We can derive the return on equity formula by dividing the net income by the shareholders’ equity. The ROE formula is a financial metric that helps in the assessment of a company’s ability to generate profits by leveraging shareholders’ investments. It shows the attractiveness of a business to shareholders. We will discuss the uses of the return on equity formula and gives some examples of ROE calculation.

What is ROE?

Return on equity (ROE) is a financial metric that helps in assessing a company’s ability to generate profits by leveraging the investments that the company shareholders made. It is derived by dividing the net income by shareholders’ equity. Because of the fact that equity equals the assets of a company minus its debt, ROE is seen as the return on net assets. In other words, ROE indicates the profit that each common stockholder’s equity generates. We can view it as the amalgamation of two financial statements, that is net income and dividend paid to preference shareholders from the income statement and shareholder’s equity from the balance sheet.

ROE has been considered a financial metric that gauges a corporation’s profitability and its efficiency in generating profits. A higher return on equity signifies that a company’s management is more efficient at generating income as well as growth from its equity financing.

ROE can be used as a benchmark for an industry and a company that has a relatively high ROE than its peers in the industry can be considered to have a competitive advantage. Also, return on equity can provide insights into a company’s financial management as well as its ability to grow business by leveraging equity.

Whether an ROE is judged to be good or not will be dependent upon what is normal among stock peers. For example, utilities have many assets and debts on the balance sheet in comparison to a relatively small amount of net income. A normal return on equity in the utility sector could be 10% or less. It is a good rule for a company to target an ROE that is equal to or just above the average of the sector under which it operates. Relatively high or low ROE ratios will vary significantly across industry groups or sectors

ROE can be used to estimate sustainable growth rates and dividend growth rates; assuming that the ratio is roughly in line or just above its peer group average. Although there may be some challenges, ROE can be a good starting point for developing future estimates of the growth rate of stocks as well as their dividends. These calculations are functions of each other and can be used to make an easier comparison between similar companies.

To estimate the future growth rate of a company, multiply the return on equity by the company’s retention ratio. The retention ratio is the percentage of net income that the company retained or reinvested to fund future growth.

Return on equity formula

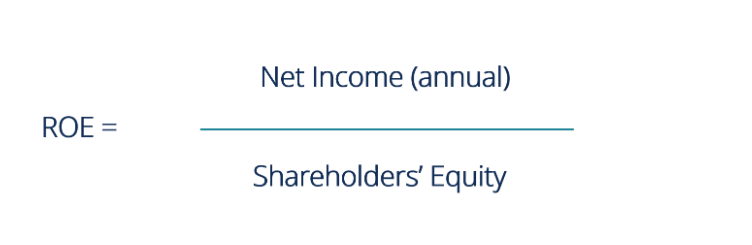

The return on equity formula can be derived by dividing the net income by the shareholders’ equity. The value of ROE is usually expressed in terms of percentage.

Net income is also known as net profit and it is found on the income statement. It shows the total profit left over after the cost of goods sold, operating expenses, and other expenses have been taken into account. Because of this, it is usually referred to as the bottom line and it can be found at the very bottom of the income statement.

Shareholders’ equity is found in the balance sheet. If a company were to liquidate all of its assets and pay off all its liabilities, what will be left is the shareholders’ equity. The balance sheet is a reflection of the accounting equation; Assets = Liabilities + Shareholder Equity. Therefore, to find shareholders’ equity, you simply subtract liabilities from assets.

ROE calculation

As earlier stated, ROE is expressed as a percentage. It can be calculated for any company if the net income and equity are both positive figures. Net income is calculated before dividends are paid to holders of common stock and after dividends are paid to holders of preferred stock and interest to lenders.

Example

If for example, the most recent net income of Procter & Gamble is $3,828 and their total equity is $17,034, calculate the firm’s return on equity. Now, we will compute the figures into the formula;

Return on equity = Net income / shareholders’ equity

Return on equity = $3,828 / $17,034

Return on equity = 22.5%

Limitations of ROE formula

Sometimes, an extremely high return on equity is a good thing if net income is extremely large compared to equity because the performance of the company is so strong. However, an extremely high ROE may not always be positive, it is usually a result of a small equity account compared to net income, which indicates risk. It can be an indicator of some issues such as;

- Inconsistent profits

- Excess debts

- Negative net income and negative shareholders’ equity

Inconsistent profits

The first potential issue that may be associated with a high could be inconsistent profits. Let us assume a company has been unprofitable for several years and the losses of each year are recorded on the balance sheet in the equity portion as a retained loss.

These losses come in the form of a negative value and reduce shareholders’ equity. Now, if this company has had a sudden large benefit in the most recent year and returned to profitability, the denominator in the ROE calculation is now very small after years of losses and this makes the ROE misleadingly high.

Excess debts

The second issue that is bound to cause a high ROE is excess debt. If the company has been borrowing aggressively, its ROE can increase because equity is equal to assets minus debt. The more a company’s debt is, the lower equity can fall. A common scenario is when a company borrows large amounts to buy back its own stock. This has the capacity to inflate earnings per share (EPS) but has no effect on actual performance or growth rates.

Negative net income and negative shareholders’ equity

The third issue that may create an extremely high ROE is negative net income and negative shareholders’ equity. However, if a company has a net loss or negative shareholders’ equity, then it is not necessary to calculate ROE.

If the shareholders’ equity is negative, either excessive debt or inconsistent profitability can be the issue. However, exceptions exist to the rule for companies that are profitable and have been making use of cash flow to buy back their own shares (treasury stock).

For most companies, this is an alternative to paying dividends and it can eventually bring about a reduction in equity (buybacks are then subtracted from equity) and it is enough to turn the calculation negative.

In all cases, one should consider negative or extremely high ROE levels a warning sign that needs to be investigated. In rare cases, a negative ROE could be a result of a cash flow-supported share buyback program and excellent management but this outcome is less likely to happen. In any case, it is not possible to evaluate a company with a negative return on equity against other stocks with positive ROE ratios.

With all tools used for investment analysis, ROE is just one among many available metrics that identify just one portion of the overall financials of a firm. Therefore, it is important to utilize a combination of financial metrics to fully understand a company’s financial health before investing.

FAQs

What is a good ROE ratio?

It is better for a company to target an ROE that is equal to or just above the average of its peers in the sector. Whether an ROE is relatively high or low will vary significantly across industries.

Is return on equity better high or low?

Whether a return on equity is high or low varies across the sector under which the company is operating. However, ROE should not be extremely low or extremely high. A company should aim at a return on equity that is equal to the average of its peers or just above the average.

What does high ROE mean?

A high ROE does not always mean a good thing. It may mean that the company is generating inconsistent profits, the company has incurred excess debts, or the company has a negative net income or negative shareholders’ equity.

What happens if ROE is negative?

When an ROE is negative, it means that the firm is in financial distress since the financial metric is an indicator of profitability.

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.