Assessing the amount of overhead cost that can be allocated to each production process can be tough. This is why an overhead rate is calculated to estimate the overhead costs for each cost driver or activity. Overhead costs can be allocated to the direct costs such as direct labor costs that are tied to production to determine the overhead rate per direct labor cost.

Overhead costs can be allocated at a set rate that is based on the direct labor hours, machine hours, or direct labor costs needed for the product. This calculation helps in the appropriate pricing of a product or service because a business will not make a profit if it prices so low that its revenues do not cover its overhead costs. In this article, we will discuss how to calculate the overhead rate per direct labor cost and its formula.

Related: How to Find Predetermined Overhead Rate

Overhead rate per direct labor cost explained

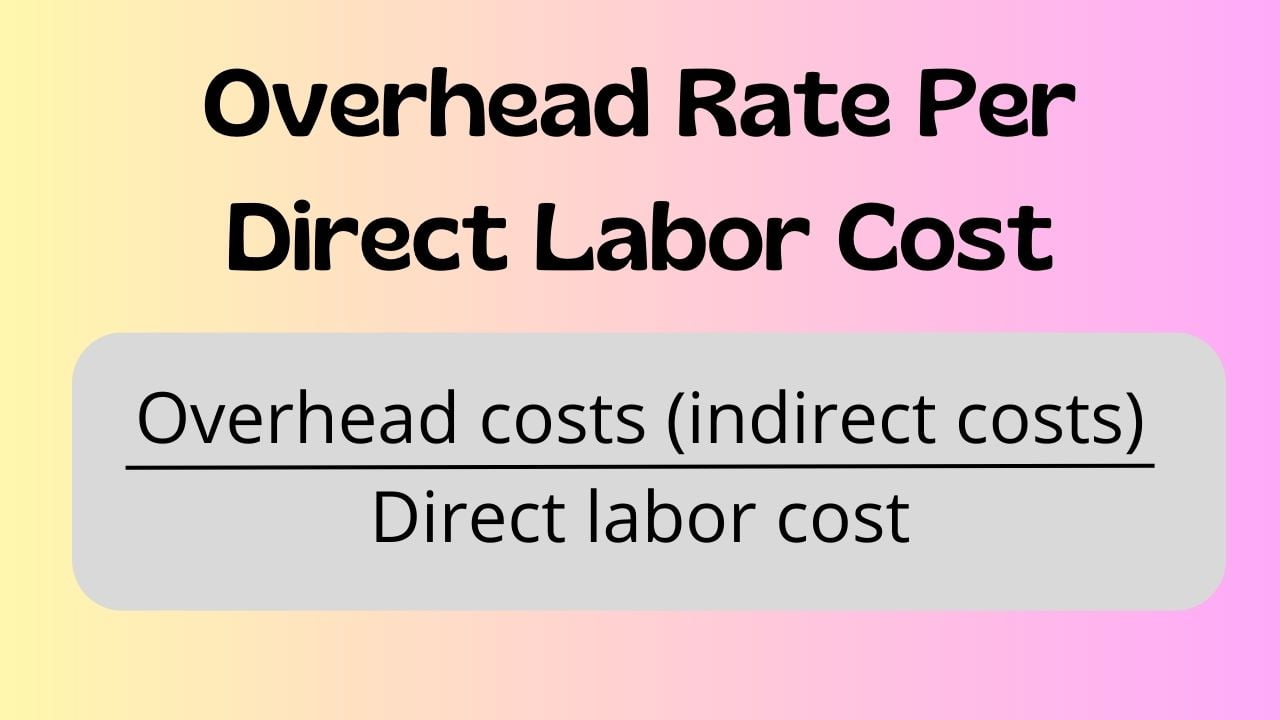

Overhead rate is the ratio of the overhead costs (indirect costs) for a specific reporting period to the allocation measure for that period. This involves summing up a company’s indirect costs that are not allocated to a single activity and then, dividing it by the allocation measure which can be direct labor costs, machine hours, or direct labor hours.

Hence, one of the ways to measure an overhead rate is to divide the total overhead cost by the total direct labor cost for a specific reporting period; the resulting figure is what is known as the overhead rate per direct labor cost. For many companies, the overhead rate per direct labor cost won’t be a very telling metric, but for agricultural operations, packing plants, and manufacturers with multiple dedicated product lines, calculating this ratio can be very handy.

