There are financial metrics that allow investors to assess a company’s ability to provide its investors with an acceptable return on their investment. Measuring a company’s tangible book value by deducting the company’s liabilities from its tangible assets gives investors a better understanding of how much money will be left after all of a company’s liabilities have been settled and its physical assets sold.

The tangible book value formula goes one step further from the book value formula by removing goodwill and intangible assets from a company’s net worth. It is a superior indicator of the money that could be distributed to common stockholders in the event of liquidation. Hence, the holders of common stock in a company calculate the TBV of a company to know its value should in case it goes bankrupt and liquidate. In this article, we will discuss the tangible book value, its calculation, and its formula.

Related: Price-to-book value ratio formula and examples

What is tangible book value (TBV)?

The tangible book value (TBV), also known as net tangible equity, is a financial metric that measures a company’s net asset value excluding the company’s goodwill and intangible assets. That is, a company’s TBV tells us the worth of all the company’s physical assets which excludes the company’s goodwill, intellectual property, patents, and trademarks. Intangible assets and goodwill are deducted in the tangible book value calculation because they cannot be easily sold in an event of liquidation compared to tangible assets like property, plant, and equipment.

Intangible assets are non-physical assets that are not easy to evaluate such as goodwill, brand equity, patents, computer software, licenses, films, customer lists, import quotas, intellectual properties (trade secrets, copyrights, patents, and trademarks), and R&D (research and development). Although such assets have value, they cannot be sold immediately for cash and as a result, may not be a part of the liquidation process.

Tangible assets, on the other hand, are assets that can be physically handled or touched such as cash, machinery, PP&E (Plant, property, and equipment), raw materials, inventories, vehicles, etc. Hence, determining a company’s tangible book value is a way of valuing the company by its equity without including its intangible assets. In the event of liquidation, common shareholders tend to receive an amount that is equivalent to the company’s net tangible book value after most of the tangible assets have been liquidated.

Net tangible equity meaning and interpretation

What does the tangible book value (TBV) of a company tell us? Since only physical assets are included in the tangible book value calculation, the TBV is a closer estimate of a company’s value should in case it file for bankruptcy and undergo liquidation. Hence, the TBV meaning to an investor is like a measure of how much the tangible assets of a company are worth. It tells us the residual net value of a company that belongs to common shareholders once all outstanding liabilities are serviced and the tangible assets are sold.

However, it is important to note that the calculated TBV is an estimation and not necessarily the actual value of a liquidated company. This is because certain intangible assets can still be sold and the liquidation value of physical assets is rarely exactly equal to the full value recorded on the books.

What is a good tangible book value?

Since a tangible book value represents the value of a company’s tangible assets minus its liabilities or outstanding debts, a higher value would be interpreted as a good tangible book value. The tangible book value shows investors and market analysts a clear picture of a company’s worth. Therefore, a company with a higher tangible book value would be more attractive to investors compared to a company with a lower TBV.

A negative tangible book value, on the other hand, can be an indication that the company has more liabilities than assets. It is an indication that the company probably has more debt than equity and owes more to creditors or shareholders than it is worth. Another possible reason for a negative tangible book value could be that the company must have been investing heavily in intangible assets, like goodwill, R&D, or trademarks. Recall, that the value of such assets is deducted during the tangible book value calculation. This means that a company that invests heavily in such assets may end up having a negative tangible book value.

Also, a negative tangible book value may also mean that the company has been losing money for a sustained period of time due to a variety of reasons, like poor investments that might have led to write-downs, high levels of debt, or poor financial management. However, a negative TBV is not automatically bad news for investors because there are several other factors that need to be considered as the TBV isn’t the only business valuation method to assess how strong a company’s balance sheet is.

