RSU stocks are a type of employee compensation that is taxed when vested or exercised. RSU stands for Restricted Stock Unit and works similarly to a bonus, except that you receive stock units (shares of your company) as opposed to a regular bonus that you receive in cash or on your paycheck.

This is a crucial concept to comprehend because you might see an RSU listed as a component of the compensation package in a job offer. Understanding restricted stock units and their benefits can assist you in negotiating better job terms during the hiring process. In this article, we will discuss RSU stock, tax implications, and how it works; we will also look at how you get to earn this form of employee compensation (RSU stock vesting), but before that, let’s grasp the meaning of RSU.

What is RSU stock?

A restricted stock unit is a type of payment or compensation made by an employer in the form of stock in the company to an employee. It is not technically worth anything right away because it is a promise of future company stock.

The RSU is converted to actual stock shares once the employee has become fully vested due to performance or length of service with the company.

RSUs are the most common type of equity compensation and are typically offered after a private company goes public or achieves a more stable valuation. RSUs, like stock options, vest over time, but unlike stock options, you are not required to purchase them. They are no longer restricted once they have vested and are treated exactly the same as if you had purchased your company’s shares on the open market.

RSUs are thus less risky than stock options. As long as the price of your stock does not fall to zero, it will always be worth something.

Let’s take a situation to illustrate; Consider receiving 10,000 RSUs with a four-year vesting period. For the entire four years, the stock price remains at $10. (rather than vary as it normally would). This means the RSUs are worth $100,000. In the same circumstance, stock options with a $10 strike price would be completely worthless unless the stock price increases.

RSUs usually vest over a number of years, just like stock options. After your first year of employment, it’s typical to receive 1/4 of your RSUs, and then every month after that, another 1/36 of the remaining grant. The value of the shares on the vesting date is subject to ordinary income tax when calculating your taxes. RSUs encourage employees to stay with the company longer because they vest gradually, just like stock options do.

How do RSU stock work?

RSUs work using the grant and vest date. These are the two important dates to remember when dealing with RSUs. The RSU is awarded on the grant date and the RSU becomes available and can be sold on the vesting date.

On significant occasions, employees are given RSUs for instance, when a new employee joins the company. This trend of granting RSU follows the step laid by many major technology companies, like Microsoft and Google, to give RSUs to their employees.

For example, let’s assume that you began working for Microsoft in January 2021. The company then grants you 100 restricted stock units with a four-year vesting period when you join the company. 25% of the RSUs vested each year. 100 more restricted stock units are granted to you each year after that.

According to this illustration, 25 shares will become vested after one year, another 25 after two years, and so on. You receive an additional 100 restricted stock units for every year you continue to work for the company. As a result, there is what is known as a “vesting cliff,” whereby a single year has multiple vesting periods.

On a whole, RSUs typically vest over time rather than all at once.

Related: Early Exercise of Stock Options

Types of RSU stock

RSUs may be offered by employers with a variety of restrictions. Some restrictions are referred to as single-trigger RSUs because they are only subject to a vesting schedule. Others, known as double-trigger RSUs, may have additional requirements that must also be met before vesting.

Single-trigger RSU stock (time-based vesting)

This kind of RSU is typical for publicly traded companies and has just one vesting requirement, which is typically time-based.

For instance, take the example of receiving 1,500 RSUs with a vesting schedule of 20% after the first year of service and equal quarterly payments thereafter for the following three years. This would imply that 300 shares would vest and become yours once you had been employed by the company for a year. Every quarter for the following three years that you stay employed by the company, another 100 shares will become yours.

The aforementioned example shows how a graded vesting schedule works, with periodic grants becoming fully vested over a period of several years.

Double-trigger RSUs (performance-based goals)

RSUs may be subject to additional restrictions, frequently connected to performance, in addition to a vesting schedule. This may entail that the business must accomplish specific objectives, such as the introduction of a new product or service, or go through a liquidity event, such as a merger, an acquisition, or going public via an IPO, direct listing, or SPAC listing.

