The stock valuation formula varies across the methods of valuation which may fall under absolute valuation or relative valuation. These formulas and methods are explained in the article with examples.

What is stock valuation?

Stock valuation is the process of calculating the values of companies and their stocks. In other words, it is the method of determining a stock’s intrinsic or theoretical value. It is necessary for every investor who wants to beat the market to master the skill of stock valuation.

The importance of valuing stocks evolves from the fact that a stock’s intrinsic value, is not attached to its current price. In other words, the intrinsic value of stocks measured on the basis of business fundamentals may or may not match the current price which is a result of market forces, that is the demand and supply factors. By having knowledge of a stock’s intrinsic value, an investor may determine whether the stock is undervalued or overvalued at its current market price.

The act of applying stock valuation helps in determining the fair price of a share. Because active investors believe that the intrinsic value of a stock is separate from its current price, they apply a series of metrics in order to compute its real value and compare it against its market price.

Another set of investors known as passive investors, however, base their argument on the efficient market hypothesis which implies that market price is on the basis of all available information, hence being the actual value of the stock. The theory of passive investment recommends investment in index funds or exchange-traded funds (ETFs) that reflect market returns rather than calculating a different stock value to outsmart the market.

Methods of stock valuation

- Absolute valuation

- Relative valuation

1) Absolute valuation

Absolute valuation of stocks is dependent upon the fundamental information of the company. Generally, this method involves the analysis of various financial information that is available or derived from the financial statements of the company. In essence, this form of valuation attempts to find the true or intrinsic value of an investment and bases only on fundamentals. Many of these techniques primarily carry out the investigation of company cash flows, growth rates, and dividends. The absolute valuation does not compare the performance of the company with peers.

The following fall under the absolute valuation method;

- Dividend discount model (DDM)

- Discounted cash flow method (DCF)

- Residual income model

- Asset-based model.

These methods are discussed below;

Dividend discount model (DDM)

The dividend discount model is one of the absolute stock valuation techniques. This method is based on the assumption that the dividend of a company represents the cash flow of the company to its shareholders. This model essentially states that the intrinsic value of a company’s stock price is equal to the present value of the company’s future dividends. It is important to note that the dividend discount model is only applicable if a company distributes dividends on a regular basis and the distribution is stable. In other words, this method calculates the actual price of stocks based on the dividends paid by the company to its shareholders.

Analysts argue that dividends are a representation of the genuine cash flow of the business going to its shareholders, therefore, calculating the present value of future dividend payments should bring about the correct worth of the stock.

In essence, large corporations that pay dividends to shareholders on a regular basis and at a stable rate are best suitable for this method of stock valuation. This method is one of the most basic of absolute valuations.

Discounted cash flow model (DCF)

Another method of absolute stock valuation is the discounted cash flow model. Under this approach, the calculation of a stock value takes place by discounting the company’s free cash flow to its present value.

One main advantage of the discounted cash flow model is the fact that it requires no assumptions with regard to the distribution of dividends. Therefore, it is suitable for companies that have unknown or unpredictable dividend distribution. However, from a technical perspective, the model tends to be sophisticated.

For a company whose dividend pattern is irregular or does not pay dividends, such a company can go ahead to check if it fits the criteria to make use of the discounted cash flow model.

This model makes use of a firm’s discounted future cash flows to value the business rather than looking at dividends. It has several variations but the most commonly used form is the two-stage discounted cash flow model. Here, the analyst forecasts the free cash flows for five to ten years and then calculates a terminal value to account for every cash flow beyond the forecasted period. The first and basic requirement for a company to use this model is to have free cash flows that are positive and predictable. On the basis of this requirement alone, one will find out that many small high-growth companies and immature firms will not be included as a result of the large capital expenditures they may typically be faced with.

Residual income model

The residual income model is another method of absolute valuation. Though it may not be familiar, it is widely used by analysts. Residual income refers to the income that is generated by a company after taking into account the cost of capital. This model makes use of data readily available from the firm’s financial statements.

The formula for this method of valuation is very similar to a multistage dividend discount model, substituting future payments of dividends for future residual earnings.

