Having a basic understanding of the taxes for stock options is essential whether you are an employee, employer, or investor. For employees, when the company you work in grants you employee stock options, they come with some tax implications.

The taxes for stock options is also important knowledge for companies and investors as it will go a long way in aiding companies and investors in understanding the tax implications of the stock options they issue or own respectively.

In reporting taxes for stock options, it is important to note form 8949, as that is the form used to report the profits or losses accrued from investing in stock options. When the stock options are held for less than a year, they are generally taxed as short-term gains, when held for over one year, they are taxed as long-term gains. We shall further discuss the various taxes for stock options hereafter but before we delve into that, let us take a look at what stock options are all about.

See also: Types of options

Understanding stock options

Stock options are derivatives whose value depends on the value of their underlying assets. They are contracts that confer on their holders the right to buy or sell the underlying assets of the option at a prefixed price on or before a specified date.

The underlying assets of stock options are the stocks for which the options were sold. The prefixed price of a stock option is its strike price, this is the price at which the stocks will be bought or sold when the option is exercised. It is also referred to as the grant price or exercise price. The specified date is the expiration date of the option; any option that is not exercised become invalid after its expiration date. Exercising a stock option is a process of buying or selling the associated stocks of the option.

When a stock option is sold and the companies that issue the stocks associated with the stock options undergo a merger, acquire a new company or carry out a stock split, adjustments are made to the stock options strike price and/or size to account for any of these events. The money which the option holder pays the option writer when purchasing the stock option is known as the option premium. Stock options are sometimes referred to as equity options.

There are different options styles such as American, Bermudan, European, Asian, Canary, etc. Each of these option styles determined when and how an option can be exercised. The most common option styles are American and European. An American-styled stock option can be exercised anytime within the period of its validity. The European-styled stock option can only be exercised on its expiration date.

Usually, a stock option contract comprises 100 stocks as its underlying asset, this means that for every stock option an investor purchases, they are entitled to either buy or sell 100 stocks when they exercise the option. Although the stock option holder has the right to either buy or sell the underlying stock, they are not obligated to exercise this right. The option seller on the other hand is obligated to either sell or buy the underlying stocks once the option holder exercises their stock option.

The prices of stock options that trade on exchanges such as NYSE Arca and NYSE American are usually determined by market forces of demand and supply and are also set by the option writers and buyers. These options are referred to as listed options and typically have four different expiration dates.

There are three main scenarios that may happen when an investor purchases listed options and want to exercise them. The listed option can be out-of-the-money, at-the-money, or in-the-money. When the listed option is out-of-the-money it means that the investor will lose, this is also referred to as an underwater option. When the listed option is at the money, the investor breaks even, neither making a profit nor losing. When the listed option is in the money, this is the best time for the investor to exercise their option as it directly translates to a profit on the option.

By investing in listed options, investors can still make a profit without having to exercise the stock option, instead, they can sell off the option once it is in the money and make an immediate profit. This is a common practice by investors who do not wish to exercise their option but rather purchased it as a means of earning an income in the interim. Additionally, the investors also save their time and mitigate transaction costs and other marginal requirements by selling off the listed option.