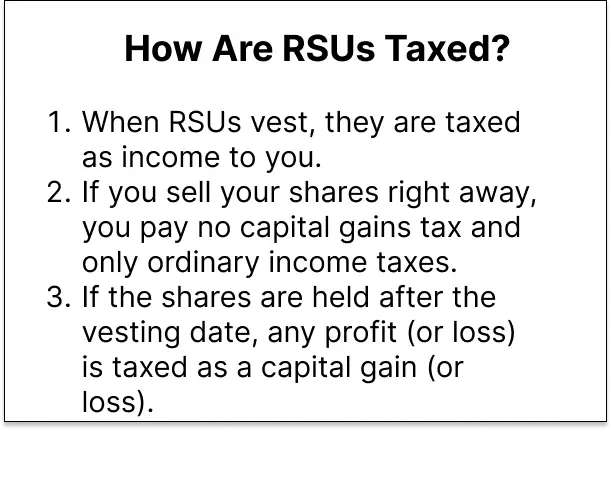

RSU Taxes

First of all, no tax payment is required when RSUs are granted, rather RSU stocks are taxed at the time the shares are delivered, which is almost always at vesting. Your taxable income is equal to the market value of the shares at the time of vesting.

Some businesses might allow you to reduce the shares you received by the amount of taxes due in order to reduce your tax obligation. For instance, if 300 shares vest and are valued at $10 each, you will be required to pay tax on $3,000 of income. Your tax obligation, assuming a 30% tax bracket, is $900, or 90 shares. You might be able to choose to only get 210 shares, with 90 of those being used to pay your taxes.

Another point in RSU taxes is that you must pay capital gains tax on any increase in the share’s market value over the vesting date’s price when you later sell the shares. For instance, you will have to pay ordinary income tax on $10,000 if, as part of your compensation package, you receive RSUs worth $10,000. If you decide to keep the $5,000 worth of stock (and decide against selling it) and the stock’s value rises to $7,000, you will be required to pay capital gains tax on the $2,000 increase in value.

RSU Taxes For Non-U.S. Employees

The timing of taxation for restricted stock units is comparable for employees outside the United States who work in other nations. Capital gains tax is imposed on the eventual sale of the shares, and income and social taxes are calculated based on the value of the shares at the time of delivery (not grant).

Minimization of capital gains tax on RSU stock

To reduce capital gains tax, there are two options. The first is to sell the stock as soon as it vests. This guarantees that there will be no taxable gain. You could repurchase the shares in a stock and shares ISA if you still want to hold onto them. By doing this, future growth will be tax-free (although you may still pay withholding taxes, particularly if the shares are held in a US company)

The second option is to give your spouse some of your RSUs. This is especially helpful if the shares you own have seen significant gains since vesting. The inter-spousal transfer exemption means that there is no tax due when you transfer shares to your spouse. After that, your spouse can sell the stock while utilizing their capital gains tax deduction.

Reduction of RSU taxes

Making contributions to your pension plan is one way to lower the amount of tax you pay on RSUs. This is due to the fact that contributing to a pension lowers your “adjusted net income,” which in turn lowers your tax bill and possibly your effective tax rate.

Let’s assume that you earn $100,000 and receive $25,000 in RSUs. Your overall income is now $125,000. You will be required to pay 60% income tax on the RSUs because they raise your total income above $100,000.

By contributing to a pension, you can reduce this 60% tax charge. For tax purposes, you will have earned $75,000 if you contribute $25,000 to a pension and receive $25,000 in RSUs as a result. With a total income of $100,000 as a result, you will not be subject to the 60% tax rate.

See also: Exercising Stock Options and Taxes

Vesting RSU stock

In RSU vesting, most vesting schedules are time-based, requiring that you work for the company for a predetermined amount of time before vesting can take place. For example, you receive 5,000 RSUs. 25% of the grant vests annually under your four-year graded vesting schedule. 1,250 Shares vest on the first anniversary of the Grant Date and thereafter on the same dates each year for the next three years. You may sell the shares after each portion has vested.

In RSU vesting, there is graduated vesting which refers to the vesting schedules under which the stock that will be awarded as part of an RSU plan will vest at specified intervals and in the amounts specified during the vesting period. Most grants with graded vesting have restrictions that expire after three to five years.

