What are stock options?

Stock options are a type of security that gives investors the right to buy or sell shares of a company at a set price, known as the strike price (grant price or exercise price) before a fixed date known as the expiration date. The strike price is the price at which the option can be exercised. The expiration date determines exactly when an option will expire.

Options can be very valuable and can provide you with an opportunity to make money if the price of the stock goes up. They can also be risky, because if the price of the stock falls below the option price, you may not be able to exercise your option and actually buy shares of the company’s stock. The actual stock that will be bought or sold is referred to as the Underlying Security. For employee stock options, it is an opportunity to acquire shares of the company at a cheaper price.

In this article, we’ll explore the basics of stock options, examples, and types of stock options so that you can better understand them. Let’s start with an understanding of common terminologies used in explaining stock options.

Expiration date

The expiration date of stock options is the date after which the contract between an employer and an employee ends. Most times, stock options’ expiration period can last for as long as 10 years.

The strike price

The strike price is the price at which the stock option can be exercised; hence it is also known as the exercise price or grant price. The holder of an option has the right to buy the security at this strike price. The strike price is determined by taking the current stock price and subtracting any premium paid on the option contract.

Premium

The premium in options is the difference between the stock’s market price and the option’s strike price. It represents the maximum profit for the writer or seller in short-call options or the maximum risk for the buyer in Put options.

Options contract

An option contract refers to the number of shares of the underlying security. In the US stock market, 1 option contract contains 100 shares; that means when you buy “1” AAPL DEC 90 Call at $2.00, you are purchasing a contract that gives you the right to buy 100 shares of AAPL (Apple) at $90 per share. That means you will spend $9,000 on or before the expiration date in December with an additional $2 X 100 = $200 as a premium. We will give more stock options examples in the following sections.

In-the-money options

Whenever the fair market value of stocks is greater than the grant price, the option is referred to as “in the money.” It is an opportunity for profit to the holder of the options.

At-the-money options

Whenever the fair market value of stocks is the same as the grant price, the option is said to be “at the money.”

Underwater options (Out-of-the-money options)

If the market value of stocks is less than the grant price, the option is referred to as “out of the money” or said to be “underwater“.

Styles

- American-style options

- European-style options

There are many styles of issuing stock options: American, European, Bermudan, Asian, etc. Each with its own set of benefits and drawbacks. The most common styles of stock options, the American and European would be discussed below.

American-style options

American-style options allow employees to buy or sell their own shares at any time before the option’s expiration date. They are the most common options styles and are included in many American companies’ compensation plans. American options have more flexibility because they allow the holder to exercise them at any time during the life of the option (that is, before the expiration date). They are often traded on standardized exchanges.

European-style options

European-style options have a fixed expiration date and allow employees to buy only shares that are available at that particular point in time. That means you can only exercise your options on the expiration date. This style of option is mostly traded over the counter (OTC).

See also: Equity stocks: types and list

Stock options explained

There are different types of options in finance; they include:

- Employee stock options (ESO)

- Bond options

- Equity option (stock option)

- Future option

- Index option

- Commodity option

- Currency option

- Swap option

We will not go into other types of options since our discussion is on stock options and how they pertain to employees. A stock option, therefore, is a type of option in which the underlying assets are shares of stocks. Stock options give you the RIGHT to own stocks at a specific price within a certain period of time.

For employees, such rights could be granted to them to motivate them to give in their best to a company; in this case, a stock option granted to an employee is referred to as an employee stock option.

An employee stock option (ESO) does not mean that the employee owns shares or stocks of the company yet. What it means is that the employee now has a right or choice to buy the shares of the company at the stated price within a specific time. If the employee decides to buy the shares at the stated price and at the specified time period; then he or she now owns stocks of the company; this process is known as exercising the stock options.

The employee may decide NOT to buy the stocks as stated in the agreement of the options; in that case, the options expire with no obligation to the employee.

