Accounting is a process whereby the financial transactions of a business or organization are recorded, classified, and summarised systematically. This is done in order to keep a chronological record of the business’s transactions. Hence, the accounting process requires constant updating of the business transactions which are guided by some accounting debit and credit rules in order to reflect an accurate and proper picture of the business’s financial statements. The accounting rules and standards are set by the International Accounting Standards Board (IASB).

In accounting, the use of debits and credits to keep accurate books, cannot be ignored. Hence, one has to learn and understand the accounting debit and credit rules to ensure one is actually doing the business’s accounting accurately. Without the accounting debit and credit rules, your books will end up unbalanced and sloppy which is a no-no for any business owner. In this article, we will discuss the golden rules of accounting that govern the accounting debit and credit rules and how they apply to different accounts. First, let’s have an understanding of debit and credit.

Related: Is Depreciation Expense Debit or Credit?

Debit and credit in accounting

Every business transaction which can be measured in monetary terms has to be accounted for in the accounting books of the business. In order to record such transactions, a system of debit and credit has to be used, which records each transaction through two different accounts. That is, whenever a business transaction occurs, at least two accounts are always impacted by a debit or credit entry.

This simply means that a debit entry is recorded against one account and a credit entry is recorded against another account. However, some business transactions may require debit and credit entries made to more than two accounts. Hence, there is necessarily no limit to the number of accounts involved in a transaction, though the minimum number of accounts involved in a transaction cannot be less than two accounts.

Recording debits and credits for each business transaction is required in bookkeeping. This is known as double-entry bookkeeping; an accounting system whereby you record debits and credits into two or more accounts for every transaction. That is, when recording transactions in your books, different accounts are impacted depending on the type of transaction.

What are the debit and credit rules in accounting

In Pacioli’s double-entry bookkeeping, a debit entry is said to be an accounting entry that either increases an asset or expense account or decreases an equity or liability account. A credit, on the other hand, is an accounting entry that increases either an equity or liability account or decreases an asset or expense account. In a ledger account, a debit is positioned on the left, so a debit column is usually on the left side of a ledger account. The credit column, on the other hand, is on the right side of a ledger account.

Debiting an account can cause it to either increase or decrease depending on the account in question, which is also the same for crediting an account. Therefore, in order not to get things mixed up, there are accounting debit and credit rules to be followed which are universally applicable and followed by everyone. These debit and credit rules in accounting bring uniformity in the presentation and the overall structure of the double-entry accounting concept. We will be discussing all the accounting debit and credit rules.

See also: Is Merchandise Inventory Debit or Credit?

