Stock options and RSU are forms of employee equity compensation that employers give to employees. They are generally the most common forms of equity compensation. Despite their similarities, stock options vs RSU differ in terms of how they are taxed, their vesting, and the form of compensation that the employee receives. Hence, they are entirely different even though they have certain similarities.

When an employee takes a new job, his/her salary may not be their only form of compensation. They are likely to also get benefits, and possibly some form of stock in the company. This will likely come in employee stock options or restricted stock units (RSUs). Each of these two compensations has its own pros and cons, so one will want to make sure they know which they are getting so they can adjust their financial plans accordingly. Hence, knowing the difference between RSU and stock options will help navigate whichever form of compensation the employee gets with their long-term financial plans.

In this article, we will discuss stock options vs RSU differences and similarities. But first, let’s have an understanding of what stock options and RSU are and how they work.

Related: Stock options vs equity differences and similarities

What are stock options?

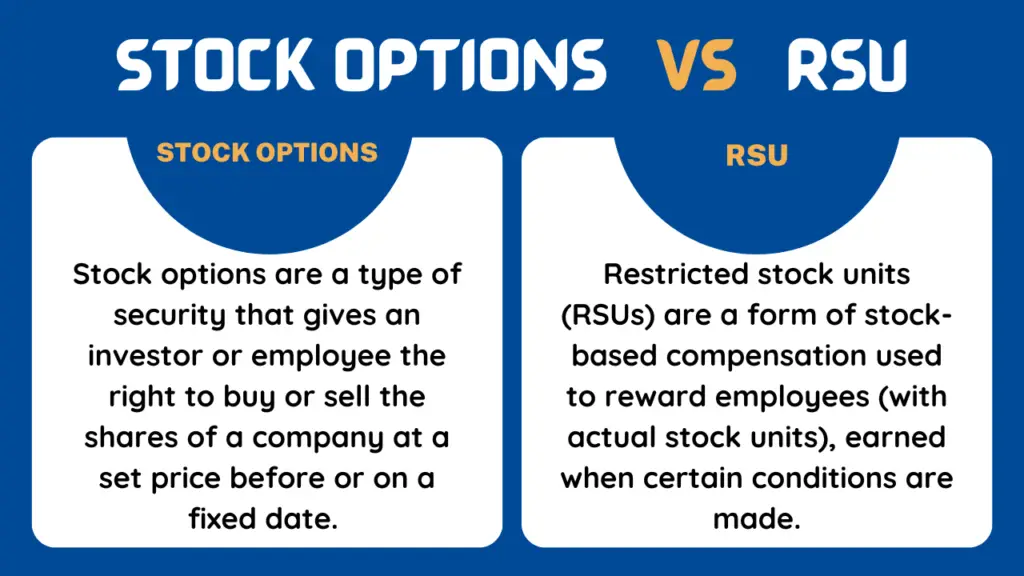

Stock options are a type of security that gives an investor or employee the right to buy or sell the shares of a company at a set price before or on a fixed date. The predetermined price of the stock is known as the grant price, strike price, or exercise price; and the fixed date of the stock option is known as the maturity or expiration date.

There are two main types of stock options, which are the stock options for employees called the employee stock options (ESO) and the standard exchange-traded stock option. The employee stock options are usually compared with the restricted stock units because they are both issued to employees as compensation.

Stock options are likely the most well-known form of equity compensation. It gives the holder the right to buy a certain number of the company’s shares at a pre-set price for a fixed period of time. The process of the option holder buying the shares at the price and time specified by the stock option is known as exercising the stock options which can be done before the expiration date (early exercise) or on the expiration date.

Before an employee can exercise, there is usually a predetermined waiting period, known as the vesting period that the employee has to wait to earn the options fully. This vesting period can span from three to five years, with a certain percentage of the options vesting each year.

How stock options work

With a stock option, you can purchase equity in a company at a determined price within a certain period of time. One stock option contract generally represents 100 shares of the company that the holder is buying into. It is a chance to buy shares of the company if interested. Therefore, an employee or investor can choose not to exercise their stock option as they are not under any obligation to do so.

An employee that is awarded stock options gets the opportunity to buy stock in the company as part of their compensation. This usually involves a vesting schedule, where they have to work at the company for a certain period of time before they can purchase the stock (at least one year). For example, an employee may be able to exercise 250 shares per year for a total of 1,000 shares, over 4 years vesting period. The stock options vesting period is usually set to prevent people who only work at the company for a short period of time from ending up with potentially valuable stock.