See also: Book Value per share formula- BVPS calculation

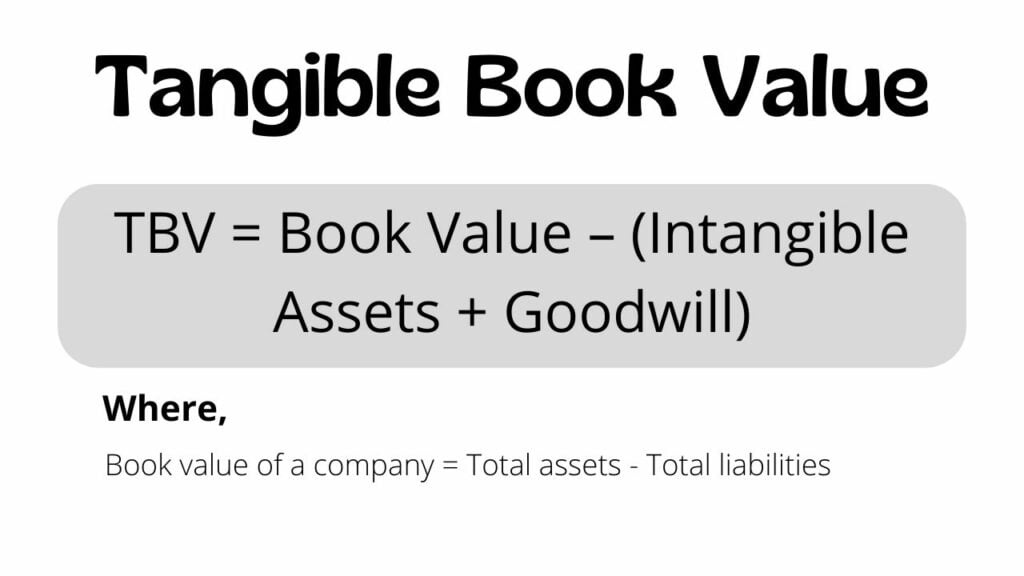

Tangible book value formula

The tangible book value formula is expressed as:

Tangible Book Value = (Total assets – Total liabilities) – (Intangible Assets + Goodwill)

OR

Tangible Book Value = Book Value – (Intangible Assets + Goodwill)

Where,

Book value of a company = Total assets – Total liabilities

Read also: Enterprise Value Multiples Formulas and Examples

Tangible book value calculation

The net tangible book value calculation is carried out by deducting any intangible assets and goodwill from the book value (total assets – total liabilities) of the company. Calculating the tangible book value for banks in an event of liquidation, for instance, would involve netting out intangible assets, such as loan servicing rights and goodwill to better represent the bank’s worth.

Let’s look at some examples of how to calculate tangible book value:

