The tax liability formula is used to calculate the payment owed by an individual, business, or other entity to a federal, state, or local tax authority. Generally, an individual or a corporation would have a tax liability when income is earned or profits are made by selling an investment or other asset.

Taxes are imposed by various taxing authorities, such as the federal, state, and local governments to generate funds that are used to pay for services such as funding social programs, repairing roads, and maintaining a military. The United States, therefore, happens to have a progressive tax rate system wherein individuals are taxed at different rates based on their income and tax brackets.

In order to calculate tax liabilities, there are separate tax slabs for single filers, married couples filing together, married couples filing separately, and heads of households which are based on taxable income brackets. In this article, we will discuss the total tax liability formula and learn how to calculate tax liability for the year.

Related: Liabilities Examples in Accounting

What is tax liability?

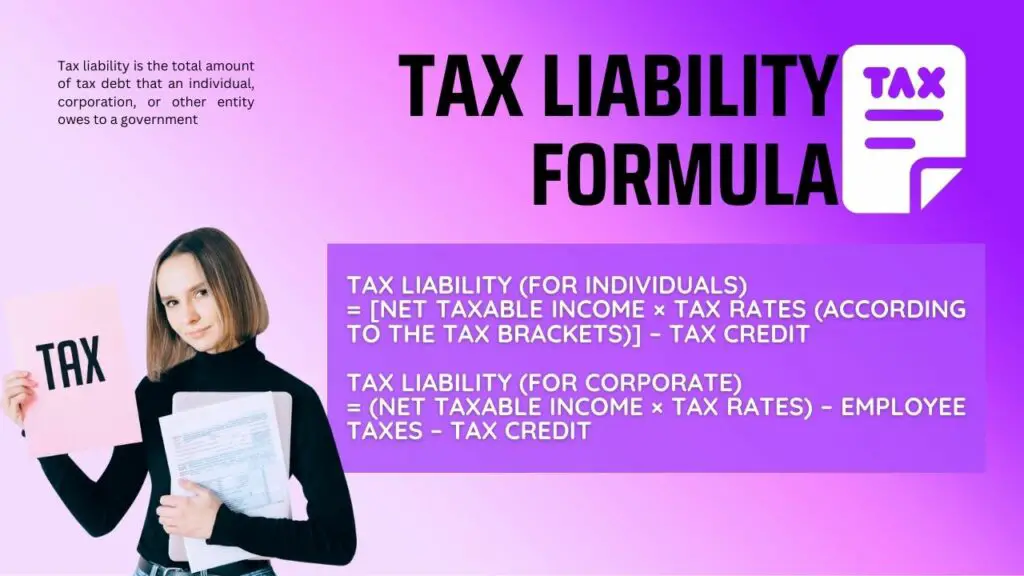

Tax liability is the total amount of tax debt that an individual, corporation, or other entity owes to a government. An individual or a corporation incurs a tax liability when income is earned or profit is made from selling an asset or investment. Hence, federal income taxes, sales tax, and capital gains tax are all types of tax liabilities.

In other words, your tax liability is any amount that you owe a taxing authority, such as the Internal Revenue Service. It is the amount of money that you owe to the IRS or another taxing authority when you finish preparing your tax return. Hence, the total tax liability formula and calculation would include any balances still owed from previous years.

Therefore, tax liability doesn’t just include the current year, it factors in any years for which taxes are owed. This means that if any unpaid taxes from previous years are due, those are also added to your tax liability. Tax liabilities cover all forms of taxes, such as capital gains and self-employment tax, as well as interest and penalties. Federal income tax is the most common for Americans. For federal taxes, you use the tax brackets and standard deductions issued by the Internal Revenue Service.

Furthermore, companies withhold income, medicare taxes, and social security from employees’ wages and send them to the federal government. These are known as deductions which are not included in taxable income. This means that a tax liability isn’t based on an individual’s overall earnings but on his/her taxable income after they take deductions and claim tax credits.