One of the major benefits of stock options is that the employee gets to buy the shares of the company stock at a specified price that may eventually be much lesser than what the stock is actually worth on the market when the option eventually vests. Employees are offered two kinds of ESOs, incentive stock options (ISOs) and non-qualified stock options (NQSO or NSO).

For ISOs, the tax treatment may be better because employees may receive favorable tax treatment if they wait for two years from the grant date of the option and one year from the date of exercise to sell their shares. Once these requirements are met, any profit generated from the sale of the shares will be taxed as long-term capital gains.

NSOs, on the other hand, are taxed upon exercise at a regular income tax rate, and depending on how soon they are sold after exercise, the profits on the sale may be taxed as ordinary income or as a combination of capital gains and ordinary income. The NSO does not qualify for the special tax treatment accorded to ISOs. Nevertheless, employers prefer NSOs because they are allowed to take a tax deduction that is equal to the amount the recipient is required to include in his or her income.

Related: ISO vs NSO Differences and similarities

What is RSU?

Restricted stock units (RSUs) are a form of stock-based compensation used to reward employees. They are a type of restricted stock (also known as letter stock or restricted securities). Restricted stocks are bonuses awarded as stock instead of cash; though they are taxed as if it was paid in cash. They are common alternatives to stock options, especially for executives, because of their favorable accounting rules and income tax treatment.

Restricted stock awards (RSAs) and restricted stock units (RSUs) are the two basic types of restricted stock. RSUs came into vogue in the 90s and early 2000s and are a bit simpler than stock options. With restricted stock units, there is no transaction or stock pricing involved. Rather, the company simply commits to giving an employee stock in the company on the condition that certain requirements will have to be fulfilled by the employee.

Hence, RSUs are company stock that cannot be fully transferable until certain restrictions have been met. These restrictions could be performance or time based, similar to the restrictions for stock options. This means that restricted stock units can only be awarded to an employee for meeting performance requirements or for being at the company for a set period of time.

How restricted stock units work

RSUs can be awarded on regular vesting schedules or performance benchmarks. They usually vest over several years just like with stock options. It is typical for an employee to not receive anything until they have been in service at the company for a full year. The vesting schedules have been structured by many companies in a way that after 1 year, the RSUs vest 1/4 or 1/5 of the total amount of RSUs granted, and then more RSUs are granted each month as the employee keeps working for the company.

RSUs are issued in the form of units and not stock which corresponds in number and value to a specified number of employer stock shares. Once the employee meets the requirements, the company gives the RSUs either in actual shares or the cash equivalent depending on what the stock is actually worth at that time.

The company may dictate whether to give the employee actual stock or the cash equivalent; or, it may be left for the employee to decide which to take. Upon vesting the employee gets their equivalent shares and the value of the restricted stock units on the day of vesting is subject to payroll and ordinary income taxation.

See also: Repricing stock options

Stock options vs RSU example

We will be looking at stock options vs RSU examples to understand the differences in how they work.

An example of how stock options works

Let’s look at an example of how stock options work. In this example, we will be using employee stock options to illustrate how stock options work.

Assume you are hired at a new startup on Jan 1, 2017, and the company offers you employee stock options as part of your compensation package. In order, to keep you working in the company, the stock option comes with a time vesting schedule for the options to vest monthly for 4 years with a 1-year cliff. This means you have to continue working with the company for one year to be able to earn any shares at all and after one year the remaining shares vest monthly at 1/36. Therefore, if you leave before this, you will have unvested shares.

Say, you were awarded a stock option of 100 shares of the company’s stock in 2017, with a strike price of $10 per share when the stock was trading at $3.5 per share. The employee stock option grant has an expiration date of Dec. 31, 2021.

Supposing towards the end of 2021, the stock was trading at $20 per share. This is a good time for you to exercise your stock options. At this point, it is said that the options are in the money. A stock option is said to be ‘in the money’ when the fair market value of the stock is greater than the strike price of the option. That is, the strike price is below the stock price at the time of exercise which is an opportunity for you to make a profit.

Your profit would be the difference between the $2,000 (i.e the shares’ value at the time of exercise) and the $1,000 exercise price (i.e the 100 shares multiplied by the $10 strike price). After exercising, you can choose to either sell the shares and pocket the $1000 profit or hold on to the shares in the hope that the share price would go higher.

