The debt to capital ratio formula compares the total debt of the company to its total capital; therefore, it is used in the calculation of the financial leverage, stability, and solvency of the company. The ratio compares the overall financial obligations of a company to its total capital and is instrumental in giving a picture of the company’s overall financial health. For instance, a company may appear to have a very high debt load in raw numbers, but if the debt load is compared to the company’s overall capital, the resulting ratio may be well within the bounds of acceptable risk.

This article will discuss the debt-to-capital ratio formula and interpretation. But first, let’s look at what the ratio is and how it is used.

What is debt to capital ratio?

The debt to capital ratio (D/C) is a financial metric that is used to measure the financial leverage of a company by dividing the interest-bearing debt, and short- and long-term liabilities of the company by its total capital.

This simply means that the debt to capital ratio of a company is the ratio of its total debt to its total capital (i.e interest-bearing debt plus shareholders’ equity, which may include items such as preferred stock, common stock, minority interest, and net debt). The D/C ratio is used to measure a company’s financial solvency, capital structure, and degree of leverage, at a particular point in time. This ratio measures the total debt of a company as a percentage of the company’s total capital which is expressed as the debt to capital ratio percentage.

Companies can finance their operational activities using either debt or equity. Hence, the debt capital ratio gives the user an insight into the financial structure of the company or provides an idea of how the company is financing its operations, together with its financial strength. However, there are many variations of the debt to capital ratio because it is a non-GAAP measure (GAAP means Generally Accepted Accounting Principles). For the debt capital ratio calculation, practitioners make use of different definitions of debt in the equation such as:

- All liabilities, including accounts payable and deferred income

- Any interest-bearing liability to qualify

- Long-term debt and its associated currently due portion (measures capital structure)

Therefore, it is very crucial to pay close attention when reading what is or is not included in the debt capital ratio on the financial statements of a company. Companies tend to even alter their debt to capital ratio by issuing additional debt, retiring debt, issuing more shares, or buying back shares.

Interpretation

The debt to capital ratio interpretation help to give investors and analysts a better idea of the financial structure of a company and whether or not the company is a suitable investment. Carrying out debt to capital ratio analysis tells investors whether a company is more prone to using equity financing or debt financing.

Debt to capital ratio analysis resulting in a numeral that is greater than 1 would indicate that the company has more debt than capital. This means the company is extremely risky. Therefore, the company is likely to go bankrupt if any more liabilities are acquired without an increase in earnings.

On the other hand, debt to capital ratio that is less than 1, would indicate that the debt levels of the company are manageable. This means the company is considered less risky to invest in or loan to given other factors are taken into consideration.

Furthermore, whether a company’s debt to capital ratio is high or low would depend on the average debt to capital ratio by industry.

High debt to capital ratio

A debt capital ratio that is greater than 1 or a debt capital ratio percentage greater than 100% is considered high. The higher the debt to capital ratio of a company, the more debt it has compared to its equity, thus, the riskier the company. A company that has a high debt to capital ratio compared to the debt to capital ratio industry average may exhibit weak financial strength. This is because the cost of the company’s debts may weigh on it and increase its default risk.

A high debt to capital ratio interpretation simply means the company is funded more by debt than equity, indicating a higher liability to repay the debt and a greater risk of forfeiture on the loan if the debt cannot be paid in due time.

Nevertheless, even though a specific amount of debt may cripple one company, the same amount of debt could barely affect another company. Therefore, using total capital in the debt calculation gives a more accurate picture of the company’s health as it frames debt as a percentage of capital instead of a dollar amount of debt.

Low debt-to-capital ratio

A debt capital ratio that is lower than 1 or a debt capital ratio percentage lower than 100% is considered low. The lower the debt to capital ratio of a company, the less debt it has compared to its equity. A low debt to capital ratio interpretation simply means the company’s capital is funded through equity capital. Therefore, the company would have greater flexibility in terms of raising additional capital through debt. This is why management tries to maintain a healthy capital structure that does not risk the solvency of the company.

