The different types of general ledger accounts are contained in the general ledger which summarizes all the financial transactions within a company. The general ledger contains important information needed for the preparation of a company’s financial statements.

Companies that make use of double-entry accounting make use of general ledgers to keep accounting records of their business transactions. The double-entry principle simply requires each transaction to have debit and credit entries and at all times, debit and credit balances should equal each other. In this article, we see what general ledgers entail, the types of general ledgers, and how to make records therein.

See also: Business Valuation Methods and Examples

What is a general ledger?

A general ledger is an accounting record that compiles every financial transaction carried out by a firm to provide accurate entries for financial statements. In other words, it is a document containing accounting summaries for accounts used by a company.

An account can be thought of as a notebook filled with business transactions from a specific account. So, the cash notebook would have records of all the business transactions that involve cash. Using the same analogy, we could consider a ledger as a folder that contains all of the notebooks in it. It is oftentimes referred to as a book of second entries because business transactions are first recorded in journal entries. After the journals are complete for the period, the account summaries will then be posted to the ledger.

With this, we can see a ledger account as a master accounting document that includes the past debit and credit transactions of a business and serves as a foundation of the double-entry accounting system. These transactions are usually organized by accounts; assets, liabilities, equity, expenses, and revenue. So, these accounts form the types of general ledger accounts.

The general ledger account is relevant for the assessment of a company’s financial performance. As a business owner, one can use a general ledger to form a more accurate picture of a company’s financial standing and profitability which may influence financial decisions positively.

In essence, general ledgers are important in terms of a company’s financial health because they are helpful in balancing a company’s books by compiling a trial balance and producing important financial statements. They are useful in tracking a company’s financial performance and cash flow, correct filing of taxes, and visualizing every financial transaction.

Many financial statements such as cash flow statements, income statements, and balance sheets are created using the transaction details contained in the general ledger.

General ledger in relation to double-entry accounting explained

Double-entry accounting is the most common system of bookkeeping, it is a way of managing a business’s daily transactions and staying on top of possible accounting errors. Here, every business transaction is recorded at least twice, when money is leaving an account and when money is entering an account. In essence, double-entry accounting requires financial statements to have debit and credit entries and the debit must be equal to the credit.

So, the term “balance the books” originates from double-entry bookkeeping. A general ledger helps in the achievement of this goal by compiling journal entries and allowing accounting calculations.

With this, we can say that the general ledger functions with double-entry accounting. Oftentimes, businesses that employ double-entry bookkeeping accounting make use of a general ledger. As stated above, this means that each financial transaction that takes place affects at least two sub-ledger accounts, remember that the types of general ledger accounts have sub-accounts under each. Here, each accounting entry has at least one debit and one credit transaction.

Double-entry transactions are also called journal entries which are posted in two columns, that is, debit entries on the left and credit entries on the right, and the total of debit and credit entries must balance.

The accounting equation which underlies the double-entry accounting states that shareholders’ equity is equal to total assets minus total liabilities. So, the balance sheet follows this format and shows information at a detailed account level. For instance, the balance sheet shows several asset accounts including cash and accounts receivable under its current assets section. Even in cases whereby the accounting equation is presented differently such as assets equal to total liabilities plus shareholders’ equity, the balancing rule is always applicable.

Assuming a company receives payment from a client for a $200 invoice, the accountant will increase the cash account with a $200 debit and complete the entry with a credit which means a reduction of $200 to accounts receivable. Here, the posted debit and credit amounts are equal, meaning that they are balanced. In this instance, we see that one account (cash) is increased by $200 while another asset account (accounts receivable) is decreased by the same amount.

The net result is that both the increase and the decrease only affect one side of the accounting equation (assets) and with this, the equation still remains in balance.

General ledger and financial statements

After the entries are made in the general ledger, the balances of all the ledger accounts are taken to the financial statements which are the trial balance from which the cash flow statement, income statement, and balance sheet, are prepared. A trial balance is a worksheet with the column of debit and credit in correspondence to the rules of double-entry bookkeeping also known as the dual aspect of accounting, which has been discussed above.