The second type of stock option is the exchange traded stock option. This form of option involves a writer (seller) and a buyer predicting the prices of stock; whoever wins gets the profit. We now talk of PUTs and CALLs in this type of option. Depending on whether the investor bought the stocks with the intention that the price will rise in the future (CALL option) or the investor may predict that the stock price may fall at a specific date in the future (PUT option). If the prediction of the investor becomes true (whether he predicts the price to rise or to fall); as far as the prediction is true, he will make a profit. I will explain more about this later.

Therefore, stock options could be GRANTED to employees (employee stock options) or they could be traded to investors – exchange traded options (CALL options and PUT options).

Types of stock options

- Standard exchange-traded stock options (Call and Put options)

- Employee stock options

Exchange-traded options (listed options)

Exchange-traded options are also called listed options. These are options that are available to investors to buy and sell by predicting whether a stock may fall below the strike price or rise above the strike price at the expiration date.

An important characteristic of exchange-traded options is that they are guaranteed by clearing houses such as Options Clearing Corporation (OCC) and regulated by the securities and exchange commission (SEC). The clearing houses facilitate the transaction of the options to reduce the risk of a company failing to honor the settlement obligations.

Types of exchange-traded options

- Put options

- Call options

Investors can buy and sell these types of stock options with the hope of making a profit but the stocks do not grant ownership or equity. This means buying listed options does not give you equity in the company. Options are simply derivative contracts that can be bought and sold but do not grant equity to the holders. They are important for hedging against market volatility.

PUT options

A put option gives you the right to sell shares of stock at a fixed price before a fixed date. The fixed price is known as the strike price while the fixed date is known as the expiration date. This type of option is useful in hedging against a future fall in the price of the underlying security. If you own shares of a company that you think the market value of the shares may fall before a future date, then you can buy the options that will cover the shares you own and no matter what happens, the maximum amount you may lose will just be the cost of buying the options to be used as a hedge and any associated fees. This way, it reduces the risk of losing the whole underlying security.

If the stock price falls below the strike price during that time period, then the option becomes an in-the-money put option (you make money from a fall in the price of the stocks).

The holder is not obligated to sell the shares when the option expires. If the option is exercised, the buyer immediately sells the shares at the set price. If the option is not exercised, it expires without any consequences and the holder loses only the cost of purchasing the options and any associated fees; but the underlying securities remain intact. An example would clarify all that we have been trying to explain.

Example

Assuming you own 1000 shares of stocks, with each share valued at $10. If you analyzed some market prospect ratios and found out the stocks are overvalued or you think with the economic conditions the stock price may fall to $7 in 6 months’ time; then in order to reduce the risk of losing money on the 1000 shares in your portfolio, you decided to hedge against such risk by buying the options that can cover for your shares.

Let’s say you go ahead to buy PUT options at $1 per option that gives you the right to sell the 1000 shares at a strike price of $10 within 6 months. This type of PUT option covers the underlying security (in this case, it covers the 1,000 shares you own); hence it can also be referred to as a covered option.

If the stock price falls to $7 or lower within 6 months as you predicted, then you can ask the option writer to buy your shares for $10 each. That means your 1,000 shares would still be sold at the initial $10 even with the current fall in prices; the options helped you to hedge against the volatility. The only loss you would get is the cost of buying the options (premium) and associated fees.

The writer of the stock options has to fulfill the order because the clearing houses would ensure the transaction is fulfilled and SEC also monitors and regulates these transactions.

Assuming the 6 months passed and instead of a fall, there was a rise in the stock price beyond $10, then you can simply allow the options to expire (because you are not obligated or forced to sell them); in this case, you still lose just the cost of purchasing the options and the fees for the transaction but your 1,000 shares would still be intact.

Uncovered PUT option

When you buy put options to hedge against a price fall for shares you already own, such options are called covered options. If you decide to buy options without having any existing stocks (or any underlying security), then such options are known as uncovered options.

Uncovered options are mainly used for profits. The following options example shows how uncovered stock options can be profitable.

Uncovered stock option example

Using the preceding example; if the price of the shares falls below or equal to $7, you can then go ahead to exercise your uncovered options by first purchasing the stocks at the strike price and selling them to the writer of the options; while the writer pays you for the stocks at the initial price of $10 per share. That means you will pay $7 X 1,000 shares = $7,000 to purchase the shares while the writer pays you $10 X 1,000 shares = $10,000 for exercising the uncovered options.