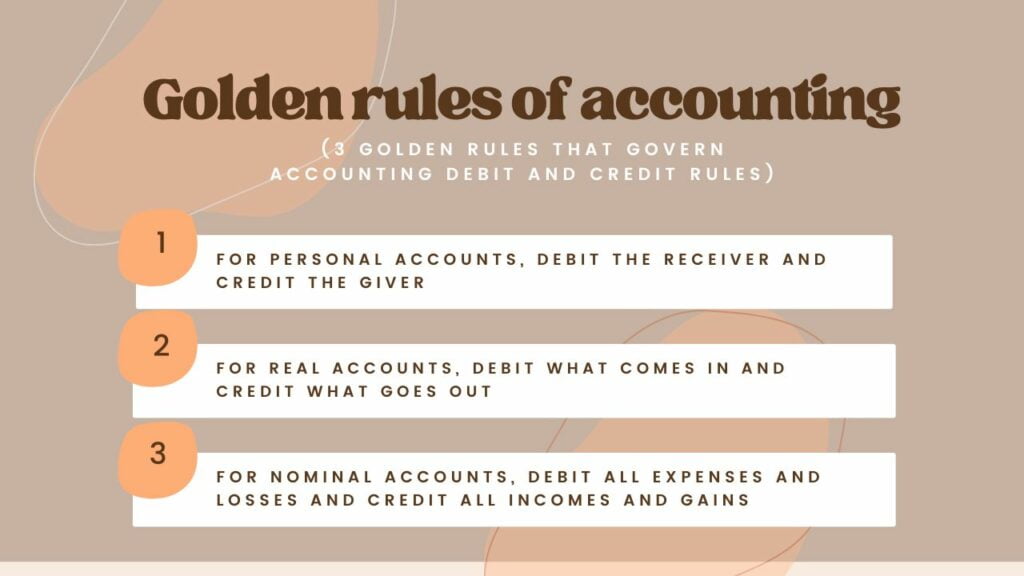

The golden rules of accounting that govern accounting debit and credit rules

- For personal accounts, debit the receiver and credit the giver

- For real accounts, debit what comes in and credit what goes out

- For nominal accounts, debit all expenses and losses and credit all incomes and profits

The rules listed above are the three golden rules of accountancy that form the basics of the debit and credit rules in accounting that guide the system of accounts. Hence, in order for a business owner to keep his/her books up-to-date and accurate, they have to follow these three basic rules of accounting.

The golden rules of accountancy govern the accounting debit and credit rules and apply to the three types of accounts related to a financial transaction, such as personal account, real account, and nominal account. The rules are, therefore, devised based on the nature of accounts and set differently for the different types of accounts.

For personal accounts, debit the receiver and credit the giver

One of the golden rules is to debit the receiver and credit the giver. This rule is applicable to personal accounts. A personal account is a general ledger account that contains transactions related to individuals or other organizations with whom the business has direct transactions.

These accounts are the ones that are related to individuals, companies, firms, groups of associations, etc., and are subdivided into a natural personal account, artificial personal account, and representative personal account. Hence, typical examples of personal accounts include customers, drawings, salary accounts of employees, vendors, creditors accounts, and capital accounts of owners, etc.

This golden rule means that if you receive something, you have to debit the account and if you give something, you have to credit the account. Let’s look at some examples to explain this rule further:

Example 1: To illustrate debit and credit rules in accounting for personal account

Assume you purchase some goods on credit from ABC Ltd worth $1,000. When accounting for this in your books, you will have to debit your Purchase Account and credit ABC Ltd. According to the debit and credit rule, you have to credit ABC Ltd because it is the giver that is providing the goods. Then, you have to debit your Purchase Account which is the receiver.

| Account | Debit | Credit |

|---|---|---|

| Purchase Account | $1000 | |

| Accounts Payable: ABC Ltd | $1000 |

Note that: In the event of a personal account rule, a company becomes the receiver when it gets money or credit from another company or individual while the other company or individual who gives it becomes the giver. When a company or individual gives something to a company, it becomes an inflow and therefore the company or individual must be credited in the books of accounts and the receiver needs to be debited.

In this example, you are the receiver because you get credit from ABC Ltd, so you are debited and ABC Ltd is credited as the giver.

Example 2: To illustrate accounting debit and credit rules for personal account

Assume you sell goods worth $500 to ABC Ltd. According to the accounting debit and credit rules for personal accounts, you have to debit the receiver- ABC Ltd. Your sale account is a nominal account and the Debtors Account is a Personal account. Hence, according to the golden rule, you will debit the receiver and credit the income or gain:

| Account | Debit | Credit |

|---|---|---|

| ABC Ltd Account | $500 | |

| Sales Account | $500 |

For real accounts, debit what comes in and credit what goes out

The second golden rule is to debit what comes in and credit what goes out. This rule is applicable to real accounts. A real account is a general ledger account that contains transactions related to the assets or liabilities of the business. They don’t close at the end of the accounting period and as such known as permanent accounts (balance sheet accounts). Rather, their balances are carried over to the next accounting period.