As per this rule, every financial transaction affects at least two accounts which in turn causes them to lose or gain something of equal amounts. For example, goods purchased with cash will cause goods to be debited as an asset while the cash account will be credited to finance the purchase.

Trial balance holds the balance of all the ledger accounts and if the bookkeeping and accounting are done appropriately, then the sum of the trial balance’s debit side will be equal to the sum of its credit side. If the summation of both sides does not correlate, it is an indication of discrepancies or errors that will call for rectification.

It is only after there is a match in the balances that the accounts will be considered for profit or loss calculation, making use of expenses and revenues in the income statement as well as assets, liabilities, and equity in the balance sheet. As emphasized, the debit and credit balances are to match.

See also: Net Income Vs Net Profit Margin Differences and Similarities

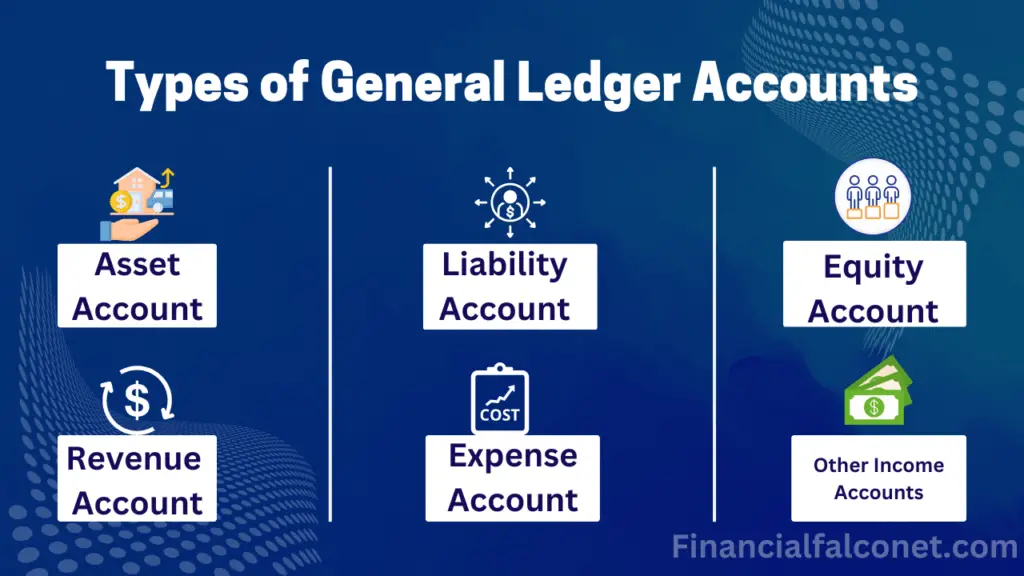

Types of general ledger accounts

- Asset accounts

- Liability accounts

- Equity accounts

- Revenue accounts

- Expenses accounts

- Other income accounts

Typically, a general ledger records the above-mentioned accounts. This structured process helps investors, management, stakeholders, and analysts to assess the ongoing financial performance of the company.

Asset accounts

Asset accounts are categories in a business’s books of accounts that show the value it owns, that is, they record the assets owned by a company. A debit to an asset account is an indication that the business owns more assets while a credit to the same account implies a decrease in assets. In other words, an asset account is debited if assets enter the company and credited if assets leave the company.

Assets are known to provide economic benefits to the company either immediately or in the future. They can be tangible assets or intangible assets and tangible assets can either be fixed or current assets. Fixed assets include plant, equipment, machinery, and vehicle. Current assets include accounts receivable, cash, inventory, and investments. Intangible assets include copyright, trademark, patents, and goodwill.

Liability accounts

A liability account is a type of account that records all the liabilities of a company, that is, all legally binding obligations payable to a third party. Liability accounts appear in a firm’s general ledger which is later aggregated into the liability line items on the balance sheet. Samples of the types of liability accounts that a company may use can fall under long-term liabilities such as loans, mortgages, etc, and short-term liabilities such as accounts payable, accrued liabilities, interest payable, notes payable, wages payable, etc.

The natural balance of a liability account is a credit, therefore, any entry that brings about an increase in the balance of a liability account will appear on the right side of the journal entry. A debit entry on the other hand reduces the balance of a liability account. Sometimes, a liability account is paired with a contra-liability account which contains a debit balance when combined with a liability account which reduces its total balance.