Nevertheless, it is important to note that not all stock option grants yield a profit. For instance, if you received 100 shares of the company’s stock with a strike price of $10 per share but the price per share of the stock stayed between $6 to $8 during your exercise window, then the stock options are said to be out of the money. A stock option is said to be ‘out of the money’ or ‘underwater’ when the market value of the stock is less than the strike price. In such an instance, you will be better off letting the stock option expire as it is obvious, that you won’t make a profit.

An example of how RSU works

Let’s look at an example of how restricted stock units work.

Assume, you receive a job offer and because the company thinks your skill set is valuable and wants you to remain a long-term employee, your employer offers you 1,000 RSUs in addition to a salary and other benefits.

Suppose, the company’s stock is worth $10 per share. This makes the RSUs potentially worth $10,000. In order to give you an incentive to stay with the company and receive the 1,000 shares, the company puts the RSUs on a five-year vesting schedule.

This means you receive 200 shares after one year with the company, then another 200 shares after the second year, and so on until you earn all 1,000 shares at the end of your vesting period. You may be awarded the actual shares or the cash equivalent depending on what the company or you decided. Moreso, depending on the performance of the company’s stock, you may receive more or less than the initial potential worth of $10,000 RSUs.

Related: Warrants vs stock options differences

Stock options vs RSU differences

Stock options and RSUs are two types of equity compensation that are offered to employees by the company. They are offered so that the companies can hold on to remarkable employees. In as much as they are both equity compensation, they are quite different. The scope of stock options vs restricted stock is diverse too. This is why understanding stock options and RSUs separately is essential and allows us to know which of these equity compensations align with our long-term financial plans.

Difference between RSU and stock options

- Stock options are a type of security that gives the employee or investor the right to purchase the company stock at a specific price which is granted on a set vesting schedule. RSUs, on the other hand, are a type of restricted stock that is granted to special employees based on a set vesting schedule or after they reach certain performance benchmarks.

- The main difference between restricted stock units vs stock options is what the employee receives. In the case of stock options, the employee has the option to purchase the company’s shares at a specific price before a certain date. It’s up to the employee to buy the shares or not. But for RSUs, the employees are granted the actual shares once the vesting period is complete. They don’t have to purchase the shares themselves.

- Another key difference between RSU and stock options is the shareholders’ rights. The employees that hold stock options receive the full right of the shareholders whereas, in the case of restricted stock units, the employee doesn’t receive the full right.

- One of the differences between stock options vs RSU is that stock option offers both voting rights and dividend rights to the employee while voting rights and dividends are not given to the employee in the case of restricted stock units.

- In the case of stock options, the payment during settlement is always stock whereas, the payment during settlement in the case of RSUs can be cash or stock.

Other essential differences between stock options vs RSUs include their exercise price, vesting, terms, payment, value, and taxation which are explained in the table below.

| Criteria for Comparison | Stock options | RSUs |

|---|---|---|

| Definition | Stock options are a type of security that gives the employee or investor the right to purchase the company stock at a specific price which is granted on a set vesting schedule | RSUs are a type of restricted stock that is granted to special employees based on a set vesting schedule or after a certain performance benchmark is reached |

| Exercise Price | The exercise price is set based on the fair market value of the underlying security | There is no exercise price |

| Terms | With stock options, the employee is given the choice to either buy or sell the underlying stock at the exercise price or leave the option to expire. | In order for the RSUs to become common stock, the employee only has to fulfill the terms of the vesting schedule or plan |

| Vesting | These are usually awarded on a set vesting schedule. Vesting could be time-based, milestone base or a combination of both | This can be awarded on a set vesting schedule or performance benchmarks. Hence, it can vest anytime for any milestone |

| Dividends paid | Yes | No |

| Payment during settlement | Stock | Cash or stock |

| Taxation | Stock options are taxed when exercised or sold depending on the type of employee stock options. ISOs are not taxed when exercised and are taxed as long-term capital gains if stock is held for at least 2 years after option grant and 1 year after exercise. While NQSOs are taxed as ordinary income when exercised and taxed as long-term capital gains when held for at least 1 year. | RSUs are taxed when vested. They are treated as regular income and as capital gains if the awarded shares are held for more than a year |

| How it works | They are usually offered to employees who perform exceedingly well and the underlying security is given at a discount rate that is less than its current price at that time so that the stock option can be considered a reward. | They are offered to keep exceptional employees in the company and are paid per a vesting schedule. RSUs don’t offer all the shares together. |

