What type of account is sales returns and allowances? Although goods are sold to customers, not all customers are satisfied with these goods due to some reasons like product defects. This may cause them to return these goods to the seller or bring about a situation whereby the seller offers to leave the goods for the customer at a reduced selling price, which the buyer may agree to keep.

Sales returns and allowances are two different transactions, however, they are recorded in the same account. Usually, this happens when the balances of these accounts are relatively small. With this, there is no point in tracking sales returns and allowances separately.

What are sales returns and allowances?

Sales returns and allowances imply a deduction from sales that shows the sales price of goods that customers returned as well as the discounts they took to retain defective goods. When this figure becomes large, it is an indication that a business is having trouble when it comes to shipping goods of high quality to its customers.

Sales returns and allowances come about when customers return goods they purchased to get their cash refunded or are allowed to keep the products without paying for them (or paying for them at a discounted rate). Although a customer may want to return goods to its seller for a large variety of reasons. Regardless of the reasons, there is a need for the business to account for the returns correctly. This includes cash refunds to customers and keeping the accounting records up to date.

If Music World returns merchandise worth say $100, Music Suppliers, Inc., prepares a credit memorandum to account for the return. This credit memorandum will then become the source document for a journal entry that brings about an increase (debits) in the sales returns and allowances account and decreases (credits) in accounts receivable.

Now, let us look at sales returns and allowances separately:

Sales returns

A sales return, otherwise known as returns inwards, is a situation whereby a customer returns the products purchased by them and receives a refund for the purchase price. This usually happens for different reasons such as product defects, a change of mind by the customer by deciding not to like the product, the product being outside the customer’s expectations, the wrong size of the product, the product arriving damaged, etc.

Whatever the case it is, the aim at which the customer returns the good is to receive a refund. When this happens, it is expedient for businesses to keep track of sales returns in order to keep their accounting records up to date. This will help in avoiding any errors in the financial statements and records.

Allowances

Sales allowances refer to a situation whereby a customer is allowed to keep the product without paying for it or without paying the full amount owed for the entire purchase price. As it is with sales returns, there are varieties of reasons why a business gives sales allowances to customers. These reasons as stated under sales returns are defective products, the customer changing their minds, product damage, etc.

In each case, the buyer is still allowed by the business or seller to keep the product and they are not required to pay for the product or continue paying for it. In other words, the buyer does not send the merchandise back to the seller but receives a reduction or discount in the total amount that has to be paid to the seller for the order.

Related: What Type of Account is Cost of Goods Sold?

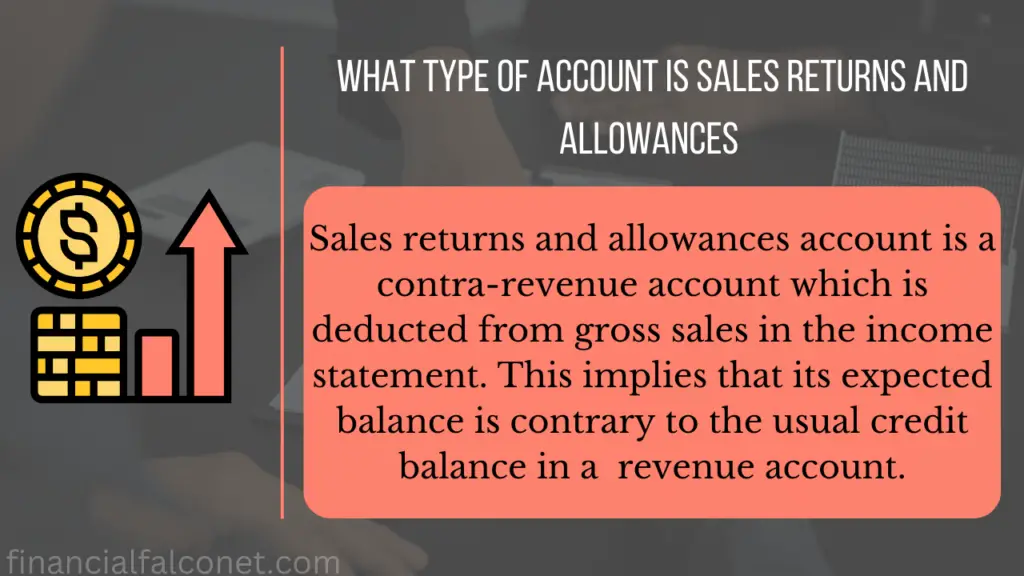

What type of account is sales returns and allowances?

