There are different types of options with various criteria for classification. An option is a financial derivative that confers on its recipient the right to buy the underlying at a specified price, in a particular quantity, within a stipulated time frame. Here, the various types of options will be discussed; but before we do that, let us understand what options are.

What are options?

Options are a part of a large class of financial instruments called derivatives. They are contracts that give their owners the right to buy or sell a predetermined number of the underlying asset at a particular price known as the exercise price on or before a specified date known as the expiration date. These are usually as stated in the options contract.

While options give their owners the right to either buy or sell the underlying, the option seller is obligated to either sell or buy the underlying once the option owner exercises their option. Options that give their owners the right to purchase the underlying at a particular price are known as call options while those that give their owners the right to sell the underlying at a particular price are known as put options.

Call options are mainly exercised when the option’s exercise price is below the underlying’s current market value while put options are mainly exercised when the option’s exercise price is above the underlying’s current market value.

Options can be a form of compensation, part of complex transactions, or acquired by buying. As part of compensation packages, options are granted to employees or service providers by the companies where they work or provide services. The options granted to employees are mostly employee stock options, restricted shares, and statutory or nonstatutory stock options.

The options granted to service providers are usually nonqualified stock options (NSO). The NSOs are so-called because they do not qualify for the tax benefits enjoyed by qualified stock options. Generally, all the aforementioned options are granted directly by the companies to the employees or service providers.

Options that are acquired by buying are mostly call and put options. These options are traded in public markets such as New York Stock Exchange Arca (NYSE Arca), the Chicago Board Options Exchange (CBOE), New York Stock Exchange American (NYSE American), etc. and are therefore known as exchange-traded options or listed options.

For these exchange-traded options, data from CBOE suggests that 60% of the options are closed out, 30% are not exercised thereby expiring with no benefit to the buyer and the remaining 10% are the options that get exercised. When an option is closed out, it means the option holder sells back the option to the person they bought it from. For options that are exercised, the owner buys or sells the underlying as specified in the options agreement.

Related: Repricing Stock Options

Options that are exchange-traded are usually standardized, settled through a clearing house, and guaranteed by the Options Clearing Corporation (OCC). The OCC guarantees these options in order to curtail sellers of these options refusing to meet their obligations of buying or selling the underlying from or to the option holder when they exercise their option.

Exchange-traded options are further regulated by the Securities and Exchange Commission (SEC). These options also have a Key Investor Document (KID) that contains the contract terms, the underlying asset, and the associated risk of owning the option; all this information can also be accessed on the exchange website where the option is sold. Some of the common exchange-traded options include bonds, callable bear/bull contracts, equity, futures contract, indexes, and stocks.

Options that are traded directly between the buyer and the seller are known as over-the-counter (OTC) options because they are not listed on any options exchange. The terms of these options are often tailored to meet the particular need of the option writer which is usually a well-capitalized corporation. It is necessary that the option writer for an OTC is a well-capitalized corporation in order to prevent the risk of not fulfilling the option.

OTC options do not have standardized terms and have minimal regulation as such, the option holder and the option writer must establish credit lines as well as agree with each other’s clearing and settlement processes. Some of the common OTC options include currency cross rate, interest rate, and swaps. Stocks such as penny stocks and fractional stocks are considered OTC stocks because they are also generally not traded on major exchanges.

The valuation of options is generally based on the price of the underlying asset, the option’s exercise price, its expiration period (time value), risk-free interest rate, and market volatility. When the price of the underlying is likely to rise, a call option for the underlying would be more expensive while its put option would be cheaper. As the expiration date of an option nears, its value decreases; this is because the chances of the market value of the underlying asset changing as predicted by the particular option become more limited due to time.

Therefore, a one-year option will be more valuable than a one-month option. Additionally, the more volatile the market for the options underlying, the more valuable the option. This is because high volatility means the market price of the underlying is more prone to fluctuations.

Although options are tangible assets, owning them does not mean the holder actually owns the underlying. The holder only gets ownership of the underlying when they exercise their option.

Options in simple terms

Options are contracts between two parties that confer on the person who purchases them (the holder), the right to buy or sell the specified underlying to or from the person that sold the contract (the writer) at a predetermined price (exercise price) on or before a particular date (expiration date).

Although the option holder has the right to either buy or sell the underlying, there is no direct penalty to them if they chose not to exercise this right. They will only lose the money they paid to purchase the option because once the expiration date has passed and the option has not been exercised, it becomes worthless and invalid.

The option writer on the other hand is obligated to either sell or buy the underlying once the holder exercises their right to either buy or sell the underlying. While the option holder loses the money paid to purchase the option if unexercised, this same amount becomes a gain to the option writer.