How it works

U.S. taxpayers use the IRS Form 1040 to file an annual income tax return. That is, in a current year, taxpayers are expected to pay taxes for the previous year’s income. For instance, the current year’s federal tax liability for 2022 appears on line 37 of the 2022 Form 1040; the return filed in 2023. If the tax amount is unpaid, it is further added to the current year’s liability which will be paid in the next tax period. Such outstanding taxes are referred to as back taxes.

An individual’s tax liability is just how much he/she owes in taxes. Also, it is possible for an individual to have no income tax liability if he or she doesn’t meet the income requirements to file taxes. For employed individuals, it is usually a simple matter of consulting the tax tables for the year and calculating their income tax on Form 1040.

Nevertheless, tax liability calculation can be a bit more complicated for those that are self-employed or run a business. To learn how to calculate tax liabilities of a business, start with knowing the type of corporation under which your business falls. That is, the amount of federal income tax liability that your business owes would depend on whether the business is a C corporation or not. If the business is a C corporation, it will be taxed twice, at both the corporate and shareholder levels. Hence, the income tax rate will be a flat 21%.

C corporations are the only kind of business that pays corporate income taxes. Therefore, if the business is not a C corporation, its tax rate will depend on your taxable income and your filing status. Businesses that are not C corporations are known as flow-through entities because profits and losses flow through the business to owners and shareholders, who pay taxes at their individual tax rates.

For federal taxes, you use the tax brackets and standard deductions issued by the Internal Revenue Service to calculate your tax liability for the year:

Standard deductions

The table below shows the IRS 2022 standard deductions and 2023 standard deductions:

| Standard deductions for 2022 | Standard deductions for 2023 |

|---|---|

| $12,950 for single filers | $13,850 for single filers |

| $12,950 for married couples filing separately | $13,850 for married couples filing separately |

| $19,400 for heads of households | $20,800 for heads of households |

| $25,900 for married couples filing jointly | $27,700 for married couples filing jointly |

Tax brackets

Tax liability is determined by subtracting your standard deduction from your taxable income and referring to the appropriate IRS tax brackets for the taxable period/year.

Tax brackets for 2022:

| Tax Rate | Single filer taxable income | Married filing separately taxable income | Married filing jointly taxable income | Head of household taxable income |

|---|---|---|---|---|

| 10% | $10,275 or less | $10,275 or less | $20,550 or less | $14,650 or less |

| 12% | Over $10,275 | Over $10,275 | Over $20,550 | Over $14,650 |

| 22% | Over $41,775 | Over $41,775 | Over $83,550 | Over $55,900 |

| 24% | Over $89,075 | Over $89,075 | Over $178,150 | Over $89,050 |

| 32% | Over $170,050 | Over $170,050 | Over $340,100 | Over $170,050 |

| 35% | Over $215,950 | Over $215,950 | Over $431,900 | Over $215,950 |

| 37% | Over $539,900 | Over $323,925 | Over $647,850 | Over $539,900 |

Tax brackets for 2023:

| Tax Rate | Single filer taxable income | Married filing separately taxable income | Married filing jointly taxable income | Head of household taxable income |

|---|---|---|---|---|

| 10% | $11,000 or less | $11,000 or less | $22,000 or less | $15,700 or less |

| 12% | Over $11,000 | Over $11,000 | Over $22,000 | Over $15,700 |

| 22% | Over $44,725 | Over $44,725 | Over $89,450 | Over $59,850 |

| 24% | Over $95,375 | Over $95,375 | Over $190,750 | Over $95,350 |

| 32% | Over $182,100 | Over $182,100 | Over $364,200 | Over $182,100 |

| 35% | Over $231,250 | Over $231,250 | Over $462,500 | Over $231,250 |

| 37% | Over $578,125 | Over $346,875 | Over $693,750 | Over $578,100 |

Tax liability on capital gains

When a capital asset is sold, the difference between the adjusted basis in the asset and the amount that is realized from the sale is a capital gain or a capital loss. Taxes are owed for any gain on the sale of assets, investments, or real estate. Any capital gain derived from the sale is taxed and if you sell it for a loss, you can report it as a capital loss.

