balance sheet (statement of operations) for the same accounting period.

In this example on a statement of retained earnings, we were asked to prepare the financial statement as well. This can be shown below.

Since we have all the balances we need for preparing a statement of changes in equity, it will look like this.

| Anael Inc. | ||||

| Statement of changes in equity for the year ended 29 February 2020 | ||||

| ORDINARY SHARES | SHARE PREMIUM | RETAINED EARNINGS | TOTAL | |

| Balance as at 01 of March 2019 | 310,000 | 60,000 | 98,000 | 468,000 |

| Profit for the year | 81,242 | 81,242 | ||

| Shares issued | 65,000 | 13,000 | 78,000 | |

| Shares repurchased | - | |||

| Dividends declared | (20,000) | 20,000 | ||

| Balance as at 29 February 2020 | 375,000 | 73,000 | 159,242 | 607,242 |

This statement of retained earnings example shows its relationship or connection with the balance sheet.

Statement of Retained Earnings Example 2

The following is the equity section of the statement of operations of JOnyx Group Ltd. at 01 March 2021. The profit for the year is $137,000.

| EQUITY | |

| Ordinary shares at $2.50 per share | $450,000 |

| Share premium | $75,000 |

| Retained earnings | $144,000 |

Assuming additional 20,000 shares were issued for $60,000 on 31 July 2021 and ordinary dividends declared was $0.35 per share on all shares held at 28 February 2022.

Also, the Property, Plant, & Equipment (PP&E) of the company were revalued and resulted in a surplus of $45,000.

Prepare the statement of changes in equity for the year ended 28 February 2022.

Calculating the balances

It is important to take note of the dates given in the question. The fiscal year ends 28 February 2022.

The revaluation reserve was not given for the beginning of the accounting period, we will have a zero balance recorded here. We were however given at the end of the accounting period, which was $45,000.

The profit for the year is given as $137,000 (from the question).

Calculating the shares issued

From the question, additional 20,000 shares were issued for $60,000 during the accounting period. We don’t know the price per share, so we have to calculate it.

Price per share = share capital/number of shares issued

Therefore the price per share for the additional shares issued = 60,000/20,000 = $3

This means the Company issued the shares at a higher value than the par value of $2.50.

The par value of ordinary shares is the face value of the shares as decided by the company in its articles of incorporation (corporate charter). Companies may assign par value to their shares to give confidence to investors that the shares cannot be issued at a later time to other investors below the par value.

Since the price per share is higher than the par value, to get the value of the issued ordinary shares at par value, we will multiply the number of shares by the par value.

This means, the value of issued ordinary shares = 2.50 x 20,000 = $50,000

Related: Stock Valuation

Calculating the share premium

The share premium is also known as Capital surplus, and it represents the excess money a company receives for issued shares above the par value.

The share premium formula is = (issued share price – par value) x the number of shares issued

In this example, the company issued the shares at $3 (as we calculated).

The share price in excess of par would be 3 – 2.5 = $0.5

Therefore, the share premium = 0.5 x 20,000 = $10,000

Calculating the dividends declared

Like I earlier said, always take note of the dates and also take note of the type of shares that is receiving the dividends. In this example, the ordinary dividends were declared on all shares that are held at 28 February 2022 at $0.35 per share. This means we must calculate the total number of shares issued from the beginning of the accounting period and also add the additional shares issued during the accounting period.

To calculate the shares issued at par value at the beginning of the accounting period as given in the table, we need to divide the value of issued shares by the par value.

Number of shares issued at par value = issued share capital/par value of issue shares

= 450,000/2.5 = 180,000 shares were issued at par value of $2.5

Therefore, the total shares issued that were held as at 28 February 2022 would be = 180,000 (issued at par value at the beginning) + 20,000 (additional shares issued during the accounting period) = 200,000 shares issued in total.

We now know the total number of shares issued = 200,000

Since $0.35 is paid as the ordinary dividend per share held; the total dividends paid out would be 0.35 x 200,000 = $70,000

Therefore, $70,000 was used for paying dividends. This will reduce the retained earnings and so would appear under the retained earnings column as explained in example 1 above.

