What type of account is cost of goods sold? The cost of goods sold (COGS) is a listed item on the income statement that includes the cost of the materials and labor that are directly used to create the company’s goods. It is not considered to be an asset or liability on the financial statements but rather recorded as an expense. In this article, we will discuss the cost of goods sold and the type of account it is on the income statement.

Related: What type of Account is Sales Discounts?

What is cost of goods sold?

Cost of goods sold (COGS) also known as cost of sales is the direct cost of producing the goods that are sold by a company which excludes indirect expenses, such as sales force costs and distribution costs.COGS counts as a business expense and therefore affects how much profit a company makes on its goods.

The COGS is seen on a company’s income statement (one of the top financial reports in accounting) which reports the company’s income for a certain accounting period (quarter, month or year). An income statement is also referred to as a profit and loss statement (P&L). On this financial statement, the cost of goods sold is usually found directly below ‘Revenue’, ‘Sales’, or ‘Income’ depending on which of these line items the company uses to represent their income. It usually appears as a second line item right after the sales revenue on the income statement.

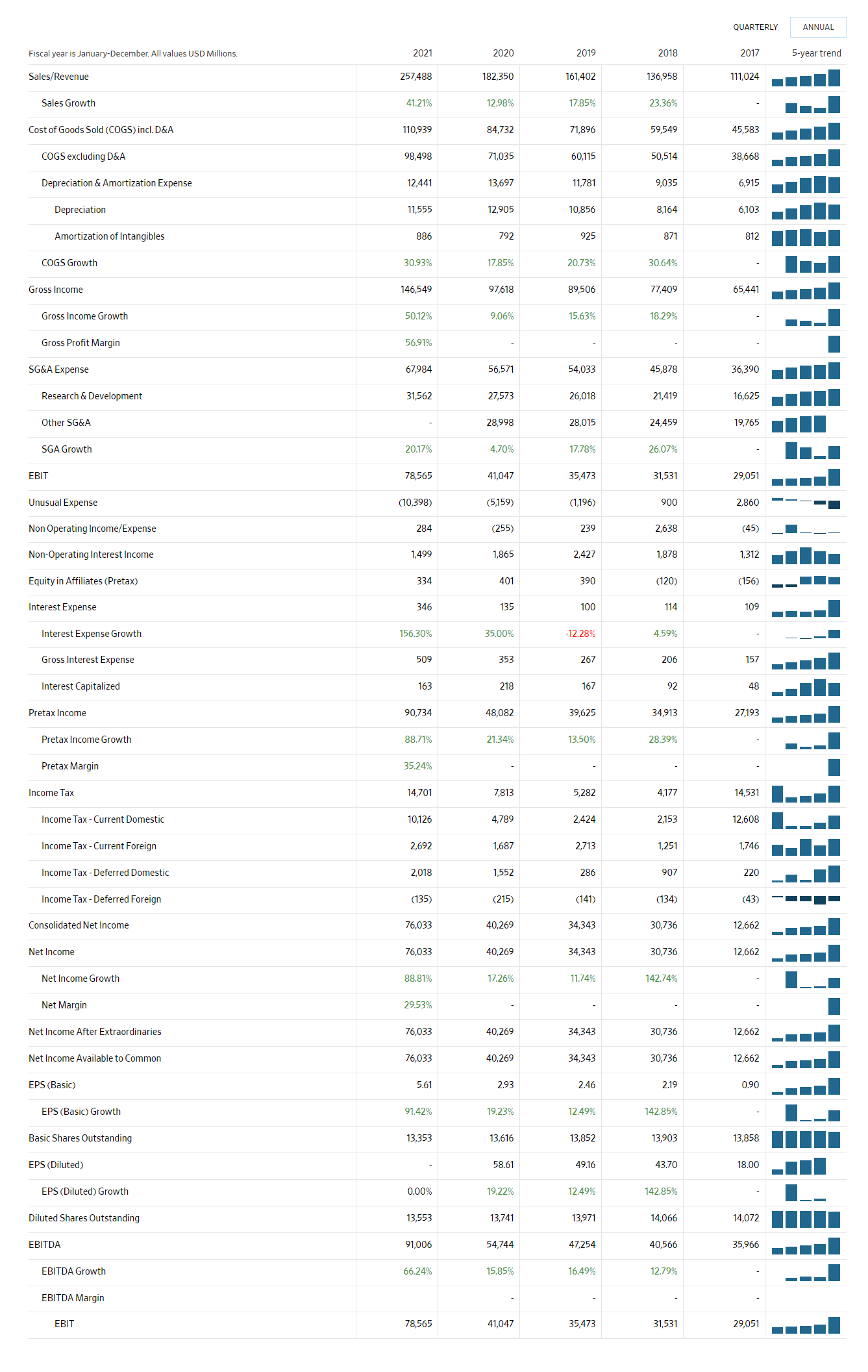

For instance, the image below is an income statement from Google. We can see that the listed item- the cost of goods sold comes beneath the top line figure “Sales/Revenue“

The COGS is the cost of manufacturing the goods and products or services that a company sells or renders during a period. It only entails the costs that are directly tied to the production of the products, which includes the cost of material, labor, and allocated overhead cost; with indirect costs like distribution and sales expenses being excluded. The costs of the goods that have been produced but not yet sold are deferred as costs of inventory until the inventory is sold or written down in value.

For example, the COGS by an automaker would include the cost of materials for the parts that are used in the making of the car plus the costs of labor used to put the car together. This means that the cost of sending the cars to dealers and the cost of labor used to sell the car are not included in the COGS. Moreso, when calculating the COGS, the costs that are incurred on the cars that were not sold during the year will not be included regardless of whether the costs are direct or indirect. Hence, the COGS only includes the direct cost of producing goods that were purchased by the customers during the year.

