Testing for the completeness of accounts payable is one of the procedures carried out by organizations to help ensure that all goods or services received on credit are accurately captured.

In this way, transactions get recorded within the correct period and the amount owed is also accurately recorded. This ensures that all creditors and suppliers get paid the right amount when due.

It also serves as a means of mitigating duplicate payments as well as reconciling the accounts payable records with payments. It is additionally one of the steps carried out by auditors when they audit the accounts payable.

Before we discuss how to test the completeness of accounts payable, let us understand what accounts payable is.

Read about: Decrease in accounts payable debit or credit?

What are accounts payable?

Accounts payable, which is commonly abbreviated as AP is a liability account that records the money a business organization owes service providers or suppliers. It is the company’s credit obligations for goods or services collected that have not yet been paid for.

The accounts payable is usually a short-term debt that is expected to be paid within a year. Most credit purchase contracts normally have payment terms stipulating the expected period of payment, normally within 30 – 90 days from the date of purchase.

When a company purchases a good or product on credit and cannot complete payment within the expected time frame, the company is said to be in default.

As a means of temporarily increasing their cash reserves, some companies wait until the latest authorized dates to settle their outstanding accounts payable. One disadvantage of this delayed payment of the outstanding AP is that the company may not benefit from a sales discount.

This is because, in most instances, sales discounts apply only to early payments. Additionally, late payment may lead to an additional payment on the amount owed in the form of a late fee.

An increasing AP balance indicates that a company purchases most of its products and services on credit while a decreasing AP balance indicates that the company has been consistently paying its debts.

A decreasing accounts payable balance further indicates that the company has reduced its use of credit in making purchases, or that it takes a longer interval between payments and new purchases on credit.

When a company has a low accounts payable balance, it increases its credit ratings because it indicates that it does not owe suppliers and creditors a large sum. It also indicates that the company pays its debts efficiently.

The accounts payable are recorded in several financial records of companies including the accounts payable subledger, general ledger, and balance sheet.

Read about: Is Accounts Payable an Asset or Liability?

How to test the completeness of accounts payable

Testing for the completeness of accounts payable is one of the mandatory steps when auditing the accounts payable. This step ensures that all owed monies are rightly captured.

The completeness of the accounts payable is checked by the auditing team whenever they are carrying out an audit of the accounts payable.

In most instances, the completeness of the accounts payable is checked annually before a company prepares and files its financial reports or before a financial audit is done.