How to calculate tangible book value example 1

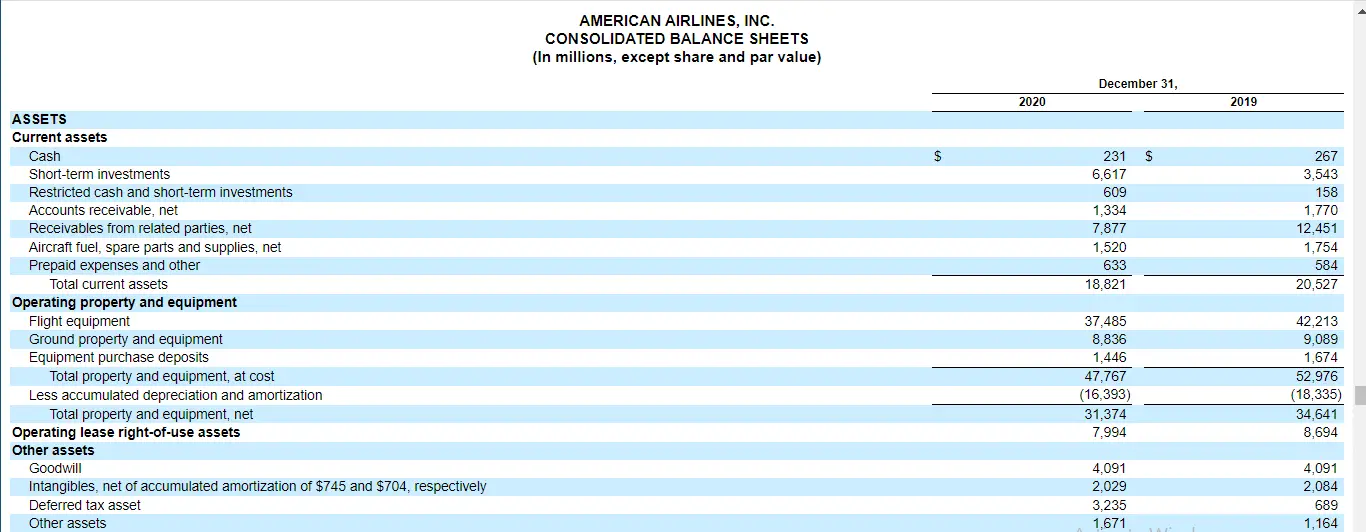

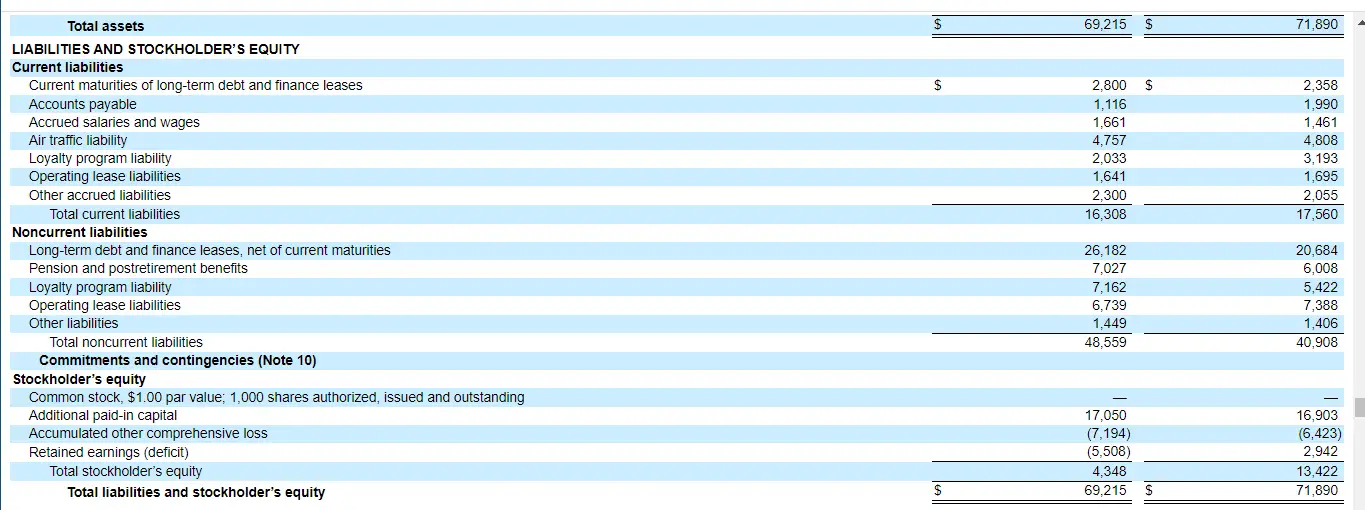

Using the balance sheet of American Airlines (AAL) below, we will calculate AAL’s tangible book value for the years 2019 and 2020.

Solution

AAL’s tangible book value calculation for 2019:

Using the tangible book value formula:

TBV = Book Value – (Intangible Assets + Goodwill)

- Book Value = (Total assets – Total liabilities) = $71,890 – $58,468 = $13,422

- (Intangible Assets + Goodwill) = $2,084 + $4,091 = $6,175

TBV = $13,422 – $6,175 = $7,247

This means that for 2019, the tangible book value of AAL is $7,247 million

AAL’s tangible book value calculation for 2020:

Using the formula for tangible book value:

TBV = Book Value – (Intangible Assets + Goodwill)

- Book Value = (Total assets – Total liabilities) = $69,215 – $64,867 = $4,348

- (Intangible Assets + Goodwill) = $2,029 + $4,091 = $6,120

TBV = $4,348 – $6,120 = -$1,772

This means that for 2020, AAL has a negative tangible book value of -$1,772 million.

Interpretation: From the calculation done, it is evident that the net tangible book value of AAL massively deteriorated in one year. The negative tangible book value of AAL in 2020 could be attributed to the global pandemic that greatly reduced demand for flight services. This eventually caused a deep deficit in shareholders’ equity as seen in the balance sheet.

How to calculate tangible book value example 2

Assume you are a financial analyst and you want to calculate the tangible book value of a particular stock from a client’s portfolio to compare it to the company’s stock price that is trading at $15.88. Let’s say you feel that the stock is overvalued, and is trading at a higher price than its assets. Hence, you get the company’s balance sheet and derive the following details:

- Total assets = $97,366 million

- Total Liabilities = $53,125 million

- Intangible assets value = $7,789 million

- Goodwill = $12,706 million

This is how you will calculate the company’s tangible book value:

Solution

Using the tangible book value formula:

TBV = (Total assets – Total liabilities) – (Intangible Assets + Goodwill)

TBV = ($97,366 million – $53,125 million) – ($7,789 million + $12,706 million)

TBV = $44,241 million – $20,495 million = $23,746 million

This means that the company has a tangible book value of $23,746 million.

Now that you know the company’s tangible book value, to compare it to the company’s stock price of $15.88, you will have to calculate the tangible book value per share (TBVPS). Assume you find that the company’s number of outstanding shares is 2,000 million. The calculation of the tangible book value per share would be as follows:

TBVPS = Tangible Book Value / Number of Outstanding Shares

= $23,746 / 2,000 = $11.873

Interpretation: From the calculation done, it shows that the company’s TBVPS is lower than the stock price of $15.88. This confirms that the stock is actually overvalued as suspected. That is, the value of the company’s shares is less than the value of its tangible assets. This means that should, in any case, the company was to be liquidated, the shareholders would get $11.873 per share.

See also: Par Value of Stock Meaning, Formula, and Example

Tangible book value vs book value

The difference between tangible book value vs book value is that tangible book value is a company’s book value less the value of any intangible assets while a book value is a company’s value of its assets minus its liabilities. The tangible book value is similar to the book value; the slight difference is that the value of intangible assets is excluded from the calculation. Hence, the formula for book value vs tangible book value is as follows:

| Tangible book value | Book value |

|---|---|

| TBV = Book Value – (Intangible Assets + Goodwill) TBV = (Total assets – Total liabilities) – (Intangible Assets + Goodwill) | BV of an asset = Total cost – Accumulated depreciation BV of a company = Total assets – Total liabilities |

A company’s book value is calculated by subtracting its total liabilities from the total assets while a tangible book value is calculated by subtracting any intangible assets and goodwill from the company’s book value. This means that the tangible book value is a more detailed book value that takes into consideration other factors like deducting goodwill and intangible assets.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.