Revenue is the income a company generates from the sale of goods or the provision of services to clients. Nevertheless, there are situations whereby an individual or a company generated income but doesn’t earn it. Such an unearned revenue example is when a customer pays for a good or service in advance to a company or individual.

This kind of prepayment is an asset to the buyer (the person that pays) which is known as prepaid expenses but to the seller, who receives this payment, it is a liability known as unearned revenue or deferred revenue. In such instances, the company has made revenue from the prepayment made for goods or services that are to be delivered at a later date but hasn’t actually earned it.

In this article, we will discuss unearned revenue examples and the journal entries for these examples.

Related: Is Capital Debit or Credit?

What is unearned revenue?

Unearned revenue is the income a company or an individual receives in advance for a good or service. This prepayment is also known as deferred revenue or prepaid revenue. It can be thought of as the prepayment for goods or services that a company or individual is expected to deliver to the purchaser at a later date. Prepayment for goods or services is a norm for several businesses; they record such income as unearned revenue because they are yet to earn it until they deliver the goods or services that were paid for.

In accounting, unearned revenue is not treated as an asset or revenue as some would think. Rather it is treated as a liability to the seller because it is the money that has been paid to the business in advance before it actually delivers the goods or services to the customer. That is, the business is indebted to the customer and is obligated to deliver the paid goods or service at a later date. Therefore, the seller has a liability that is equal to the revenue earned until the paid good or service is delivered.

A typical unearned revenue example would be prepaid insurance, alongside others such as airline tickets, services contracts paid in advance, rent payments made in advance, annual magazine subscriptions, legal retainer, etc. Such an unearned revenue example can be beneficial to the company in the sense that the early receipt of cash flow can be used for business activities like paying interest on debt and purchasing more inventory. Also, the seller tends to have the cash to perform the required services that have been paid for.

Companies benefit greatly from customers paying in advance to receive their products or services. The cash flow from unearned revenue or deferred revenues can be invested right back into the business to purchase more inventory or pay off debts. However, these companies must ensure they deliver the products that have been paid for to the customers as at when due, in order to keep transactions steady and drive customer retention. This is why it is essential to recognize unearned revenue as a liability (an obligation) and not revenue.

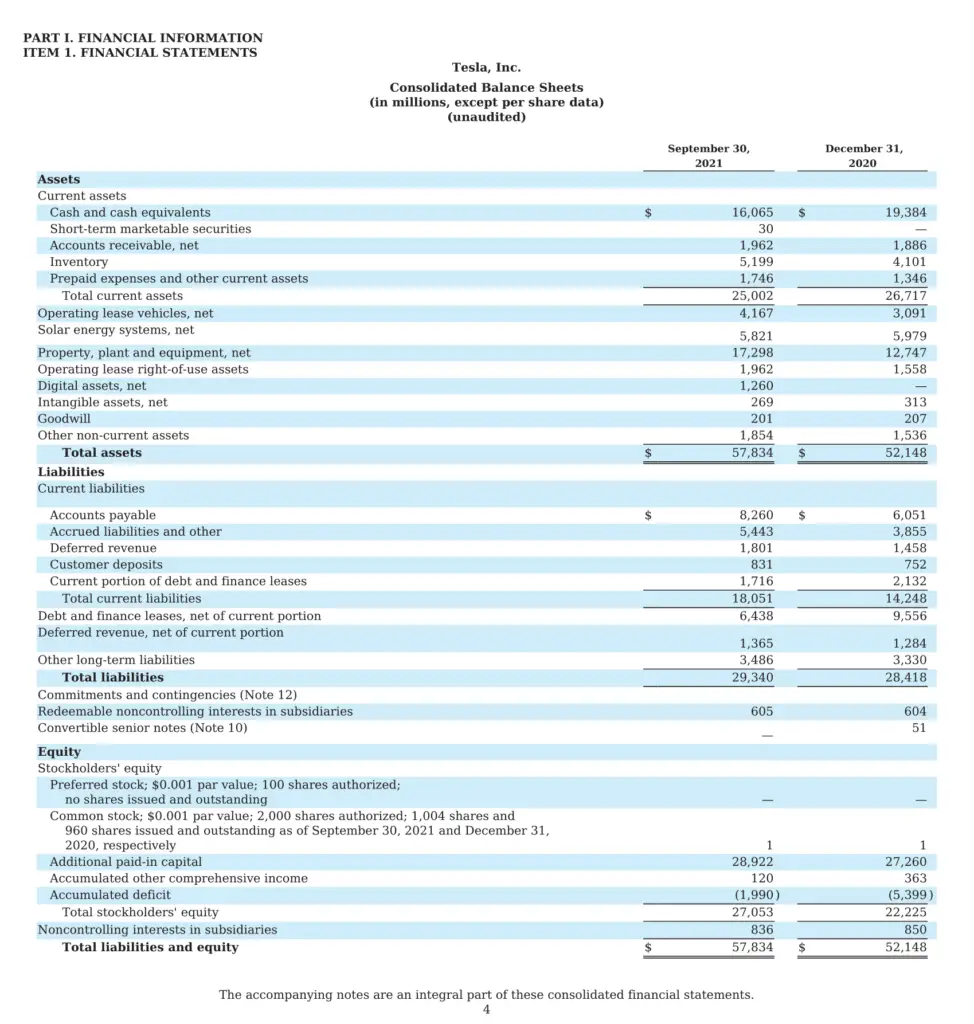

Unearned revenue example in a balance sheet

Unearned revenue or deferred revenue is found in a company’s balance sheet as a current liability. This is because it is thought of as a debt or obligation that is owed to a customer. It is usually recorded under current liabilities because it is expected to be settled within a year. Below is an unearned revenue example in a balance sheet as a current liability:

Source: Tesla

As seen in Tesla’s balance sheet above, deferred revenue (unearned revenue) is listed under liabilities as a current liability. In the balance sheet above it was listed after other current liabilities such as accounts payable and accrued liabilities. It is important to note that unearned revenue will have to remain a liability on the balance sheet until when the distribution or delivery of what the customer paid for has been done. It is when unearned revenue has been earned that it is converted from a current liability on the balance sheet to an actual revenue that is recorded on the income statement.

If unearned revenue is not recorded as a liability and a company records it at once as a revenue, revenues and profits would initially be overstated. Then, for the additional periods in which the revenues and profits should have been recognized, they will be understated. This is also a violation of the matching principle because revenues are being recognized at once, and the related expenses are not being recognized. The accounting matching principles state that revenue and expenses for the same project must be matched.

Hence, unearned revenue is not initially recorded as revenue, but as a current liability until the revenue is earned. However, if the prepayment made for the goods or services is due to be provided 12 months or more after the payment date, unearned revenue will appear as a long-term liability on the balance sheet.

Calculation

When prepayment is made to cover a certain number of months, as time passes and months go by, a certain amount of unearned revenue is earned. That is, the unearned revenue to be earned for a month can be calculated by dividing the amount received for providing goods or rendering services by the number of goods or months of services for which the amount is received.

A typical unearned revenue example to explain this would be professional fees of $12,000 that was received for six months. In order to calculate the unearned revenue that will be earned for a month, the $12,000 unearned revenue is divided by the 6 months, which will give us $2,000. This $2,000 is now what is recognized as the monthly earned revenue over time.

See also: Statement of Cash Flows Examples and Purpose

Unearned revenue examples

- Rent payments made in advance

- Goods paid in advance

- Services contract paid in advance

- Prepaid insurance

- Legal retainers

- Airline tickets

- Prepayment for newspaper or magazine subscriptions

- Annual prepayment for the use of a software

Related: Liabilities vs Assets Differences and Similarities

Unearned revenue examples for different journal entries

Unearned revenue is a liability to the business, so its initial entry would be a credit entry. Since it is an amount that the business owes its customer in terms of prepaid undelivered products or services, a credit entry will be made to the unearned revenue account and a debit entry will be made to the cash or bank account. This journal entry will show that the business has an influx of cash that has been earned on credit.

Later on, when the business has actually provided the goods or services, an adjusting journal entry will be made. The balance of the unearned revenue account will then be reduced with a debit entry and then the balance in the revenue account will be increased with a credit entry.

Let’s look at some unearned revenue examples and their journal entries.

Unearned revenue examples of journal entries for rent payments made in advance

Rent payments made in advance are a common unearned revenue example. An example is a landlord that receives 12 months advance rent from his tenant, which is about $12,000. This $12,000 paid to the landlord is an unearned revenue example that has to be recorded by the landlord in the books as advance rent.

The journal entry for this unearned revenue example will be as follows:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash A/c | $12,000 | |

| To Unearned Rental Income A/c | $12,000 |

The rental income for this $12,000 unearned revenue for each month would be:

$12,000/12 months = $1,000

Therefore, after each month, the landlord earns $1,000 in rental income and records the rental income earned for each month as:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Unearned Rental Income A/c | $1,000 | |

| To Rental Income A/c | $1,000 |

Unearned revenue example 2: Journal entries for services contract paid in advance

Another typical unearned revenue example would be a service contract that has been paid for in advance. Take, for instance, a contractor who received $100,000 for a project, to be executed over ten months. This amount of $100,000 paid to the contractor is an example of unearned revenue because the contractor is yet to complete the job. Hence, the total amount received for the project would be recorded as unearned revenue because the project is yet to be completed.

The journal entry for this would be:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash A/c | $100,000 | |

| To Unearned Contract Income A/c | $100,000 |

The amount that would be recognized as income for the next ten months in the contractor’s books would be:

$100,000 / 10 months = $10,000

The journal entry for this $10,000 recognized as income would be:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Unearned Contract Income A/c | $10,000 | |

| To Contract Income A/c | $10,000 |

Unearned revenue example 3: journal entries for prepayment for newspaper subscriptions

Prepayment for subscriptions, be it software, magazine, or newspaper is a typical unearned revenue example. For example, a publishing company receives $1,200 for a one-year subscription. This amount received is an unearned revenue example and as such would be recorded as an increase in cash and an increase in unearned revenue. The journal entry for this prepayment for newspaper subscriptions would look like this:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Cash A/c | $1,200 | |

| To Unearned Revenue A/c | $1,200 |

If the newspaper is a monthly publication, as each periodical is delivered, the unearned revenue is reduced by the monthly income of $100 (i.e $1,200 unearned revenue / 12 months) while revenue is increased by $100. The journal entry for this $100 earned would look like this:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Unearned Revenue A/c | $100 | |

| To Revenue A/c | $100 |

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.