Is capital debit or credit? Every business requires capital for its startup as well as its sustenance. In other words, capital is critical for the day-to-day running of the business and financing its future growth. It is a vital source of financing a business operation. Business capital can be derived from debt financing, equity financing, and business operations.

The question, “capital debit or credit?” usually arises because there is confusion with regard to whether capital is an asset or a liability since it is beneficial to any business startup and operations. In this article, we see what capital means, whether capital is debit or credit and why, its journal entries, and a few examples.

Related: Debt to Capital Ratio Formula and Interpretation

What is capital?

Capital refers to the financial resources that can be used by businesses to fund their operations. In other words, they are the amount that an owner, partner, or a shareholder invested in a business in the form of assets or cash.

Businesses can raise capital by issuing stocks and bonds to investors who then purchase these financial instruments with cash or other assets.

It is important to differentiate between money and capital because they do not mean the same thing. Capital has more durability than money and it is used to produce something as well as to build wealth. Property rights give value to capital and allow it to generate revenue and build wealth. Equipment, buildings, and land are examples. Also, intangible assets such as patents, trademarks, and brand names.

From the accounting perspective, there are three types of capital namely debt capital, equity capital, and working capital. Although capital is invested in the form of assets, it is still considered a liability. This is so because the business is always faced with the financial obligation to repay the owner of the capital.

It is also important to note that business and capital are two distinct entities. Although it is the sum invested in the business to earn profits, they differ as the investor will always expect returns, not only in the form of profit but also the capital they invested. For this reason, capital is considered a liability to the business from the accounting perspective. In other words, the business is liable to pay back the capital to the investor.

Also, investment and capital are different although people get confused and use these terms interchangeably. While investment is the deployment of funds, capital is the sourcing of funds. it is for this reason that investment is shown on the asset side while capital is shown on the liability side of the balance sheet.

Another reason why capital is considered a liability is the fact that the owner of the capital is different from the business. It is the owner of the business who invests capital into the business. So for this reason, the business is financially liable to the owner.

Having said this, we can see that capital is simply the owner’s claim in the business and liabilities are debts owed by the business to external and internal stakeholders. In essence, this capital that is always a liability to the business can take two forms namely internal liability and external liability.

According to the accounting equation, liabilities are the difference between assets and capital (shareholders’ equity). Generally, it is expected that since capital adds value to the business or is used to start an enterprise, it should be an asset and not a liability. In accounting, this is not so, as explained above.

Related: What is Financial Leverage? Types and Example

Meaning of debit and credit

In double-entry bookkeeping, debits and credit are entries that are made in accounting ledgers to record the changes that occur in values as a result of business transactions. A debit entry represents a transfer of value to an account while a credit entry represents a transfer of value from an account. Therefore, each transaction take takes place and transfers value from credited accounts o debited accounts. For instance, value can be transferred from a company’s capital account to the investors’ or lenders’ accounts.

Traditionally, debits and credits are distinguished by writing the transfer amounts in separate columns of an account book. Debits are in the left column and credits at the right column. When the total of debits in an account is greater than the total of credits, we would say that the account has a net debit balance that is equal to the difference. When this applies to the opposite, we would say that the account has a credit balance.

In double-entry, five types of nominal accounts exist namely income accounts, expense accounts, asset accounts, liability accounts, and capital accounts. Debit balances are usually for asset and expense accounts while credit balances are normal for liability which may include capital, equity, and revenue accounts. In other places, we would see that shareholders’ equity is also the capital that a business used in financing its operations.

So in a nutshell, there is a need to debit some accounts and credit some accounts in order for one to increase the amount in his business accounts. For accounts such as income, liability, and capital, a credit brings about an increase in their balances while a debit brings about a decrease in their balances. On the other hand, for accounts such as expenses and assets, a debit brings about an increase in their balances while a credit brings about a decrease in their balances. For the accounts to be in balance, the debit side has to be equal to the credit side.

Having explained what capital implies and debit and credit in relation to capital, let us look at whether capital is debit or credit and why.

Related: Sales Debit or Credit?

Capital debit or credit?