A question with regard to whether companies already account for their cost of capital in their interest expense may be going through one’s mind. Well, the answer can be yes and no. On the income statement, the interest expense only takes into account the cost of a firm’s debts. This means that it ignores the cost of equity such as dividend payouts and other costs of equity.

In another way, taking a look at the cost of equity in another way, see it as the opportunity cost of shareholders or the required rate of return. The residual income model makes attempt to adjust the future earnings estimates of firms to compensate for the cost of equity and place a volume that is more accurate on a firm. Even though the return to equity to holders is not a legal requirement like the return to bondholders, it is necessary for firms to compensate them for the investment risk exposure in order to attract investors.

2) Relative valuation

As the name implies, relative valuation has to do with the comparison of the investment with peers or similar companies. It deals with calculating the key financial ratios of similar companies and deriving the same ratio for the target company. The P/E ratio forms the basis of the relative valuation method. For instance, if a company’s P/E ratio is lower than that of a comparable company, we may consider the original company undervalued. The relative valuation model is typically easier and quicker than the absolute valuation.

An example of relative stock valuation is comparable companies analysis also known as the comparables model.

Comparable companies analysis

This valuation method does not determine the intrinsic value of a stock using the fundamentals of the company, it aims at deriving the theoretical price of a stock using the price multiples of similar companies.

The most commonly used metric in the comparable analysis includes price-to-earnings ratio (P/E), price-to-book ratio (P/B), price-to-sales ratio (P/S), and price-to-cash flow (P/CF), and enterprise value-to-EBITDA (EV/EBITDA). As earlier stated, the P/E ratio is the most commonly used as it pays more attention to the earnings of the company which is one of the driving factors of the value of an investment.

The P/E ratio has to do with the valuation of stock price against the earnings per share (EPS) that are most recently reported. Investors make use of it as a gauge to measure the stock value of a company. A higher price-to-earnings ratio implies overvalued shares. On the other hand, a lower price-to-earnings ratio when we compare it against peers, as well as the broader market, implies undervalued shares. Value investors are constantly in search of undervalued shares that have the potential for long-term growth. Analysts review the P/E ratio in order to determine if the price per share is an accurate representation of projected earnings per share.

From a technical perspective, the comparable companies analysis is one of the simplest methods of valuation of stocks. However, the challenging factor here is the determination of the companies that are truly comparable.

Stock valuation formula

The formula for the valuation of stocks varies across the methods which may fall under absolute valuation or relative valuation. Let us look at them individually.

Dividend discount model formula

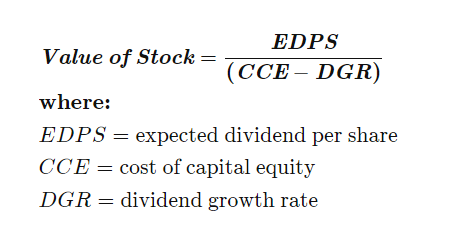

We can calculate the DDM through the Gordon growth model (GGM), which assumes that every future dividend grows at a constant rate. On the basis of the expected dividend per share as well as the net discounting factor, the formula for the valuation of stocks using the DDM is expressed mathematically in the image below;

In using this method, the first step is to determine if the dividend payment is stable and predictable as it is not enough for the company to just pay dividends. Companies that make stable and predictable dividend payments are typically mature and are usually in well-developed industries. It is such companies that are best suited for the DDM valuation model.

Example of stock valuation using the dividend discount model stock valuation formula

For example, if the stock price of a company is listed at $50, it has a required rate of return of 15% and pays $1 as a dividend per share, and then its constant dividend growth rate is 6%. Using the formula above, we would calculate the stock value as follows;

Value of stock = $1/(0.15 – 0.06)

= $1/0.09

= $11.11

We can therefore say that the stock price is overvalued because the Gordon growth model states that the value of the stock will only be $11.11.