Since you purchased the uncovered options at $1 each, it means you spent $1 X 1,000 = $1,000. This amount used for purchasing the options is known as the premium.

In total you spent $1,000 (to buy the options) + $7,000 (to exercise the options) = $8,000 was spent.

While you got $10,000.

Your profit for buying the uncovered PUT options and exercising them when the price actually falls as you predicted would be $10,000 – $8,000 = $2,000.

Even though uncovered options allow you to buy the options without having existing security (such as stocks or bonds); before you exercise the options for profit, you have to buy the underlying security first.

If the share prices increase in value instead of falling, you are under no obligation to exercise the options. You can simply allow the options to expire and you lose the premium (the money used for purchasing the options, in this case, you lose $1,000).

Uncovered put options can be very profitable when the stock market becomes bearish but you can lose the premium as well if your prediction doesn’t come true; the premium represents your maximum risk.

CALL options

A call option gives you the right to buy shares of stock at a fixed price within a specified period of time. Just as with put options, the fixed price is known as the strike price while the date beyond which your options expires is called the expiration date. It means within the agreed timeframe, you are allowed to buy the stocks of the company at an amount that is fixed; market fluctuations do not affect it.

If the stock price rises above the strike price during that time period, the option becomes an “in-the-money” option and can be exercised. If the stock price falls below the strike price during that time period, the option becomes “out-of-the-money” and cannot be exercised.

The option holder has the right to purchase shares of the underlying security at the strike price before the expiration date. If the option is exercised, the buyer immediately purchases the shares at the set price. If the option is not exercised, it expires without any obligation, you will only lose the premium. The premium of options is the amount of money paid to purchase the options; it represents the risk on the underlying security if your prediction doesn’t go as planned.

Call options example

Let us assume you purchased call options to buy 500 shares of stock at a value of $20 per share within 4 months with a $1 premium per share. The strike price in this instance is $20. If the stock price later increases in value to $30 per share within 4 months, it means you can now purchase the stocks at $20.

Your profit would be given by the formula: Current market value of the stock – strike price – premium; in this case, your profit would be $30 – $20 – $1 = $9 per share. For the 500 shares, your total profit is 500 X $9 = $4,500.

If the stock price falls below the strike price (not as you predicted), then you are under no obligation to buy the shares but instead, allow the options to expire. The amount you will lose will be the one used for purchasing the stock options (the premium), in this case, you will lose $500.

See also: What are income stocks? Examples and Types of Income stocks

Employee Stock Options (ESO)

Employee stock options (ESOs) are a type of compensation plan that gives employees the CHOICE to buy shares of the company’s stock at a discounted price before the stock is publicly released. The ESO grant gives employees the opportunity to participate in the company’s future success. This can be valuable for employees as it can help them attain a greater share of the company’s profits.

ESOs are forms of equity derivatives. An equity derivative is a contract between a seller and buyer to buy or sell an asset in the future at an agreed price and date. This gives the employee the opportunity to make an investment in the company. It’s often used as a retention tool for talented employees since it gives them a way to retain ownership of the company even when they leave.

This right is typically granted by the company’s board of directors and can be exercised at any time before its expiration. Options can be granted to current or former employees, partners, or members of the company’s advisory board.

There are two types of ESO grants: performance-based grants and time-based grants. The former allows employees to receive additional shares based on their company’s performance, while the latter provides employees with a fixed number of shares that they receive at specified dates. ESOs often have tax advantages, allowing employees to reduce their tax liability while they hold onto their shares, we will discuss later on taxes for stock options.

Employee stock options are one of the most common forms of compensation that employees receive in the United States.

Other compensation plans for employees may include Restricted Stock Units (RSU), Stock Appreciation Rights (SARs), Phantom Stock, and Employee Stock Purchase Plans.

To better understand ESOs, let us define some financial terminologies, used in describing ESOs.

Stock options vesting

The vesting period of options is the timeframe during which an employee can earn the options; it means you don’t get to own all the options granted to you in the grant letter at once; you rather earn them over a period of time. The intention is to entice and keep you working for the company for as long as possible using the options vesting as bait. The more the number of years, the more the options earned.

