Tangible assets are the opposite of intangible assets which do not take a physical form and have a theorized value rather than a transactional exchange value. Tangible assets examples include physical properties with monetary value; they are usually the main forms of assets in most industries and are usually the easiest to understand and value.

What are tangible assets?

Tangible assets are physical properties that possess definite monetary value. In essence, they take a physical form. They are frequently used as collateral for loans because they possess long-term valuations that are of great value to the lender. With this, it is important to note that they have a finite and discrete value.

Tangible assets are important to a business as they possess great value, they are very essential for the daily operations of the business. These assets have a clearly defined purchase value or acquisition cost. They can typically be transacted for some monetary value, however, the liquidity of different markets varies.

In order to uphold the value and productive capabilities of these assets, they require a significant amount of maintenance. They also require insurance protection in the event of a loss.

The net worth and core operations of a business are highly dependent upon its assets. Asset management and implications are one key reason for companies maintaining a balance sheet overall. Every organization records its assets on the balance sheet and there must be a balance in the simple equations asset minus liabilities equal to shareholders’ equity which governs the balance sheet.

A quick review of the balance sheet provides a layout for the tangible assets of a company listed by liquidity. The asset portion of the balance sheet is divided into two parts, current assets, and fixed assets. Current assets are assets that are convertible to cash in less than one year. On the other hand, long-term or fixed assets are not convertible into cash within a year. These assets in their categories support the operations of a company and help to achieve its main objective which is to generate revenue.

Types of tangible assets

- Fixed assets

- Current assets

The above-mentioned are the two types of tangible assets.

Fixed assets

Fixed assets are those assets that possess essential value for the business in the long run and are not readily convertible to cash at the end of an accounting period. They are needed for the daily operations of the business. As they cannot be converted to cash, they must be accounted for in the current accounting period and this is achievable by the means of depreciation. In other words, they are reduced in value over time through depreciation. Depreciation is a noncash balance sheet notation that reduces an asset’s value by a scheduled amount over time.

In the balance sheet, fixed assets comprise the second portion of the asset section. Examples of fixed assets include manufacturing plants, real estate properties, vehicles, equipment, furniture and fittings, computers, and office supplies.

The cost of these assets may or may not be part of the company’s cost of goods sold, but regardless of that, they are assets that hold real transactional value for the company.

Fixed or long-term assets are convertible to cash but not as quickly as current assets. Except for land, fixed assets depreciate over time. Land appreciates over time.

Current assets

Current assets refer to those assets that are useful in the business for a short period of time. By implication, they have a short life span because they can easily be converted to cash during the accounting period. Current assets may or may not possess the physical presence but they are of great use as they have definite value. They are highly liquid in nature, in other words, you can easily convert them to cash.

Examples of current assets are stocks, cash, marketable securities, accounts receivables, and cash equivalents. All these tangible assets are included in calculating the quick ratio of a company. Other current assets are included in calculating a company’s current ratio which shows how well a company can cover its liabilities with its current assets. Current ratio physical assets include inventory which is not as liquid as cash equivalents. However, it has a finite market value and can be sold for cash if needed in a liquidation.