See also: Repricing stock options

Taxes for stock options

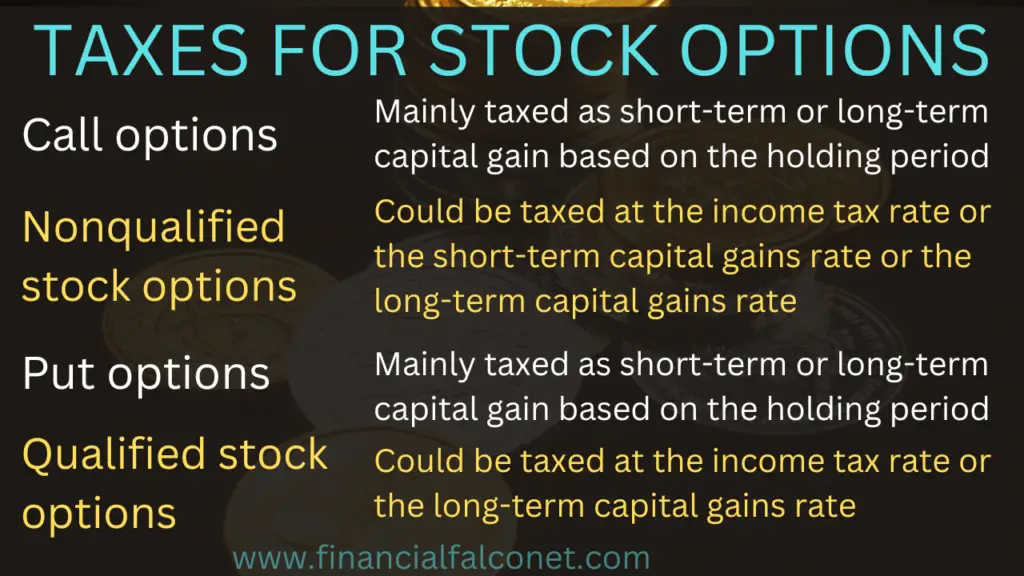

- Taxes for Call options

- Taxes for Put options

- Taxes for Qualified stock options

- Taxes for Nonqualified stock options

Listed above are the four stock options whose taxes we will discuss below. The call options and put options are broadly classified as listed options while qualified stock options and nonqualified stock options are broadly classified as employee stock options. As stated earlier, form 8949 is important when filing options losses or profits whether you are selling or buying stock options.

Taxes for call options

- Call option buyers

- Call option sellers

A call gives its holder the right to buy the underlying stocks at the predetermined strike price within the stipulated time frame. The expiration date of call options varies between three months to one year, some call options may however offer a longer expiration window.

We shall discuss the tax implications for investors (Call option buyers) and option sellers below.

Taxes for call option buyers

The profits or losses from call options for most individuals are taxed as capital gains while it is taxed as income for institutional investors. When you buy call options, they will either expire unexercised because they are out-of-the-money or at the money, be exercised because they are in the money, or be sold off before their expiration date. In either of the aforementioned, the gains or losses will be taxed as either short-term or long-term capital gains or losses.

Short-term capital gains or losses are reported for call options that were held for less than a year. Long-term capital gains or losses are reported for call options that were held for more than one year.

When the profits or losses accrued from buying call options are reported for call options that have been exercised, the option premium is added to the strike price at which the underlying stocks were bought before being taxed. For call options that expired unexercised, the option premium is deducted within the tax year. For options that were closed off by selling them, the gains are included in the investor’s income tax while the option premium that was paid is written off in the tax year that the option was sold.

Taxes for call option sellers

The profits or losses from call options, whether naked or covered are taxed as income for options brokers. However, in Canada, naked call options could be treated as capital gains based on IT-479R transactions in securities, paragraph 25 (c), provided that the option writer consistently reports the gains or losses from the naked options as capital gains every year.

Naked options are those options for which the option writer does not already own the underlying stocks. Covered options are those in which the option writer already owns the underlying stocks.

The profits or losses accrued from the sale of call options are taxed as income and must be reported in the same tax year that the options were exercised, expired, or were bought back.

For call options that are exercised, the sum of the option premium and the total amount received for the underlying stock purchase are taxed as either short-term or long-term gains. This is dependent on how long the option seller owned the stocks before selling. For call options that expire, the option premium is taxed as a short-term capital gain irrespective of whether the option’s validity period was less than a year or more than a year.

Put options taxes

- Put option buyers

- Put option sellers

A put option is a contract that enables its holders to sell the underlying stock at the strike price within the stipulated time frame of the contract. While the option holder has the right to sell, it is not compulsory that this right be exercised. Conversely, the option seller is obligated to purchase the underlying stocks once the option holder exercises their right to sell.

The taxes for put options differ for option buyers and option sellers. We shall discuss these taxes below

Put option buyers

The taxation of put options is similar to that of call options. For most individuals, the profits or losses from put options are taxed as capital gains whereas, for institutional investors, they are taxed as income.

