Consol perpetuities examples include the British and American consols that were first issued in the eighteenth and nineteenth centuries respectively.

Aside from these two popular examples, other governments and public corporations such as the Dutch water board, Lekdijk Bovendams have also issued securities that are additional examples of consol perpetuities.

Apart from consols, other types of perpetuities exist in the form of endowment funds and real estate investments.

See also: Delayed Perpetuity Examples and Types

What are consols?

The term consol is a contraction of consolidated annuities. It refers to government-issued securities that pay their holders a fixed amount at regular intervals. Similar to other perpetuities, consols do not have a maturity date but they could be redeemed at the government’s option.

Consols were initially used to refer only to consolidated annuities but were subsequently used to refer to consolidated stock as well. Although perpetuities were mostly issued by the government, some business corporations also issued them.

These investment options largely arose as a means for the government to ease access to funds especially during times of war or for large scale projects. During wartime, loans were usually harder to come by because yields on government debt usually rose as investors were uncertain about the safety of their investments.

Hence, the creation of consols helped to solve this uncertainty by providing investors with an assured fixed income that is paid out at fixed intervals without a maturity date.

Additionally, the availability of funds provided additional advantages to governments as they could finance more developmental projects as well as financing wars that aided them in expanding their territories.

See also: Perpetuities and Interest Rate Risk

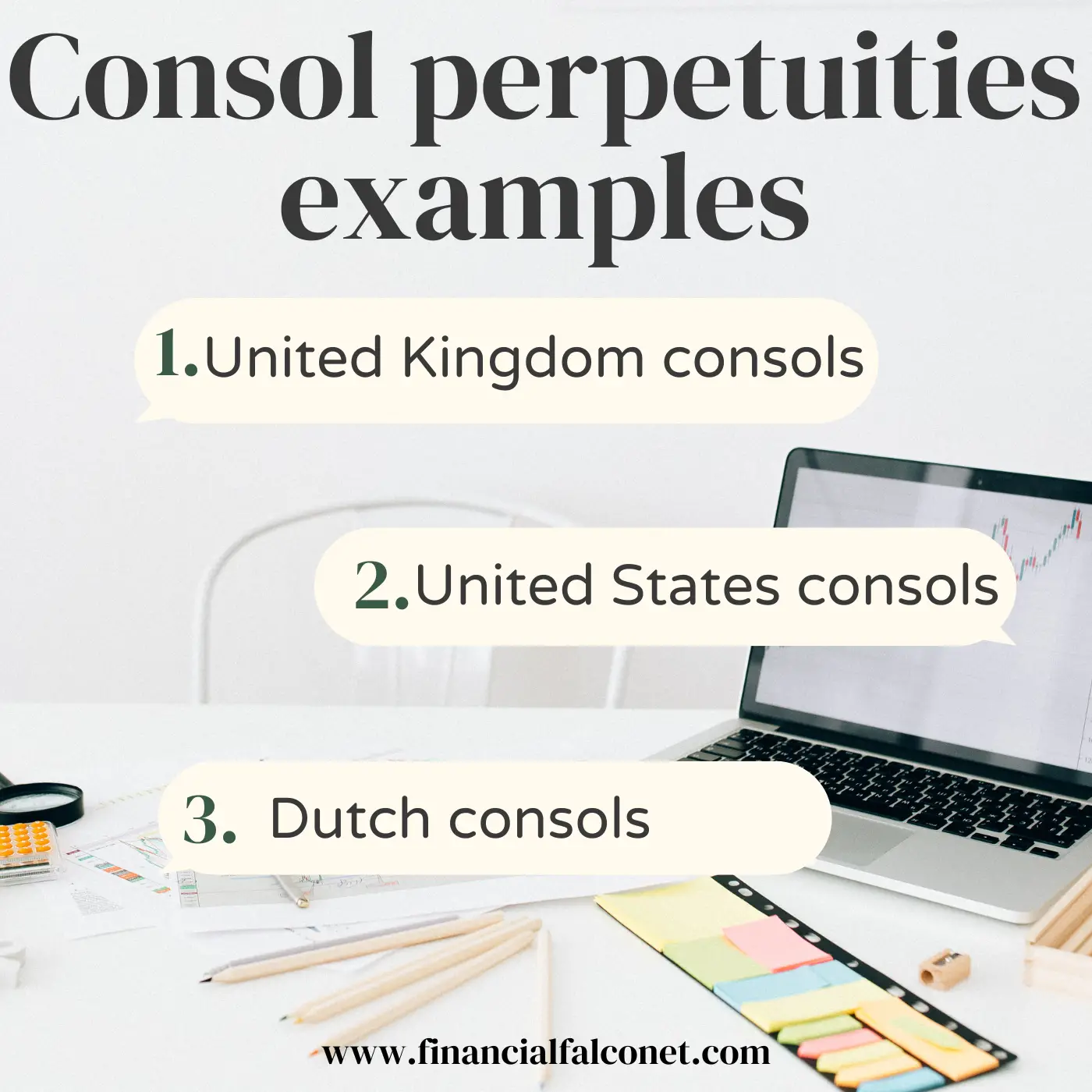

Consol perpetuities examples

- United Kingdom consols

- United States consols

- Dutch consols

United Kingdom consols

- British consols

- Undated bonds

British consols

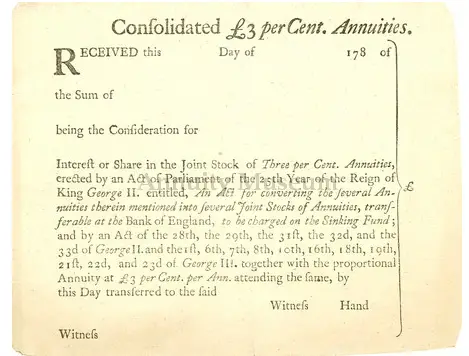

The consols that were issued in the United Kingdom are the most common examples of consols. Before the British government began issuing consols in the eighteenth century, borrowing costs were high and the government paid eight percent (8%) annually in interest.

In a bid to reduce this interest payment and expand the government’s access to funds, the government turned to the sale of annuities.