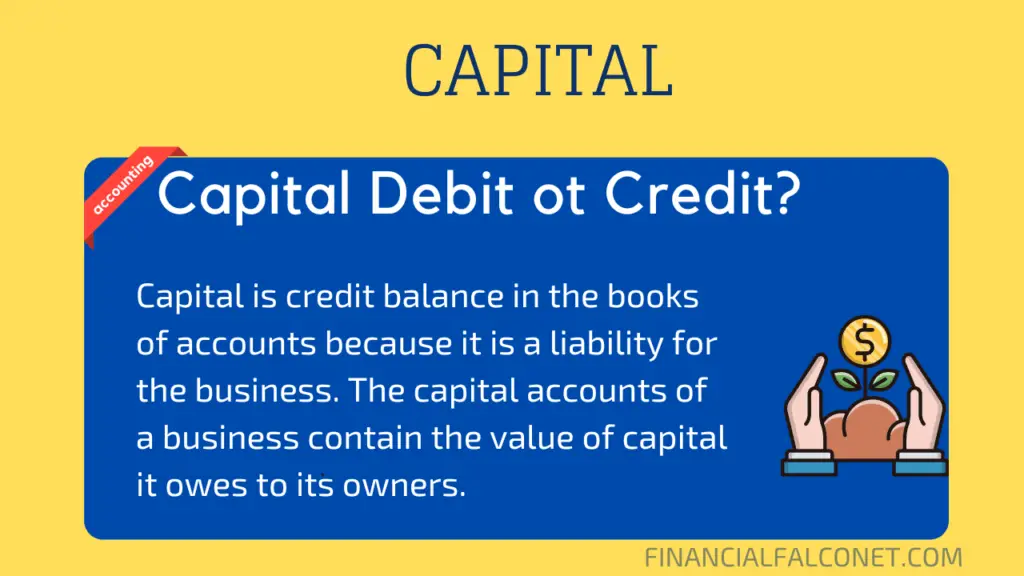

Capital is not a debit but a credit balance in the books of accounts. This is simply because it is a liability for the business. The capital accounts of a business contain the value of capital it owes to its owners.

To have a more comprehensive understanding, there is a need for one to get familiar with the Golden and Modern rules of accounting which are designed to explain the debit and credit relationship as explained above.

When there is a debit to a capital account, it is an indication that the business does not owe much to its owners, that is, a reduction in the business’s capital. On the other hand, credit to a capital account is an indication that the business owes more to its owners, that is, an increase in the business’s capital.

For example, a limited liability company will always be owned by the same person or group of people, so the directors and shareholders will be the same individuals. If the business is an LLC or LLP, the amount of profit that the business made in previous years and has not been paid out to shareholders or members is also a capital account. This is because it is money that could theoretically be taken out by the owners.

If one is a shareholder-director, then the money that he spent on shares in the company will go into the capital account, usually referred to as the share capital. Any other money that is owed by the company such as unpaid wages or costs that were personally paid for will do into the director’s loan account, which is a liability account of the business

Capital accounts usually appear at the bottom of the business’s balance sheet. The figure in the capital accounts will always be equal to the amount in all the asset accounts less the amount in all the liability accounts, as it is in the accounting equation. This is because if the business sold all its assets to pay all its debts, the difference would be left over for the business owner to keep.

Therefore, the capital account should have a credit balance which represents the amount of money that the business owes to its owner. If a capital account ever has a debit balance, then it is an indication that the business is insolvent. In the case of sole proprietorship and partnership businesses, the capital account is credited by business profits and debited to the business losses. Then, any money or business property that is removed from the business by the owner will be classified as drawings which will also be debited to the capital account.

In the case of a company, capital refers to the share capital which is the amount that the owners invested in the company and is not changed by profits or losses. An equity account represents the amount the business owes the company and it serves a similar purpose to the sole proprietor’s capital account.

Debit and credit journal entries for capital

We have considered why a capital account is a credit balance, looking at the fact that capital in accounting is treated as a liability. The golden accounting rule states that debit is the receiver while credit is the giver. In making journal entries for capital, the cash account will be debited while the capital account is credited as follows:

| Account | Debit | Credit |

|---|---|---|

| Cash | 00 | |

| Capital | 00 |

Example

A sole proprietor invested $50,000 as capital. The journal entries in his books of accounts are:

| Account | Debit | Credit |

|---|---|---|

| Cash | 50,000 | |

| Capital | 50,000 |

The capital account is credited as the business is liable to repay the invested amount to the proprietor. So in the modern rule, a debit decreases the capital account balance while a credit decreases the same.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.