When you exercise your put option by selling the underlying stocks to the option seller at the strike price, the difference between the sum of the option premium and other related fees and the total amount realized from the sale of the underlying stocks will be taxed as a capital gain. Your taxation being a long-term or short-term capital gain or loss is dependent on how long you had owned the underlying stock before you sold them to the option seller.

When an investor buys put options, the option’s premium is written off in the year in which the options expire, are exercised, or are closed out by selling them.

Put option sellers

The premium which option sellers receive upon the sale of call options is not liable to taxation until the stock option is exercised, expires unexercised, or gets offset in a closing transaction. For put options that are exercised, the difference between the amount spent on purchasing the underlying stocks and the premium received for selling the put option is taxed as income.

If an option seller sells a put option that expires unexercised by the option holder, the option premium is taxed as a short-term capital gain upon the expiration date irrespective of whether the option’s validity period was less than a year or more than a year. If the option expires in a different year from the one in which it was written, then, the option seller will be taxed only in the year in which the option expired. There will be no tax event in the previous year.

For put options that are offset by a closing transaction, the amount that is taxed is the option premium paid to the option seller when they sold the put option and the premium paid on the offsetting put option. Put option sellers offset their obligation to buy the underlying stocks by purchasing an equivalent option. This must be reported within the same year that the closing transaction was made.

When an option seller has an offsetting position, it is referred to as a straddle. For straddles, the taxation is dependent on the extent to which the offset gains affect the losses in the opposite position. If the loss on the expired option is greater than the unrealized gains from the offsetting position, the excess loss is deferred until when the offsetting position is sold. These are taxed at the income rate.

Taxes for qualified stock options

- Tax at Exercise

- Tax at sale

- Double taxation

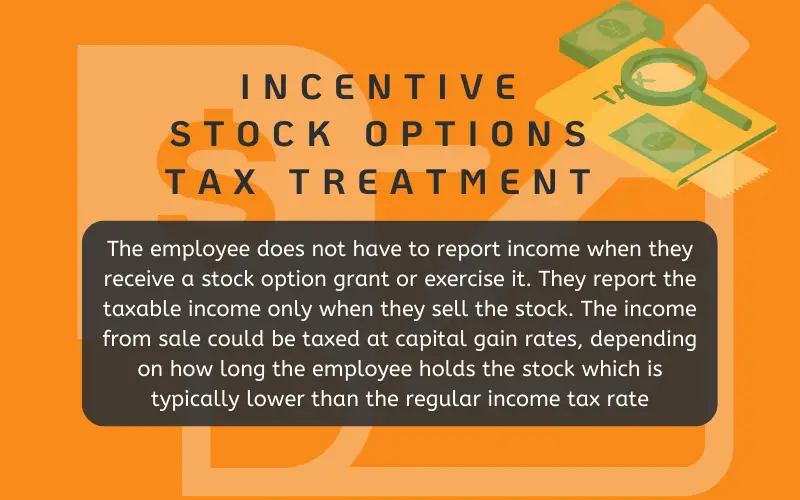

Qualified stock options are otherwise known as statutory stock options or incentive stock options (ISO). These stock options give the employees who own them the right to purchase a stipulated number of the granting entity’s common stocks at a predetermined price within a stated time frame. The predetermined price is generally a discounted price such that the employee can buy the stocks at a lower price than they are trading on the stock exchange. This predetermined price is also referred to as the grant price or exercise price. The stated time frame is the validity period of the stock option contract, otherwise known as its expiration date. The expiration date of qualified stock options is usually 10 years after they were granted.