In 1726, the British government with the assistance of the Bank of England issued the first three percent (3%) annuities; these were known as the three percent bank annuity. Additional three percent annuities were issued in 1727 and 1731.

The British government also issued annuities that had a four percent (4%) interest rate and by 1749, a significant percentage of the British public debt comprised mainly of 4% bonds.

The funds realized from the sale of these annuities were used to repay the government’s outstanding debts that had a higher interest payment.

Both the 3% and 4% annuities paid a fixed interest rate annually and did not have a maturity date but they were redeemable by the government at any time.

The clause of the annuities being redeemable by the government at any time provided grounds for renegotiations as the government could offer bondholders the option of accepting a lower rate of interest or redemption of the bonds.

In a bid to unify the interest rates of the issued annuities, two consolidation attempts were made by the government in 1737 and 1749 respectively.

Although the first consolidation attempt failed, the second one was successful and by 1750, a significant portion of the 4% annuities were converted to 3% annuities while the remainder of £7 million worth of 4% annuities were paid off at face value.

Thus, by the end of 1750, the government’s long-term debt comprised exclusively of 3% bonds as the government succeeded in cutting the debt service costs of the largest part of its debt by 25%.

In the same year, the different issuances of 3% annuities were consolidated into the three percent consols with the Consolidating Act of 1751. Hence, the annuities became commonly known and referred to as consols.

These consols continued to pay their holders a fixed interest amount annually until 2015 when the British government made legal provisions for ending the consol through Section 124 of the Finance Act 2015.

Undated bonds

Another consol perpetuity example is a type of government bond known as gilts or undated issue. This type of bond also pays the bondholders interests indefinitely and has no maturity date.

The government of the United Kingdom issued undated bonds in the nineteenth and early twentieth centuries as an additional source of financing for war expenses ranging from the purchase of arms to the payment of soldiers.

The largest glits which the UK government issued was in the early 20th century. The bond had a 3.5% coupon rate and an issue size of £1.9 billion.

United States consols

The United States government also issued consols from the late nineteenth to the early twentieth centuries, precisely between 1877 to 1930.