For instance, if an RSU plan stipulates that the employee will become fully vested after five years of employment, the employee may only become fully vested in accordance with the RSU plan at specified intervals during the five-year period. For instance, the RSU plan might specify that vesting will be phased in over time, with 10% of shares vesting after one year, 30% after two years, 50% after three years, 80% after four years, and 100% after five.

RSU stock vs Stock options

In the past, startups have almost exclusively used stock options to give their valued employees a stake in the company’s success. RSUs became a well-liked form of compensation over the course of the last decade or so, which caused the trend to start to change. Each option has advantages and disadvantages, and you should consider your business, tax situation, and voting rights when choosing the best course for your organization.

In stating the difference, we’re breaking down the definitions and key distinctions between stock options and restricted stock units to help you decide which is best for your business.

Difference between Stock Options and Restricted Stock Units

Paying salaries, providing benefits like health insurance and paid time off, and even giving employees the option to receive compensation in the form of company stock are all options that you as an employer have. When creating employee benefits packages, your business will need to consider the distinction between stock options and RSUs.

Let’s take a quick look at the history of stock options before we go too far into the details of RSUs vs stock options. The first stock options appeared in the early 1970s. They were created by a Silicon Valley lawyer as a component of a startup capital structure to support the boom in the high-tech sector. The objective was to develop a business model that would appeal to venture capitalists and offer staff members a worthwhile incentive to contribute to the company’s success.

Early in the new millennium, the IRS established a new regulation that required option strike prices to be set at the common stock’s fair market value at the time the option was granted. This was done to stop businesses from receiving excessive non-taxable benefits. Since the new regulation, businesses that grant stock options at prices below the common stock’s fair market value put employees in a position where they are subject to taxation on the portion of the option’s value that exceeds the cost of exercising it.

Let’s now examine how stock options and RSU definitions differ from one another:

- Stock Options: Grants the holder of the options the right to purchase shares of a company’s stock at a price set at the time of issuance.

- Restricted Stock Units: Provides holders with a promise to receive the equivalent value of a specific number of shares in the future without the need for a cash payment now. The vesting periods for these units typically apply.

Key differences between stocks vs RSU

| Characteristics | Stock Options | Restricted Stock Units (RSU) |

|---|---|---|

| Exercise price | In accordance with the underlying security’s full market value | None |

| Payment | Stock | Stock or Cash |

| Popular for this type of company | Earliest-stage, fastest-growing startups | Companies that are later stage and more developed |

| Rationale | Greater potential for value growth, time taxation for employees | Taxes are due when stocks are vested, and the sale of mature stock may help with the necessary payment. |

| Tax | The alternative minimum tax treats NSOs as preferred items while treating ISOs as regular income. | Treated as regular income (stock held longer than a year is treated as capital gains) and taxed at vesting |

| Vesting | Can be vested whenever a specified milestone occurs | Can be vested whenever a specified milestone occurs |

| Voting rights / Dividends | Upon exercise | No, but the company may offer a bonus equal to a dividend instead. |

Because employees don’t have to pay anything to obtain the stock, RSUs are less risky, which is another important factor in why businesses choose them. RSUs give employers a way to give employees a share of the company’s equity when the current value of the company won’t be realized until it has developed more. RSUs could be compared to an unfunded promise to issue shares of stock or cash equivalents in the future.

Related: ISO vs NSO Differences and Similarities

Advantages and disadvantages of RSU stock

RSUs have certain benefits and drawbacks that will be explained below.

Benefits or advantages of RSU stocks

- RSUs are simpler to comprehend than other equity compensation options, like stock options. When you will receive shares is specified in the vesting schedule, and it is simple to determine how much your award is worth.

- Employees who have stock options have the option to purchase shares of company stock at the strike price or exercise price. With RSUs, you do not need to make a purchase; the shares are yours once they have vested. RSUs typically cost less than stock options for the employee because some businesses let you surrender shares to pay your tax withholding.