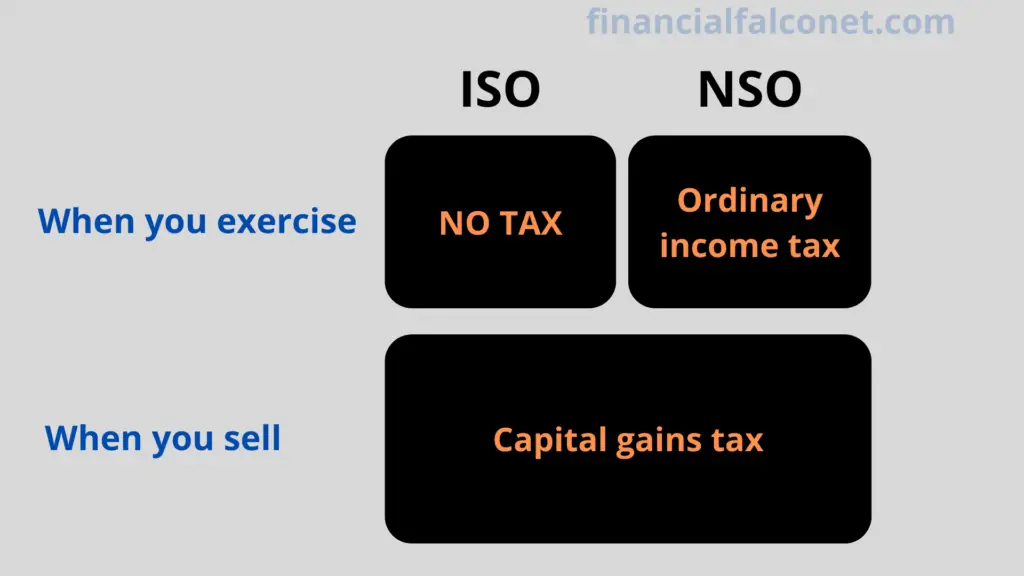

Qualified stock options generally have a more favorable tax treatment, hence they are referred to as qualified. The Revenue Act of 1950, Section 218 created some of these favorable tax treatments. These stock options are generally not liable to taxation when they are granted or when the employee exercises their right to buy the stocks. However, there might be taxation if the gain on the stock option is large and additionally, at the time of the stock’s sale.

Qualified stock options tax at exercise

Although there is generally no tax event at the time of exercising a qualified stock option, if the bargain element; the difference between the stock’s exercise price and its fair market value (FMV) at the time of exercise is greater than $73,600 or $114,600 for individuals or married persons filling their taxes jointly respectively, the bargain element might be taxed alternative minimum rate (AMT).

The alternative minimum tax rate for most US states is zero, hence the employee might end up paying no AMT even when the bargain element is above the stated range. If the employee resides in California, Colorado, Iowa, or Minnesota, they will have to pay the AMT as these state charge 7%, 3.47%, 7%, and 5% respectively as the AMT rate. Individuals and couples whose income is below the $73,600 and $114,600 range are not taxed AMT.

Qualified stock options are not liable to Payroll taxes such as Social Security taxes and Medicare taxes. These employee options are taxed when the employee sells them.

Taxes at the time of stock sale

Timing is very important when it comes to the taxation of qualified stock options. The time of stock option exercise and the time when the employee decides to sell off the stock options are two defining parameters in whether or not the employee will enjoy the favorable tax treatment that is associated with this employee stock options type.

At the sale of qualified stock options, the income realized which is the difference between the exercise price and the stock’s current market value at the time of sale is taxed at the capital gains rate which ranges between 0-23.8% depending on the employee’s income.

The capital gains rate is a considerably lower taxed rate compared to the income tax rate. In order to qualify for this lower capital gains rate tax, the employee must be held by the employee for at least one year after the options were exercised and must not be sold for at least 2 years after the stock option was granted. When these conditions are met, the gain is taxed at the long-term capital gains rate and the employee is said to have a qualifying disposition.

When an employee does not hold the stocks for at least 2 years after they were granted before selling and one year after exercising, the gains on the stock options get taxed at the higher ordinary income tax rate ranging between 10% to 37%. The rate is dependent on the income level of the employee. The employee is said to have a disqualifying disposition meaning they are no longer eligible for the favorable long-term capital gains rate tax when they do not meet the holding period requirements.

Double taxation of qualified stock options

When an employee whose income level is above the $73,600 range for individuals and the $114,600 range for couples filing jointly; if they hold their stocks for at least a year after exercise and at least two years after the grant date before selling the stocks, they will be subject to pay the AMT tax at the time of the option’s exercise and the long-term capital gains tax rate at the time of its sale.

These taxes are calculated based on the difference between the stock selling price and its grant price and the difference between the stock grant price and its fair market value at the time of exercise respectively. This means that individuals and couples who fall within the stipulated income bracket and live in any of the US states that charge AMT pay double taxes on their qualified stock options.

