For accounting purposes, revenue is recorded on a company’s statement of income rather than on the balance sheet where assets, liabilities and equity are recorded. Revenue is not an asset or equity, rather it is used to invest in other assets of the company, settle liabilities, and pay dividends to shareholders.

In this article, we will discuss, revenue, assets and equity and the reasons why revenue is not an asset or equity.

Related: Return on assets

What is revenue?

Revenue is the money generated by a company from its normal business operations. This is the money that the operation of the business brings to a company. It is the gross income returned by investment which can be calculated as the average sales price multiplied by the number of units sold. Revenue appears first on a company’s income statement and as such is known as the top line figure.

Revenue is also known as sales on the income statement. Since revenue can also be referred to as sales, it can be used in the price-to-sales (P/S) ratio which is an alternative to the price-to-earnings (P/E) ratio that has revenue as its denominator. The net income of a company, also known as the bottom line, is expressed as revenues minus expenses. Therefore, in order to ascertain the net income a company attained, costs are subtracted from the revenue (gross income). That is, profits are made in business when revenues exceed expenses. In order for a company to increase its profits and earnings per share (EPS) for its shareholders, revenue has to be increased and expenses reduced.

Investors, when evaluating the health of a business, investors consider the revenue and net income of a company separately. This is because a company’s net income can grow even when its revenues can remain stagnant due to cost-cutting. Therefore, revenues and earnings per share are the two figures that tend to get a lot of attention when public companies report their quarterly earnings.

Revenues, in more formal usage, are calculated and estimated based on particular standard accounting practices or based on the rules established by a government or government agency. Based on standard accounting practices, revenue can be calculated differently using cash basis accounting or accrual basis accounting. These two common accounting methods do not use the same process for measuring revenue.

The sales that the company makes on credit for goods or services delivered to the customer are included in accrual accounting, as revenue. That is, revenue under accrual accounting is recognized even if the payment has not yet been received. Cash basis accounting, on the other hand, will only recognize sales as revenue when payment is received. The cash paid for the goods or services to the company is known as a receipt.

Furthermore, it is possible for a company to have receipts without revenue. For instance, a customer can pay for a service in advance that has not been rendered to him/her by the company or a customer can pay for goods in advance that the company has not yet delivered to the customer. In such a case, the transaction will result in a receipt and not revenue.

Revenue account

In financial accounting, the revenue account is the financial account that contains the receipts of the income or revenue that the company receives through its business transactions. All income statements include revenue information and this revenue information is a good measure of how well the business is doing on the commercial front. Generally, a high revenue turnover would indicate business success whereas, a low revenue turnover would indicate that the business has some issues.

In a double-entry bookkeeping system, Revenue accounts are general ledger accounts that are summarized periodically on an income statement under the heading Revenue or Revenues. On an income statement, the kind of revenue is described in the revenue account such as Repair service revenue, Rent revenue earned, or Sales.

All increases in equity such as services rendered, sales, rental income, membership fees, recurring receivables, interest from investment, interest income, donations, etc are recorded in the revenue accounts. In an income statement, there are two kinds of revenue which are operating revenues and non-operating revenues.

The money that the company earns from its principal business operations is the operating revenues. Generally, this forms a greater part of the total income of a company. Typical examples of operating revenue are when the business earns income from making a sale to a customer, either from a product or a service rendered; others include rental income and payment from professional services (professional income). The most common ways that companies usually earn revenue are from services and sales.

The money that the company earns from business activities that are not its core business operations is nonoperating revenue. A typical example of this is the interest that the business receives from investments known as interest income. Other examples of nonoperating revenues include dividend income and asset sales.

Conclusively, the subgroups that are generally found within revenue accounts include:

- Interest income

- Dividend Income

- Investment Income

- Service revenue

- Sales revenue

- Rent Income

Now, that we have an understanding of what revenue is; to answer the question of whether revenue is an asset or equity, let’s look at what an asset is in a company’s financial statements.

See also: Is preferred stock an asset?

What are assets?

Assets are anything of value or resources that are owned by an individual, corporation, or country with expectations that they will provide future economic benefit. An asset adds value to a business and is used to generate income/revenue and reduce expenses. That is, owning an asset enables a business to meet its commitments and increase its equity.

Assets contain economic value and can benefit the operations of a company, increase the value of a business, or raise an individual’s net worth. A business having a high proportion of assets compared to its liabilities is an indicator of a successful business. This is because more assets to liabilities indicate a higher degree of liquidity. Assets can be available for long-term sale, currently available to sell, or used for the daily operation of a business. However, in order to own more assets, companies can make use of their revenues or liabilities to purchase assets. Therefore, revenue is not an asset but can be used to invest in assets. Simultaneously, assets can be used too to generate revenue.

Revenue, just like assets can increase the value of a business but is not a type of asset. Assets can be grouped into different types based on physicality, liquidity, and operating activities. These different kinds of assets appear on a company’s balance sheet and are created or bought to increase the value of a business or benefit the business’s operations.