The Sales Returns and Allowances Account is a contra-revenue account, which is deducted from sales or gross sales in the income statement. A contra-revenue account is a revenue account that is expected to have a debit balance rather than the usual credit balance. In other words, its expected balance is the opposite of or contrary to the usual credit balance in a revenue account. This account allows a company to see the original amount sold and also see the items that brought about a decrease in the sales to the amount of net sales.

As earlier stated, sales returns come about when customers return goods to the seller because they are defective or the wrong products were delivered, while sales allowances come about when the customer agrees to keep products at a price that is lower than the original price.

In the sales revenue section of an income statement, the sales returns and allowances account is subtracted from the actual sales because these accounts have the opposite impact on net income. This, therefore, simply explains why this is considered a contra-revenue account, which has a debit balance on a normal note.

When management records sales returns and allowances in a separate contra revenue, it allows them to monitor returns and allowances as a percentage of overall sales. As earlier stated, a high level of returns is an indication of the presence of serious problems, however, these problems are correctable.

For example, an improvement in packaging might minimize damage during shipment, new suppliers might work toward reducing the amount of defective merchandise, or better methods adopted for recording and packaging orders might either eliminate or reduce incorrect merchandise shipments. The first step taken in order to identify such problems is to carefully monitor sales returns and allowances in a separate, contra-revenue account.

In the income statement, accountants deduct Sales Returns and Allowances from sales alongside Sales Discounts which in turn arrive at Net Sales. In cases whereby only “Net Sales” is presented in the income statement, its computation is shown in notes to financial statements.

In accounting for sales returns and allowances, the line item is the two general ledger accounts which are the sales returns account and the sales allowances account. Both are contra accounts which means that they offset gross sales.

Related: What Type of Account is Sales Discounts?

Journal entries for sales returns and allowances

It can be tricky when it comes to accounting for sales returns and allowances but no worries. Once one gets the hang of which accounts to increase and decrease, then purchase returns and allowances can be recorded in the books. These responsibilities are dependent on how the original purchase was made and how reimbursing the customer was planned.

However, regardless of how the customer paid for the goods, the need for one to update his sales returns and allowances account remains unchanged. This account represents the goods returned to a business. As a contra-revenue account, the sales returns and allowances account opposes the revenue account from the initial purchase. This means that one must debit sales returns and allowances account to reflect the decrease in revenue.

In the journal entries, the amount is removed from the accounts receivable balance by crediting the customer’s account (for credit sales or sales on account).

| Accounts | Debit | Credit |

|---|---|---|

| Sales returns and allowances | 00 | |

| Accounts receivable | 00 |

If the return allowance has to do with a refund of a customer’s payment, the cash account will be credited or a payable account will be credited if the refund will be made at a future date.

| Accounts | Debit | Credit |

|---|---|---|

| Sales returns and allowances | 00 | |

| Cash or payable to customers | | 00 |

Examples

1) Johnny Diary Co. sold 1,200 bottles of milk to Mr. Teddy for $0.50 per bottle. On the account, the journal entry to record the sale would be:

| Accounts | Debit | Credit |

|---|---|---|

| Accounts receivable | 600 | |

| Sales | | 600 |

Later on, Mr. Teddy returned 6 boxes containing 300 bottles because they were expired. It is apparent that Johnny Diary Co. sent some wrong boxes to the customer. Johnny Diary agreed to deduct the amount from the customer’s account. The journal entry will be as follows:

| Accounts | Debit | Credit |

|---|---|---|

| Sales returns and allowances | 150 | |

| Accounts receivable | | 150 |

2) Linkage Enterprise sold a computer set to Daniel at $1,050. Daniel later returned the product after discovering that there was a missing part. However, he agreed to accept the product after Linkage Enterprise refunded $100. The journal entry to capture the sales adjustment will be as follows:

| Accounts | Debit | Credit |

|---|---|---|

| Sales returns and allowances | 100 | |

| Cash | | 100 |

Note that some companies do not maintain a sales returns and allowances account, rather, they record customer returns by simply debiting sales. However, it is good to maintain sales returns and allowances account in order to be able to track returns and allowances as well as to make decisions about them if necessary.

Related: Accumulated Depreciation is What Type of Account?

Does sales returns and allowances get closed?

Sales returns and allowances accounts get closed because they are temporary accounts. The balances in these temporary accounts are transferred to the permanent account in the balance sheet, and these entries are made at the year-end. The temporary balances are zeroed out in order for the balances of the new year to flow into those accounts. In other words, these accounts are closed at the end of every accounting period in order to reset the balances of revenue, expense, and withdrawal accounts and prepare them for the next accounting period.

Are sales returns and allowances an expense?

Sales returns and allowances are not considered expenses. Rather, they are a reduction of sales revenue and are deducted from sales revenue while calculating net sales.

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.