Are expenses liabilities? Expenses and liabilities both represent a cash outflow that is either incurred in the current period as an expense or to be settled on a future date in the case of a liability. Expenses and liabilities represent two distinct components in a company’s financial statements.

In this article, we see what these two items are, whether expenses are liabilities, and their comparison to show the areas in which they differ.

Related: What Type of Account is Cost of Goods Sold?

What are expenses?

An expense connotes a reduction in the value of an asset as it is used in revenue generation. In other words, it is the cost of operations that a company incurs in order to generate revenue, that is, the cost one is required to spend on obtaining something. An expense, therefore, implies the outflow of cash in return for goods or services.

In terms of the accounting equation, expenses bring about a productive decrease in the business owner’s equity. An expense can take the form of depreciation as it is charged over the useful life of a fixed asset. If the expense is meant for an immediately consumed item such as salary, then it is usually charged to expense as incurred. This brings about this popular saying, “it costs money to make money”.

Common expenses incurred include rent expenses, payments to suppliers, salaries and wages, factory leases, and depreciation. Businesses are allowed to write off tax-deductible expenses on their income tax returns in order to lower their taxable income as well as their tax liability. However, the internal revenue service (IRS) has strict rules on the expenses businesses have permission to claim as a deduction.

One of the primary goals of a company is to maximize profits which is achievable by boosting revenues while keeping expenses in check. Therefore, slashing costs can help companies to make even more money from sales. However, if a company cuts expenses too much, the effect could be detrimental. For example, paying less for advertising reduces costs/expenses but lowers the company’s visibility and ability to reach out to potential customers.

Companies can give a breakdown of their revenues and expenses on their income statements. Accountants use any of the two methods to record expenses, that is, the cash basis and the accrual basis. Under the cash basis accounting, expenses are recorded when they are paid. On an accrual basis, on the other hand, expenses are recorded when they are incurred. Meanwhile, expenses are generally recorded on an accrual basis in order to ensure that they match up with the revenues reported in accounting periods. Expenses are used to calculate net income using the equation, revenues minus expenses.

In accounting, expenses fall under two main categories namely operating expenses and non-operating expenses. Operating expenses are the expenses that are related to the main activities of a company such as the cost of goods sold, administrative fees, office supplies, direct labor, and rent. These are expenses that a company incurs from normal daily activities. To arrive at operating income, one has to deduct operating expenses from revenue. It is important for companies to manage their operating expenses in order to ensure profit maximization. This is usually achievable by minimizing expenses at a moderate level.

Non-operating expenses are expenses that do not have a direct relationship with the core operations of the business. Common examples are interest charges and other costs associated with borrowing money. From an accounting perspective, non-operating expenses are distinct from operating expenses in order for a company to determine the amount of revenue earned from its core activities.

What are liabilities?

Liability refers to an obligation of a company that brings about future sacrifices of economic benefits to other entities or businesses. It is simply a legally binding obligation payable to another entity. Liabilities as financial obligations are eventually settled through the transfer of cash or other assets to the other party. They may also be written off through the proceedings of bankruptcy.

A liability such as debt can be an alternative to equity as a source of a company’s financing. Some liabilities such as accounts payable or income taxes payable are essential for daily business operations.

Liabilities are recorded as a debit to an asset or expense account, depending on the nature of the transaction, and a credit to the applicable liability account. When the liability gets eventually settled, the liability account will be debited and the cash account credited from which the payment took place.

Liabilities are broadly categorized into noncurrent, current, and contingent liabilities on the balance sheet. Current or long-term liabilities are expected to be settled within a year, noncurrent liabilities are expected to be settled within a timeframe greater than one year, and contingent liabilities are probable in nature, that is, they may or may not arise. In essence, they are listed according to the time they are due.

According to the accounting equation, the total amount of liabilities must equal the difference between the total assets and equity.

Liability, therefore, connotes taking responsibility for something. Although they help a business in setting up profitable operations and speeding up value growth, they can bring about big problems such as a drop in financial performance and bankruptcy if they are not managed properly. Liabilities also have an effect on how liquid a company is and how its capital is set up. They are usually defined by past business transactions, events, sales, exchange of goods and services, or any other thing that could give the company an economic advantage in the future.