What is a good debt to capital ratio?

A good debt to capital ratio would depend on the average debt to capital ratio by industry. However, a ratio of less than 1 is considered an ideal debt to capital ratio because the higher the ratio, the greater the risk to lenders and shareholders.

Nevertheless, a high debt-to-capital ratio percentage may not always mean a bad thing. For instance, utility companies usually carry high levels of debt due to the fact that their operations are capital intensive. Therefore, such companies would have high debt-to-capital ratios. This doesn’t mean the companies will be insolvent soon as utility companies have an extremely steady base of customers, so, they have consistent revenues. Therefore, these companies are able to meet their obligations without worrying about downturns in revenues.

Conversely, a high debt-to-capital ratio for new, expanding companies would indicate risk compared to the case of the utility companies. These companies may not have established customer bases, but still, need to finance their daily operational activities.

More so, even though they have steady sales at the moment, it’s not a guarantee like with the utility companies. Therefore, the sales of these new companies could level off or likely decrease leaving fewer funds to service their debt.

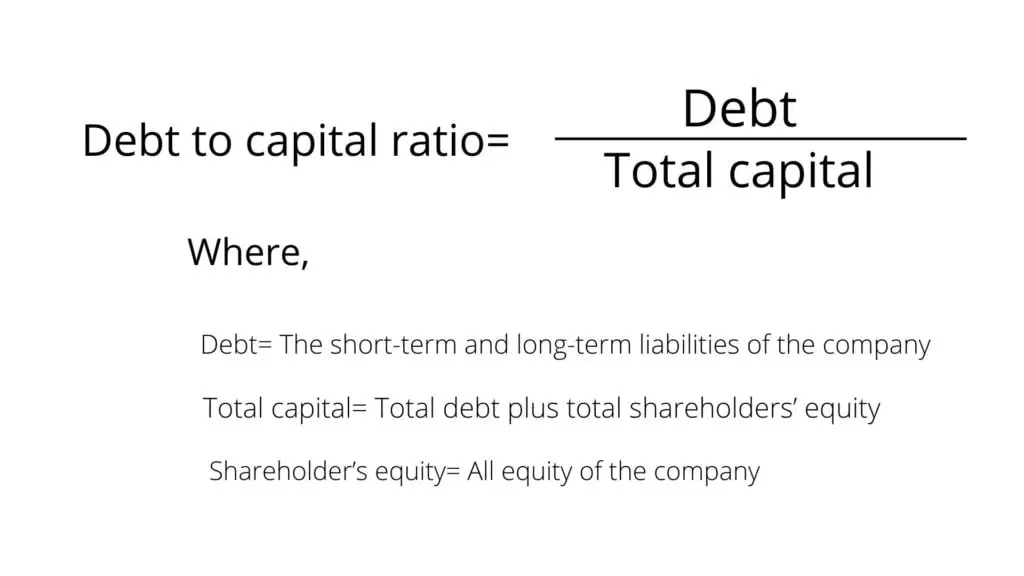

Debt to capital ratio formula

The debt-to-capital ratio formula is expressed as:

Debt to capital ratio = Debt / (Debt + Shareholder’s equity)

The debt to capital ratio formula is expressed as a relationship between a company’s total debt to its total capital.

Where,

The total debt= The company’s short-term and long-term liabilities

The total capital= Total debt plus total shareholders’ equity

The shareholder’s equity= All equity of the company such as common stock, preferred stock, net debt, and minority interest

Calculation

The debt to capital ratio calculation is done by dividing the total debt of the company by the sum of the total debt and shareholder’s equity of the company. The data used to calculate the debt to capital ratio are found on the balance sheet of the company.