Criteria for qualified stock options tax advantages

In order for qualified stock options to enjoy the favorable tax treatments in Section 421(a) of the Internal Revenue Code (IRC), there are certain parameters set out by the IRC that must be met by the granting entity as well as the employee to whom the stock options were granted. When any of the under-listed conditions are not met, the stocks that are gotten from the exercise of the stock option get taxed at the ordinary income tax rate. These conditions include:

- The qualified stock option cannot be granted to stakeholders and nonemployees of the granting entity. They must only be granted to employees.

- The stock option must be granted under a written document plan that clearly outlines the total number of stocks that may be issued and the eligible employees for the stock option grant. This must be approved by the granting entity’s stockholders within one year before or after the adoption of the plan.

- The option must be exercisable only within 10 years of grant and must be granted to the employee within 10 years of the plan adoption and approval by stockholders.

- The employee to who qualified stock options was granted must exercise their option while still an employee of the granting entity or not more than 90 days after the termination of their employment. This is known as the post-termination exercise period (PTEP)

- In a situation whereby the employee dies, the option can be exercised by their legal heirs within its validity period. If the employee becomes disabled or lunatic, their PTEP is one year.

- Each option must be granted under a written qualified stock option agreement with the restrictions placed on exercising the stock option clearly listed.

- Each option must outline an offer to sell the underlying stock at the grant price and the validity period of the option contract.

- The grant price of the stock option must be equal to or greater that the fair market value (FMV) of the underlying stocks at the time of option grant.

- At the time of grant, the employee to whom the option is granted must not have more than a 10% ownership stake in the granting entity, unless the options ‘ grant price is at least 110% of its FMV and the expiration date of the option is 5 years.

- The qualified stock agreement must clearly state that the option cannot be transferred except by the laws of descent or will and that the option can only be exercised by the employee to whom it was granted.

- The total sum of the FMV of the underlying stocks that can be exercised by the employee during a calendar year cannot exceed $100,000. If the amount is above this value, Section 422(d) of the IRC stipulates that such an option be taxed as a nonqualified stock option.

Nonqualified stock options taxes

- Tax at Exercise

- Tax at sale

- Payroll taxes

- Withholding tax

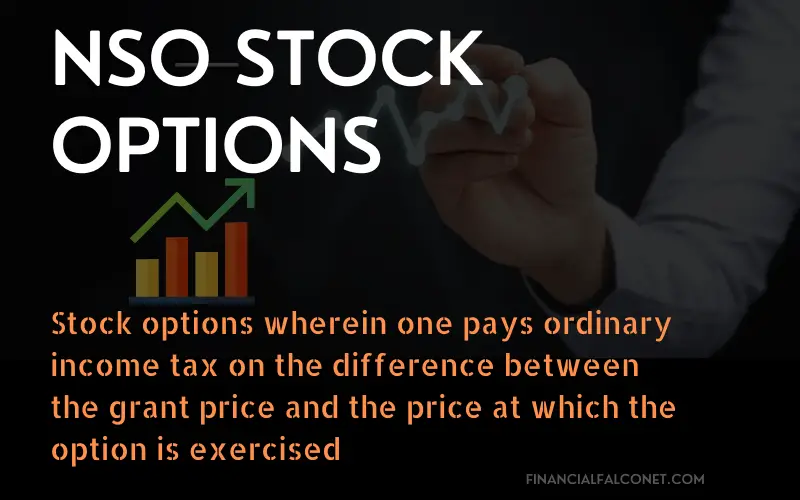

Nonqualified stock options (NSO) do not qualify for the favorable tax treatments which qualified stock options enjoy. They are also known as statutory stock options. These stock options give their holders the right to buy a specified number of the granting entity’s common stocks at the exercise price before or on the options expiration date. The expiration date of nonqualified stock options varies from one company to the next based on the option’s contract terms.

Nonqualified stock options are generally not taxed when they vest or when they are granted, they are also not subject to the stringent criteria to which qualified stock options must adhere. NSOs have several tax events which we shall discuss below.