| Companies likely to issue them | The use of stock options is common with early or mid-stage start-ups | The use of RSUs is common with late-stage start-ups and public companies |

| Shareholder’s right | There’s a full right of the shareholders offered | There’s a restricted right of the shareholders offered |

| Voting right | There’s a voting right given | There’s no voting right given |

| Value | As the company’s valuation goes up, the value of the stock options will go up, but if the company’s valuation depreciates or stays the same, the stock options value drops | RSUs will retain some value regardless of how well the company performs in the future. If the company’s valuation depreciates, the value of RSUs may not end up being all that much, but will still have some value. |

| Expiration | It is common for employee stock options to have a maximum maturity/expiry of 10 years from the date of issuance. The stock option contract comes with an expiration date which is usually identified as a month. A specific date which is the third Friday of the expiration month is usually identified as the exact deadline. | RSUs do not have an expiration date. Once, they are vested, they are converted to shares and do not expire. |

See also: Examples and types of equity options

Similarities

- Stock options and RSUs are types of equity compensation.

- They are both offered to employees.

- Stock options and RSUs have vesting schedules.

- The shares of the company could be the payment for the settlement of stock options and RSUs.

- There are tax implications for both RSUs and stock options.

Employee stock options vs RSU tax implications

The tax implication for restricted stock units vs stock options differs. Stock options vs RSU tax implications are an important factor to consider. For stock options, there are no tax implications when the company grants them. You only worry about paying taxes on stock options when you exercise them or sell the stocks depending on the type of stock option- incentive stock option or nonqualified stock options.

Incentive stock options are not taxed when exercised. The sale of ISO stocks is taxed as long-term capital gains if stock is held for at least 2 years after option grant and 1 year after exercise. Non-qualified stock options, on the other hand, are taxed as ordinary income when exercised and taxed as long-term capital gains when held for at least 1 year.

The tax implications for RSUs are different from stock options. The tax for incentive stock options vs RSU or non qualified stock options vs RSU differs in the sense that RSUs are taxed when vested. Meanwhile, ISOs and NQSOs are not taxed when vested only when exercised or when the stock is sold.

An employee pays taxes on his/her RSUs upon vesting. In several cases, the employer may withhold some of the employee’s RSUs to cover the tax burden. Whereas, in other cases, the employee may be given the option to pay the taxes in cash in order to receive the full amount of their vested RSUs.

Restricted stock units are taxed as ordinary income, that is the rate that the employee may pay can range from 10% to 37%, depending on his/her household income. RSUs are also subject to withholding for social security taxes and medicare taxes. This will result in another 7.65% in tax liability. Moreso, depending on where the employee lives, their RSUs may be subject to state income taxation.

Related: ISO vs NSO; which is better?

Stock options vs RSU which is better?

There are benefits and disadvantages to both stock options and RSUs. Therefore, deciding which one is better will depend on an individual’s circumstances and other factors, like taxation and value.

RSU vs stock options tax advantage

Taxation is an important factor to consider when comparing stock options vs RSU to know which is better. As soon RSUs become vested and liquid, they are taxed at ordinary income tax rates. Employers usually withhold some of the RSU to pay taxes, though you may be given the option to pay taxes with cash on hand so that you can retain all of your vested RSUs.

Stock options, on the other hand, aren’t taxed until they are exercised. The advantage to stock options is that if you hold onto them for at least one year, they will be taxed at more favorable capital gains tax rates. Moreso, stock options aren’t usually exercised until after a company goes public. So, the employee can sell enough shares to cover the tax owed on the appreciation of the options.

Value of RSU vs Stock options

Value is another important thing to consider when comparing stock options vs RSU to know which is better. Stock options only have value if the market price of the underlying stock goes up in the future. Therefore, if the stock price doesn’t rise, you would be paying more for the shares than you could sell them for.

The value of RSUs, compared to stock options, isn’t contingent on the stock price rising in the future. They are simply awarded to you by the company after you’ve worked with the company for a certain period of time or when certain performance requirements are fulfilled. Therefore, compared to stock options, RSUs are relatively safe due to the fact that their value doesn’t depend on stock price appreciation. This is basically one of the reasons why RSUs tend to be less common than stock options. The bottom line is that RSUs are pure gain because you don’t have to pay for them.

However, if you are given the choice to choose, you should weigh the potential benefit of price appreciation that could render stock options extremely valuable in the future against the risk of the stock price not appreciating at all and the options being worthless. Then compare that to the relative safety of RSUs.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.