When investing in financial securities such as stocks, bonds, and stock options, investors want to know about the particular security before investing in it.

The primary function of the capital market is to distribute ownership of the capital stock of the economy. Ideally, stock prices should provide accurate signals for resource allocation, meaning that firms can make informed decisions about production and investment, and investors can choose from among the securities that represent ownership of firms’ activities.

This is based on the assumption that security prices are fully reflective of all available information at any given time. A market that consistently exhibits this characteristic is referred to as being efficient.

The EMH asserts the unpredictable nature of markets and how the available information on assets usually determines their price in the market. Before we discuss the different types of efficient market hypotheses, let us understand what the efficient market hypothesis is all about.

See also: Stock Valuation Formula and Methods

What is the efficient market hypothesis?

The efficient market hypothesis (EMH) is a financial economics hypothesis linked to Eugene F. Fama’s 1970 work titled, “Efficient Capital Markets: a Review of Theory and Empirical Work.” The hypothesis states that the price of assets reflects all relevant and available information about the asset.

It was developed to explain why changes in the price of securities appear to be random, thereby making it impossible to accurately predict future changes in security prices based on historical price movements.

Hence, it indicates that it is impossible to consistently beat the market because market prices should only react to new information. The efficient market hypothesis is otherwise referred to as the efficient market theory.

See also: Overvaluation of Stock

What are the three assumptions of the efficient market hypothesis?

The three assumptions of the efficient market hypothesis are that there is equal access to all available information, investors are rational, and stock prices change randomly. These assumptions ensure that the efficient market hypothesis holds true.

When all investors have equal access to all available information, whether public or private as well as access to historical information on the stock prices, it provides the same opportunity to everyone.

This implies that no investor has an undue advantage in the market due to having access to privileged information, instead, all investors have the same level of access to all information.

For instance, if a company is considering a merger with another company, the merger is most likely going to affect its stock price. Because of this, the company is expected to make such information public. Hence, for the efficient market hypothesis to hold true, all investors should have access to this information.

Therefore, it is generally impossible to consistently beat the market by investing in and receiving returns that are significantly higher than the market average over a long period.

The rationality of investors is another assumption of the efficient market hypothesis. By this, all investors are considered rational, such that when presented with an investment, they look out and invest in assets with lower risks and higher returns.

For example, when presented with two investment options that have the same rate of returns at 10% per annum and differing risks, a rational investor is expected to invest in the one with a lower risk.

The third assumption on the random changes in stock prices implies that past trends, even when closely monitored do not provide adequate patterns upon which one can rely to make future predictions on the stock’s future price movements.

It therefore means that investors cannot use fundamental or technical analysis to aid them in deciding what assets they should invest in.

In reality, however, the efficient market hypothesis does not always hold true because, despite the criminalization of insider trading, some individuals and organizations will always have access to privileged information that confers them with the ability to make certain decisions that benefit them.

Additionally, some investors have a high-risk appetitive and may choose a riskier investment when presented with differing choices, especially when it has a higher return rate. Furthermore, despite the random changes in stock prices, some investors are still able to make lucky guesses based on previous observations of the market trends and may beat the market for a significant period.

See also: What is Financial Leverage? Types and Example

What are the 3 forms of efficient market hypothesis?