Capital gains can be taxed in two different ways, either as long-term capital gain or short-term capital gain (see Topic no. 409 capital gains and losses). A short-term capital gain is included in your income if you’ve held an asset for one year or less and sold it for a gain. However, if an asset is held for more than one year and then sold for a gain, it is considered a long-term capital gain which is subject to the capital gains tax. That is, long-term capital gains tax rates for the 2022 and 2023 tax years are 0%, 15%, or 20% of the gain made, depending on the income of the filer.

Similar to the income tax brackets, there are capital gains thresholds that are used to calculate tax liability owed on the capital gain:

2022 Capital gains tax:

| Tax Rate | Taxable income for a single filer | Taxable income for married filing separately | Taxable income for married filing jointly | Taxable income for the head of household |

|---|---|---|---|---|

| 0% | $41,675 or less | $41,675 or less | $83,350 or less | $55,800 or less |

| 15% | $41,676 to $459,750 | $41,676 to $258,600 | $83,351 to $517,200 | $55,801 to $488,500 |

| 20% | $459,751 or more | $258,601 or more | $517,201 or more | $488,501 or more |

2023 Capital gains tax:

| Tax Rate | Taxable income for single filer | Taxable income for married filing separately | Taxable income for married filing jointly | Taxable income for the head of household |

|---|---|---|---|---|

| 0% | $44,625 or less | $44,625 or less | $89,250 or less | $59,750 or less |

| 15% | $44,626 to $492,300 | $44,626 to $276,900 | $89,251 to $553,850 | $59,751 to $523,050 |

| 20% | $492,301 or more | $276,901 or more | $553,851 or more | $523,051 or more |

Tax liability for corporations

The Tax Cuts and Jobs Act greatly simplified the tax liability calculations for C corporations by replacing the graduated corporate tax rate schedule that included eight different tax rate brackets with a flat 21% tax rate. This means that if a business is a C corporation, no matter how much taxable income the business has, its income tax rate will be 21%.

On the other hand, if a business is not a C corporation, it means that the business is considered to be a flow-through entity, which means that the owner will pay the taxes himself, instead of the business paying them. Hence, his tax rate will depend on the amount of the business’s taxable income and his tax filing status.

See also: Taxes for Stock Options

Reducing tax liabilities

In as much as taxes can take a huge toll on your take-home pay, it is something that everyone has to live with to fund the government programs that society relies on. Nonetheless, there are a few ways one can reduce the amount of taxes one pays. Tax liabilities can be lowered by claiming deductions, exemptions, and tax credits. Hence, it is important to determine your eligibility for tax credits and deductions before you file.

One of the ways that people reduce their tax liabilities is by contributing to a retirement or health savings account. People also use credits or other deductions to reduce their taxable income. Deductions can help reduce the amount of an individual’s income before the tax owed is calculated. Such deductions include:

- Work-related deductions

- Itemized deductions

- Education deductions

- Health care deductions

- Investment related deductions

Credits can also reduce the amount of tax one owes or increase their tax refund. Such credits include:

- Family and dependent credits

- Income and savings credits

- Homeowner credits

- Electric vehicle credits

- Health care credits

As a matter of fact, certain credits may even give you a refund even if you don’t owe any tax.

Check out: RSU Taxes- How are RSUs taxed?

Tax liability formula

The calculation of tax liability is done by subtracting your standard deduction from your taxable income and referring to the appropriate IRS tax brackets. Hence, the tax liability formula is expressed as:

Tax Liability (for individuals) = [Net taxable income × Tax rates (according to the tax brackets)] – Tax credit

Tax Liability (for corporate) = (Net Taxable Income × Tax Rates) – Employee Taxes – Tax Credit

According to the income tax liability formula, income tax is determined in part by tax brackets; that is there is a percentage of each portion of your income that you must pay in taxes which varies depending on both your filing status and how much you earn.