Here are some examples of how to calculate debt to capital ratio:

How to calculate debt to capital ratio: Example 1

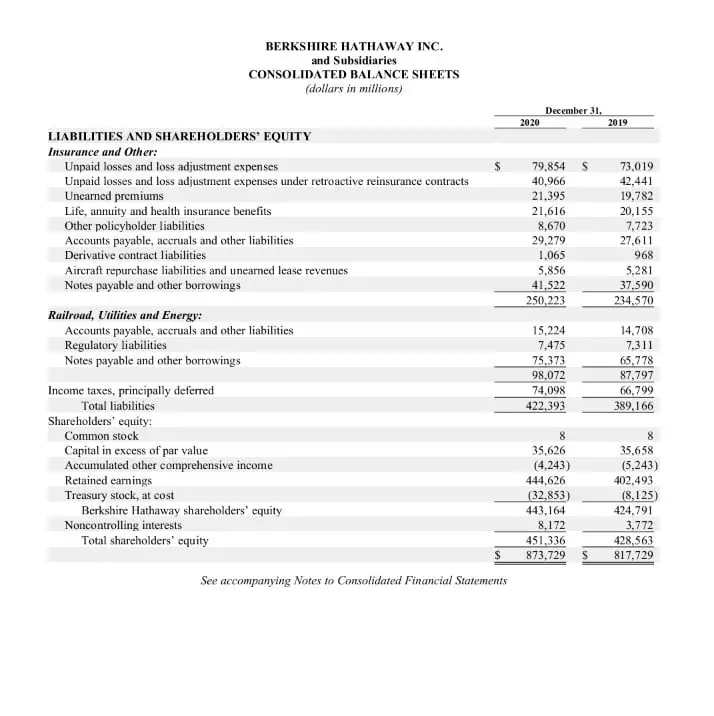

Berkshire Hathaway is an American multinational conglomerate holding company that owns businesses in rail transportation, insurance, energy generation and distribution, manufacturing, and retailing. Using the excerpt from Berkshire Hathaway’s balance sheet for the fiscal year of 2020 below, let’s calculate the debt to capital ratio for Berkshire Hathaway.

For the fiscal year (FY) ended December 31, 2020, it can be seen from the excerpt of the balance sheet above, that the company had total liabilities of $422,393,000 and a total shareholder’s equity of $451,336,000,000.

Solution

How to calculate debt to capital ratio of Berkshire Hathaway using the debt to capital ratio formula:

Debt to capital ratio = Debt / (Debt + Shareholder’s equity)

Debt to capital ratio= $422,393 million / ($422,393 million + $451,336 million)

Debt to capital ratio= $422,393 million / ($873,729 million)

Debt to capital ratio= 0.4834 or 48.34%

Debt to capital ratio analysis: This means Berkshire Hathaway had a debt to capital ratio of 0.4834 (48.34%). The debt to capital ratio of Berkshire Hathaway is considered low as the ratio is below 1. The lower the debt to capital ratio of a company, the less debt it has compared to its equity. This simply means the capital of Berkshire Hathaway is funded through equity capital. Therefore, the company would have greater flexibility in terms of raising additional capital through debt.

