In an ongoing effort to help small businesses, the Internal Revenue Service (IRS) permits business owners to claim first-year bonus depreciation for some of their properties that are used in business. However, going by the passage of the Tax Cuts and Jobs Act of 2017 (TCJA), this bonus depreciation begins to phase out in 2023. The bonus depreciation phase out which starts after 2022 would be a significant change for businesses that have been relying on the accelerated tax deduction for business and tax planning.

This is because electing to take bonus depreciation can lower a company’s tax liability in that the tax incentive helps to reduce the company’s taxable income. In this article, we will discuss the bonus depreciation phase out schedule for the coming years and how this changes things for taxpayers.

Related: Rental Property Bonus Depreciation

Bonus depreciation explained

Bonus depreciation can be a tax-saving tool for businesses because this tax incentive allows business owners to take an immediate deduction on the cost of eligible business property in the first year. By claiming bonus depreciation, a taxpayer can deduct a certain percentage of the purchase price of an asset in the first year that the asset was purchased, while the remaining cost of the asset can be deducted using regular depreciation or Section 179 expensing over several years.

Bonus depreciation is optional but if you want to get the largest depreciation deduction, you may want to make use of this option whenever possible. Nonetheless, not all properties qualify for bonus depreciation. Property can qualify for bonus depreciation only if it has a useful life of 20 years or less (this includes all types of tangible personal business property and software, but not real property. The property can be new or used but must be acquired from someone that is unrelated to the taxpayer (it can’t be a gift or inheritance). Also, the listed property must be used for business more than 50% of the time.

Bonus depreciation was set at 50% of the purchase price of a qualifying asset for the tax years, 2015 through 2017. This percentage was scheduled to go down to 40% in 2018 and 30% in 2019, and completely phase out in 2020 and beyond. However, the Tax Cuts and Jobs Act of 2017 increased the first-year bonus depreciation from 50% to 100% of the cost of a qualifying asset.

When did 100% bonus depreciation start?

100% bonus depreciation started in 2017; from September 27, 2017, to December 31, 2022, you can deduct up to 100% of the cost of an asset in the year that you purchased it and put it into service. The deductible amount was increased in 2017 by TCJA from 50% to 100% and goes into effect for any qualifying asset placed in service after September 27, 2017, and before January 1, 2023.

When does 100% bonus depreciation end?

100% bonus depreciation ends after 2022; after this year, the 100% decreases by 20% until it phases out in 2027. This means that unless Congress extends the rate, bonus depreciation phase out by 2027. That is, only qualifying assets purchased after September 27, 2017, and before January 1, 2023, are subject to the 100% bonus depreciation. Starting in 2023, bonus depreciation phases out gradually by dropping to 80%, and continues to reduce by 20% over the next years.

See also: Can you take bonus depreciation on rental property?

When does bonus depreciation phase out?

As earlier said, The bonus depreciation phase out begins in 2023 with qualifying assets getting only an 80% bonus deduction in 2023 and less in later years. Unless the law changes, each year, starting in 2023, the bonus percentage will decrease by 20 points until the percentage rate of the tax incentive reaches zero in 2027. Therefore, according to the TCJA bonus depreciation phase out schedule, the bonus percentage over the next few years will be 80% in 2023, 60% in 2024, 40% in 2025, and 20% in 2026, until it completely phases out in 2027.

It is important to know that the amount of bonus deduction that your asset qualifies for would depend on the bonus depreciation rules that have been put in place for that tax year. For instance, let’s assume you placed a rental property into service in 2022 but you waited until 2024 to implement a cost segregation study in order to claim bonus depreciation on your rental property improvements or the assets used within the rental property.

The fact is, regardless of the TCJA bonus depreciation phase out schedule for 2024, your assets would still qualify for 100% bonus depreciation when your method change is filed. This is because your assets were put into service in 2022 which qualifies it for the 100% bonus depreciation rather than the 2024 bonus rate of 60%.