The dividend cash flow can as well be calculated by making use of the formula below;

[CF ÷ (1+r)^1] Where;

CF = cash flow

r = interest rate

n = number of periods

For example, if the current cash flow of a company is $10,000 with a growth rate of 3% for one year, we will calculate the dividend cash flow as;

Current dividend cash flow =[10,000 ÷ (1 + 0.05)^1] = $9070.29

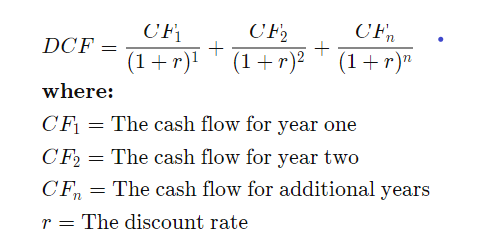

Discounted cash flow model formula

The discounted cash flow formula works by the addition of all cash flows for each reporting period as well as dividing these sums by one plus the discount rate raised to the power of n.

The cash flow represents a company’s current or free cash flow that a company has after subtracting payments on investments, operating expenses, and capital expenditures. The r variable denotes the discount rate which equals the weighted average cost of capital (WACC). The WACC of a company here refers to the average rate it expects to pay its stakeholders to finance its assets. The variable ‘n’ in the formula denotes the period number that the company is reporting. For example, a company may record on a quarterly basis or yearly basis. The variable may connote quarter one, quarter two, or year one, year two, and so on.

Discounted cash flow model stock valuation formula example

For example, a company has some information from its discounted cash flow analysis which include a current investment value of $24,500, free cash flow of $450,000, future projected investment returns of $925,000, and a discount rate of 15%.

If the company is measuring its discounted cash flow over the period of three years, it will make use of the formula above and substitute for n=3, r=0.15, and cash flow = $450,000.

DCF = $450,000/(1+0.15)1 + $450,000/(1+0.15)2 + $450,000/(1+0.15)3

= $450,000/(1.15) + $450,000/(1.32) + $450,000/(1.521)

= $391,304 + $340,265 + $295,882

= $1,027,451

Based on the discounted cash flow method, the result of the stock valuation shows that the company can expect the investment to yield a return that appears to be far above its initial projection which was $925,000. As a result of the high valuation of the future expected cash flow, the company can decide to go ahead with its investment. With this, we can say that the company is embarking on an informed investment decision based on the valuation.

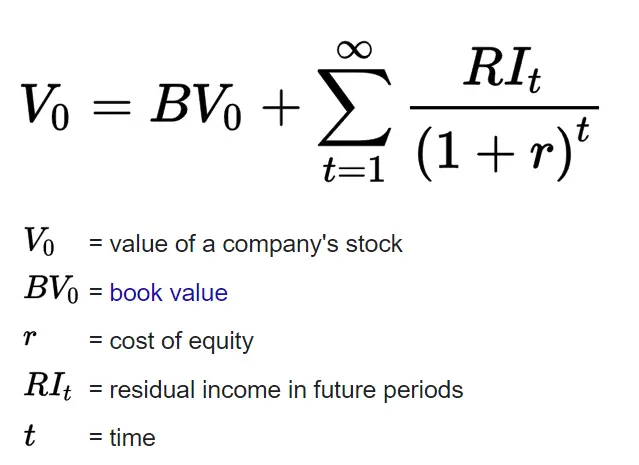

Residual income model stock valuation formula

Before determining the value of stocks using the residual income model, it is important to calculate the residual income which will form the basis of the valuation of stocks. The formula for calculating the firm’s residual income is;

RI = Net income – (Equity x Cost of Equity)

Residual income stock valuation example

An industry that produces different types of food for pets, particularly dogs and cats has been in this business for over three years. Over this period, it has been gaining market share in the different segments it serves. Presently, the company is in need of additional funds to expand its operations and the board of directors has arrived at a decision to issue new shares for those that have an interest in investing in the business.

The major thing now is to determine a fair value for the company in order to issue the new shares. Because the business only has a few years, the discounted cash flow model will not fit in the valuation. Rather, they will have to adopt the residual income valuation method.

The company’s net income as of last year is $3,445,000, its total equity is $16,000,000, the book value is $12,500,000, the cost of equity is 11%, and there are 1,000,000 shares outstanding. Let us look at how the calculations went.