The shares repurchased were not given in the example so we will still include it in the statement of retained earnings as an item but with an empty balance.

We can now prepare the statement of changes in equity for the company in this example as shown below.

| JOnyx Group Ltd. | |||||

| Statement of changes in equity for the year ended 28 February 2022 | |||||

| ORDINARY SHARES | SHARE PREMIUM | RETAINED EARNINGS | REVALUATION RESERVE | TOTAL | |

| Balance as at 01 of March 2021 | 450,000 | 75,000 | 144,000 | 0 | 669,000 |

| Profit for the year | 137,000 | 137,000 | |||

| Revaluation surplus | 45,000 | 45,000 | |||

| Shares issued | 50,000 | 10,000 | 60,000 | ||

| Shares repurchased | - | ||||

| Dividends declared | (70,000) | 70,000 | |||

| Balance as at 28 February 2022 | 500,000 | 85,000 | 211,000 | 45,000 | 841,000 |

From this example of a statement of retained earnings, we can see that the equity of the business changed from $669,000 at the beginning of the fiscal year 01 March 2021 to $841,000 at the end of the fiscal year 28 February 2022.

Related: Retained Earnings, Debit or Credit?

Is the statement of retained earnings the same as shareholders’ equity?

The statement of retained earnings is not the same as shareholders’ equity as they are two different things. Shareholders’ equity refers to the portion of a company that belongs to shareholders based on the stocks they own in the company (equity stocks); the shareholders’ equity is a complete section on the balance sheet under which the number of common stocks owned by shareholders is stated. On the other hand, the statement of retained earnings is a financial document that shows how much money a company reinvests into growth after dividend payments; it also shows the changes occurring in the equity, hence, it is also known as the statement of changes in equity (or the equity statement).

The equity of a company can be divided into two parts: common stock and retained earnings. Common stock is the portion of the equity that belongs to the shareholders, while retained earnings is the portion that belongs to the company. The statement of retained earnings shows how these two parts have changed over time, hence the name “the statement of changes in equity or equity statement“.

The statement of retained earnings can be used to track the progress of a company over time. It can also be used to help assess whether a company is using its profits wisely or if it is distributing too much money to shareholders through dividends.

What information does the statement of retained earnings provide?

- It shows the retained earnings starting balance (gotten from the previous statement)

- Net income

- Share premium

- Shares repurchased

- Dividends paid out to shareholders

- Retained earnings ending balance

A simple retained earnings statement would provide just the retained earnings: beginning and ending balances together with the net income and dividends paid during the reporting period. In an extended statement of equity changes for a corporation, additional information is provided such as the par value of common stock, total shareholders’ equity, treasury stock, and additional paid-in capital.

Statement of retained earnings purpose

The statement of retained earnings is a financial statement that shows how much of a company’s net income has been retained by the company during a certain period of time; this is very important to investors and lenders as it gives an idea of what a company does with its money when the dividends have been paid. For creditors, does the company still have some money left when it repays its debt? If there is no money left after dividends have been paid, then how is the company going to pay its debt? Therefore, the equity statement is very important to lenders.

Another purpose of the retained earnings statement is that it shows the trend of how a company invests in growth and development by outlining what a company does with its profits.

Negative retained earnings statement

A negative retained earnings means a company has incurred losses in previous accounting periods and has been carried over to the current accounting period. It, therefore, shows the company has nothing left to reinvest into the business. Investors that are interested in growth and not dividends may not be interested in companies with negative retained earnings. Lenders prefer giving loans to companies with positive retained earnings.

Any firm that does not keep part of the net income as retained earnings means that it has to finance growth through debt or by issuing new shares (which further dilutes the equity).

How is the retained earnings statement connected to other financial statements?

The four basic financial statements: balance sheet, income statement, cash flow statement, and retained earnings statement are connected using the retained earnings formula.

The Retained Earnings Formula or equation is expressed as Ending Retained Earnings = Beginning Retained Earnings − Dividends Paid + Net Income

The beginning retained earnings is derived from the balance sheet of the previous accounting period while the Net income is derived from the income statement.