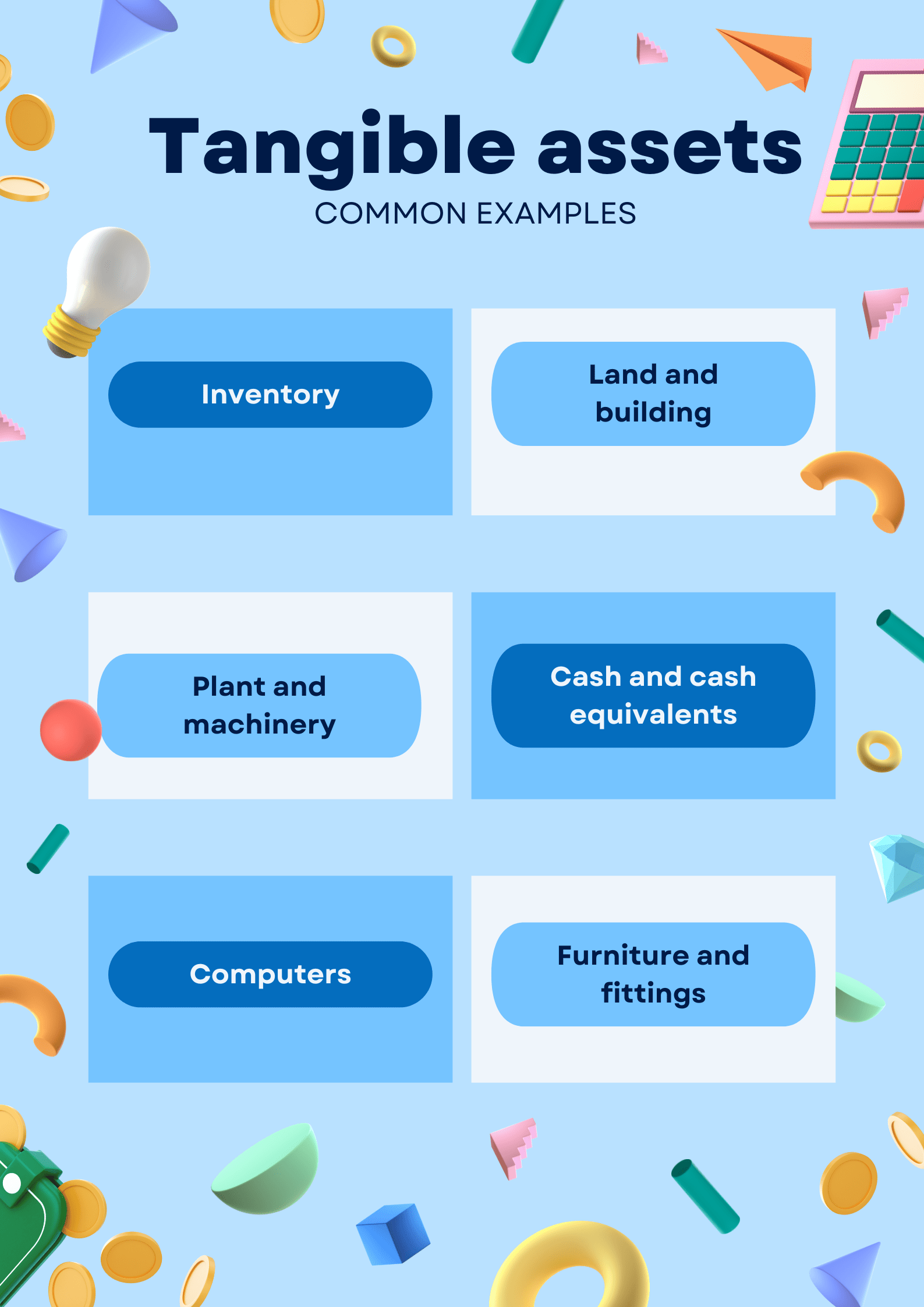

Tangible assets examples

- Inventory

- Plant and machinery

- Land and building

- Furniture, fixtures, and equipment (FF&E)

- Cash

Let us look at some examples of tangible assets of a company below.

Inventory

When we talk about inventory, it refers to the raw materials used in carrying out production as well as the goods produced and available for sale. This term can also be referred to as stock. A company’s inventory is a representation of one of the primary sources of revenue generation and subsequent earnings for the shareholders of the company. Inventory comes in three forms which are raw materials, work-in-progress, and finished goods. It falls under current assets on a company’s balance sheet.

In the balance sheet, opening stock in the trading, profit, and loss account does not reflect. The closing stock is reflected as a current asset on the balance sheet.

Plant and machinery

The term plant and machinery refers to any type of equipment and apparatus used for industrial activity. It can be the equipment used in manufacturing goods and services in the company and it can also be equipment such as excavators used in the construction industry. These are fixed assets that can depreciate over their years of useful life. Plant and machinery are considered a fundamental part of any business as they are useful in carrying out production activities.

Land and building

In economics, the land is the resource that contains the natural resources used in carrying out production. It is considered to be an inexhaustible gift of nature that is fixed and immovable.

Although other fixed assets depreciate, land does not. It appreciates over time and does not have a definite useful life. Building on the other hand probably the company or factory, is subject to depreciation as its value decreases over time.

Depreciation is not charged on land alone, but when a building is included, then depreciation can be charged.

Furniture, fixtures, and equipment (FF&E)

Furniture, fixtures, and equipment are movable assets. They do not have a permanent connection to the structure of a building. These items include desks, chairs, computers, electronic equipment, tables, partitions, etc. There is a substantial depreciation over their long-term use. However, they are important costs to be considered when valuing a company, especially during the events of liquidation.

Cash

Cash is a current asset and it is the most liquid type of asset. It can be used to purchase other assets.

Characteristics of tangible assets

- Physical presence

- Collateral

- Daily business operations

- Capital structure

- Depreciation

Physical presence

Unlike intangible assets, tangible assets have a physical appearance. This implies that you can see, touch, and feel them.