Based on the information above, the residual income for the firm will be;

Residual income = $3,445,000 – ($16,000,000 x 11%)

= $3,445,000 – $1,760,000

= $1,685,000

After calculating the residual income, we will now calculate the current market value of this industry according to the residual income valuation method as follows;

V0 = $12,500,000 + $1,685,000 / (1+0.11)1 + $1,685,000 / (1+0.11)2 + $1,685,000 / (1+0.11)3 + $1,685,000 / (1+0.11)4 + $1,685,000 / (1+0.11)5

V0 = $12,500,000 + $1,685,000 / (1.11)1 + $1,685,000 / (1.11)2 + $1,685,000 / (1.11)3 + $1,685,000 / (1.11)4 + $1,685,000 / (1.11)5

V0 = 12,500,000 + 1,515,315.32 + 1,367,583.80 + 1,232,085.41 + 1,109,940.06 + 999,940.66

V0 = $18,724,865.25

The value of total shares is $18,724,865.25. To get the estimated price per share, we will divide the V0 by the number of shares outstanding.

That is;

Estimated price per share = $18,724,865.25/1,000,000 outstanding shares

Estimate price per share = $18.73

According to this valuation, each share will be issued at $18.73.

Importance of stock valuation

- Legal obligations

- The authenticity of financial statements

- Determine liquidity

- Determine income

- Understanding of risk

The valuation of stocks is a crucial part of doing business. If this is not carried out properly, it can result in two incorrect financial statements which in turn have a negative impact on the ability of a business to meet its objectives, resulting in serious consequences for the business.

Legal obligations

Another reason why a business should perform stock valuation such as retail stocktaking and food & beverage stocktaking is to fulfill legal obligations. By law, businesses are required to make sure that there is full disclosure of their stocks including their true number and value.

Determine financial position

Also, the valuation of stocks has a crucial role to play in the authenticity of a firm’s financial statements. The reported stock amount will have an effect on gross profit and net income on the profit and loss account and the amount of the current assets which includes total assets, working capital, and the owner’s equity on the balance sheet. Therefore, having an accurate stock valuation is critical. The valuation of stocks has been underemphasized in the small-size and mid-size business world. It is, however, crucial to ensure accurate stock measurement which in turn is helpful in producing meaningful financial statements as well as enabling informed business decision-making.

The stocks of a business are its largest current assets. A proper stock valuation can eliminate errors in the value of stocks. In turn, it ensures correct financial statements as well as presents the true financial position of the business.

Determine liquidity

The liquidity position of a business firm is a thing of interest to most creditors and investors. By ensuring that there is no understatement or overstatement of current assets, stock valuation is helpful in presenting the true liquid position of a business.

Determine income

If there is an error in the valuation of stocks, even if it is minor, it can affect the figures on the income statement. This will bring about an incorrect net income in the financial statement. A firm that performs proper stock valuation can correctly determine its business income.

Understanding of risk

As earlier pointed out, stock valuation can help a business firm to determine whether its stock is undervalued, overvalued, or at the market price. Investing in a company that has an overvalued stock brings about a huge downside risk. On the other hand, investing in a company that has an undervalued stock can reduce the risk significantly. With this, stock valuation enables both a firm and the investor to understand their risks.

Without having knowledge of when a stock is overvalued or undervalued, an investor may miss out on an opportunity to cash in on investment and profit. On the other hand, an investor who locates stocks that are undervalued in the market, or priced below where they are worth based on certain metrics, can grab an opportunity to earn profits.

FAQs

How is a stock price determined?

A stock price is determined through various methods. however, before a firm determines the method to use in valuing its stock, it is expedient to determine whether it is fit for that method. There are two basic methods of valuing a stock, that is absolute valuation and relative valuation. Under the absolute valuation, we have methods like the dividend discount model, the discounted cash flow model, and the residual income model. Under the relative valuation method, we have the comparative model which involves the use of financial metrics such as the P/E ratio among others are used.

What is stock value?

Stock value is the price of a stock in the marketplace. The stock value can be determined through an activity known as stock valuation. In other words, we are talking about the intrinsic value or theoretical value of shares. A stock can either be undervalued or overvalued. If it is undervalued, then it is an advantage for an investor to invest in those shares but if it is overvalued, it is a risky venture.

What are the different methods of stock valuation?

The different methods of stock valuation include the dividend discount model, discounted cash flow model, residual income model, and comparative model (comparable company analysis).

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.