Options mainly function as some form of insurance for their holders and are mainly used to speculate on the movements and changes in the price of real estate, cars, currency, stocks, and any other commodity for which the option was issued. Since markets are often unpredictable with the prices of these securities constantly changing, the options protect their holders from potential losses or enable them to benefit from a potential rise in prices.

If for instance, you own a large-cap stock that you feel might experience a decline in price, you can choose to buy a put option which gives you the right to sell the stock at the strike price even if the stock’s current market price decreases below it.

Conversely, if you want to buy property in a location where you feel the prices of property might soon increase but you do not have the money to make the purchase right away, you can buy a call option which gives you the right to buy the property at the strike price in the future. This way, you get to purchase the property at the lower strike price even though the current market price is higher.

Related: Stocks vs real estate

Terms related to options

- At the money (ATM)

- Exercise

- Exercise price

- Expiration date

- In the money (ITM)

- Option buyer

- Option writer

- Premium

- Underlying asset

- Underwater

- Vesting and vesting schedule

At the money (ATM)

An option is said to be an at-the-money option when the current market price of the underlying asset is the same as its strike price. When this happens, the option buyer does not make a profit, instead, the option premium paid and any other related fees become a loss whereas the option writer profits from the premium.

Exercise

Before an option holder can enjoy the potential benefits arising from the options they own, they will have to exercise their option. Exercise or exercising an option is the process in which the option buyer decides to utilize their right of either buying or selling the underlying asset. Once an option is exercised, the option writer must fulfill their obligation to sell or buy the underlying asset.

Related: Exercising stock options

Exercise price

The exercise price is the predetermined price as set in the option’s contract, at which the underlying assets will be bought or sold when the option buyer exercises their right. It is usually listed in increments that vary based on the options’ price level. The increments range from 0.5, 2, 2.5, 5, or 10 points. The exercise price is also known as the option’s grant price or strike price.

Expiration date

The expiration date is the stipulated date after which the option contract is no longer valid. Option holders who wish to exercise their options must do so on or before the expiration date because once the options expire, their right to either buy or sell the underlying asset becomes automatically forfeited. The option holder is also no longer obligated to sell or buy the underlying asset.

For exchange-traded options, the last trading day for the options that are expiring within a given month is the third Friday of that given month. This Friday is commonly called the expiration Friday. Options expiration dates vary from as short as a week to as long as ten years; depending on the options agreement terms.

In the money (ITM)

In the money options are options whose current market value is above the strike price – for options that give a right to buy- and below the exercise price -for options that give the right to sell the underlying asset. When an option is in the money, the option holder’s profit is the difference between the current market value of the underlying asset and its exercise price. This same profit becomes the option writer’s loss.

Option buyer

The option buyer is the person who purchases the option contract from the option writer. As a result of the option purchase, the buyer has the right to either sell or buy the underlying asset to or from the option writer at the contract’s specified exercise price. The option buyer is also referred to as the option holder.

Option premium

The option premium is the amount that the option buyer pays to the option writer when purchasing the option contract. For exchange-traded options, it is also the price at which the option trades daily on the exchange market; because of this, the premium on exchange-traded options fluctuates daily based on market forces. The premium also serves as a way of reducing the unlimited loss that the option writer is liable for.

Option writer

The option writer is the person who sells the option contract and is also referred to as the options seller. The writer is obligated to either sell or buy the underlying shares once the option buyer exercises their options.

Underlying asset

The underlying asset of options is what the option holder buys or sells to the option writer when they exercise their option. What the underlying asset of an option is, depends on the particular type of option; it could be stocks, bonds, commodities, currency, etc.

Underwater

Options that are underwater are those whose underlying asset market value is above the exercise price for a put option or below the exercise price for a call option. When this happens, the option holder will be at a loss if they choose to exercise the option. Therefore, options that are underwater are generally not exercised and are left to expire. Underwater options are also referred to as out-of-the-money options.

Vesting and vesting schedule

Vesting and vesting schedules are terms that are common with options that are issued by companies to employees, service providers, and other stakeholders of the company. Vesting is a legal term that relates to earning the right to purchase the underlying assets of a particular option after the option holders have met the restrictions on the option.

The vesting schedule is part of the option contract that specifies the particular performance-based event or time frame that must elapse before the option holder can exercise their option. Time-based options generally have a vesting schedule varying between 4 to 10 years.

Related: RSU Stock Vesting, Taxes, and Meaning

Option contract features

- Contract size

- Down payment

- Expiration date

- Intrinsic and extrinsic value

- An option holder’s right

- Settlement terms

- Strike price

The above are features of options. Most options possess these features, there might however be some options that have other additional features. This might occur especially with over-the-counter options whose terms are not standardized and could be adjusted to meet certain preferences of the option seller or buyer. We shall briefly discuss each of these features below

Contract size

The contract size of an option specifies the number of underlying assets to which the option holder is entitled when they exercise their option. The option contract size is normally fixed. For example, a stock option normally contains 100 shares per option contract. This means that the option writer is obligated to either sell or buy 100 shares to or from the option buyer when they exercise their option.