How to find debt to capital ratio: Example 2

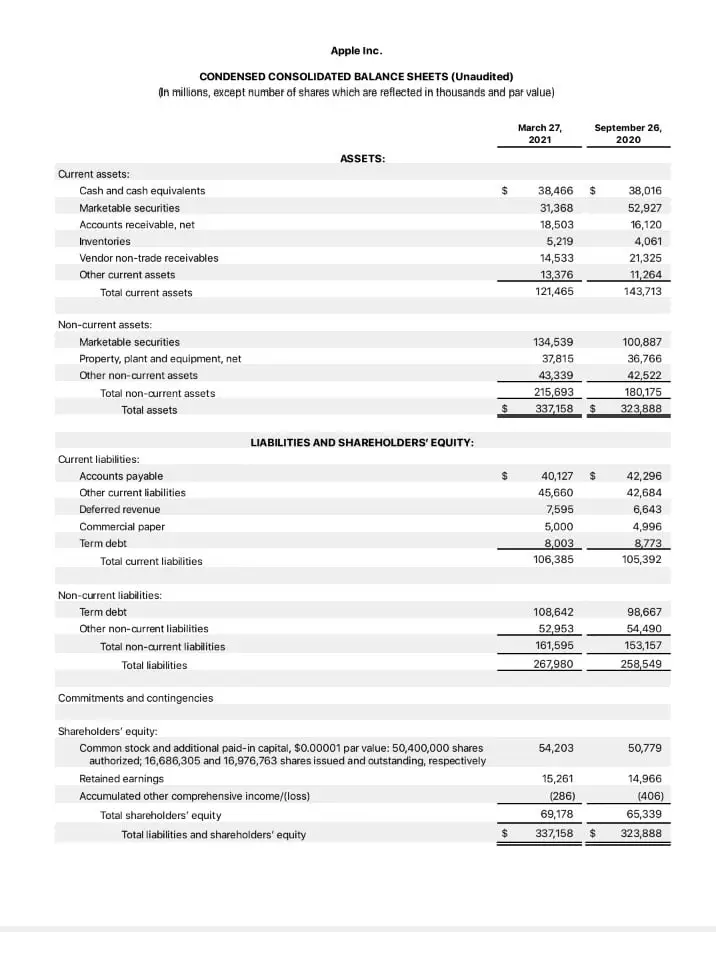

Apple is an American multinational company in the Information technology sector that specializes in consumer electronics, software and online services. Using the excerpt from Apple’s balance sheet for the fiscal year of 2020 below, we can carry out debt to capital ratio calculation for Apple Inc.

For the fiscal year (FY) ended September 26, 2020, it can be seen from the excerpt above, that the company had total liabilities of $258,549,000,000 and (total liabilities and shareholder’s equity) of $323,888,000,000.

Solution

How to find D/C ratio of Apple Inc. using the debt to capital ratio formula:

Debt to capital ratio = Debt / (Debt + Shareholder’s equity)

Debt to capital ratio= $258,549 million / $323,888 million

Debt to capital ratio= 0.7982 or 79.82%

Debt to capital ratio analysis: This means Apple had a debt to capital ratio of 0.7982 (79.82%). The debt-to-capital ratio of Apple may seem higher than that of Berkshire Hathaway in the first example. An acceptable explanation for this is that the operational activities of Apple are capital intensive. Financial firms, banks, capital-intensive companies, large manufacturing companies, and utilities tend to have much higher debt-to-capital ratios than other businesses because they make use of a high level of debt financing as a common practice.

Example 3

Assuming you work as the chief financial officer (CFO) in a successful sales and marketing company that makes use of loan money to finance its large marketing campaigns and promotional activities. The executives of the company have been meeting with a potential investor for the company but, the investor is interested in knowing the risk of investing in the company.

So, the executives of the company have asked you to calculate the debt to capital ratio of the company because the investor has decided not to invest in the company if the debt to capital ratio percentage of the company is more than 40%.

How would you calculate the debt capital ratio of the company you work for if you’ve gathered from the balance sheet that the company has accrued $770,000 total in debt and has $2.2 million in shareholder’s equity, counting preferred and common stocks? From your calculation, do you think the investor would still be interested in investing in the company? What will be your report?

Solution

Calculating the D/C ratio of the company as the chief financial officer (CFO)

Using the debt to capital ratio formula:

Debt to capital ratio = Debt / (Debt + Shareholder’s equity)

Debt to capital ratio= $770,000 / ($770,000 + $2.2 million)

Debt to capital ratio= $770,000 / $2,970,000

Debt to capital ratio= 0.2592 or 25.92%

Debt to capital ratio analysis: From the calculation done the company has a debt to capital ratio of 25.92%.

The CFO can report the ratio to the executives. As a result of the low ratio, there is a very high possibility of the investor investing and becoming a stakeholder of the company as the debt to capital ratio is below the investor’s limit of 40%.

Importance and uses

The debt to capital ratio is an important financial metric used to evaluate how much a company depends on debt to finance its daily activities. The ratio is used to estimate the risk level to a company’s shareholders. This ratio is also important as it assesses the creditworthiness of a business to meet its liabilities in the form of interest expenses and other payments.