The company often sets timelines over a length of time known as the vesting schedule. This gives you the dates and the number of years it will take you to work with the company in order to earn the options. For example, the vesting schedule can show it will take you 4 years of working with the company in order to gain 1,500 options.

Companies often use targets to set vesting schedules; this could be time-based targets, milestone achievements, or a combination of time and milestones.

Milestone-based vesting can give an employee the opportunity to quickly earn options as long as the milestones can be achieved earlier; this gives you control compared to time-based vesting where you have to stay with the company for the required number of years.

For example, a bank may give a marketer (an employee) a target of getting $2 million deposits in order to get 1,000 options. Whenever the marketer achieves this milestone, the 1,000 options are vested (earned). That means if the marketer gets a customer to make this deposit within 2 months, the options are vested immediately; compared to having to work for years to earn the same options for time-based vesting.

Some milestones are based on your performance while others may be based on the company achieving a milestone (it means everyone has to work as a team to earn the options).

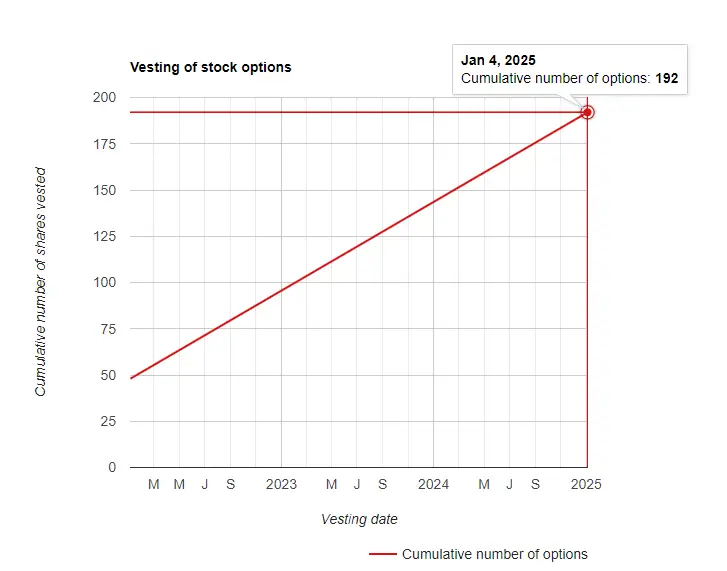

Example

Financial Falconet, Inc. hired Anael on May 1, 2021. As part of the compensation package, Financial Falconet gave Anael an option grant with the following details:

Grant date: 4/1/2021

Options granted: 192

Vesting schedule: Time-based; options would be vested yearly for 4 years.

One year after Anael’s hire date, on May 1, 2022, she reached the vesting cliff and 1/4 of the options (48 shares were vested). That means Anael can decide to exercise the 48 shares vested, but no one will force her to exercise the options. To exercise the shares that were vested, Anael will go ahead and purchase them at the agreed price (if the current stock price is higher than what was agreed, it means Anael would purchase the shares at a lower price). She can also decide to sell the shares for a profit.

If the current stock price is lower than the exercise price (as earlier agreed); Anael may decide not to exercise the 48 options vested and nothing will happen.

The table below shows how the remaining options are vested.

| Vesting Date | Number of options vested | Cumulative options |

|---|---|---|

| 4/1/2022 | 48 | 48 |

| 4/1/2023 | 48 | 96 |

| 4/1/2024 | 48 | 144 |

| 4/1/2025 | 48 | 192 |

Click on the interactive chart above to see how many cumulative options Anael gets over time.

If she decides to quit the company before May 1, 2025; she would forfeit any unvested options, which are then returned to the options pool of the company.

Termination and post-termination exercise (PTE) period

When an employee leaves a company without vesting all the options; he has the right to buy only the vested options (he has the choice to buy the stock options he has earned) only for a limited period of time. The time interval during which an employee is allowed to buy the stock options he has vested is known as the post-termination exercise (PTE) period; this is often 3 months for most companies but some may give a longer time.