Down payment

The down payment on an option is also known as its premium. This is the money that the option holder pays the option writer when purchasing an option. In a case where the option holder does not exercise their option, they lose this down payment and it becomes a profit to the option writer.

Options that are issued to employees, service providers, and other stakeholders by a granting entity generally do not require the holder to make a down payment. in which case the option holder does not pay a premium for the option, instead, the option is often granted free and it is only when exercised that the option holder pays for the underlying assets and even then, it is usually a discounted price.

Expiration date

Every option has a defined period within which the options may be exercised. The expiration date for an option is often fixed and unchanged throughout the option’s validity. Options that do not get exercised become worthless after their expiration date and can no longer be exercised.

Intrinsic and extrinsic value

The intrinsic value of an option is the difference between its exercise price and the current market value of its underlying asset. The intrinsic value basically tells the option holder what they stand to gain or lose if they were to exercise their option today.

The extrinsic value of an option is its time value and is based on the predicted volatility of the market price of the option’s underlying asset and the time frame before its expiration.

Time value is the option contract’s extrinsic value. It’s based on the expected volatility of the underlying asset’s price and the time until the option’s expiration date. Options that have a long expiration period such as up to 10 years have a higher extrinsic value, this is because it has more probability of becoming an in-the-money option before their expiration date. Options with a shorter expiration time frame are considered to have lesser extrinsic value.

Related: What are Restricted Shares: RSA vs RSU

The reduction in the value of an option as it nears the expiration date is known as time decay. Options lose one-third of their extrinsic value within the first half of their expiration period and lose two-thirds in the second half. Thus, the time decay of an option does not happen in a linear fashion.

An option holder’s right

The option contract also specifies the right that the option holder gets upon purchase of the option. If the option holder’s right is to buy the underlying asset, it is called a call option while a right to sell the underlying asset is called a put option.

Settlement terms

The settlement terms of the option are another feature of the options contract. When an options contract is first written or first bought by the option holder, there is no exchange of the underlying asset. It is only when the option is exercised that the underlying asset gets exchanged. The settlement terms indicate if the option holder gets the actual underlying asset or its cash equivalent upon exercising their option. The settlement terms may also indicate when the option holder can exercise their option. Unexercised options have no settlement.

Strike price

The strike price refers to the price at which the underlying asset will be bought or sold by the option holder upon exercising their right to either buy or sell the underlying asset. The strike price is usually fixed and does not change all through the options validity period.

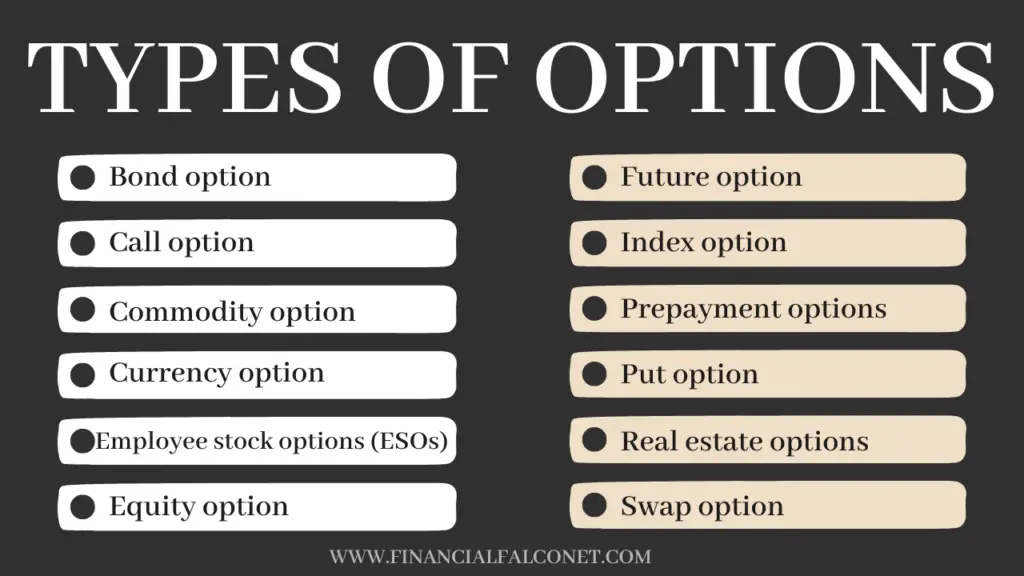

Common Types of Options

- Bond option

- Call option

- Commodity option

- Currency option

- Employee stock options (ESOs)

- Equity option

- Future option

- Index option

- Prepayment options

- Put option

- Real estate options

- Swap option

Listed above are the various types of options. Although they vary based on their underlying asset, the risk management principles and valuation criteria for options apply across all the different types of options since they are all financial derivatives. We shall discuss each of these option types below.