Collateral

A company can use its physical assets as collateral for obtaining loans for the expansion of its business. In other words, the lender can seize these assets if the company defaults on its loan payment because they possess definite transactional value.

Daily business operations

Tangible assets are essential for the maintenance of day-to-day business operations. Every company needs assets for its business to continue operating. This means that without assets, the continuity of the business is not guaranteed.

Capital structure

They play a vital role in determining the capital structure of the business.

Depreciation

Fixed assets are depreciated over a period of time, this also means that they possess a scrap or residual value.

Importance of tangible assets

- Depreciation

- Liquidity

- Collateral security

- Business valuation

- Daily running of the business

Depreciation

The depreciation of tangible assets is important to a company as it is a non-cash expenditure. By implication, it is an expenditure that helps a company to receive a tax benefit. However, there is no cash outflow from the business.

Liquidity

As tangible current assets are easily convertible to cash, they make provision for liquidity to the business thereby reducing risk. As long as the value of the assets that a business owns is greater than the money risked in acquiring them, a business typically remains safe and solvent.

Collateral security

Above, we stated that one of the features of tangible assets is that they can be used as collateral security to obtain loans. This is an important factor for every business. They play an important role in the capital structure of a business. They are positively related to leverage. In essence, companies that have more tangible assets generally utilize debt financing more heavily. It is easier to collateralize such assets and they do not lose a lot of value when the company faces financial distress. Therefore, it has been observed that companies that have fewer tangible assets borrow less from creditors while companies with more assets tend to borrow more from creditors.

Business valuation

Tangible assets are essential for business valuation. Because of this, it is important for a company to efficiently manage its assets during its life cycle. This is because errors can lead to an inaccurate valuation of the business as well as incorrect tax reporting. Therefore, a company must record and value its assets accurately in order to make the most of them.

By maintaining accurate asset records on the balance sheet, a company can show the profitability and the financial position of its business. This is why a balance sheet is also referred to as a statement of financial position. Also, a company can create accurate profit and loss reporting, increase goodwill and positive attitudes towards the business, give shareholders quality assurance, and attract investors.

In the course of selling the business, identifying assets and valuing them correctly is vital in determining the business’s net worth whether for the purpose of sale or bankruptcy.

With the presence of tangible assets, a company can determine its liquidity ratios which point toward its ability to repay debts.

Daily running of the business

As earlier pointed out, tangible assets are needed for the daily operations of every business. Without them, a business will not operate successfully. This also means that it can close down because while fixed assets possess long-term value for the company, current assets possess short-term value. In other words, a company is valueless without assets.

Tangible assets valuation

- Appraisal method

- Liquidation method

- Replacement cost method

Appraisal method

Under this method, a company hires an appraiser to determine the actual fair market value of its assets. The asset appraiser will carry out an assessment of the current condition of the assets such as the degree of obsolescence and level of wear and tear. After this, the appraiser will compare these values to the values that the assets can fetch in the open market.

Liquidation method

Here, the company tries to find out the cash it would acquire if it sells the assets as they can be converted to cash. It is important for the company to have knowledge about the minimum value it would receive from a quick sale or liquidation. The company hires an assessor to determine the value that an auction house, equipment seller, or other bulk asset buyers will be willing to pay for such categories of assets as those that the company owns.

Replacement cost method

Generally, an insurer makes use of the replacement cost method to calculate the value of the asset for insurance purposes. It helps in determining the amount it will cost to replace the asset.

Net tangible assets

Net tangible assets refer to the difference between the total physical assets of a company and all intangible assets and liabilities. In other words, they focus on physical assets such as property, plant, and equipment (PP&P) as well as cash instruments and inventory. Physical assets are listed on a company’s balance sheet while intangible assets as we know are assets without a physical form. The net tangible assets of a company can help in securing financing and determining the amount of risk it carries.

Determining the net tangible assets helps to find out if a company’s market share price is undervalued or overvalued. this activity takes place by comparing the value of the net tangible assets per share to that of the company’s current price. When it comes to liquidity, a company with a high net asset value has low risk. A high value of net tangible assets can serve as immunity against the uncertainty that can occur in the market and help in supporting the stock price of the company.

Net tangible assets can be seen as the book value of the company.

Tangible assets formula

Net tangible assets = Total assets – (liabilities + intangible assets)

Explaining the tangible asset formula:

- Total assets which can be found in the company’s balance sheet contain both tangible and intangible assets.