Shareholders’ equity accounts

Equity accounts represent the financial representation of business ownership. Equity can come from payments to a business by its owners or from residual earnings that the business generates. Because of the different sources of equity funds, equity is recorded in different types of accounts.

With the exception of the treasury stock account, every equity account has a natural credit balance. If the retained earnings account has a debit balance, it is either an indication that the business has been experiencing losses or that the business has issued more dividends than it had available through retained earnings.

Equity is calculated by subtracting a company’s liabilities from its assets, therefore, it is concluded as the remaining assets available to the company. Examples of equity accounts include retained earnings/earnings surplus, common stock, and treasury stock accounts.

Revenue accounts

Revenues are the assets that a company has earned through its business activities such as delivering a service or sales. The aim of designing revenue accounts is to record different types of sales transactions. An organization can generate different types of revenue, so, these sub-accounts are recorded in the revenue account in order to report the aggregate revenue by type. This is done for further management analysis. The accounts in which revenue transactions can be recorded are dependent on the nature of the underlying transactions. Examples of revenue accounts are sales and service fee revenue.

Expense accounts

Expense accounts represent the record of all expenses incurred by a company. It includes the different types of expenditures in an organization’s accounting records or money spent on business activities with the hope of generating profit. In essence, expense accounts record the cost of running a business which includes salaries, rent, advertising, cost of goods sold, etc.

Expenses have a natural debit balance, meaning that a credit to this account indicates a decrease in the balance in the expense account.

Non-operating or other income accounts

This is an additional type of general ledger account that refers to business income that is not related to core business operations and generally takes place outside of the daily operations of a business. For example, one might sell an asset that has been owned for years and record the revenue received from the sale of the asset in a non-operating income account. Non-operating income accounts include interest received, loss on disposal of assets, gain on sale of assets, etc.

How to prepare a general ledger

A general ledger contains the date and description of each transaction (which could be an expense, revenue, asset, liability, or equity) alongside the debit and credit side of a T-shaped visual picture of the transaction. The model is known as T-account.

The basic steps below are followed to prepare a general ledger:

- The name of the account should be written at the top of the page in order to make it easy to find in the future. In the general ledger, each account should have at least one entire page.

- The account numbers should be added below the account name in the general ledger.

- Records of transactions should be done in chronological order in order to keep the company’s financial records organized. This will make it easy to find specific items by date.

- The next thing to do is to decide whether the account needs to be debited or credited. Under the types of general ledger accounts, we explained that assets and expenses increase on the debit side and decrease on the credit side of the account while liabilities, equity, and revenue are increased on the credit side and decrease by a debit entry.

For the general ledger to balance, the account balances on both the debit side and the credit side must be equal. If the ledger does not balance, then there will be a need to investigate and include appropriate adjusting entries at the end of the accounting cycle.

General ledger format

| Account: |

Page Number: |

|||

| Date | Description | Ref. | Debit (amount) | Credit (amount) |

Examples: Types of ledger accounts

Example 1

A business owner receives $700 from a debtor on March 1 and on March 15, he purchased goods with $200 cash. The general ledger entries will look like this:

| Cash Account: | ||||

| Date | Description | Ref. | Debit | Credit |

| March 1 | Debtor | 700 | ||

| March 15 | Goods purchased | 200 | ||

| Debtor Account: | ||||

| Date | Description | Ref. | Debit | Credit |

| March 1 | Cash | 700 | ||

| Goods Account: | ||||

| Date | Description | Ref. | Debit | Credit |

| March 15 | Cash | 200 | ||

In the general ledger, the cash amount in the company’s bank account increased and it is debited while the debtor account is credited since the debtor now owes less money. The purchase of goods transaction on March 15 brings about a decrease in the company and with this, the cash account is credited by the amount of transaction while the amount of goods in the company increases, and the goods account gets debited by the amount of transaction.

T-accounts are useful for the creation of a visual presentation of transactions in the general ledger. Subsidiary ledgers also referred to as sub-ledgers help one to understand the numbers in the general ledger by showing all the transactions that are associated with the account.