Bond option

A bond option is a derivative contract that gives the holder the right to buy or sell a bond at a predetermined price in the future within a stipulated time frame. These options are typically traded over the counter and useful in locking in the price of the underlying bond as long as the contract has not expired or been exercised. Thus, bond options reduce the credit risk due to the fluctuations in the price of bonds.

Additionally, bond options can be used to protect an existing bond portfolio, enhance the portfolio’s performance over time or make short-term income. The bond option holder has no obligation to either buy or sell the underlying bond if they do not wish to do so. Bond options are mostly settled in cash but when held until the maturity date, the underlying bond gets delivered to the holder.

Types of underlying bonds in bond options

- Callable bond

- Convertible bond

- Exchangeable bond

- Extendible bond

- Putable bond

Callable bond

A callable bond enables the bond issuer to repurchase from the bondholder at a prefixed price at a specified time in the future. However, for the first few years, these bonds cannot be repurchased (called); this period is referred to as the lock-out period.

Convertible bond

A convertible bond lets its holder convert the bond into the stock of the bond issuer at a preset price within a stipulated time in the future.

Exchangeable bond

These bonds allow their holder to demand the bond’s conversion into the stock of a different company which is usually the issuing company’s subsidiary. This conversion is usually at a preset price and within a stipulated time frame.

Extendible bond

When bonds are issued, they generally have a stated maturity date, but for extendible bonds, this maturity date can be extended by a certain number of years.

Putable bond

When an investor purchases a putable bond, they have the right to demand early redemption of the bond with a stipulated time in the future at a preset price. This means that the bond issuer buys back the bond from the bondholder.

Related: Stock Options vs RSA differences

Call option

Call options are contracts that give their holders the right, but not the obligation, to buy the underlying option asset at a predetermined exercise price anytime before or on its expiration date. The party that issued the call option, otherwise known as the option writer is obligated to sell the underlying asset to the option holder once they decide to buy it.

Any option type that grants its holder the right to purchase the underlying asset is a call option. The pricing of call options is based on the probability of the option holder making a profit from exercising the option before or on its expiration. Generally, the expiration date of a call option depends on its underlying assets, but broadly speaking, the expiration date is within 3 months or 10 years.

Corporate and institutional investors generally use call options to hedge their investments, increase marginal revenue, and hedge against positional risks. Broadly speaking, call options are a potential source of generating capital gains from a relatively small initial investment amount. Thus, they are considered an investment with a high return.

Types of call options

- Long call option

- Short call option

Long call option

This particular call option is a contract that allows the holder to buy the underlying asset at the exercise price before or on its expiration date. Investors commonly buy the long call option to either speculate on the price of the underlying asset in order to realize a profit or plan ahead to purchase the underlying asset in the future at the cheaper exercise price.

Short call option

The short call option is an obligation to sell the underlying asset of the option to the option holder whenever they exercise their option provided the expiration date has not passed. With the short call, investors can boost their income through the premium paid on the option contract.

Commodity option

A commodity option is a contract that gives its holder the right to either buy or sell the underlying commodity. These underlying commodities may be in the metals sector such as gold, silver, copper, platinum, etc., or in the energy sector such as crude oil, natural gas, petroleum, gasoline, etc., or in the agricultural sector such as wheat, soybeans, maize, rice, sugar, cotton, cocoa, etc.

For ages, commodity options were only available in these three sectors but recently, options for more commodities might be available. Investors use commodity options to hedge against currency depreciation, high inflation in prices of commodities, or benefit from an increase in prices of commodities, especially in the agricultural sector.

These options function just like equity options in the fact that the option holder’s risk is limited to the option premium whereas the option seller’s risk is unlimited based on the underlying commodity’s price.

Currency option

A currency option is a financial instrument that confers on its holder, the right to buy or sell currencies at a notional (speculation). This exchange of one currency into a different currency is done at the preset ratio of notionals on the delivery date. Simply, currency options enable their holders to engage in foreign exchange transactions. The notional is the amount of each currency that the option allows the option holder to buy or sell.

The ratio of notional is the price at which the currency will be bought or sold, it is also known as the option’s strike price. The delivery date is the date on which the currencies will be exchanged if the holder exercises their option.

Currency options generally trade over the counter with few regulations but some trade on exchanges such as the Nasdaq International Securities Exchange (ISE). The holder of this option pays the seller a premium when purchasing the option. The amount paid as a premium depends on whether the option is a call or put option, its ratio of notional, the option style and its expiration date. Most currency options are American-styled options while some are European-styled. A currency option is also referred to as the foreign exchange option or FX option.