Real accounts can be asset accounts, liability accounts, or equity accounts. They also include contra assets, liability, and equity accounts. Therefore, typical examples of real accounts include accounts receivable, accounts payable, additional paid-in capital, cash, accumulated depreciation, etc. Real accounts also include tangible and intangible assets such as machinery, buildings, goodwill, patent rights, etc.

According to the rules of debit and credit for balance sheet accounts, when something comes into your business (for instance an asset like merchandise inventory), debit the account. Then, when something goes out of your business, credit the account. This golden rule means that you should debit what comes in and credit what goes out. Let’s look at an example to explain this rule further:

Example

Assume you purchased furniture for $3,000 in cash. According to the accounting debit and credit rules for real accounts, you will have to debit your Furniture Account (furniture comes in) and credit your Cash Account (cash goes out).

| Account | Debit | Credit |

|---|---|---|

| Furniture Account | $3,000 | |

| Cash Account | $3,000 |

For nominal accounts, debit all expenses and losses and credit all incomes and profits

The third golden rule is to debit all expenses and losses and credit all incomes and profits. This rule is applicable to nominal accounts. Nominal accounts are general ledger accounts that are used to track the revenue, expenses, profits, and losses of the business. These accounts are closed at the end of each accounting period and are also called temporary accounts. Hence, nominal accounts include revenue, expense, and profit and loss accounts which are reported on an income statement.

According to the accounting debit and credit rules for nominal accounts, you debit the account if the business has an expense or loss and credit the account if the business needs to record income or profit. Let’s look at some examples to explain this golden rule further:

Example 1: To illustrate accounting debit and credit rules for expense or loss

Assume you purchase $5,000 worth of goods from ABC Ltd. In order to record this transaction, in accordance with the accounting debit and credit rules for nominal accounts, you have to debit the expense ($5,000 purchase) and credit the real account- Cash Account (cash goes out, so it is credited according to the golden rule for real accounts).

| Account | Debit | Credit |

|---|---|---|

| Purchase Account | $5,000 | |

| Cash Account | $5,000 |

Example 2: To illustrate accounting debit and credit rules for income or gain

Let’s say you sell $2,000 worth of goods to ABC. In accordance with the accounting debit and credit rules for nominal accounts, you have to credit the income to your Sales Account and debit the real account- Cash Account (cash comes in, so it is debited according to the golden rule for real accounts).

| Account | Debit | Credit |

|---|---|---|

| Cash Account | $2,000 | |

| Sales Account | $2,000 |

Related: Is Depreciation Expense Debit or Credit?