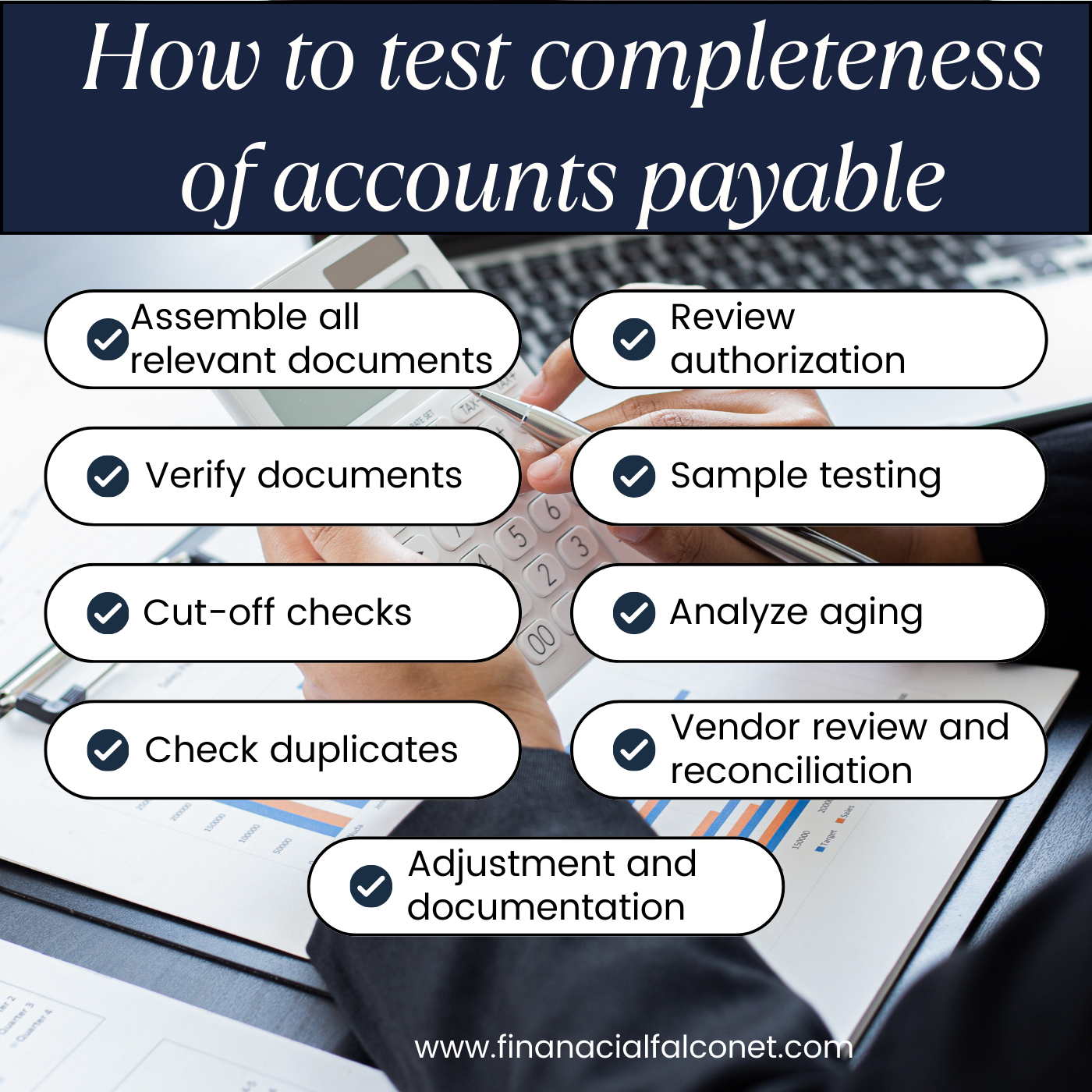

Assemble all relevant documents

Before the completeness of the accounts payable can be tested, the first step taken requires assembling all relevant documents such as orders, invoices, purchase contracts, and payment receipts.

These documents are important because they provide a trial for all transactions carried out which adds to the overall accounts payable balance.

Review authorization

For every purchase order, invoice, contract, or payment receipt, there are usually approved personnel who need to make authorization.

When testing for completeness, all documents must have the right authorization such as the required stamps or signatures to indicate their authenticity.

Verify documents

At this stage of testing for the completeness of the accounts payable, documents are matched side by side to ensure that each transaction has all necessary documentation.

For instance, if a company spent $30,00 to purchase a machine, there should be corresponding documents tracing its order right to the payment.

This means there should be a machine order, invoice from the supplier, purchase contract if applicable, and payment receipt for the transaction.

Sample testing

Due to the large volume of transactions that are carried out by most companies, it may be impossible to track all transactions individually. Thus, sample testing of transactions is carried out.

The sample testing entails reviewing select purchase orders and checking to ensure that all documents for a particular transaction are properly recorded.

This helps ensure that there is a traceable paper or electronic trail for the accounts payable transactions.

Cut-off checks

This is one of the easiest steps when checking for the completeness of accounts payable. It is simply ensuring that all transactions are correctly recorded within the exact time frame when they occurred.

For example, if a transaction occurred in February, it is expected that such a transaction should be recorded in February and not earlier or later.

Analyze aging

An important step in testing for the completeness of the accounts payable is analyzing the aging of accounts payable. This enables the company to have a summarized outlook of how much it owes as well as the supposed time of payment.

Most aging reports categorize accounts payable in several 30-day blocks, with each block indicating how much the company needs to pay within the stipulated period.

For example, if a company owes $100,000 which is due to be paid in 6 months, analyzing the aging of the AP helps split up the payment into 30, 60, 90, 120, 150, and 180 days based on the different payment contracts.

Thus the company may pay $5,000 in the first 30 days, $20,000 by 60 days, and so forth. The splitting up of payments into defined 30-day blocks eases payments and also helps companies in keeping up with their obligations without defaulting.

Check duplicates

Check all AP transactions to ensure that no transaction was recorded twice. The elimination of duplicates ensures that the company does not lose money by overpaying its suppliers or service providers.

Vendor review and reconciliation

In order to mitigate fraud, wrong records, and completeness of the accounts payable, vendors are contacted randomly to ascertain whether the records in the accounts payable tallies with the records of vendors.

For example, if there is a record for a $10 purchase of office supplies, a vendor review would help confirm such a transaction as genuine. Thereby matching vendor statements with the AP balance.

Adjustment and documentation

If any errors have been noticed in the prior steps, adjusting journal entries are made to correct such errors. Once the record has been ascertained free of errors and complete, it is adequately documented and recorded in the company’s financial statements.

Read about: Is accounts payable a permanent account?

How do you test completeness of accounts payable?

You can test for the completeness of accounts payable by reviewing authorization, document verification, sample testing, and cut-off checks.

Additional steps in testing for completeness of AP are analyzing aging, duplicate checks, vendor review, reconciliation, adjustments, and documentation.

All these steps are necessary when testing for the completeness of accounts payable as they aid in ensuring that all transactions involving the AP account are rightly recorded.

Read about: How do you verify Payables?

Conclusion

Testing for the completeness of the accounts payable is a necessary step that auditors take when carrying out an audit of the accounts payable. This test ensures that all transactions are fully captured and reflected within the correct period.

It also ensures that there is traceable supporting evidence of all transactions, a correspondence between a company’s records and that of its vendors, as well as a match between the AP balance before and after checking for completeness.

When auditing the accounts payable, the completeness test is one of the key stages.

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.