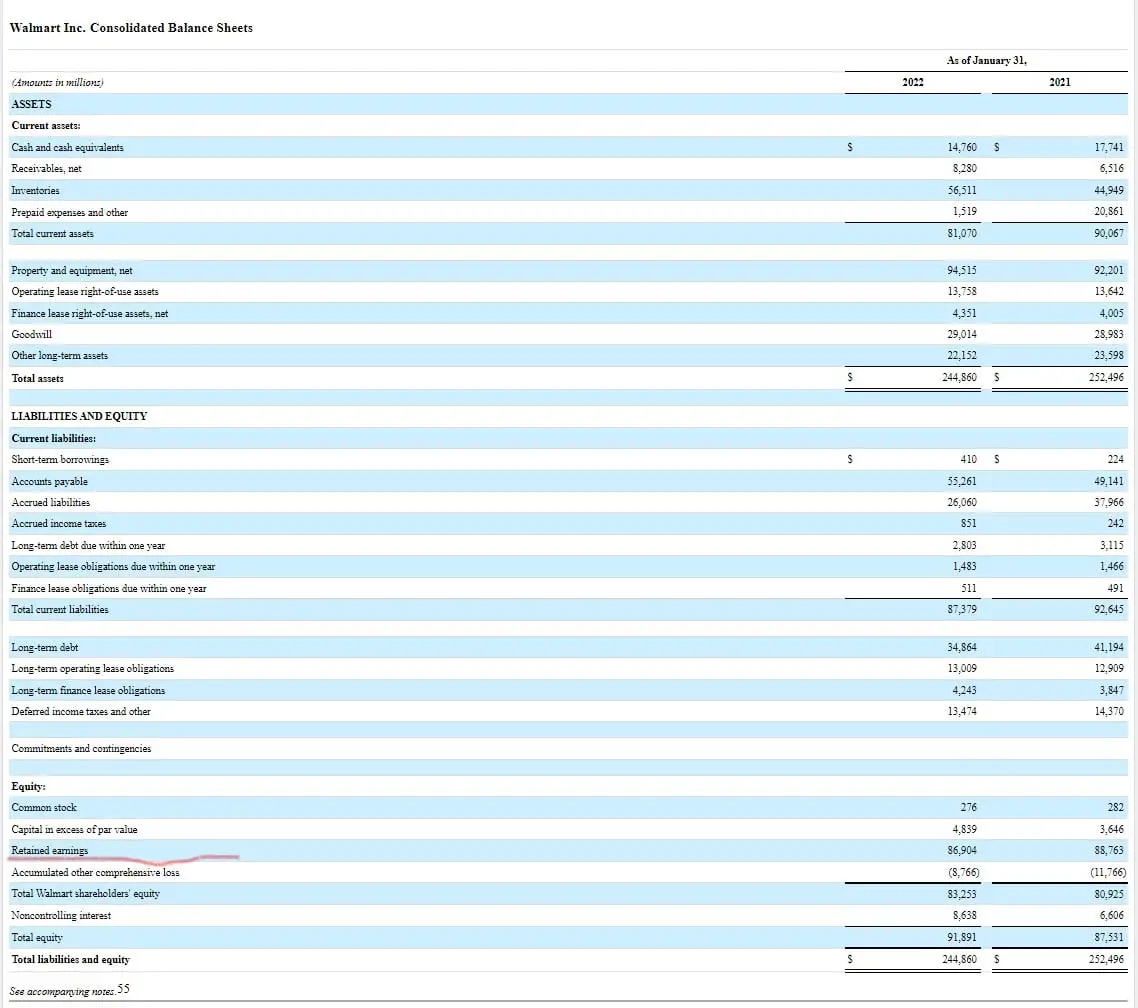

What type of account is retained earnings? Retained earnings (RE) are reported on the balance sheet of companies while the changes are reported on the statement of retained earnings. They represent the portion of a company’s profits that have been reserved for reinvestment back into the company.

Profits give company management the ability to plan the use of such earnings effectively, mainly for the payment of dividends to shareholders. The portion of the profits that are not declared as distributions are held back and constitute the company’s retained earnings. The retained earnings are mainly used as working capital, for the settlement of debt, or for purchasing assets.

The decision to distribute the profits made by a company in each accounting period is normally made by its management team although the company shareholders can challenge their decision through a majority vote against retaining the earnings. Shareholders mainly want distributions to be declared in order to get a return on their investment in the company through the dividend that they will receive in the short term. However, the company management may have a reinvestment plan that they perceive will yield substantial returns in the future and thus, prefer to increase the company’s retained earnings account balance in order to be able to reinvest. They may also prefer to pay up high-interest rate debt instead of declaring distributions.

When such a disparity occurs between the company management and its shareholders, a compromise is reached; with the company’s management declaring a nominal amount as dividends to shareholders while retaining a larger portion of the profits for future use. In the long run, the reinvestment of such retained earnings often results in a higher dividend payment to shareholders. Here, our discussion shall be on understanding what type of account retained earnings are.

See also: Supplies expense is what type of account?

What are retained earnings?

Retained earnings (RE) are the difference between the profits a company has made in an accounting period and the amount spent as distributions to the company’s shareholders. The amount a company has as retained earnings is usually reported in its balance sheet along with other assets, liabilities, and equity of the company. Retained earnings are also referred to as earnings surplus.