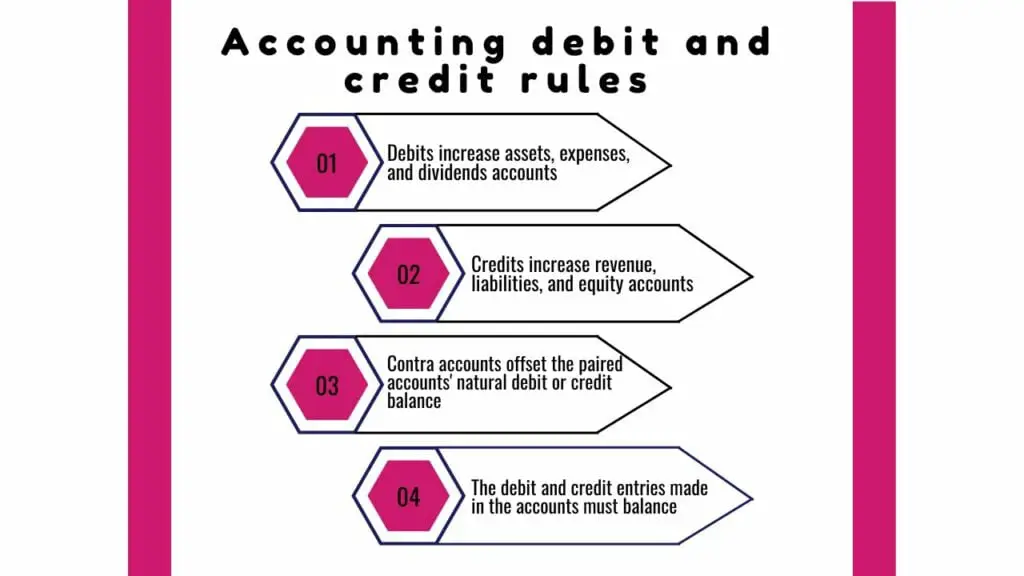

Accounting debit and credit rules by accounts

- Debits increase assets, expenses, and dividends accounts

- Credits increase revenue, liabilities, and equity accounts

- Contra accounts offset the paired accounts’ natural debit or credit balance

- The debit and credit entries made in the accounts must balance

The golden rules of accounting form the basis of these accounting debit and credit rules listed above. They are the accounting debit and credit rules for each type of account. Knowing these rules helps you to determine which accounts are increased by a debit (or decreased by a credit) and which accounts are increased by a credit (or decreased by a debit).

The debit and credit rules in accounting actually reflect the balance sheet equation which is expressed as:

That is, accounts that are assets, which is on the left side of the equation would be increased by a debit. Whereas an account that is a liability or equity, which is on the right side of the equation would be increased by a credit. This means that assets are debits while liabilities and equity are credits. Recall, that just like in this equation, a debit column is usually on the left side of a ledger account while a credit column is on the right side of a ledger account.

Let’s further discuss the rules governing the use of debits and credits in a journal entry for several accounts.

Debits increase assets, expenses, and dividends accounts

All accounts that usually contain a debit balance will increase in amount when a debit entry is added to them and will decrease when a credit entry is added to them. This particular accounting debit and credit rule applies to accounts such as expenses, assets, and dividends. This means that you record assets, dividends, and expenses as a debit and not a credit. That is, expenses, assets, and dividends contain a debit balance that will increase in amount when debited and reduce when credited.

The table below shows accounts that increase and decrease with a debit entry:

| Accounts | Debit |

|---|---|

| Assets + | Increase |

| Liability – | Decrease |

| Equity – | Decrease |

| Expenses + | Increase |

| Income / Revenue – | Decrease |

| Dividend + | Increase |

For a better understanding of the type of transaction that should be entered as a debit in accordance with the accounting debit and credit rules, let’s look at an example:

Jenny’s beauty shop sells hair gel to a customer for $50 and gets paid in cash. Cash is an asset and from the table above, we can tell that assets increase by debiting it. So, Jenny would record this $50 increase in cash as a debit to the asset account of Jenny’s books. This is what debiting the asset account would look like:

Jenny’s beauty shop

| Account | Debit | Credit |

|---|---|---|

| Asset Account (or Cash Account) | $50 |

Note that according to the accounting debit and credit rules, this transaction is not yet balanced because it needs a credit entry in another account to complement it.

Credits increase revenue, liabilities, and equity accounts

All accounts that usually contain a credit balance will increase in amount when a credit entry is added to them and will decrease when a debit entry is added to them. This particular accounting rule applies to accounts such as revenue, liabilities, and equity accounts. This means that you record equity, liabilities, and revenue as a credit and not a debit. That is, according to the accounting debit and credit rules, revenue, liabilities, and equity accounts should contain a credit balance that will increase in amount when credited and decrease when debited.