Using the debt-to-capital ratio can show if or not a company has the ability to pay back the interest on the loans taken. It also gives an insight into whether the company will have enough money left over (free cash flow) for other investments like acquisitions or research and development.

Company managers and investors use the debt-to-capital ratio to know if the company has too much debt and whether the company should consider selling off assets in order to reduce its liabilities and level out its D/C ratio. They might also consider using the D/C ratio to compare businesses within an industry.

Limitations of the debt to capital ratio formula

The debt-to-capital ratio is a better metric than simply totaling the debt obligations of a company. However, in as much as the debt to capital ratio is important for measuring the financial leverage, stability and solvency of the company, there are limitations to using the ratio.

One of them is that the ratio may be affected by the accounting conventions that the company uses. Usually, the values on the financial statements of a company are based on historical cost accounting and may not actually reflect the true current market values. So, it is very crucial and necessary to ensure that the correct values are used in the debt to capital ratio calculation, in order to avoid the ratio from becoming distorted.

Furthermore, as investors and creditors use the D/C ratio as a metric to decide whether or not to invest in or lend to a company, they should consider the following limitations of the debt-to-capital ratio:

- Debt service

- Comprehensiveness

- Accounting standards

Debt service

The debt to capital ratio as a measure of leverage ratio tends to favor companies and sectors that do not rely heavily on debt. Take, for instance, large, capital-intensive firms like electricity providers or other utilities tend to have a higher debt-to-capital ratio despite the fact that they have a large, stable customer base. Having a large, stable customer base gives such companies plenty of reliable income, even if they have to service a lot of short- and long-term debt. Therefore, contrary to what their high debt to capital ratio says, these companies are probably less susceptible to temporary downturns or shortfalls.

Comprehensiveness

The debt to capital ratio may not be comprehensive enough. Therefore, an analyst may consider calculating the debt-to-asset ratio and debt-to-equity ratio with the D/C ratio in order to get a comprehensive sense of a company’s overall value as an investment. The debt-to-asset ratio also known as the debt ratio compares the debt obligations of a company to the company’s total assets. The debt-to-equity ratio, on the other hand, compares the total liabilities of a company with its shareholders’ equity. The debt capital ratio, together with these financial ratios will give a proper insight into the bigger picture of a company’s overall value as an investment.

Accounting standards

Like other financial measurements, the metrics for debt-to-capital ratios are not constant across different time periods and businesses. One of the limitations associated with the debt to capital ratio is that accounting standards might vary like a company using out-of-date means of measuring value on their financial statements. Sometimes, a company will add accounts to the overall debt. Therefore, getting the most up-to-date information is important and may need some research and analysis.

Debt to capital vs debt to equity

What is the difference between the debt to capital ratio vs debt to equity? The major difference between these two ratios is that the debt-to-equity ratio compares the total liabilities of a company with its shareholders’ equity while the debt-to-capital ratio compares the total liabilities of a company to its total capital (debt + shareholder’s equity).

Even though each of these ratios indicates something different about the operations and funding of a business, they both provide information about how risky or financially stable a business is. In the debt-to-equity ratio formula, only the total shareholder’s equity is included in the denominator whereas in the debt-to-capital ratio formula the total debt plus total shareholder’s equity is included in the denominator.

FAQs

Is debt to capital ratio a solvency ratio?

Solvency ratios are the ratios used to measure a company’s solvency, which evaluates the financial health of a company. The solvency of a company is determined by how much money the company has borrowed as debt and its ability to repay this debt apart from its regular obligations. The debt to capital ratio is one of the other many solvency ratios used to evaluate the financial health of a company. The ratio compares the total debt of a company to its total capital, thus, measuring the financial leverage, stability and solvency of the company.

What is a good debt to capital ratio percentage?

A good debt to capital ratio percentage would depend on the average debt to capital ratio by industry. However, a percentage of less than 100 is considered an ideal debt to capital percentage because the higher the D/C ratio, the greater the risk to lenders and shareholders.

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.