Tax at the exercise of NSO

When nonqualified stock options have been granted to an employee, they generally have a vesting schedule that determines how many and when the underlying stocks of the options can be bought. When an employee exercises their NSO, the price break between the nonqualified stock options’ grant price and its fair market value (FMV) at the time of exercise is reported as taxable income and taxed at the regular income rate that ranges between 10-37%. This must also be reported in the same year that the NSO was exercised.

Although part of the taxes for NSOs are withheld by the granting entity at the time of exercise, the employee still needs to pay up any balance on their tax themselves when they file their income with the Internal Revenue Service (IRS). More shall be discussed on withholding taxes afterward.

Additionally, after the employee has paid the income tax on their NSO, they get a reduction on the alternative minimum tax they are liable to pay on any qualified stock options they own and exercise within the same year. As a result of this, individuals and couples who are liable to pay AMT taxes due to their income range generally exercise any nonqualified stock options they own first before exercising the qualified stock options they own in order to pay a reduced AMT at the exercise of their qualified stock option.

Furthermore, employees who opt for an early exercise of their stock options get a tax deduction because there will likely be no difference between the underlying stock’s fair market value and its exercise price. But in order for the employee to exercise their NSO early, the option has to be inherent in the stock option agreement or has been approved by the board of directors.

Tax at sale

After the employee exercises their nonqualified stock options, they now own the underlying stocks and can choose to either sell the stocks immediately or hold them for a while before selling. On selling the stocks, taxes have to be paid on the spread between the exercise price and its fair market value (FMV) at the time of sale. This spread which is the difference between the two prices is taxed at the personal income tax rate.

When selling NSOs, taxes have to be paid on the difference between the grant price and the market value of the shares at the selling time. The difference is the gain resulting from the sale is taxed as personal income or short-term capital gain or long-term capital gain depending on when the employee sells the stocks.

When the employee sells the stocks immediately, the spread is taxed at the personal income tax rate. If the employee holds the stocks for a while but sells them after one year from the time of exercise, the spread will be taxed at the short-term capital gain s rate. If the employee holds the stocks for over one year after they were exercised before selling them off, the spread will be taxed at the lower long-term capital gains rate.

Payroll taxes

In addition to the income tax that employee pay at the time they exercise their nonqualified stock options, they are also subject to payroll taxes. This payroll tax comprises Social Security tax and Medicare. The payroll taxes amounts to an addition of 1.45% to the income tax for employees whose income is greater than $137,700. The additional 1.45% is Medicare tax. Employees whose income is below $137,700, pay an additional 7.65% in payroll taxes asides from their income tax. This 7.65% accounts for 1.45% of Medicare tax and 6.2% of Social Security tax.

The granting entity for nonqualified stock options is also subject to payroll taxes which include Social Security taxes, Medicare, and Federal Unemployment Tax (FUTA). Furthermore, if the granting entity is undergoing a merger or acquisition, holders of nonqualified stock options are liable to pay payroll taxes.

Withholding taxes

When nonqualified stock options are exercised by the employee, the granting entity withholds part of their tax. The tax on the difference between the exercise price and its fair market value at the time of exercise is withheld if the difference is up to $1,000,000 and above. For spreads that are up to $1,000,000 the withheld amount will be 22% while the withheld amount for spreads greater than $1,000,000 is 37%.

See also: ISO vs NSO which is better

Taxes for stock options simplified

- Taxes for holders of call

- Taxes for sellers of call options

- Taxes for holders of put options

- Taxes for sellers of put options

- Taxes for qualified stock options

- Taxes for nonqualified stock options

So far, we have discussed the various taxes for stock options, here, we shall outline these various taxes within the tables that will follow

Taxes for holders of call options

| Event | Tax report |

|---|---|

| Exercised | The sum of the call option premium and the strike price of the underlying stocks are taxed at the short-term capital gains rate if held for less than a year and taxed at the long-term capital gains rate if held for over a year. |

| Expired | The option premium is deducted within the tax year |

| Sold to close | The option premium is written off while the gain is taxed at the personal income tax rate |