The value of an FX option depends on:

- The prevailing spot rate is the price at which the currencies are trading at the time of the option purchase.

- The volatility level of the currencies as determined by the extrinsic value of the option.

- The interbank deposit rate of the currencies.

Investors generally use these factors to estimate the best time to purchase currency options, ensuring they buy at times of low volatility and sell at times of high volatility in order to make a profit. Thus making them an effective hedge against FX risk.

Related: ISO vs NSO Differences and Similarities

Employee stock options (ESOs)

Employee stock options are often used as a form of incentive for employees which gives the employee to whom they are granted the right to buy the company’s common stock at a discounted price in the future. It is only after the employee exercises their ESO that they get to own the shares associated with the option that they were earlier granted. They are granted either as part of a promotion package, hiring contract, or work bonus. It is often used by companies as a means of retaining top talents and encouraging high performance.

Employee stock options that are granted to employees usually have a vesting schedule that determined the number of shares the employee can exercise per time. This vesting schedule could be based on achieving certain milestones as a company such as expanding to new regions, or employee performance based such as meeting specified sales for the company or time based or in some cases, a combination of all the earlier mentioned three ways.

Time-based vesting could be graded whereby a certain percentage of the stocks can be exercised yearly or it can be cliff where all the stocks vest at a stated date.

Generally, employees that have been granted a stock option do not pay a premium on it, instead, they only pay for the stocks when they exercise their right to purchase them. The price at which they purchase the shares is known as the grant price and is usually cheaper than the current market price of the shares. Thus, they can make a profit on it when they sell.

Types of employee stock options

- Incentive stock option (ISO)

- Nonqualified stock option (NSO)

Incentive stock option (ISO)

Incentive stock options (ISO) are also referred to as qualified stock options or nonstatutory stock options. They are a corporate benefit to employees and the difference between their exercise price and their current market value at the time of exercise is a gain to the employees to whom they are granted. This gain is generally eligible for certain tax exemptions such as not being taxed at the time of exercise. These options are mostly issued to exceptional employees who have contributed greatly to the issuing company’s growth and successes.

Nonqualified stock option (NSO)

Nonqualified stock options (NSO) can also be referred to as nonstatutory stock options. As implied by their name, they do not qualify for certain tax advantages such as not being taxed at the time of their exercise. NSOs are also a form of employee compensation to encourage dedication to duty and loyalty to the company.

These options reduce the cash compensation given to employees by rewarding them with a possible stake in the company if they exercise their option to purchase the shares at the exercise price within the stipulated period of the contract.

Related: Incentive stock option vs nonqualified stock option – which is better?

Equity option

Equity options otherwise known as stock options are one of the most popular types of options. These options are contracts that offer the investors who own them, the right to buy or sell the underlying shares at the strike price on or before the option’s expiry date. The option that confers on the holder the right to buy is known as call equity options while those that confer on the holder the right to sell are known as put equity options.

Equity options contracts usually contain 100 stocks per option; this means that for each equity option an investor owns, they are entitled to get 100 stocks when they exercise their option. The holder usually pays the seller a premium when purchasing this option, this amount is non-refundable and if the holder does not exercise their option, it becomes a gain to the option seller.

When equity options are exercised, the option holder buys the shares or sells them at the strike price irrespective of the market price being higher or lower than the strike price at the time of exercise. If the exercised option is a call option, it becomes an in-the-money option when the strike price is below the market price at the time of exercise. If it is a put option, it is in the money if the strike price is higher than its current market value.

These types of options are used by investors either to protect their existing shares against share price volatility, plan ahead or speculate on market changes in order to make a profit. Employee stock options and exchange-traded options are the two types of equity options.

Future option

This is a financial security that gives traders the right to buy or sell a futures contract at the strike price by a stipulated date. These options are traded on various exchanges in the US such as the Chicago Mercantile Exchange (CME) and in other exchange markets around the globe. Future options are traded with a future broker in a separate futures account. Before trading futures options, the trader must have a specified deposit called the margin in their futures trading account. The margin varies based on the underlying futures.

These types of options (future options) grant the trader the right to buy are call future options and those that grant the right to sell are put future options. Traders purchase the call futures options when they predict that the price of the underlying futures will rise and purchase put futures options when they predict a fall in price.

The contract terms of these options are tailored based on the particular one purchased. This variation makes trading them more complex than equity options. One of such variations is that the time of expiration of the futures contract is usually a month before their delivery month; for instance, if the underlying futures were to be delivered in December, the future option will expire in November.