Option pool

An option pool is the number of shares of a company set aside by the company for the purpose of compensating employees; it forms part of the authorized shares of a company and therefore can dilute shareholder’s equity. The stock option pool is also known as an equity pool, employee stock ownership plan (ESOP), or employee stock option pool.

Repricing stock options

Repricing of stock options is the changing of the options price whenever the market value of stocks falls below the initial grant price; a company reprices the stock options to allow the employees to exercise options that are underwater at the new grant price. For example, if the initial exercise price (grant price) was $35 but then, market volatility caused a drop in the market value of the company’s stocks to $15; then the company may reprice its stock options to a new grant price of $15. This allows employees to exercise their initial options at this new grant price. Investors may not like this but repricing of stock options is legal.

Employee stock option valuation

A company can determine the value of an option by using the intrinsic value method, which determines the value of the option based on the company’s share price at the time it is granted. For startups or companies that are yet to go public, the grant price can be determined by the recent price of shares at a funding round.

To an employee, you can determine the value of your options by simply finding the difference between the current market price and the strike price.

See also: Float stocks: calculation and formula

Stock options vs RSU

Stock options and Restricted Share Units (RSU) are all forms of employee compensation plans. Restricted stock units are actual shares awarded free to employees when they meet certain conditions. These conditions are the restrictions you must fulfill before being awarded the shares. Some conditions may be meeting a target or milestone or it could be working for the company for a certain number of years. RSU is different from stock options in the sense that options do not grant equity whereas you own equity the moment you earn RSU.

You don’t have to buy shares with RSU, you are actually given the shares for free after meeting the conditions; whereas you still have to exercise your options before you can own the shares of the company.

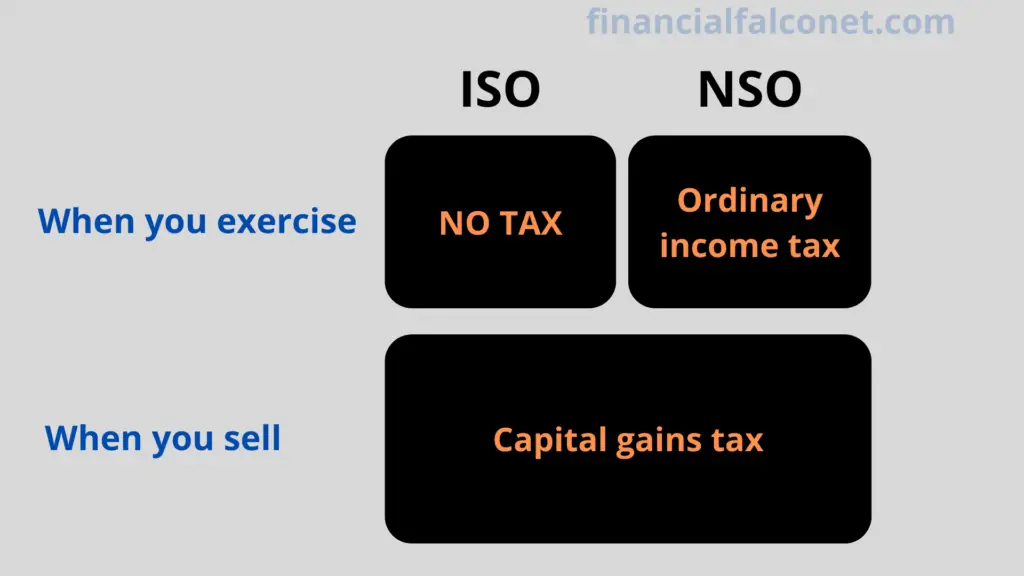

The taxes for stock options are different from RSU; for restricted stock units, you will pay ordinary income tax on the fair market value of the shares granted to you when you acquire them. Whereas you only get to pay taxes when you exercise NSO stock options or when you sell (for both ISO and NSO).

How to exercise stock options

There are various ways through which you can exercise stock options; these include:

- Cash payment: this involves purchasing the options with cash; including the transaction fees and applicable withholding taxes.