- RSUs will continue to have value, unlike stock options, unless the share price of your company drops to $0. In the case of stock options, you could exercise your right to buy shares at the lower strike price, sell them for more money at the higher market price, and profit from the difference if the market price is higher when you sell them. There would be no reason to exercise your options if the strike price remained above the market price, as you could purchase shares on the stock exchange for a lower price. Your options could therefore expire being worthless. Selling 300 shares of RSUs at $10 per share would bring in $3,000 in profit. You could still make $1,500 even if the share price falls to $5.

- As soon as your shares have vested, you can keep them even if you leave the company. RSUs offer flexibility to employees, especially if the business is publicly traded. Employees may sell vested shares to fund other priorities. With the proceeds, they may fund retirement accounts, debt repayment, down payments for homes, or college savings accounts for their children.

Drawbacks or disadvantages RSU stock

- Finding the money to pay taxes could be challenging for some employees if your company is private and unable to help reduce your tax burden. If you have many double-trigger RSUs, you may be subject to a significant tax burden when a liquidity event occurs and all of your shares vest at once. The number of shares surrendered or cash withheld for taxes may not entirely offset the actual tax owed, even if your employer helps manage the taxes. Depending on their tax situation, employees may face additional tax consequences when it comes time to file their taxes.

- In the case of private companies, there will be a hazy waiting period before you can sell and profit from having to pay the taxes upfront. If the business does not expand as anticipated, even though the final award may be compelling, it may also leave you disappointed. When creating your strategy for holding or selling, it may make sense to seek advice from a financial or tax professional. You should also take into account your own financial situation.

Selling restricted stock units

You might be granted restricted stock if you contribute startup money to a private company, take part in an employee stock benefit plan, or purchase stock in a private placement. Before you can sell restricted stock, there are a few extra steps you must take, but otherwise, it is the same as stocks you can buy and sell on the open market. The sale of restricted stock is regulated by Rule 144 of the U.S. Securities and Exchange Commission, though most regulations only apply to sellers who are connected to the company, such as company officers. Sellers who are not affiliated must only abide by the holding period requirement.

There are 6 steps to follow in other to sell your restricted stock units. These steps will be briefly explained below.

- Comply with SEC holding period specifications: You must keep the shares for a minimum of six months after the full purchase price has been made. That holding period increases to a full year if the company issuing the stock is required to comply with the Securities Exchange Act of 1934 reporting requirements. The majority of publicly traded stocks are subject to the 1934 Act’s reporting requirements.

- Abide by reporting requirements set forth by federal law: The 1934 Securities Exchange Act stipulates that a company must publish periodic reports on its current situation. No transactions may be made in a company’s securities if this kind of information about the company is not made publicly available in accordance with the law, so you cannot sell your restricted stock.

- Verify the trading volume: You are only permitted to sell a certain amount of restricted stock within a three-month period if you are connected to the company. You are not allowed to sell more than 1% of the average reported trading volume over the previous four weeks for publicly traded stocks. You are only permitted to sell 1% of the outstanding shares of a particular stock class in private stocks during that three-month window.

- Take away the default legend: The removal of a stock legend, which makes the stock available for trading, must be requested from the issuing company’s transfer agent. You will be unable to sell your stock and have the legend removed without the issuer’s permission, which may necessitate hiring an attorney.

- Carry out a typical brokerage transaction: Your trade must be routine if you are a company employee, with no extra commissions paid to the broker and no requests to buy made by either the seller or the broker.

- Send necessary notices to the SEC: No later than three months prior to selling your restricted stock, you may need to file Form 144 with the SEC if you are an affiliated person. Sales of 5,000 shares or more, or shares with a total value of $50,000 or more, over a three-month period are subject to this requirement.

Conclusion

On a whole, RSU stock gives employees a stake in the company but no monetary value until vesting is completed. When RSUs vest, they are assigned a fair market value (FMV). Once vested, they are considered income, and a portion of the shares is withheld to pay income taxes. Once RSU is taxed, the employee receives the remaining shares and has the option to sell them or not.

See also: Stock Options vs Equity Differences and Similarities

Last Updated on November 8, 2023 by Nansel Nanzip Bongdap

Nansel is a serial entrepreneur and financial expert with 7+ years as a business analyst. He has a liking for marketing which he regards as an important part of business success.

He lives in Plateau State, Nigeria with his wife, Joyce, and daughter, Anael.