When estimated or budgeted amounts are used to calculate the overhead rate, it is also known as the predetermined overhead rate. Knowing how to calculate the overhead rate per direct labor cost enables businesses to have a better understanding of the costs that are associated with manufacturing a product or rendering a service. Once a business is informed about how much overhead cost is associated with each product it makes, it can add the cost to the price of the product in order to make a profit.

Therefore, businesses determine the overhead rate in order to price their products appropriately and accurately assess profitability. The calculation of the overhead rate per direct labor cost has a basis for a specific period. This means that, if a business wants to determine the overhead rate for a week, for instance, it would have to sum up its weekly indirect costs and then measure the total direct labor cost for production in the same period.

That is, the total direct labor cost for the week would be the denominator. Hence, the total indirect cost for the week would be divided by the direct labor cost to determine how much in overhead costs for every dollar spent on the direct labor for the week. Measuring and tracking this rate is essential to gauge how a business’s administrative costs are evolving over time; helps to ascertain whether the business is being overburdened with administrative costs instead of profit-producing activities.

See also: Process Costing System- Examples, Methods, and Steps

Overhead rate per direct labor cost formula

There are multiple ways to calculate an overhead rate, but we are focusing on calculating an overhead rate based on direct labor costs. The general formula for overhead rate is the overhead costs divided by the allocation measure or activity driver (direct labor cost, machine hours, or direct labor hours). Hence, the overhead rate per direct labor cost formula is expressed as:

Overhead rate per direct labor cost = Overhead costs (indirect costs) / Direct labor cost

Where;

- Overhead costs= The Indirect costs that are not directly tied to the production of a product or service.

- Direct labor cost= The expenses, such as wages, salaries, fringe benefits, and payroll taxes that are incurred in order to produce goods or provide services

Read about: When to use process costing

How to calculate overhead rate per direct labor cost

Knowing how to calculate overhead rate per direct labor cost gives a better understanding of the costs that are associated with manufacturing a product or rendering a service. Here are the basic steps to calculating overhead rate:

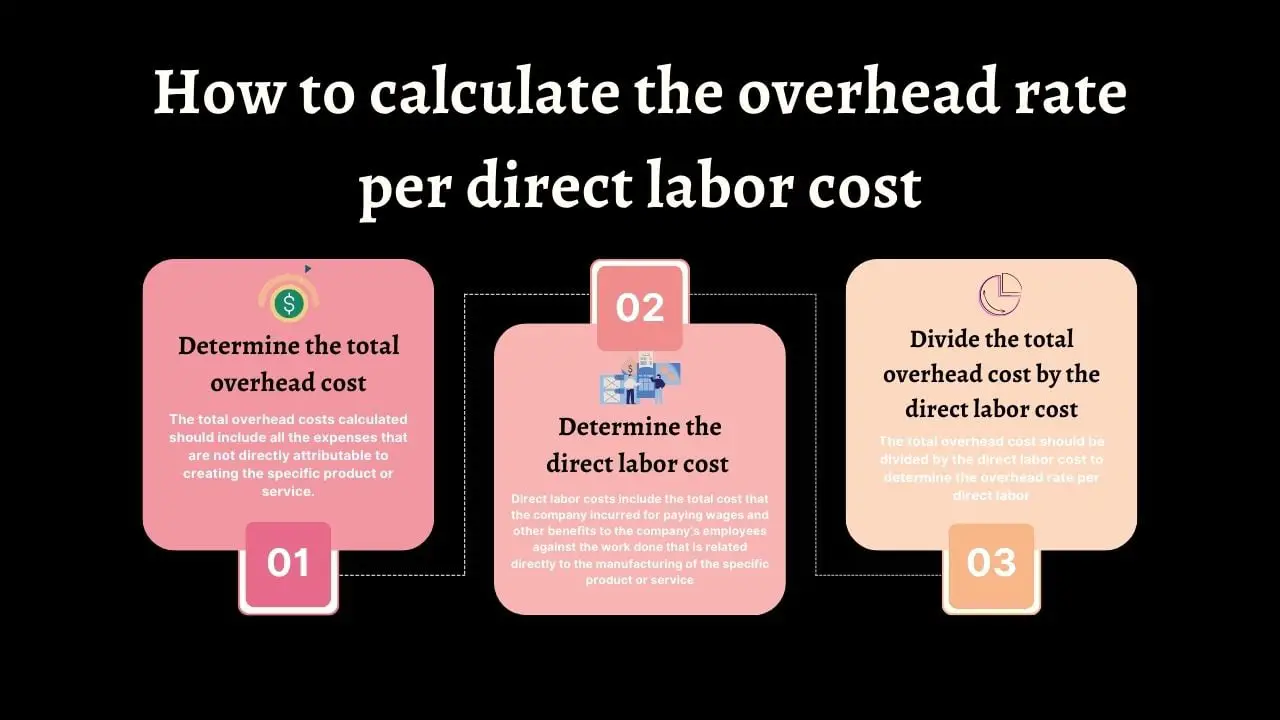

Determine the total overhead cost for the specific reporting period

The first step to calculating overhead rate per direct labor cost is to calculate the total overhead costs for the specific reporting period. This involves the indirect costs that are incurred whether or not a company manufactures a product or a retail store sells a single product. That is, overhead costs include fixed costs like building or office space rent, utilities, supplies, insurance, maintenance, and repair.

Overhead costs also include some expenses that are tucked under selling, general, and administrative (SG&A) on the company’s income statement. That is, the total overhead costs calculated should include all the expenses that are not directly attributable to creating the specific product or service.

Determine the direct labor cost for the specific period

The next step to calculating the overhead rate per direct labor cost is to calculate the direct labor costs for the specific reporting period. Direct labor costs include the total cost that the company incurred for paying wages and other benefits to the company’s employees against the work done by them; the work done is related directly to the manufacturing of the specific product or service.

Divide the total overhead cost by the direct labor cost

The final step to calculating the overhead rate per direct labor cost is to divide the total overhead cost by the direct labor cost. Once the indirect costs are summed up, and the sum of the direct labor cost has been determined, the resulting figures should be entered into the overhead rate per direct labor cost formula below:

Overhead rate per direct labor cost = Overhead costs (indirect costs) / Direct labor cost

See also: Profit Margin Calculation, Formula, and Examples

Examples of overhead rate per direct labor cost calculation

Let’s look at some examples to further explain how to calculate overhead rate per direct labor.

Example 1: how to calculate overhead rate per direct labor cost

ABC Company wants to know how much indirect costs relate to its direct labor costs for a specific period. Supposing, the company has total overhead expenses of $20 million for the period and direct labor expenses summing up to $5 million for the same period; here is how to calculate the overhead rate:

Solution

Using the overhead rate per direct labor cost formula:

Overhead rate per direct labor cost = Overhead costs / Direct labor cost

= $20 million / $5 million

= $4

This means that it costs ABC Company $4 in overhead costs for every dollar in direct labor costs.

How to calculate overhead rate per direct labor cost example 2

For this example, let’s assume a manufacturing company that makes one line of products incurs the following expenses:

- Annual rent- $25,000

- Utilities- $10,000

- Materials to manufacture the products- $100,000

- Machine maintenance- $15,000

- Packaging & transportation for the products- $18,000

- Salaries and benefits to administrative staff- $200,000

- Hourly pay to workers in the plant- $180,000

Here is how to calculate the overhead rate per direct labor cost:

Solution

First, we will calculate the total overhead cost for the year. This would involve the costs that are not attributable to the company’s product line such as the annual rent of $25,000, utilities of $10,000, and salaries & benefits to administrative staff that amounted to $200,000. That is, the total overhead costs would be calculated as:

Overhead costs = $25,000 + $10,000 + $200,000 = $235,000

This means that even if the company stopped production tomorrow, it will still incur $235,000 in business expenses if it wanted to stay operational, but would stop incurring the other costs on the lists that are attributable to the company’s product line.

The direct labor cost amounted to $180,000 which is the hourly wages paid to workers in the plant. Hence, using the overhead rate per direct labor cost formula:

Overhead rate per direct labor cost = Overhead costs / Direct labor cost

Overhead rate per direct labor cost = $235,000 / $180,000

= $1.305

This means that it costs the manufacturing company $1.3 in overhead costs for every dollar in direct labor costs.

How to calculate overhead rate per direct labor cost example 3

The overhead rate can also be expressed as a proportion, as far as the numerator and denominator are in dollars. Take for instance, Financial Falconet has total indirect costs of $100,000, and calculating its overhead rate, it chooses to use the cost of its direct labor as the allocation measure. Assume, this company incurs $50,000 of direct labor costs, the overhead rate per direct labor cost would be calculated as:

Solution

Using the overhead rate per direct labor cost formula:

Overhead rate per direct labor cost = Overhead costs / Direct labor cost

= $100,000 / $50,000

= $2 or 2:1

This means that Financial Falconet has an overhead rate of 2:1 and it costs the company $2 of overhead costs for every $1 of direct labor cost incurred.

Last Updated on November 2, 2023 by Nansel Nanzip Bongdap

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.