Retained earnings are the portion of profit left over after payments of dividends to the holders of preferred and common stock of the company. It is gotten by subtracting the dividends and all other distributions that will be made to investors from the company’s profits within the accounting period in view. The retained earnings account gets affected whenever there is an increase in revenue or new purchases are made by the company.

Growing companies and companies focused on business expansions and other reinvestments generally usually avoid paying dividends to their common stockholders. They do this to increase their retained earnings which in turn, increases their working capital and the funds available for research and development of new products or services, acquisition of other companies, purchases of new assets, marketing, and repayment of debt. Additionally, some companies elect against paying dividends and grow their retained earnings to save as a fallback in case of future losses or have available funds instead of taking out loans from the bank or issuing more shares that could lead to share dilution.

As these companies mature, exceed their retained earnings goals, or implement strategies that reduce their cash outflows and increase cash inflows, they may elect to start dividend payouts to their common shareholders. When a company experiences continued losses or have distributed more dividends than its retained earnings can cater for, it will result in having a negative retained earnings balance. The negative retained earnings account balance is known as the accumulated deficit.

Uses of retained earnings

- For share buybacks

- It can be distributed fully or partially to shareholders as dividends.

- It can be used to expand business operations like increasing its products and services or opening new branches.

- Used in diversifying the business operation

- For partnerships, mergers, and acquisitions in order to improve the company.

- It can be used for debt repayment.

- Retained earnings are commonly used for the purchase of tangible and intangible assets.

Factors affecting retained earnings account

- Business sector

- Age of company

- Profits

- Dividend policy

Generally, a large retained earnings account balance implies that a company is financially healthy while a small retained earnings account balance indicates that the company spends most of its profits on dividend payments or immediate reinvestment back into the company. However, in order to evaluate a company’s retained earnings account balance accurately, these points listed above should be put into consideration. We shall discuss each of them below:

Business sector

When the business sector in which a company operates is one that is highly seasonal, its retained earnings are likely to be high at their peak season and drop low out of season. companies in such sectors must ensure they build a considerable amount of retained earnings during their peak seasons in order to be able to stay in business through the low season and survive until another peak period comes by.

One way that such businesses could maintain a steady retained earnings level is by diversifying their business to include aspects that can cater to their operations and other expenses during downturns. For instance, companies that produce lawnmowers are likely to have more sales during spring and little or no sales in fall. In order to prepare for this downturn, they could include a business division that sells sweepers; by so doing, they have products to sell both in spring and fall.

Age of company

Generally, the older a company the more likely it is to have a large retained earnings balance. This is so because they have had the advantage of time; which must have enabled them to accumulate more retained earnings compared to newer companies. Additionally, new companies might even have an accumulated deficit since the starting years of companies are generally turbulent as they try to build up their client base and become profitable.

Profits

Companies that are highly profitable are more likely to have a large retained earnings balance. This is because even if they pay dividends, they are likely to still have a considerable sum that can be retained for future use. Conversely, companies that are not as profitable might have a lower retained earnings balance even if they do not pay dividends to their shareholders.

Dividend policy

Another factor that can affect a company’s retained earnings is its dividend policy. Irrespective of the company’s profitability, if it pays out dividends consistently, its retained earnings will be lower than a company within the same profitability range that does not pay dividends.

See also: Is accounts receivable a current asset?

What type of account is retained earnings?

Retained earnings are the cumulative profits of a company after dividend payments are subtracted. The retained earnings of a company are reported in its balance sheet along with share capital and paid in capital under the equity section. Hence retained earnings are an equity account.

The retained earnings account shows that this amount was held back or retained in the company for future use. As a result, a company’s retained earnings decrease when it experiences losses or pays dividends and increase when profits are held back. When retained earnings are expressed as a percentage of a company’s total earnings, it is referred to as the retention ratio and is equal to one minus the dividend payout ratio.

Retained earnings are an equity account on the company’s balance sheet and although they are not assets in themselves, they could be used for the purchase of assets such as equipment, inventory, real estate, and other kinds of investments. Hence companies with a large retained earnings balance will be better positioned to declare higher dividends, make investments or purchase new assets.

Even though retained earnings alone cannot be used to accurately ascertain the financial well-being of a company, companies with negative retained earnings are mostly considered to have poor financial health as it indicates that they have been experiencing more losses than profits over their operating years. Conversely, companies with high retained earnings are considered financially stable since it suggests that they have made considerable profits and were able to retain more than they spent.

Conclusion

What type of account is retained earnings? Retained earnings is an equity account that represents the amount leftover from a company’s profits after paying dividends to its shareholders. Most companies that are growth-focused may however choose not to declare dividends and use their profits for other business operations such as research and development on new products and services, expansion to new territories, increasing their marketing, debt repayment, etc.

Retained earnings accumulate from year to year as companies hold back a portion of their profits, thus older companies tend to have a higher retained earnings balance than younger companies within the same industry. Retained earnings are an important variable for assessing how much of a company’s profits it was able to save over time thereby indirectly showing how much it can declare as distributions or use for reinvestment purposes in the future.

See also: Notes receivable debit or credit?

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.