Similar to the UK, the United States had also incurred a significant debt profile due to wars, this led Treasury officials to borrow funds in less regular ways and on terms that may not be attractive.

Thus, during the following peacetime, the funds from consols provided the government with the means to lower its borrowing costs and pay off the debts that were incurred during wartime.

Consols also provided solutions to the government by providing considerable funding for major large-scale projects. They also provided flexibility in payments since they did not have a fixed maturity date on which the principal must be repaid.

Additionally, citizens who had the means to invest were more willing to invest in consols due to the promised continued cash flow they were to receive. This is because it provided a sure income source in the future, preserving their buying power, and saving them from penury in old age.

Usually, coupon payments to investors are made either semiannually or quarterly until the government decides to call the bond. Some consols such as the 4% consol pictured below could be recalled by the government from 1907, that is, 30 years after they were issued.

Thus the U.S. Treasury typically sought to redeem bonds soon after they could be called, rather than allowing them to remain outstanding for centuries.

These consols were considered examples of perpetuities because although the government could redeem them after 30 years, they typically lacked a fixed maturity date.

Consols proved very useful for America because apart from sponsoring major projects and wars, the funds aided in financing the purchase of gold bullion to back the dollar’s value.

The U.S. Treasury issued 4% consol bonds in 1895 and 1896 to replenish its gold reserve and cover deficits, hence facilitating a return to the gold standard.

Dutch consols

- War-time consols

- Water board consols

War-time consols

War-time annuities are an additional consol perpetuity example, these were issued by Holland’s government in the late fifteenth and sixteenth centuries. It precisely started in 1542 when Charles V, the Habsburg Emperor, placed certain wartime demands on his Dutch provinces.

The local governments issued annuities as an alternate source of funding when raising funds via taxation was resisted by the citizens. The annuities required that investors pay a lump sum to the government in exchange for a promised series of payments in the future.

These annuities were issued as either life annuities or heritable annuities. The life annuities offered their holders equal payments over the course of one or two lifespans while the heritable annuities offered perpetual payments with no end date.

Annuities remained a common means of financing state debts for more than three centuries.

Water board consols

An additional Dutch consol is that issued by the Dutch water board, Lekdijk Bovendams. The consol was first issued in 1624 when a dyke burst and the water board needed money to fix it.

The 33-kilometer-long dyke from Amerongen to Vreeswijk, protects large parts of Holland and Utrecht against the water. Thus, the water board used funds raised for improvements, restoration, and new projects. The bonds were bearer bonds which means that anyone who presented the bond certificate to the water board could collect the interest as the board did not keep a register that contained ownership details.

The bonds that the water board issued in 1624 and 1648 still pay their holders interest of about 15 euros a year.

See also: Perpetuities and Derivatives: Differences and Similarities

Features of consolidated perpetuities

- Fixed income stream

- Regular payment intervals

- No maturity date

Fixed income stream

One of the prominent features of consils is the consistent cash flow they provide their holders. Consols pay their holders a fixed coupon, depending on the interest rate. The fixed income is usually denominated in the currency of the issuing government or country where the corporation is located.

For instance, payments from US consols are in dollars while those from UK consols are in euros.

Regular payment intervals

The fixed payments that consol holders get may be done quarterly, semi-annually, or annually depending on the terms of the consol. This means that the investors know when to expect their next payment since they are done following a regular payment interval.

No maturity date

Another feature of consols is that they do not have a maturity date, this means there is no specified date when the holder is expected to receive back their principal investment when they purchased the consol.

See also: Present Value of Perpetuity Formula and Calculation

Conclusion

Perpetuities exist in different forms and consol perpetuities are one example. Consols were initially the short form for consolidated annuities but have been broadened to include consolidated stock as well.

Different countries and corporations have issued consols in the past as a means of raising funds to fund wars and other large-scale projects. The main features of consols include recurrent fixed payments at regular intervals and a lack of expiration dates.

Although consols are rarely issued in recent times and most of those that were issued in the past such as the UK consols have been fully redeemed by the government, some others such as the Dutch water board consols still pay their holders annually.

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.