The table below shows accounts that increase and decrease with a credit entry:

| Accounts | Credit |

|---|---|

| Assets – | Decrease |

| Liability + | Increase |

| Equity + | Increase |

| Expenses – | Decrease |

| Income / Revenue + | Increase |

| Dividend – | Decrease |

In order to understand the type of transaction that should be entered as a credit, let’s look at an example:

Recall, in our preceding example, Jenny’s beauty shop sold some hair gel for $50 cash. Also, remember that in double-entry accounting, there is always an equal credit entry to a debit entry, to balance out the transaction. The sale of this hair gel would be labeled as income for Jenny’s beauty shop. Revenue/ income as seen from the table above, increase by crediting it. So, Jenny would record this $50 income as a credit to the revenue account of Jenny’s books. This would now balance the transaction as shown below:

Jenny’s beauty shop

| Account | Debit | Credit |

|---|---|---|

| Asset Account (or Cash Account) | $50 | |

| Revenue Account | $50 |

The transaction is now balanced since the debit entry is now complemented with an equal credit entry. Hence, the transaction will be reflected properly on Jenny’s beauty shop’s financial statements in the future.

It is important to note that debit entries are always listed first and on the left side of the ledger, while credits are listed on the right.

Contra accounts offset the paired accounts’ natural debit or credit balance

The accounting debit and credit rules for contra accounts require that since contra accounts reduce the balances of the accounts with which they are paired, their natural balance would be contrary to the paired account. This means a contra account paired with an asset account would have a credit balance that is opposite to the natural debit balance of an asset account.

There are four main types of contra accounts which are contra asset, contra liability, contra equity, and contra revenue. These accounts are usually reported on the same financial statement as the associated account. They are usually used in a general ledger to reduce the value of the related account when the two are netted together. Hence, according to the accounting debit and credit rules, the natural balance of a contra account has to be the opposite of the associated account. See the table below:

| Contra account | Type of contra account (with associated account) | Debit/Credit |

|---|---|---|

| Contra asset account (offsets the debit balance of assets) | Allowance for doubtful accounts (Accounts receivable) Accumulated depreciation (Fixed asset) | Credit |

| Contra liability account (offsets the credit balance of liabilities) | Discount on notes (Notes payable) Bond discount (Bonds payable | Debit |

| Contra equity account (offsets the credit balance of equity) | Treasury stock (Equity) | Debit |

| Contra revenue account (offsets the credit balance of revenue) | Sales discounts, Sales returns, and Sales allowances (Gross revenue) | Debit |

The debit and credit entries made in the accounts must balance

In a transaction, the total amount of debits must equal the total amount of credits. This is one of the most important rules amongst the accounting debit and credit rules. If this rule is not adhered to, a transaction would be unbalanced, and the business’s financial statements will be inherently incorrect. Some accounting software packages will even flag any journal entries that are unbalanced so that they cannot be entered into the system until they have been corrected.

In simple terms, have it in mind that whenever you add or subtract money from an account you’re using debits and credits. Hence, a debit would be any money that is coming into an account, whereas a credit would be any money that is leaving an account. Therefore, the same amount must be entered as a debit entry in one account and as a credit entry in another account. This means that for every transaction, the totals of the debits and credits must always equal each other so that the transaction is said to be in balance.

Related: Utilities Expense Debit or Credit?

Examples of the application of accounting debit and credit rules in journal entries

Assume, you own a business and decide to purchase a piece of new equipment for your business and on the 1st of September, you purchase this equipment for $15,000. This equipment is an asset, so according to the accounting debit and credit rules, you must debit $15,000 to your Fixed Asset account to show an increase in the account. Also, you purchased the equipment on credit which also means your liabilities have increased. To record the increase in the liabilities in your books, you have to credit your Accounts Payable account with $15,000.

Your record of the new equipment purchase would look like this:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 1st Sept | Fixed Assets: Purchase of equipment | $15,000 | |

| Accounts Payable | $15,000 |

Furthermore, let’s assume on the 10th of September, you made sales on credit worth $500 to a customer. This sale is revenue, so according to the according debit and credit rules, you must credit the revenue account with $500. Your customer didn’t pay cash so you don’t increase the Cash account, rather you increase your Accounts Receivable account with a debit of $500 since the goods were bought on credit.

Your record of this sale would look like this:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 10th Sept | Accounts Receivable: Sale to a customer on credit | $500 | |

| Revenue | $500 |

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.