The expense items that make up the Cost of goods sold include:

- The cost of raw materials

- Cost of parts used to make a product

- Container costs

- Direct labor costs including associated costs such as payroll taxes and benefits

- Supplies used in either making or selling the product

- Cost of items intended for resale

- Overhead costs such as utilities for the manufacturing plant or site

The COGS is actually a tax reporting requirement. According to the Internal Revenue Service, the companies that produce and sell products or buy and resell goods have to calculate the cost of goods sold to write off the expense. This would decrease the total amount of taxes they need to pay. In order to calculate the COGS, the business needs to figure out the value of its inventory at the beginning and end of every tax year.

The end-of-year inventory value is subtracted from the beginning of the year’s inventory value when calculating COGS. A higher COGS means a company pays less tax, and can also mean a company makes less profit. Hence, in order to increase profit, the COGS should be minimized.

Calculating COGS

In accounting, the cost of goods sold is a calculation of all the direct costs incurred on the production of goods manufactured and sold within a certain time period. It doesn’t include indirect costs like sales expenses and distribution and the figure of COGS only includes the costs for the goods sold during the period and not the finished goods that are not yet sold. Therefore, the formula for calculating COGS is expressed as:

COGS = Beginning Inventory + Purchases during the period – Ending Inventory

As seen in the formula above, inventory is an important item in the calculation of COGS. The inventory consists of the raw materials and work-in-process as well as the finished products and merchandise awaiting sale. The unsold inventory from the previous year is considered the beginning inventory used in the formula while any unsold inventory at the end of the year is considered the ending inventory. In order to calculate the COGS, the purchases made throughout the year are added to the beginning inventory, and the ending inventory is subtracted from the total of the beginning inventory and purchases.

For example, assume, the beginning inventory of a company is $3,000, and then the company purchase $1200 worth of supplies during the period and the ending inventory is $1000. The calculation for the COGS would be:

COGS = $3,000 + $1200 – $1000 = $3,200

i.e the cost of goods sold would be $3,200

See also: Accumulated depreciation is what type of account?

What type of account is cost of goods sold?

Because the cost of goods sold is the direct cost of producing the goods that are sold by a company, it is recorded on the company’s income statement as an expense account. The income statement (profit and loss statement) lists the income, expenditure, profit and losses of a company over a period of time. That is, it is a financial statement for only revenue and expenses, and as such does not contain other accounts like assets, liabilities and equity. These other accounts are found on the company’s balance sheet.

The cost of goods sold is not listed on the balance sheet because it is not an asset (an item that the business owns), a liability (what a business owes), or equity (represents ownership of a company’s shares in proportion); rather it is found on the income statement. On the income statement, the cost of goods sold is not listed as a revenue account but as a type of expense account. Expense is one of the main five accounts in accounting; the others are assets, liabilities, revenue and equity. An expense account in accounting contains the cost of doing business.

Examples of expense accounts that can be seen on an income statement include Cost of Goods Sold, Costs of Sales, Finance Expenses, Operating expenses, Costs of services, Non-operating expenses, Prepaid expenses, Accrued expenses, etc. An expense account on the income statement records either all the increases in liabilities from delivering goods or services to customers or the decreases in the owners’ equity that occur from using assets. Therefore, in a journal entry, any expenses will be recorded as a debit to the expense account and as a credit to the asset or liability account.

‘Cost of goods sold’ as an expense account

The cost of goods sold is a type of expense account and therefore has a debit entry. As an expense account, a debit increases a COGS account and a credit decreases it. When making a journal entry, the cost of goods sold account is debited and the inventory and purchases account (which are asset accounts) are credited. This journal entry shows that these assets have been sold and their costs have been moved to the cost of goods sold account.

Expenses have a debit balance because they cause the owner’s equity to decrease. A debit entry will either cause an increase in an asset or expense account or a decreases in a liability or equity account; whereas a credit entry will either cause an increase in a liability or equity account or a decrease in an asset or expense account. At the end of the accounting year, the debit balances in the expense account are usually closed and transferred to the owner’s capital account, or Retained Earnings (which is a stockholders’ equity), thereby reducing equity.

Therefore, the cost of goods sold as an expense account on the income statement increases by debits and decreases by credits. In the journal entry for this type of expense, one account (COGS) is debited, and one or more other accounts (purchases and inventory accounts) are credited. Also, in order to balance the entry, the credits to purchases and inventory must equal the debit to COGS. Hence, the journal entry for the cost of goods sold should equal purchases plus inventory. This gives us the formula for COGS:

COGS = Beginning inventory + Purchases during the period – Ending inventory

In order to record the figure for the cost of goods sold account, one must collect the purchased inventory costs, beginning inventory balance, and ending inventory count. These pieces of information are used to calculate the COGS. After that, a journal entry is created for the COGS as a debit entry. That is, when adding a COGS journal entry, the COGS Expense account is debited and the Purchases and Inventory accounts are credited.

Therefore, when materials are purchased for the production of goods, the Purchases account is credited to record the amount spent, the COGS Expense account is debited to show an increase, and then the Inventory account is credited to increase it.

Below is how the journal entry of the Cost of goods sold for materials purchased would look like:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| 01/01/2022 | Cost of Goods Sold Expense | Materials purchased | AAAA | |

| Purchases | BBBB | |||

| Inventory | CCCC |

Related: Is Sales Discount Debit or Credit?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.