- Exercise-and-sell transaction: this involves a brokerage making the transaction on your behalf. You don’t use your cash to pay for the options; instead, the brokerage would exercise the options on your behalf and immediately sell the associated stocks. When the whole transaction is completed, the cost of exercising the options and any associated fees are deducted while you take what remains.

- Exercise-and-sell-to-cover transaction: In this method of exercising options, you purchase the options but only sell the stocks that would cover the cost of exercising the options; the remaining shares or stocks are held as equity. This only occurs in companies that have gone public.

If your company allows early exercising of options; it comes with some benefits as outlined below together with some disadvantages.

Benefits of early exercising

- You will get tax benefits for ISOs: you can qualify for ISO tax benefits by early exercising such as holding your shares for at least 2 years after the stock option grant or 1 year after exercising.

- Early exercising of stock options ensures you start holding earlier, making any income from the sale of the stocks to be taxed as a long-term capital gains tax.

- Exercising early reduces the spread and therefore reduces the amount of tax that would have been paid; because you are buying the stocks at almost their fair market value.

Disadvantages

You have to use cash for early exercising of options, other methods of payments are not allowed. Again, there is no guarantee that the stock price may increase in the future, and therefore, you may lose your money by exercising early.

Stock options vs shares

Stock options are a type of security that gives the holder the right, but not the obligation, to purchase shares of stock at a set price within a certain time period. Options are a CHOICE granted to an employee to buy shares of the company within a period of time and at a fixed price. Shares of stock grant ownership or equity in a company. Stock options may give you equity only when you exercised them, that is, you are given stocks when you exercise your options.

Another difference between shares and stock options is that there is no expiration date for shares but options can expire. Depending on the type of stocks, some can earn dividends (income stocks) which can be a source of income.

Trading options

Stock options are a form of derivative security. They give the owner the right, but not the obligation, to buy or sell shares of a company at a set price on or before a certain date. Options can be traded on exchanges like the New York Stock Exchange (NYSE) and Nasdaq, or they can be bought and sold privately between investors (over the counter).

For ESOs, they can be publicly traded in exchanges for companies that have gone public but private companies and startups can also design their stock plans using their own prices. The grant price for private companies is often determined by the recent price of shares at a funding round.

See also: Stocks vs Real estate: which is a better investment?

Taxes for stock options

There are two types of taxes for stock options: ordinary income tax and capital gains tax. You can get tax benefits for some stock options. How you get taxed, depends on the type of option and also on how you exercise them. The timing for exercising options and selling also matters as we would see below.

How stock options are taxed

When you exercise NSO options, the difference between your exercise price and the current stock price would be taxed as ordinary income. This is not taxed for ISO options; that means you get a tax benefit when you exercise ISO options.

To get tax benefits for ISO options when you exercise, the shares must be held for more than 2 years from the date you were granted the options or 1 year from the date you exercise the options. That means you are not taxed when you fulfill the criteria mentioned. But when you sell the stocks, the income is taxed at the long-term capital gains tax rate (which is lower than regular income tax rates).

If you decide to sell your stocks that were exercised, the difference between the current stock price and the exercise price would be taxed as capital gains. Capital gains tax is applicable to both ISO and NSO stock options. This is because you now have ownership of the stocks when options are exercised; therefore selling them is like selling assets, of which any profit made from selling assets would be taxed as a capital gain.

The capital gains tax rate for most assets held for more than a year is about 0% to 20% while that of the ordinary income tax rate of about 10% to 37%; depending on the income bracket. That shows the tax rate for capital gains is lower than the rate of ordinary income. It shows you get more tax benefits when you optimize for capital gains.

This means you can benefit from lower tax liabilities by maximizing long-term capital gains tax treatment; the lower the difference between your exercise price and the stock price when you exercise your options, the more the tax benefit you get from capital gains tax treatment. When you exercised stock options and sell the shares within a year, the income is taxed as a short-term capital gain (of which the tax rate is higher than the long-term capital gains tax rate).