Taxes for sellers of call options

| Event | Tax report |

|---|---|

| Exercised | The sum of the option premium and the amount gotten from the underlying stock’s sale is taxed as short-term capital gains if the stocks were held by the seller for less than one year or long-term capital gains if they were held for more than one year before selling. |

| Expired | The option premium is taxed as a short-term capital gain irrespective of whether the option’s validity period was less than a year or more than a year. |

| Bought back to close | Gains or losses are taxed at the income rate |

Taxes for put option holders

| Event | Tax report |

|---|---|

| Exercised | The difference between the sum of the option premium and other related fees and the total amount realized from the sale of the underlying stocks will be taxed as either short-term or long-term capital gains depending on the stock’s holding period before the sale. |

| Expired | The option premium is written off |

| Sold to close | The option premium is written off while the gain is taxed as income |

Taxes for sellers of put options

| Event | Tax report |

|---|---|

| Exercised | The difference between the amount spent on purchasing the underlying stocks and the premium received for selling the put option is taxed as income. |

| Expired | The option premium is taxed as a short-term capital gain irrespective of whether the option’s validity period was less than a year or more than a year. |

| Bought back to close | Gains or losses are taxed at the income rate. |

Taxes for qualified stock options

| Event | Tax report |

|---|---|

| Granted | No tax event |

| Exercised | No tax event unless the employee’s income is within the range of $73,600 for individuals and the $114,600 range for couples filing jointly; in which case, they are subject to Alternative Minimum Tax (AMT) |

| Sold | Tax at the long-term capital gains rate if held for more than two years after grant and more than one year after exercise. Otherwise, it is taxed as ordinary income |

Taxes for nonqualified stock options

| Event | Tax report |

|---|---|

| Granted | No tax event |

| Exercised | The difference between the exercise price and the fair market value is taxed at the income rate. The issuing company withholds 22% tax if the difference between the exercise price and the fair market value is up to $1,000,000 and 37% tax if the spread is greater than $1,000,000 Payroll taxes are paid which amount to an additional 7.65% for employees making less than $137,700 and 1.45% for those making more the $137,700 |

| Sold | The spread between the exercise price and its fair market value at the time of sale is taxed at the personal income tax rate if sold immediately. If sold after one year from the time of exercise, the spread will be taxed at the short-term capital gains rate. If sold more than one year after they were exercised, the spread will be taxed at the long-term capital gains rate. |

See also: How do stock options work?

Examples of how taxes for stock options work

- Call options

- Put options

- Qualified stock options

- Nonqualified stock options

The examples of how taxes for stock options work will look at the hypothetical situations of the tax implications of investing in these stock options. The examples will only consider the option premium and the gains from the sales or purchase of the underlying stocks. Commissions and other related fees will not be considered in the examples.

Taxation of call options example

When a call option is exercised, the sum of the option premium and the cost of the shares are taxable. For instance, if Mary buys a call option for Alphabet stocks in January 2022 at $100, with a strike price of $30 and an expiration date of July 2023. The cost of the call option purchase is $3,100. Where the cost of the stocks is $30 x 100 and the option premium is $100.

If the stock trades at $35 per share in November 2022, and Mary decides to exercise her option, she would have made $400 which will be taxed at the short-term capital gains rate since the option was not held for up to one year before exercise. The gain is the difference between the proceeds of $3,500 minus the cost basis of $3,100

Now if Mary waits until May 2023 to exercise her options when the stocks are trading at $39 per share, then she would have made $800 which will be taxed at the long-term capital gains rate since she held the investment for more than a year.

If she however decides to sell the stock option instead of exercising it, and she sells the option for $120, the $20 gain will be taxed at the personal income rate.

If by July 2023 the underlying Alphabet stocks are trading at $30 or lesser, Mary will let them expire as there will be no gain in exercising the option. In this case, the premium will be deducted within the tax year 2023.

Put options taxes

Suppose Joseph bought a put option in February 2022 for Amazon stocks that cost $200. If the strike price is $18 and the expiration date is February 2023. Assuming the fair market value of the stocks drops to $10 by January 2023 and Joseph decides to exercise his option to sell the underlying stocks, he will make a gain of $600. The gain is the difference between the strike price of $1,800 for the stocks and the sum of the stock’s fair market value and options premium ($1,000 +$200). Since the put option was not held for up to one year, the gain will be taxed at the short-term capital gains rate.