Check out: Adjusting Entry for Depreciation

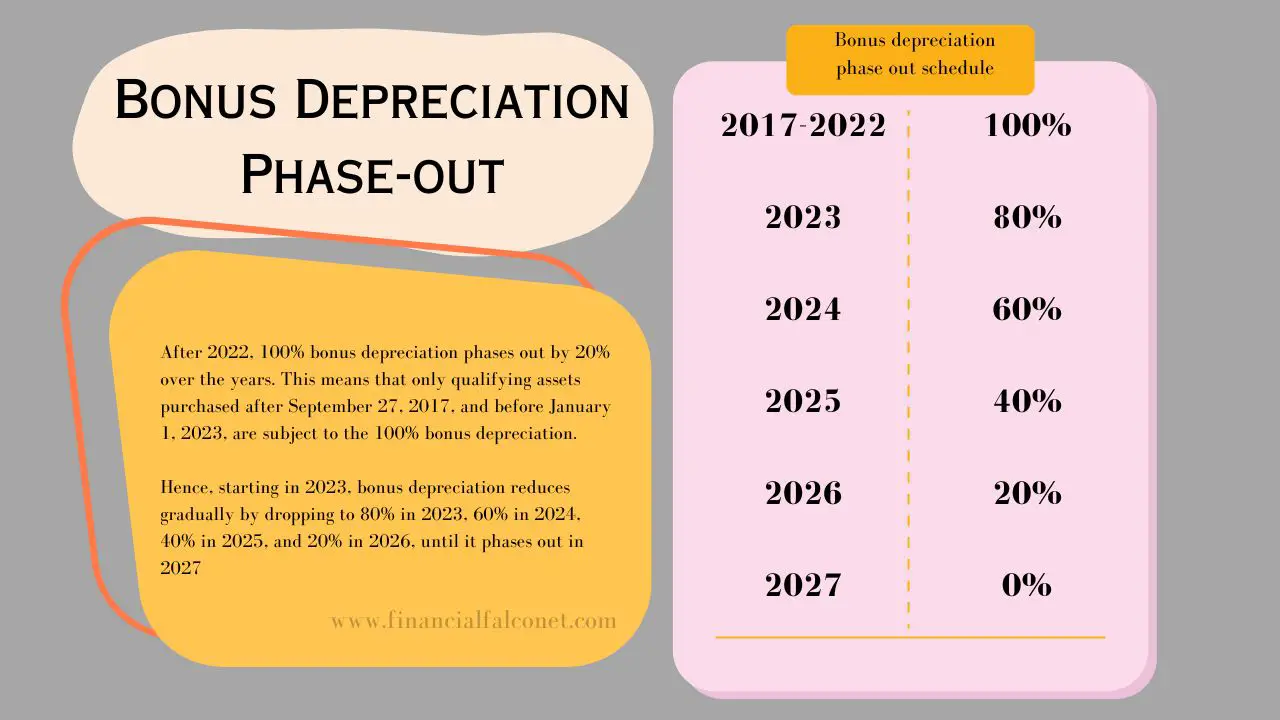

Bonus depreciation phase out schedule

According to the bonus depreciation phase-out schedule, starting with 2023, the bonus depreciation by year reduces by 20%. Taxpayers can only elect to take 100% bonus depreciation on an eligible property that has been purchased and put into use after 2017 and before 2023. However, for other eligible properties placed in service after 2022 and over the next five years, the following bonus depreciation phase out schedule applies:

| The year the asset was placed In service | Bonus depreciation rate |

|---|---|

| 2017 – 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| 2025 | 40% |

| 2026 | 20% |

| 2027 | 0% |

As seen in the bonus depreciation phase out schedule table above, there are scheduled bonus rates assigned for the next coming years. These rates are going to be used for the bonus depreciation calculation in accordance with the year in which the asset was put in service. In order to calculate the deductible bonus depreciation amount, you have to multiply the bonus rate by the cost of the asset. That is, the formula to calculate bonus depreciation is:

Bonus depreciation rate (e.g 80% for 2023) x Cost of the eligible asset

However, before doing this, ensure you must have subtracted any Section 179 expense from the original cost of the asset or reduce the basis of the asset by the applicable percentage of any credits you might have claimed (for instance, energy credit).

Conclusively, in accordance with the TCJA bonus depreciation phase out schedule starting in 2023, the amount of bonus depreciation for assets put in service in tax years 2023, 2024, 2025, and 2026 must be calculated using 80%, 60%, 40%, and 20% respectively (in accordance with the year in question) rather than the initial 100% bonus rate.

Last Updated on November 2, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.