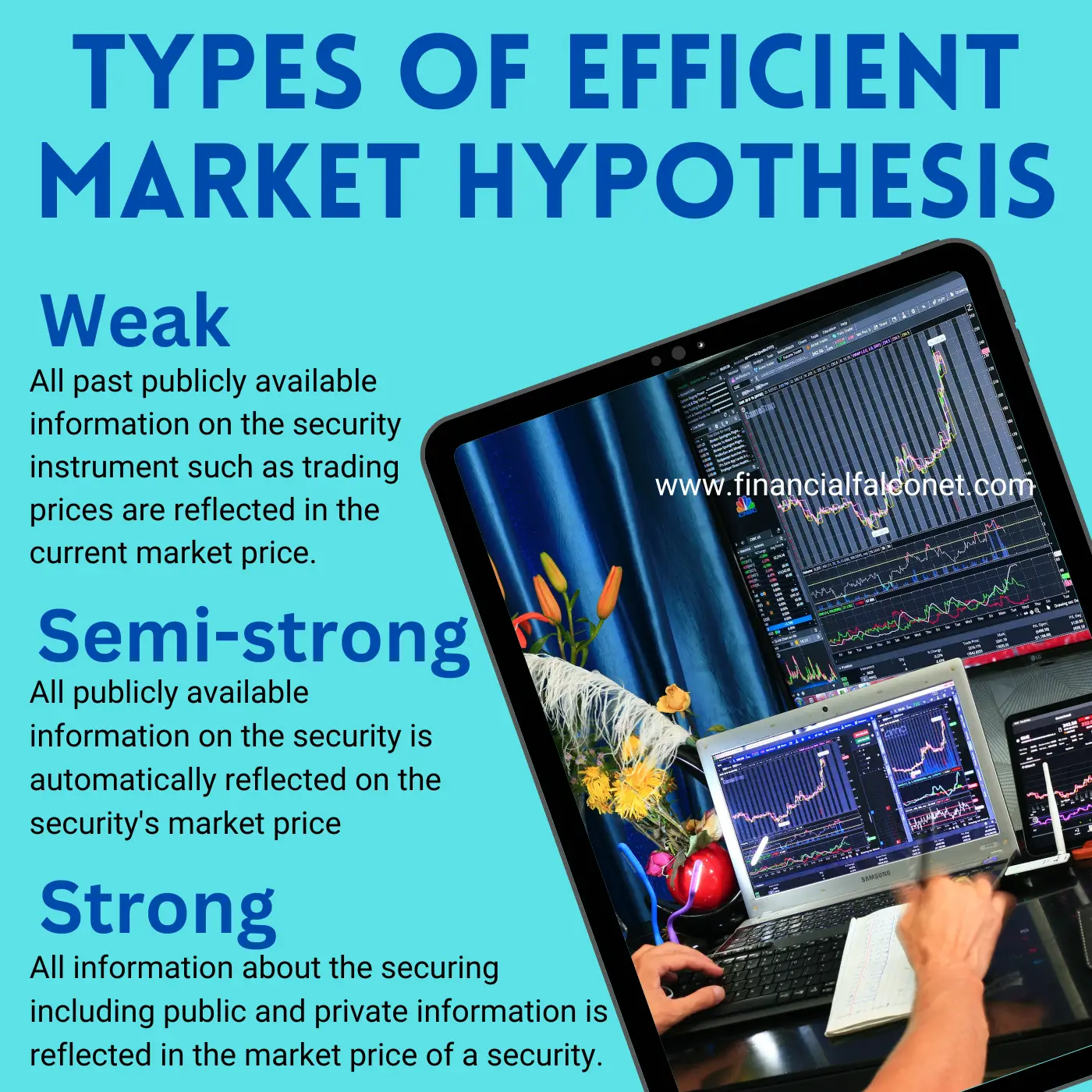

The three (3) forms of the efficient market hypothesis are the weak, semi-strong, and strong form.

Types of Efficient Market Hypothesis (EMH)

- Weak

- Semi-strong

- Strong

Weak form efficient market hypothesis

The weak type of efficient market hypothesis suggests that the current market price of a security reflects all past publicly available information related to the market. It does not reflect any information that has not been made public in the past.

This means that if for example a company is planning to buy back some of its common stock, but has not made the information public, the price at which its stocks trade on the stock market will not reflect this information.

Weak EMH also assumes that historical information on pricing and returns earned have no direct impact on the future price and returns associated with the security. Hence, technical analysis of the stock is of no use as it will not provide one with set patterns on price or returns movement.

It however acknowledges the possibility of investors gaining short-term advantages in the form of returns that are higher than the market average when they use fundamental analysis to find out more information on the security.

Semi-strong EMH

The semi-strong efficient market hypothesis asserts that the market price of securities makes quick adjustments to reflect any new public information.

This means that if for instance, a company uses part of its retained earnings to pay dividends to its stockholders, once an announcement is made about the dividend payment, the market price of that stock will self-adjust to reflect the new publicly available information.

Thus, both technical and fundamental analysis does not provide an investor with any advantage in this scenario.

Strong form efficient market hypothesis

This type of efficient market hypothesis states that the current price of a security reflects all past information as well as current information about the security.

This includes both information that has been publicly disclosed as well as insider information that is only available to a few individuals such as a company’s Chief Executive Officer (CEO) or its board of directors.

Therefore, it suggests that no investor can gain an advantage over the market as a whole. It, however, does not completely negate the possibility that there may be outliers who may gain an advantage and get above-average returns but that is generally tied to luck and not any available information.

Summary of the types of efficient market hypothesis

| Form of EMH | Information reflected | Analysis ruled out |

|---|---|---|

| Weak | All past publicly available information on the security instrument such as trading prices are reflected in the current market price. | Technical analysis |

| Semi-strong | All publicly available information on the security is automatically reflected on the security’s market price | Technical and fundamental analysis |

| Strong | All information about the securing including public and private information is reflected in the market price of a security. | All types of analysis |

Implications of the efficient market hypothesis (EMH)

The efficient market hypothesis has different implications for individuals, portfolio managers, companies, and governments.

For individual investors, it implies that earning an above-average return is only possible for a short time but not consistently over a long period. Thus, investing in a low-risk, well-diversified portfolio that mirrors the market is more beneficial in the long run.

For portfolio managers, it implies that although active management strategies may provide some advantages in the short term, they cannot outperform passive management strategies consistently, hence, EMH discourages the pursuit of supposed undervalued stocks intending to beat the market.

For companies, the efficient market hypothesis implies that its stock price at any given period will always be fairly priced and company decisions such as the payment of dividends, buyback of shares, stock splits, mergers, and other financial decisions will have no effect on the company’s value.

For governments, EMH justifies the criminalization of insider trading and promotes transparency and information dissemination associated with securities and other assets.

Conclusion

The varying types of efficient market hypotheses all reecho the impossibility of consistently beating the market. They also support making all information concerning securities publicly available such that the prices of securities reflect this information.

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.