Before companies launch a new product or service, they often need to find the predetermined overhead rate for that particular good or service. Finding the predetermined overhead rate is necessary in order to keep expenses in tandem with both production levels and expected sales. This ensures that businesses price their products and services using the right type of pricing strategy to earn a profit. It also aids companies to monitor their expenses and review them when necessary to continue being profitable. In this article, we shall discuss how to find predetermined overhead rate.

See also: How to calculate bonus depreciation

What is predetermined overhead rate?

The predetermined overhead rate is an allocation rate that is mostly used by manufacturing companies or service providers at the beginning of a particular reporting period to provide an estimate of the expected cost that the company will incur in the course of producing a good or service. This usually involves dividing the estimated manufacturing overhead cost by the estimated units of the allocation base for the particular period.

Manufacturers usually use the predetermined overhead rate in comparison to the actual cost of production to monitor expenses and ensure that costs are not escalating above the desired threshold such that it affects their bottom line. It also aids in setting accurate prices that account for the cost of production while maintaining profitability.

The predetermined overhead rate also aids companies in closing their financial books more quickly as it allows them to avoid compiling actual overhead costs as part of their closing process. However, reconciling the difference between the estimated overhead rate and the actual overhead rate is still important, hence, companies should ensure this is done at the end of each quarter or each fiscal year.

What is the formula for predetermined overhead rate?

The predetermined overhead rate formula is the estimated manufacturing overhead cost divided by the estimated units of the allocation base or the activity driver for the allotted period. This is expressed as Predetermined overhead rate = Estimated manufacturing overhead cost ÷ Estimated units of the allocation base for the period

The estimated manufacturing overhead cost of a company includes all overhead costs associated with the manufacturing process excluding the selling cost, direct labor, administrative cost, or direct materials. Instead, it includes rent, facility maintenance, utilities, factory supplies, and depreciation of equipment. The facility maintenance usually includes all monies spent on keeping the manufacturing facility operational such as janitorial costs or the cost of repairs. Utilities include waste disposal, electricity, and water supply.

The allocation base is a cost accounting descriptor based on the common activity that affects overhead cost. It usually includes costs directly associated with manufacturing or the main activity driver such as the cost of direct labor, hours of machine operation, direct material, or direct labor hours.

See also: How to scale your business

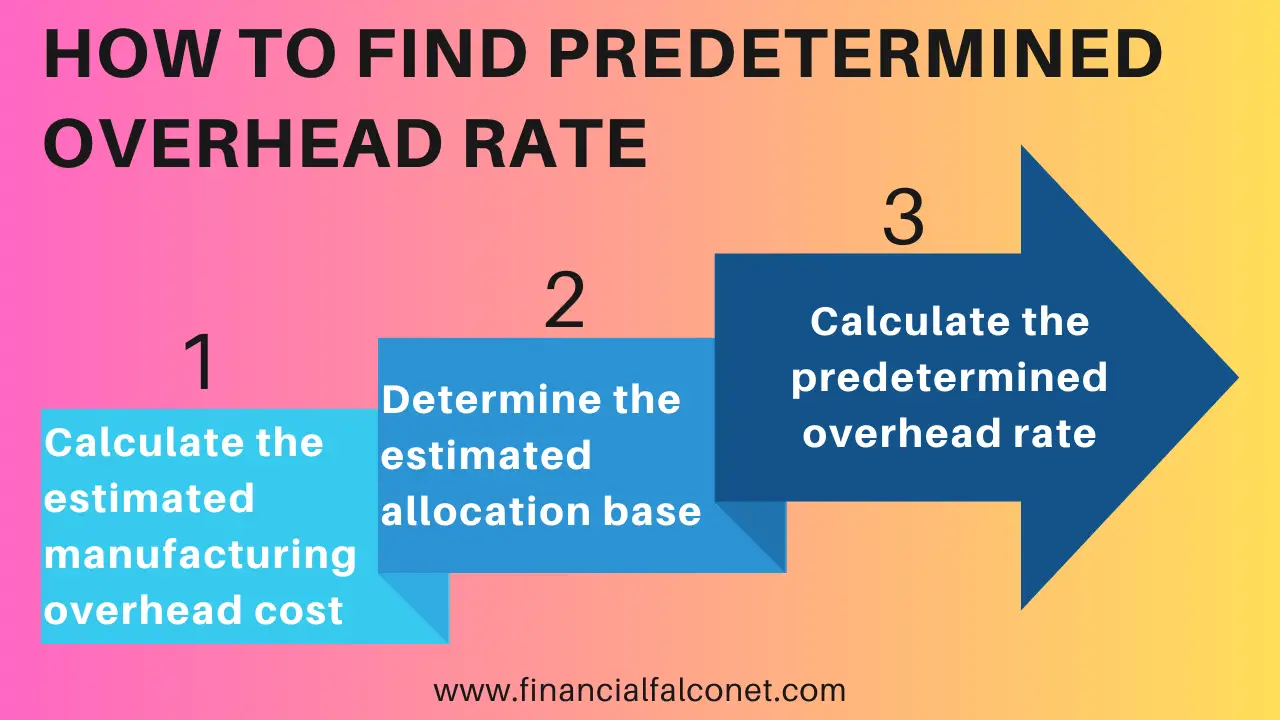

How to find predetermined overhead rate

Finding the predetermined overhead rate is very important as it is used to estimate the future manufacturing cost that may be incurred in the process of producing a good. We shall look at how to find the predetermined overhead rate in 3 simple steps below:

Calculate the estimated manufacturing overhead cost

This involves summing up all expenses associated with overhead costs that are a result of the manufacturing process. They usually include the cost of facility maintenance, factory supplies, utility bills, and depreciation of equipment. In some cases, the salaries of factory workers that are directly involved in the production process such as maintenance workers and factory supervisors may also be included as manufacturing overhead.

Determine the estimated allocation base

The allocation base is usually the main activity driver of the manufacturing process. Hence, it depends on whether the production is mainly a good or service. For factories that produce goods, the cumulative number of machine hours utilized for the good production is used. For services such as construction or car repair, the number of hours needed to complete the project is used.

Calculate the predetermined overhead rate

After determining the manufacturing overhead cost and the allocation base, the last step in finding the predetermined overhead rate is to divide the manufacturing overhead cost by the allocation base.

See also: What does the current ratio inform you about a company?

Predetermined overhead rate examples and calculations

Example 1

Assuming Mr. Reginald owns a bicycle production company and has budgeted the following as cost for the year:

| Item | Value |

|---|---|

| Direct labor hours | 150,000 |

| Direct labor cost | $80,000,000 |

| Property tax | $4,000,000 |

| Supervisor salaries | $40,000,000 |

| Cost of raw materials | $150,000,000 |

| Factory rent | $10,000,000 |

| Depreciation | $6,000,000 |

In order to calculate the predetermined overhead rate we will use the formula, Predetermined overhead cost = Estimated manufacturing overhead cost ÷ Estimated units of the allocation base for the period

Estimated manufacturing overhead cost = Property tax + Supervisor salaries + Factory rent + Depreciation = $4,000,000 + $40,000,000 + $10,000,000 + $6,000,000 = $60,000,000

Estimated units of the allocation base for the period = Direct labor hours = 150,000

Predetermined overhead cost = $60,000,000 ÷ 150,000

Predetermined overhead cost = $400 per hour

This means that the predetermined overhead rate for Mr. Rginald’s bicycle production company is $400 per hour for the year.

Example 2

Miss. Grey is the head of an automobile production company and the company wants to produce a new line of automobiles. In order to ensure that the price of the new automobile is not too high or too low, she has directed the head of production to develop the details of costing based on the overhead cost of their already existing automobiles. After making necessary inquiries and adjustments based on the specifications of the new automobile, the following production cost details were given to Miss. Grey:

| Particular | Units | Amount |

|---|---|---|

| Direct labor hours | 3,000 | |

| Direct machine hours | 10,000 | |

| Direct labor | Based on labor hours | $28,000,000 |

| Direct material | Based on number of units | $40,000,000 |

| Fixed overhead | Based on labor hours | $500,000,000 |

| Variable overhead | Based on labor hours | $189,000,000 |

To calculate the predetermined overhead rate, we will take into account the variable and fixed cost, as well as the direct machine hours since the allocation base we are using, is the machine hours.

The formula we will use is Predetermined overhead rate = Estimated manufacturing overhead cost ÷ Estimated units of the allocation base for the period

Estimated manufacturing overhead cost = Fixed overhead + Variable overhead = $500,000,000 + $189,000,000 = $689,000,000

Estimated units of the allocation base for the period = 10,000

Predetermined overhead rate = 689,000,000 ÷ 10,000

Predetermined overhead rate = $68,900 per hour

This implies that the predetermined overhead rate for the new automobiles based on machine hours is $68,900 per hour

Example 3

Suppose a cable Tv manufacturing company uses its labor hours to assign the manufacturing overhead cost. If the estimated manufacturing overhead cost is $265,000 and the estimated labor hours are 3,000 hours. We can calculate the predetermined overhead rate as follows:

Predetermined overhead rate = Estimated manufacturing overhead cost ÷ Estimated units of the allocation base for the period

Predetermined overhead rate = $265,000 ÷ 3,000

Predetermined overhead rate = $88.33 per labor hour

See also: Asset Turnover Ratio Interpretation and Examples

Conclusion

Finding the predetermined overhead rate is very important for manufacturers as it provides a hint on the overhead of production thereby aiding businesses in understanding and managing costs. It also aids in cost allocation when it comes to budgeting. It also guides the accurate pricing of products to ensure that products are not overpriced or underpriced so as to make optimum profit from products.

Furthermore, the simple steps we have discussed above on how to find the predetermined overhead rate can be easily applied by amateur entrepreneurs, accountants, or seasoned business owners when they want to calculate the predetermined overhead cost of any of their products.

Last Updated on November 2, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.