For instance, if you were single and you were to earn a net taxable income of $10,200, you will be in the 10% tax bracket in 2022. Therefore, using the tax liability equation (10% of $10,200), your income tax liability would be $1,020. Assuming you were to earn a net taxable income of $95,000, it means you would be pushed up into a 24% tax bracket on the portion of your income that exceeds $89,075.

It is important to note that your annual tax liability formula shouldn’t be based on the total money you earn in a given year. Rather, it should be based on your earnings minus the standard deduction for your filing status, or your itemized deductions if you decide to itemize instead.

Also, it can be based on any above-the-line deductions (adjustments to income) or tax credits you might be eligible to claim. Hence, the net taxable income in the tax liability formula for an individual is calculated by deducting the exemptions and deductions as allowed in income tax from the total income earned.

For the corporate tax liability formula, the net taxable income is calculated by deducting all the expenses and deductions from the total revenue and other income earned. That is, in order to calculate a corporation’s taxable income, the cost of goods sold, operating expenses, and interest paid on debts are deducted from the company’s gross sales.

Also, adjustment for a tax deduction or credit is made to arrive at the final income that can be taxable. In other words, net taxable income is the amount of income earned by an individual or an organization that eventually creates a potential tax liability.

For an individual, the formula for the taxable income is expressed as:

Taxable Income = Gross total income – Total exemptions – Total deductions

On the other hand, the formula for a corporation’s taxable income is expressed as:

Taxable Income = Gross sales -Cost of goods sold -Operating expense -Interest expense – Tax deduction/ credit

Deferred tax liability formula

Deferred tax liability is a listing on an organization or entity’s balance sheet that records taxes that are owed but are not due to be paid until a future date. The deferred tax liability formula is expressed by finding the difference between the organization’s taxable income and its account earnings before taxes, then multiplying that by its expected tax rate. That is, deferred tax liabilities can be calculated using the formula:

Deferred tax liability = Temporary difference x Tax rate

Where; Temporary difference = Carrying amount – Tax base

The deferred tax liability formula above can be used in the calculation of deferred taxes that may arise from unused tax losses or unused tax credits.

Related: Incentive stock options tax treatment

Calculation of tax liability

In order to calculate tax liabilities for the year, simply add up all your income and subtract any applicable deductions; then apply the resulting adjusted gross income figure to the tax tables for your filing status. That is, if, for instance, you paid interest on student loans or you are self-employed and paid health insurance premiums throughout the year, you may be able to subtract those amounts from your gross income.

Another instance of applicable deductions would be if you contributed to a health savings account (HSA) or an employer-sponsored retirement plan that allows pre-tax deferrals. Such amounts won’t be included in your taxable income and are referred to as adjustments to income, or above-the-line deductions which results in your adjusted gross income (AGI).

Here are various examples showing how to calculate tax liability for the year:

Example 1: How to calculate tax liability for a single filer

Assume Miss Mary is a single filer in 2022, earning $72,950 per year. After applying her standard deduction of $12,950, her reportable income (adjusted gross income) would be $60,000. Assuming Miss Mary has no other deductions or income; this is how to determine tax liability for Mary:

Solution

Since Mary’s adjusted gross income of $60,000 is between $41,775 and $89,075, she falls into the 22% tax bracket. However, her federal tax liability is computed for each tax bracket up to the one that she is in.

| Tax Rate (2022) | Single filer taxable income | Tax liability calculations [Net taxable income x Tax rates] |

|---|---|---|

| 10% | $10,275 or less | 10% x $10,275 = $1,027.5 |

| 12% | Over $10,275 | 12% x ($41,775 – $10,275)= 12% x $31,500 = $3,780 |

| 22% | Over $41,775 | 22% x ( $60,000 – $41,775) = 22% x $18,225 = $4,009.5 |

| 24% | Over $89,075 |

- Her first $10,275 is taxed at 10%, so she owes $1,028

- Her taxable amount is over $10,275 but under $41,775 and so is taxed at 12%, thus she owes $3,780