- Intangible assets are those assets that do not have physical properties such as goodwill, trademarks, and copyrights.

- Total liabilities are also found in the company’s balance sheet and this includes both long-term and current liabilities.

The approach used in transferring them to the income statement is that liquidity should be used to organize the current assets with the most liquid assets at the top of the list.

How to calculate tangible assets

A company can calculate its tangible assets by examining its balance sheet. The first step in doing this is to assess the worth of the assets, starting with the one that is the most liquid including cash and cash equivalent. Secondly, go to investing and ascertain the current market worth.

We have looked at the meaning of net tangible assets above. It was stated from the definition that the term refers to the total physical assets of a company minus the total liabilities and intangible assets of the company. This can be represented in a formula.

Example

Let us take, for example, a firm has total assets worth $1 million, total liabilities worth $100,000, and intangible assets worth $100,000. Using the formula above, we will calculate the net tangible assets as follows;

NTA = $1,000,000 – ($100,000 + $100,000)

= $1,000,000 – $200,000

= $800,000

Therefore, The value of the net tangible assets for this company is $800,000.

Tangible asset management

Tangible asset management is the process in which an organization tracks and maintains its physical assets and equipment. As we know, asset types include motor vehicles, furniture, machinery, etc.

Using the asset management system, an organization can do the following;

- Track and monitor all the physical assets.

- Oversee equipment and machinery in multiple locations.

- Lower the cost of maintenance.

- Improve efficiency in operation.

- Maintain a record of retired, sold, lost, or stolen assets.

Tangible asset management helps organizations to monitor all assets especially fixed assets, assess their condition, and keep them in good working condition. Through this, they minimize the lost inventory, equipment failures, and downtime, then improve the lifetime value of the asset.

The importance of tangible asset management

Fixed assets require large capital investment and may comprise a large portion of the company’s net worth. There are businesses where as much as 40% of investment goes to the purchase of equipment and vehicles. A company has a greater prospect of maximizing value from its investments the better and more effectively it manages its assets.

If a company fails to manage its assets, it may experience the following;

- Equipment failures

- Unplanned downtime

- Misplacement or loss of inventory

- Safety or environmental breaches

- Failure to comply or meet regulatory standards

For companies that have large inventories, the results may convert into millions of dollars in lost productivity, replacements, fines, or repairs. Beyond immediate costs, substandard equipment can have a negative impact on the quality of an organization’s products or services. In turn, this will affect customer satisfaction and the reputation of the business.

According to the ISO 55000 international standard, asset management should maximize the value of money. Generally, fixed asset management brings about an improvement in the quality and useful life of the equipment and ensures the best return on investment.

Accounting for tangible assets

As earlier pointed out, tangible assets are the easiest to value because they typically have a finite life span and value. Initially, they are recorded in the balance sheet but as they get used up, they are carried over to the income statement.

For example, an inventory is a tangible asset that when used, is then included in the cost of goods sold for a company. Cost of goods sold area representation of the costs directly involved in the production of goods. As a company uses up its inventory in the process of production, it is then recorded in the cost of goods sold.

Fixed assets such as machinery, are fixed tangible assets that are being recorded on the balance sheet. As their years of useful life are reduced, that portion is being expensed on the income statement in a process known as depreciation.

Depreciation is the process in which a company allocates a portion of the cost of an asset over the years as it is used to generate revenue for the company. This process is helpful because it helps to reflect the wear and tear on tangible assets as they are used during their lifetime.

As stated under the types of tangible assets, they are classified under fixed and current assets. They appear in the asset section of a firm’s balance sheet. Usually, fixed assets appear first with the depreciation amount. Here, the depreciation is subtracted from the actual value of the asset to give the net book value. After all the fixed assets are recorded in this case, then the current assets follow and they are summed up.

These assets may be aggregated into a single summary number or listed within several classifications of assets such as plant and machinery or furniture and fittings. On a contra account, fixed assets are being paired with an accumulated depreciation thereby reducing the fixed asset balance by the depreciation amount charged to date against all fixed assets on the books of the reporting entity.

FAQs

What makes an asset tangible?

An asset is tangible when it takes a physical form, that is, it can be seen, touched, and felt. Also, such assets have a definite life span and transactional or monetary value.

What is a tangible asset example?

Tangible asset examples include land, building, cash, cash equivalent, inventory, shares, plant, and machinery.

Are investments tangible or intangible assets?

Investments are tangible assets, this is because they are easily convertible to cash. For example, when you invest in shares, they are cash equivalents and are regarded as tangible assets.

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.