Future options premium is determined by the contract strike price, volatility of the underlying futures, expiration date, and underlying futures price. Generally, the quoted premium is the price for one future in the contract meaning that the trader will have to multiply the stated amount by the total number of underlying futures to arrive at the price of the whole future contract. For instance, if the price of a future option is quoted as $1 and the underlying futures are 10,000; it means the option’s premium is $1 x 10,000 ($10,000).

Related: Stock Options Vesting Schedule

Index option

Index options are derivative contracts that have an index as their underlying asset. They give their holders the right to either buy (call) or sell (put) the underlying index at a prefixed strike price. Thereby allowing traders to speculate on the volatility or direction of a particular market segment or the whole stock market as represented by the underlying index of the particular option. An index is a collection of the stocks of different companies which comprise the particular index.

Common indexes include the S&P 500, Wilshire Mid-Cap Index, Rusell 2000, etc., or sector-based such as Vanguard Real Estate Index Fund ETF Shares, Technology Select Sector SPDR Fund, Energy Select Sector SPDR Fund, etc.

These types of options are low-risk investments that investors use to benefit from the directional swings of certain indexes. The loss potential for both call or put options is the premium paid to purchase the options. The potential profit for call index options is unlimited while that of a put index option is the difference between the index price and the premium paid. Thus, investors limit their losses on one hand and gain exposure to a basket of stocks at a fraction of the cost.

Like stock options, an index option normally contains 100 stocks of the particular index as the contract size. The purchase of index options does not give the option holder the right to own the stocks in the index and even when exercised, settlement is usually done by cash since delivering the underlying index stocks is mostly impossible. Most index options are European-styled meaning that they cannot be exercised and settled except on the expiration date.

Furthermore, investors use index options to protect their portfolio from a decline in price below the preset strike price by locking in any accumulated gains. This can be achieved by purchasing a put index option that can lock in a particular position on the underlying stocks. For hedging large diversified portfolios, the investor determines the particular index that covers the particular index they own and purchases the number that tally with their index holding in order to protect their diversified portfolio.

Prepayment options

The prepayment option gives mortgagee’s the right to prepay a mortgage and is sometimes subject to a fee or penalty if the mortgagee fails to meet up with the terms. This option may be exercised if the building for which the prepayment option was purchased gets sold or if the interest rate on the building declines and the mortgage can be refinanced at a lower rate.

Put option

While call options confer the right to buy the underlying asset, put options confer on their holders the right to sell the underlying asset at a predetermined strike price on or before the expiration date. The holder pays a premium to the seller who is obligated to buy the underlying shares from the put option holder. In order for the put option to be in the money, the underlying asset’s strike price must be higher than its current market price at the time of exercise.

The option seller experiences the highest loss when the price of the underlying asset declines to zero while the option buyer gets the most profit in such an event. In an event when the option buyer does not exercise their option, the premium paid becomes a loss to them and a gain to the option seller. These options are frequently used by investors to speculate about a decline in the price of the underlying shares especially expecting their prediction to turn out right so as to benefit from it.

Purchasing a put option is a wager that the price of the underlying asset will decline in the future. Investors use these options to hedge against a future decline in the market price of the underlying asset. It becomes beneficial if the asset’s price does fall especially when it is far below the strike price, in that instance, the investor can now sell the asset at the higher strike price thereby reducing the loss they would have otherwise had.

The value of put options decreases when the market price of the underlying asset increase and increases when the market price decrease. Therefore the relationship between these two prices is opposite.

Related: Early Exercise of Stock Options

Types of put options

- Covered put options

- Uncovered put options

Covered put options

When investors purchase put options, they mostly buy covered put options. These options are said to be covered because the investors already have the underlying asset for which they bought the option. The covered put option enables investors to effectively hedge against a reduction in the market value of the underlying asset such that they limit the loss that they would be liable to if such a reduction occurs.

Uncovered put options

When investors purchase put options for which they do not own the underlying asset, such an option is known as an uncovered put option. Investors use these options mainly to speculate and gain from them if their prediction turns out right. They do this by either selling off the option or purchasing the underlying asset at the lower market price to sell it at the higher strike price.

Real estate options

Real estate options are also known as option-to-buy contracts or real estate purchase agreements or purchase and sale agreements. They are uniquely designed contracts that grant the optionee the right to purchase real estate from the optioner at a prefixed price within a limited time frame. The prefixed price remains unchanged irrespective of market conditions and the optionee buys the real estate at that price. The optionee is the real estate option buyer while the optioner is the seller.

Even though the optionee is not obligated to buy the property, the optioner cannot offer the real estate whose option has already been bought to another buyer unless the time frame as stipulated in the contract has elapsed. Thus the contract ensures that the option buyer has exclusive access to purchase the real estate which means it is off the market.