In essence, based on the transaction that takes place, a debit and credit journal entry will be made and from there, general ledgers will be created. It is from the general ledger that financial statements will be prepared.

Example 2

On July 16, 2018, a UK textile company sold goods to customers for cash of $45,000. The journal entry will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| July 16, 2018 | Cash | 45,000 | |

| Sales | 45,000 |

The general ledger will be as follows:

This example shows the general ledgers in T-format.

Example 3

On the 1st of January, a firm received $10,000 from a debtor and on the 9th, it purchased goods worth $4,000. The business also paid $ 1,000 for rent on the 11th of January. Ledgers are to be prepared for all the accounts involved in the transaction.

Considering the debit and credit rules, the fact that the firm received cash from the debtor will increase the cash balance which will be a debit entry. On the other hand, cash payments for rent and goods will have a credit entry which implies a reduction in the cash account balance. The debtor’s account will be credited, which means the debtor is the giver of cash.

After purchase, the goods which are an asset will be debited as this entry will increase the asset account. Rent expenses will have a debit entry which implies an increase in the account balance. After subtracting the credit balance from the debit balance, the balance that is left for the business will be $5,000 cash.

Debtors, goods, and rent will have no adjustments since they are single entries. The balances after adjustments in the general ledger will be taken to the trial balance, debit, and credit sides respectively.

Note that balance adjustments in the general ledger usually occur at the end of an accounting period, usually a year, although there are firms that opt for monthly adjustments.

We can now prepare general ledgers for each account involved in the transaction.

| Cash Account: | ||||

| Date | Description | Ref | Debit (Amount in $) | Credit (Amount in $) |

| January 1 | Debtor | 10,000 | ||

| January 9 | Goods purchased | 4,000 | ||

| January 11 | Rent | 1,000 | ||

| Total (adjustment) | 5,000 | 5,000 | ||

| Debtors Account: | ||||

| Date | Description | Ref. | Debit (Amount in $) | Credit (Amount in $) |

| January 1 | Debtor | 10,000 | ||

| Goods Account: | ||||

| Date | Description | Ref. | Debit (Amount in $) | Credit (Amount in $) |

| Cash | 4,000 | |||

| Rent Account: | ||||

| Date | Description | Ref. | Debit (Amount in $) | Credit (Amount in $) |

| January 11 | Cash | 1,000 | ||

In the examples given above, the general ledgers look different, however, general ledgers can be prepared in any form. Examples 1 and 3 were given based on the format explained while in example 2, the general ledgers were prepared in T-account which is common.

Also note that though the general ledgers are created for different sub-accounts, these sub-accounts still represent the different types of general ledger accounts. For example, cash, debtors, and goods accounts are sub-accounts of an asset account, rent account is a sub-account of an expense account, sales account is a sub-account of a revenue account, etc. So in a general ledger, one would see the basic accounts represented by their sub-accounts in the record.

So the ledgers prepared in the examples above still make up the types of general ledger accounts. It is for this reason that the account is referred to as a general ledger account since it summarizes all the transactions of a company with the accounts affected.

See also: Consolidated Statement of Financial Position

Importance of general ledger

- Foundation of financial statements

- Filing of taxes

- Pictures all transactions

Foundation of financial statements

Before a company gets its financial statements, it has to go through the general ledger. Financial statements help a company to track its business’s financial performance and cash flow, they draw on data that has been compiled in the general ledger. The core financial statements that are useful to business owners are the income statement, the balance sheet, and the cash flow statement. So as financial statements matter, the general ledger matters as well.

Filing of taxes

Every business needs to file its taxes, with this, there is a need to refer to the general ledger for the filing of taxes. For instance, if the business is filing Form 1099 for a contractor, there is a need to know the amount of money that was paid to them during the accounting period. In this case, a firm checking its invoices against the general ledger will ensure the correct preparation of Form 1099.

Pictures all transactions

As defined, the general ledger shows the summary of all transactions performed by a firm with the various accounts or sub-accounts affected. With this, a company has a view of all its transactions. In the general ledger, one can see every journal entry that was ever made rather than combing through the bank statements, credit statements, and invoices when looking out for one transaction. So the general ledger can be looked upon to see all accounting records in one place.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.