Related: Financial Leverage Ratios and Formula

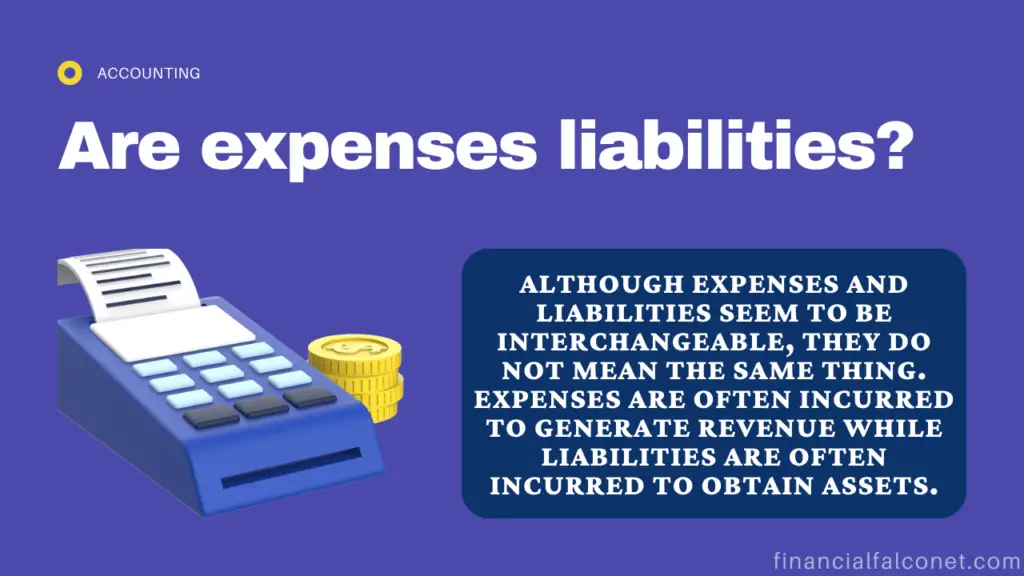

Are expenses liabilities?

Expenses are not liabilities although they seem to be interchangeable. In a way, expenses are a subset of liabilities, they are used differently to track a business’s financial health.

Paying expenses immediately keeps a business afloat. The balance sheet reflects business expenses by drawing down the company’s cash account and increasing accounts payable. Also, expenses are more immediate in nature and are paid on a regular basis. They are shown on a company’s monthly income statement to determine the company’s net income.

Failure to pay expenses makes it a liability. For instance, a company is unable to afford to pay cash to purchase its monthly office supplies. It then decided to take out a loan to pay for these expenses which then becomes a liability. The company will, however, still continue to track expenses monthly on its income statement to determine the net income.

When a company records an expense, it most obviously appears within a line item on the income statement. The income statement shows a business’s financial results for a designated period of time. An expense appears more indirectly on the balance sheet where there will always be a decline in the line item of retained earnings within the equity section, by the same amount as the expense. Also, either the assets section of the balance sheet will decrease by the amount of the expense or the liabilities section will increase by the expense amount thereby keeping the balance sheet in balance.

There will be a decline in cash assets if a company pays the expense item in cash, or inventory declines if some inventory is written off. The accumulated depreciation contra account will experience an increase if a depreciation charge is created. In terms of liabilities, accrued expenses will increase if an expense accrual or accounts payable is created, or if an unpaid supplier invoice is recorded.

Because expenses appear directly on the income statement and indirectly on the balance sheet, it is always important to read both the income statement and balance sheet of a company in order to see the full effect of an expense.

Expenses vs liabilities Differences and Similarities

In order to have a better understanding of why expenses are not liabilities, let us look at their differences.

| Expenses | Liabilities |

|---|---|

| It is listed on the profit and loss account and the income statement. | It is listed on the balance sheet. |

| Failure to pay expenses brings about the creation of liabilities as well as the malfunction of the company’s operations. | The failure to pay liabilities leads to default especially when it comes to noncurrent loans such as loans from nabks and other financial institutions and working capital. |

| Paid off in real-time as it can affect business operations. | Accrued and then paid off. |

| They are generally matched with revenue as they appear in a company’s income statement. | Generally related and matched up with an asset on the balance sheet. |

| Expenses are incurred to generate revenue for the company. | Generally incurred to generate an asset or a capital expenditure. |

| When expenses are incurred, payments are made during that period only. | Liabilities and incurred but the benefits are usually reaped over the years in the company’s lifetime. |

| It is basically the cost of operating a firm and running the business. | Basically incurred for a future date and future payments are owed or payable to creditors. On the balance sheet, liabilities follow a payment cycle which is generally known as a credit cycle. |

| Immediate in nature. | Not immediate in nature. |

| Can either be cash or noncash in nature. | Usually noncash in nature. |

5+ years of professional experience in the business and finance sector with 1 year experience as a sales associate.

Writer, Editor, and economic activist.