Simply put, the option seller cannot sell the real estate to another party as long as the option is in effect unless the optionee outrightly informs them that they are no longer interested to make the purchase, in which case the option becomes invalid.

If the optionee changes their mind about purchasing the real estate for which they bought the option, they have to inform the optioner within the first seven to ten days after the option purchase. This period is known as the option period. If they do so, they get refunded the money paid to purchase the option which is referred to as the earnest money or option consideration.

Real estate professionals use this type of option to provide stipulations in land or property contracts, mortgage notes, and deed of trust, reduce the initial investment or the down payment on the real estate, attract investors and provide flexibility on purchase transactions. Investors use this option to plan ahead for the future in order to own properties in high-brow areas or as a source of future income if they decide to sell off the option to another investor.

The real estate types of options are usually sold over the counter with the terms agreed upon by both the optionee and the optioner. Although they are not regulated, the options contract makes them valid and enforceable. Therefore investors are assured of getting the underlying asset for which the option was bought.

Swap option

These types of options are also referred to as swaptions. It is a contract that confers on the payer the right to enter into an underlying swap within the preset time frame. Although the underlying swap for these options is typically interest rate swaps, they might also be used for other kinds of swaps.

Swap options are traded over the counter and as such, have a great deal of flexibility. The various contract features such as the premium, notional amount, strike price, length of the option, the fixed and float legs, the benchmark for the floating leg, adjustment frequency for the variable leg, etc are decided and agreed upon by both parties involved in the swaption.

The fixed leg and floating leg have some standardized determining factors. The fixed leg rate is generally determined by a benchmark such as a treasury. The floating leg rate is determined by LIBOR (London Interbank Offered Rate). The length of a swap option generally ends 2 business days before the date of the swap.

Swap options can be settled either in cash or physically. If settled as cash, the cash value of the swap is paid to the option buyer. If settled physically, the buyer and seller carry out the swap. They are mostly used by financial institutions and large corporations to hedge a variety of macroeconomic risks, especially interest rate risk, or change their payoff profile.

Types of swaps

- Payer swap

- Receiver swap

Although these are the two major types of swaps, there is another kind of swap which is the combination of both the payer and receiver swap as the underlying sway. This swap is referred to as a straddle.

Payer swap

A payer swap works like a call option by granting the owner the right to enter into a swap where they receive the floating leg when they pay the fixed leg.

Receiver swap

The receiver option works like a put option by granting the owner the right to enter into a swap where they pay the floating leg and receive the fixed leg.

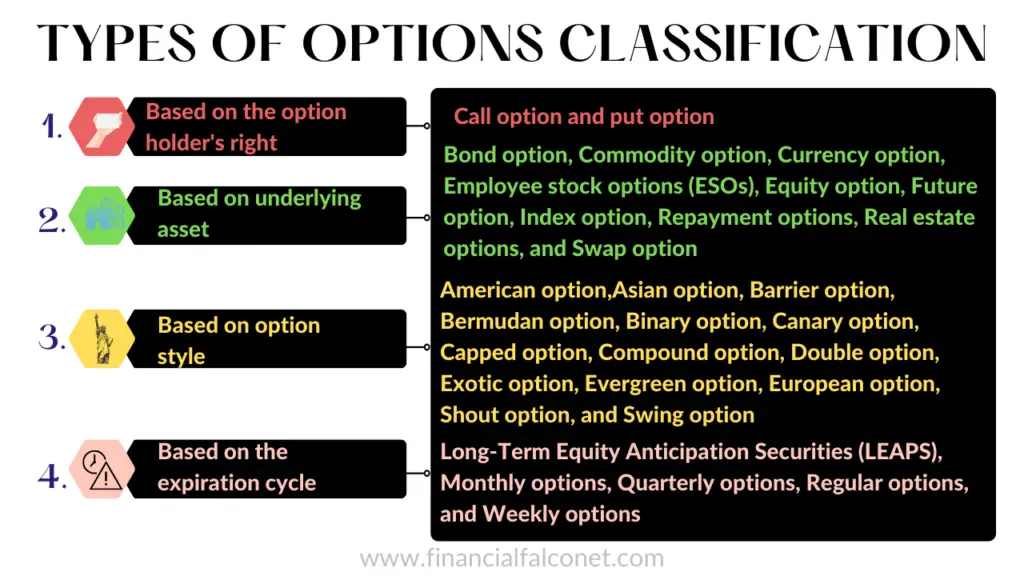

Types of Options (Criteria for Classification of Options)

The common way of classifying options is based on the underlying asset, but there are other criteria as well. Below we will classify the types of options using the common criteria.

Criteria for classification of the different types of options

- Based on the option holder’s right

- Based on underlying asset

- Based on option style

- Based on the expiration cycle

Each type of option would be discussed after the listing.