Disqualifying disposition of ISO

When you sell the stocks from the exercise of your ISO options the same year they were exercised, it means you have disqualified the ISO. Any income generated from the sale would be taxed as regular income tax for that year. The tax in this case would be calculated based on the lesser of the spread; that is, the difference between the exercise price and the stock price of the shares at the time of exercise or disposition.

Example 1: disqualifying disposition of ISO when the stock price is lower than the strike price

For example, if the exercise price is $5 and the stock price at the time the options were exercised is $25, then the difference (the spread) is $25 – $5 = $20. Assuming 1,000 ISO shares were exercised and then later disqualified at the time when the stock price has fallen to $15. This means the amount of income that would be taxed at the regular income tax rate would be ($15 – $5) X 1,000 = $10,000.

Example 2: disqualifying disposition of ISO when the stock price is higher than the strike price

Assuming you disqualify when the stock price is $35, it means the lower exercise price of $25 would be used to calculate your income tax. That means the income that would be charged will be $25 – $5 = $20 X 1,000 = $20,000. The remaining income from the excess $10 per share would be treated as capital gains. When you hold it for less than a year, it would be taxed as a short-term capital gain, and when you hold it for more than a year, it would be taxed as a long-term capital gain.

A disqualifying disposition ISO below the market value at the time the options were exercised would cause you to lose the capital invested with no ordinary income tax.

Disqualifying disposition of ISO and Alternative minimum tax (AMT)

When you disqualify in the same year that you exercised your options, AMT would not be an issue; but when you disqualify after 1 year of exercising your options, then you have to pay 2 taxes: one for AMT in the year you exercise your options and another tax for ordinary income tax in the year you disqualified the ISO shares.

What happens when the stock price falls below the exercise price?

In this case, you will have to pay the tax when the stock options were exercised and you lose the money used for exercising the options.

Related: What are large-cap stocks?

Alternative minimum tax (AMT) for ISO stock options

The alternative minimum tax (AMT) is a system of taxation that ensures everyone pays the right amount of income tax, especially high-income earners. Usually, there is an AMT amount below which you are not taxed, but above which you will be taxed.

When you earn more than the AMT amount, you have to calculate the tax for your ordinary income and also for AMT; the higher amount would be paid as tax.

For incentive stock options, if you exercise and sell the options within 1 year the AMT is not applicable to your income. But if you exercise ISO and hold them for more than 1 year before selling the stocks, you have to calculate the AMT amount and then compare it with your income from the sale of the stocks. Whichever is higher would be taxed as ordinary income. The stock options value is determined by subtracting the strike price from the current stock price or simply the difference between the two.

Example

Assuming you were granted 600 ISO stock options at $2 and then exercise the options, 2 months after they were granted; 14 months after you exercise your ISO options, the stock price is now worth $12 and you sold them.

From the example above, the stock option value would be (stock price – strike price) = 12 – 2 = $10

When multiplied by the number of options exercised, we have 10 X 600 = $6,000.

The $6,000 would be added to your ordinary income and used for calculating the AMT. One thing to note is that if the current market value of stocks is higher than the strike price (exercise price), then the difference would be taxed as ordinary income; irrespective of whether you sell the stocks or not. Holding the stocks without selling them may continue to accumulate more taxes and increase your tax liability; it becomes worst when the stock price falls. This shows early exercising of stock options may increase your tax liability.

Companies need to file the IRS Form 3921 whenever any employee exercises an incentive stock option.