- The amount is over $41,775 but under $89,075 and so is taxed at 22%, thus Mary owes $4,009.5

We total each amount that Mary owes per bracket. That is, using the total tax liability formula, Mary’s total tax liability will be: $1,027.5 + $3,780 + $4,009.5 = $8,817

This means that Miss Mary owes a tax liability of $8,817 for the year 2022 plus any back taxes if any.

Example 2: Calculation of tax liability on capital gains

Let’s assume Mr. Peter purchased 100 shares of Company ABC common stock for $10,000 in 2022 and sells them five years later for $18,000. He makes an $8,000 gain which is a taxable event. Since he held the stock for more than one year, the gain is a long-term capital gain.

The long-term capital gains tax rates are 0%, 15%, or 20% of the gain made, depending on the income of the filer. Imagine Mr. Peter is a single filer in 2022, earning $72,950 per year and after applying his standard deduction of $12,950, his adjusted gross income was $60,000 which falls between $41,676 to $459,750. This means his capital gains bracket is 15%.

| Tax Rate | Taxable income for a single filer |

|---|---|

| 0% | $41,675 or less |

| 15% | $41,676 to $459,750 |

| 20% | $459,751 or more |

This means that Mr. Peter would have to pay 15% of $8,000 in taxes. That is, using the federal tax liability formula: Net taxable income x Tax rates = 15% x $8,000 = $1,200

This means that on the long-term capital gain of $8,000, Mr. Peter owes $1,200.

For short-term capital gains

On the other hand, if Mr. Peter had held the stocks for less than one year, he will include the $8,000 profit in his gross income before subtracting his standard deduction. That is since he earned $72,950 and had $8,000 in short-term capital gains, his total income is $80,950. After applying his standard deduction of $12,950, his adjusted gross income will now be $68,000. This means Mr. Peter will be in the 22% tax bracket and would work through his tax liability calculations like this:

| Tax Rate (2022) | Single filer taxable income | Tax liability calculations [Net taxable income x Tax rates] |

|---|---|---|

| 10% | $10,275 or less | 10% x $10,275 = $1,027.5 |

| 12% | Over $10,275 | 12% x ($41,775 – $10,275)= 12% x $31,500 = $3,780 |

| 22% | Over $41,775 | 22% x ($80,950 – $41,775) = 22% x $39,175 = $8,618.5 |

| 24% | Over $89,075 |

Tax liability = $1,027.5 + $3,780 + $8,618.5 = $13,426

This means that Mr. Peter owes a tax liability of $13,426 for the year 2022.

Example 3: How to determine tax liability for married couples filing jointly

Let’s look at an example of how to find tax liabilities for married couples filing jointly. Assuming Wally owns a flow-through entity (Wally’s Widgets) that supposedly ends up with a taxable income of $300,000 in 2023 and he files a joint tax return with his wife, Sandra. Here is how to calculate his total tax liability:

Solution

| Tax Rate (2023) | Married filing jointly taxable income | Tax liability calculations [Net taxable income x Tax rates] |

|---|---|---|

| 10% | $22,000 or less | 10% x $22,000 = $2,200 |

| 12% | Over $22,000 | 12% x ($89,450 – $22,000)= 12% x $67,450 = $8,094 |

| 22% | Over $89,450 | 22% x ($190,750 – $89,450)= 22% x $101,300 = $22,286 |

| 24% | Over $190,750 | 24% x ($300,000 – $190,750)= 24% x $109,250 = $26,220 |

| 32% | Over $364,200 |

Therefore, Wally’s tax liability calculations would be: $2,200 + $8,094 + $22,286 + $26,220 = $58,800

Last Updated on November 3, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.