Types of options based on the option holder’s right

- Call option

- Put option

Types of options based on underlying asset

- Bond option

- Commodity option

- Currency option

- Employee stock options (ESOs)

- Equity option

- Future option

- Index option

- Prepayment options

- Real estate options

- Swap option

Types of options based on option style

- American option

- Asian option

- Barrier option

- Bermudan option

- Binary option

- Canary option

- Capped option

- Compound option

- Double option

- European option

- Evergreen option

- Exotic option

- Shout option

- Swing option

The option style of an option determines how or when the option holder can exercise their option. We shall have a brief look at what these different option styles mean below

American option

An American-styled option is one that allows its holder to exercise their option at any time within the stipulated time frame of the option contract. Most stock and futures options are American-styled.

Asian option

An Asian-styled option is one whose settlement is influenced by the average price of the underlying asset over a predetermined time frame.

Barrier option

When an option is a barrier option, the price of its underlying asset must be above a particular level before it can be exercised.

Bermudan option

A Bermudan-styled option is a mix of American and European options. It allows the option holder to exercise their option at different preset times before the expiration and on the expiration date. The preset times are generally well-spaced.

Binary option

The binary option is also referred to as an all-or-nothing option; this is because the option holder can only exercise their option if the underlying asset meets the contract’s preset conditions on the expiration date. If the contract fails to meet the conditions, it cannot be exercised and therefore expires worthless.

Canary option

An option that is canary-styled can only be exercised at quarterly intervals after a preset time frame. The preset time frame is generally one year and the ability to exercise ends before the option’s expiration date. This option style is considered a hybrid of the Bermudan and European styles.

Capped option

A capped option becomes automatically exercised once the market price of the underlying asset reaches a predefined amount. This amount is usually written in the contract thereby putting a cap on the profit that could be made when the option is exercised.

Compound option

This type of option is an option within another option, simply, it is buying an option on another option. The first option is known as the inner option. The compound option presents the option holder with two separate exercise dates, which enable the buyer to exercise the option twice. First on the first exercise date and secondly, on the option’s final maturity date.

Double option

A double type of option is one that combines both a call and a put option in one option contract. This means at the options expiration date, the option holder can sell and also buy the underlying asset. This option is common in commodities options that are traded over the counter.

European option

After the American option, this is another very popular option style. For the European options, they can only be exercised at one single preset point which is the expiration date. Most OTC options are European-styled and are commonly described as vanilla options.

Evergreen option

The holder of an evergreen option can only exercise their option after giving notice to the option seller. This notice usually gives the option seller time to prepare for the settlement of the option. The evergreen option is normally combined with other option styles such as American, Bermudan, European, or any other option style that the buyer and seller agree on.

Exotic option

Financial derivative contracts that contain a broad category of options that have complex financial structures are referred to as exotic options.

Shout option

A shout option lets the option holder exercise their option twice. First within the options expiration period and on the expiration date. The first exercise time is known as the shout; when an option seller shouts, the price of the underlying asset at that time is noted and locked in. If by the options expiration date the price on the shout date ensures a better payoff to the investor, then, it is used to settle the option instead of the price at the options expiration.

Swing option

The swing option is mainly used in trading commodity options in the energy sector. They allow the option holder the flexibility on the quantity of commodity taken and when. This means the commodity quantity swings either daily (daily contract quantities; DCQ), annually (annual contract quantities; ACQ), or the total contract quantities (TCQ). Thereby limiting the quantity that can be taken per time. If the stipulated constraint on a swing option is violated, the option holder pays a penalty.

Related: Warrants vs Stock Options Differences

Types of options based on the expiration cycle

- Long-Term Equity Anticipation Securities (LEAPS)

- Monthly options

- Quarterly options

- Regular options

- Weekly options

Long-Term Equity Anticipation Securities (LEAPS)

One of the main types of options is the LEAPS. These options have an expiration period that lasts from one to ten years depending on the contract specifications.

Monthly options

The expiration date of monthly options is the third Friday of the month. This is known as the expiration Friday.

Quarterly options

Quarterly options have five expiration dates that are spread within the nearest four quarters from the time the option was purchased and the final quarter of the subsequent year. These options are also referred to as quarterlies.

Regular options

Regular options have at least four different expiration dates within four different months. Investors can choose to exercise their options on any of the dates based on their investment strategy and preference.

Weekly options

These types of options have the shortest expiration period which is weekly. They are also referred to as weeklies and expire on Fridays.

Conclusion

There are various types of options to choose from when an investor decides to make use of these financial derivative contracts, it can therefore pose a challenge to choose one that is suitable and meets the investor’s specific plan. It is therefore important to carry out your personal research and also consult a professional before investing in any type of option.

Last Updated on November 8, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.