The retained earnings equation is important in calculating the Profit Before Tax to be used in the indirect method of preparing a statement of cash flows.

Statement of retained earnings vs Statement of Cash flows

The statement of retained earnings is a financial statement that summarizes the changes in a company’s retained earnings over a period of time. The statement of cash flows, on the other hand, is a financial statement that provides information about a company’s cash inflows and outflows over a period of time.

The retained earnings statement shows how much of a company’s profits are reinvested back into the business, and how much is paid out to shareholders as dividends. It also includes information on any changes in equity that result from things like stock splits or the issuance of new shares.

The statement of cash flows includes information on where a company’s money is coming from (revenue) and going (expenses). This information can be helpful in assessing a company’s short-term liquidity and its ability to meet its obligations.

Statement of retained earnings vs Balance sheet

The balance sheet shows the assets, liabilities, and equity of a company. It shows the financial position of a business at a particular point in time.

The statement of retained earnings begins with the beginning balance of retained earnings and then subtracts any dividends that were paid out during the period. It then adds or subtracts any net income or loss for the period. Finally, it adjusts for any other items that affected retained earnings during the period.

The balance sheet only shows the ending balance of retained earnings. It does not show any changes during the period.

Does common stock go on the statement of retained earnings

The common stock goes on the balance sheet and not on a retained earnings statement. The common stock can be found under the equity section of the balance sheet.

Statement of retained earnings vs Income statement

The statement of retained earnings reconciles the beginning-of-period balance of retained earnings to the end-of-period balance. The net income or loss for the period is used to calculate the change in retained earnings. Dividends paid during the period are deducted from net income to arrive at the change in retained earnings.

The income statement reports revenues and expenses for a specific period of time, typically a fiscal quarter or year. The bottom line on the income statement is net income, which is calculated by subtracting total expenses from total revenue.

The net income of the income statement is used in calculating the ending retained earnings balance in an equity statement.

Are dividends reported on the statement of retained earnings?

Yes, dividends are directly reported on the retained earnings statements.

Statement of retained earnings GAAP vs IFRS

The statement of retained earnings is one of the most important financial statements for a company. It shows the amount of money that a company has available to reinvest in its business, pay its debt, or pay out dividends to shareholders. The statement can be prepared using either Generally Accepted Accounting Principles (GAAP) standards or International Financial Reporting Standards (IFRS).

There are key differences between the two accounting standards (GAAP vs IFRS) that impact the statement of retained earnings.

In GAAP, the statement of retained earnings can be attached to the income statement, or the balance sheet, or be prepared as a separate financial statement.

Whereas IFRS requires all business entities to prepare the statement of changes in equity to be a separate financial statement (this means, it should not be prepared combined with the balance sheet or the income statement) – IAS 1.

Also, IFRS (IAS1.107) allows for the amount of dividends recognized as distributions as well as the related amount per share to be reported under the notes and not necessarily in the statement of changes in equity.

IFRS requires that the statement of changes in equity shows:

– total comprehensive income for the period, showing separately amounts attributable to owners of the parent and to non-controlling interests.

– the effects of any retrospective application of accounting policies or restatements made in accordance with IAS 8, separately for each component of other comprehensive income

– reconciliations between the carrying amounts at the beginning and the end of the period for each component of equity, separately disclosing: profit or loss, other comprehensive income, and transactions with owners, showing separately contributions by and distributions to owners and changes in ownership interests in subsidiaries that do not result in a loss of control.

https://www.iasplus.com/en/standards/ias/ias1

Conclusion

We have seen some statement of retained earnings examples, calculations, and format. It is a type of financial statement that is important to assess how a company utilizes its retained earnings.

What is the purpose of the retained earnings statement?

The purpose of a statement of retained earnings is used to show how much of a company’s net income has been retained by the company during a specific period of time. This information is important for shareholders and investors to know because it can help them make informed decisions about whether or not to invest in the company.

To the company, the purpose of a statement of retained earnings is to help the management to make decisions about how to allocate the company’s resources towards growth and development, payment of dividends, or repaying debt.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.