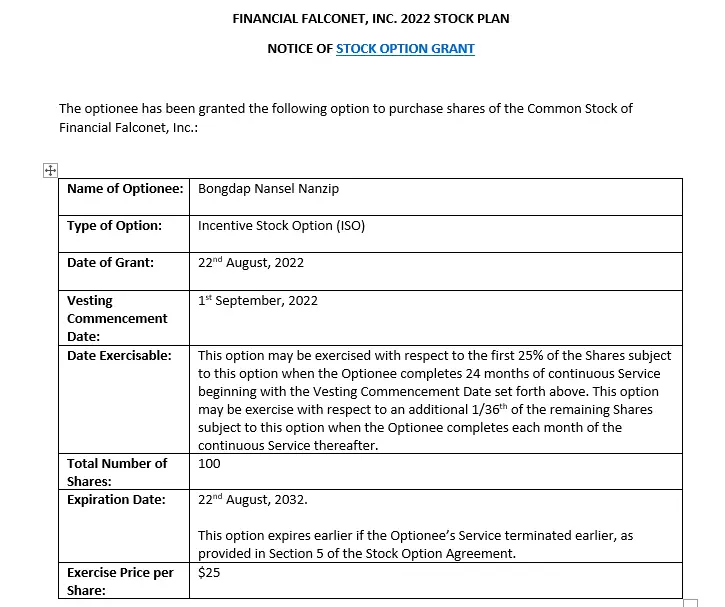

Stock options grant letter

A stock option grant is a letter or document that shows you the details of your options as an employee. It outlines the number of options awarded, the type of options awarded, the grant date, expiration date, and the vesting commencement date.

You can download the template of the stock options grant here:

While defining stock options, we stated that they give you the right to buy (but you are not obligated to buy); this means no one will force you to buy the shares of the company even after signing the stock option grant.

What do stock option grants contain?

Contained in the stock option grants are the type of stock options, the number of shares granted, the grant price, expiration date, and vesting schedule. Above is the template of a stock option grant.

Should I accept a stock option grant?

Yes, accept the stock option grant offered to you; it is not compulsory to exercise your options. Accepting it is just to give you the opportunity to exercise the option; who knows, you may want to purchase the shares one day and you can sell the purchased shares for profit in the future or simply hold on to the stocks to gain equity in the company; especially when the company has a prospect for growth.

See also: Overvalued and Undervalue Stocks

Stock option agreement

The stock option agreement is the document that serves as the contract between you and your employer stating the terms and conditions of your stock option grant. You have to sign and agree to the terms before your options become start vesting. The employee in a stock option agreement is known as the grantee or optionee; while the employer is known as the grantor.

Options agreements include information such as the option grant number, the exercise price, and the expiration date. The terms of an option agreement can also include restrictions on how and when the options can be exercised.

The most important part of a stock option agreement is the vesting schedule. This tells us how long it takes for the option to become effective. For example, if an option has a three-year vesting schedule, it means that the employee will have to work with the company for three years before they can start exercising them.

FAQs

Are stock options the same as shares?

No, stock options are rights granted to an employee to buy shares of the company at a specific price within a specific time; the employee has the choice not to buy the shares. The employee can own the stocks only when he/she goes ahead to purchase the shares as agreed in the contract of the stock options.

Can stock options be granted to an entity?

Under the Securities Act Rule 701, you cannot grant stock options to an entity but only natural persons (individuals) such as employees, investors, or consultants acting as persons and not as entities or organizations.

Stock options and startups

In most cases, startup companies issue stock options in order to attract and retain talented employees. Stock options are an important part of compensation packages for executives and other key employees.

When issuing stock options, startup companies must adhere to various securities regulations. Stock options must be granted pursuant to an offering statement that is filed with the SEC. In addition, stock option grants must be consistent with applicable law, including anti-takeover provisions. Finally, startup companies must provide holders of stock options with appropriate notice regarding the terms and conditions of their options.

What is the benefit of stock options?

Stock options are a type of compensation that give employees the right to buy or sell stock at a set price before or after the option expires. They can provide an incentive to sellers and buyers and help companies maintain control over their employees.

Options also allow startup employees to buy the stocks at a set price before they become publicly traded, usually, weeks or months before the stocks are available to the general public. This creates a sense of exclusivity and gives employees a chance to invest early in a company’s success.

Why are they important?

Options are important because they give you flexibility in how and when you buy shares. For example, if you’re waiting for the right moment to buy shares in a company, using stock options can help you do so at a lower cost. Stock options also provide opportunities for growth – by exercising them early, you can potentially increase your shareholding in the long run. Again, having part of the company can motivate employees to become very productive as they see the company as theirs.

Are options better than stock?

Options are not better than stocks because their values are dependent on stocks or other underlying securities. An option is a derivative whose value comes from the value of another security such as stocks, bonds, etc. An option in itself is worthless unless it is exercised in order to have shares of stocks.

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.