If by the options expiration the fair market value of the stocks rises to $25 per share, Joseph will let the option expire thereby incurring a loss of $200 which was the premium paid on the option’s purchase. This premium will be written off.

If on the other hand the option is in the money and Joseph sells it off at $300 instead of exercising it, the $100 gain is taxed as income.

Qualified stock options taxation

Suppose Melvin works for a real estate development agency and he recently got promoted in August 2021. As part of his promotion package, he was granted 200 shares at a strike price of $10 which will expire in ten years. If the stocks have a performance-based vesting schedule whereby Melvin needs to sell a thousand properties before the option can be exercised.

Assuming he was able to meet this target in January 2026, he exercises the option when the stock’s fair market value is $40 per share. Suppose his income as an employee is less than $73,600 he will not be liable to pay tax. If however, his income is above $73,600 then he will be liable to pay Alternative Minimum Tax on the difference between the strike price of $10 and its current fair market value of $40. Thus the gain that will be taxed AMT will be $30 x 200. This will result in him having $6,000 which is subject to the alternative minimum tax rate.

Now, since the qualified stock options took over four years after the grant before they were exercised, Melvin has already met one out of the two holding requirements for the gains on the sale of the stocks to be charged at the long-term capital gains rate.

The other condition is for him to hold the shares for at least one year after exercising before he sells the stocks. If he does this, it means he has met the holding requirement for the gains on the sale of the stocks to be taxed at the long-term capital gains rate and thus has a qualifying disposition. Therefore assuming the gain on the sale is $10,000 this amount will be taxed at the lower long-term capital gains rate.

On the other hand, if Melvin does not hold the stocks for up to one year after exercise before selling, he has a disqualifying disposition and the $10,000 gain will be taxed at the income tax rate.

Taxes for nonqualified stock options

Assuming Samantha is a highly skilled Human resource personnel and got hired by a Tech company. In order to keep her in the company, she was granted nonqualified stock options with 100 underlying shares as part of her hiring package. The shares will have a 25% yearly vesting schedule and get fully vested in four years but the terms of the options agreement allow for early exercise.

If the strike price of underlying stocks is $10 and the expiration date is six years. Assuming Samantha opts for an early exercise, and she exercises the options when the stock’s fair market value is also $10 per share, there will be no tax event since the difference between the share strike price and its market value is zero.

If she waits to exercise later when the fair market value of the stocks raises to $20, the $1,000 spread will be taxed at the income tax rate and she will additionally be charged 7.65% as payroll taxes if her income is less than $137,700 whereas she will be charged an additional 1.45% in payroll taxes if he income is more than $137,700

If after exercising the options the fair market value of the stocks raises to $50 per share and she decides to sell off the stocks immediately so as to make a gain of $40,000. This gain will be taxed at the ordinary income rate.

If she decides to hold the shares for up to one year before she sells off the stocks and the gain she makes at that time is still $40,000 it will be taxed as a short-term capital gain.

If she holds the stocks for up to two years after exercising before selling them off, the $40,000 gain will be taxed as long-term capital gain which is a lesser tax rate.

See also: Stock options vesting

Conclusion

We have discussed the taxes for stock options, noting the various tax implications for exercised, expired, or sold stock options. As we have seen the taxes on stock options are varied and are affected by various factors such as whether filing individually or as a couple, the income range of the option holder as well as being an option holder or seller amongst other things.

Call and put options offer similar taxation for their holders and sellers, qualified stock options have stringent conditions attached that must be met before the stock options qualify for the tax advantages which the options are generally known for. Nonqualified stock options do not have stringent conditions attached to them but their tax rate is considerably higher than that of qualified stock options.

Although the basic taxes for stock options have been discussed here, it only serves as an introduction to finding out more information about taxes for stock options. In order to get the best advice that is curated to your unique position as an option seller or buyer, it is best to seek the counsel of a tax professional to further guide you on the taxes for the stock options you hold or have sold.

Last Updated on November 8, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.