Based on physicality, assets could be tangible or intangible. Tangible assets are the company’s physical and real property such as cash, machinery, real estate, equipment, bonds, furniture, inventory, etc. The majority of tangible assets are considered current assets because they are easily converted to cash. Intangible assets, on the other hand, are items or goods that do not exist physically but exist theoretically such as permits, logos, business licenses, intellectual property, brand reputation, patents, and trademarks. These assets cannot easily convert to cash and have their value boosted through successful use.

Assets, based on their liquidity, can also be grouped into current and fixed assets. Current assets are highly liquid because they can be sold and converted into cash easily. Typical examples of current assets are cash, inventory, accounts receivable, prepaid expenses, and financial assets such as mutual funds, bonds, stocks, and other marketable securities.

Fixed assets, on the other hand, are generally considered to have low liquidity because they may take a long period of time to earn cash value. They are also known as noncurrent assets, hard assets or long-term assets and usually cannot be converted into cash within one year or be sold at their desired value quickly. Typical examples include land, buildings, furniture, or any other type of asset that is not intended for sale within the year.

Moreso, assets can be grouped into operating and non-operating assets depending on whether they are used for the operational activities of the company. Operating assets are assets that generate revenue or income through the day-to-day business operations and help maintain workflows such as machinery, licenses, copyrights, or inventory.

Non-operating assets, on the other hand, are business-owned items that generate revenue even though they are not necessarily needed for the day-to-day running of the business. Non-operating assets examples include vacant land or short-term investments.

Revenue is definitely not an asset, but is it equity? Let’s look at equity in a company’s financial statements.

Related: Is the common stock a current asset?

What is equity?

Equity which is usually referred to as shareholders’ equity (or owners’ equity for privately held companies) can be found on a company’s balance sheet. In a case of liquidation, equity represents the amount of money that would be returned to the shareholders of a company if all the company’s assets were liquidated and all the debt of the company had been paid off. In the case of acquisition, equity is the value of the company sales minus any liabilities that the company owes not transferred with the sale of the company.

This means that equity represents ownership of a company’s shares in proportion and can be thought of as a degree of residual ownership in a company or asset after subtracting all debts associated with the company or asset. Therefore, shareholder equity can represent a company’s book value and is one of the most common pieces of data used by analysts to assess a company’s financial health. Hence, it is used in several key financial ratios such as return on equity (ROE).

Equity can sometimes be offered as payment-in-kind. It can be found on a company’s balance sheet together with assets and liabilities. The equity of a company represents the owners’ or shareholders’ stake in the company which is calculated as the company’s total assets minus its total liabilities.

Hence, equity happens to be of utmost importance to a business owner or shareholders because it is their financial share of the company. It is basically the portion of the company’s total assets that the owner fully owns which may be in cash or assets such as buildings and equipment. Therefore, equity can also be referred to as net worth.

Take, for instance, a company that purchases a $50,000 asset with a $40,000 loan and $10,000 in cash. The company has acquired an asset of $50,000 but has only $10,000 of equity. The balance sheet equation states that:

Assets= Liabilities + Owner’s Equity

From our example, we can see that this equation holds as the company’s $50,000 Asset = $40,000 Liability + $10,000 Owner Equity.

Revenue is therefore not equity but has an impact on the shareholders’ equity on the balance sheet. An increase in an asset account from the use of revenue will definitely cause a matching increase in an equity account. Moreso, revenue is used to pay dividends to shareholders. There are three types of equity accounts that will meet the needs of many businesses. These equity accounts have different names depending on the structure of the company:

- Contribution (money invested): There are times when the owners of the company must invest their own money into the business of the company. The money invested may be start-up capital or a later infusion of cash. When this contribution occurs, a Capital account or Investment account is credited.

- Distribution or Draw (money withdrawn): If the business of a company is profitable, the owners usually want some of the profit returned to them. In order to track this transaction, a Draw account or Distribution account is debited. This is the only Equity account (non-contra) that is debited.

- Accumulation from prior years: To track the net income of a company as it accumulates over the years, the Owner’s Equity or Retained Earnings are credited. Most accounting programs on the first day of the fiscal year automatically credit this account with the net income of the previous year.

See also: Accumulated depreciation on balance sheet

Is revenue an asset or equity?

Revenue is not an asset or equity. For accounting purposes, revenue, asset, and equity are very different accounts. Revenue will appear on a completely different part of a company’s financial statements compared to an asset and equity account. The revenue account is shown on a company’s income statement whereas assets and equity are listed on the company’s balance sheet.

Revenue refers to the money generated by a company from its normal business operations which is recorded on the income statement rather than on the balance sheet with assets and equity. An asset is any item that will provide an economic value to the company whereas equity represents the owners’ or shareholders’ stake in the company.

Revenue is therefore not an asset or equity rather it is used to invest in assets, pay off liabilities, and pay dividends to shareholders. However, even though revenue is not recorded on a balance sheet like the asset and equity, it is accounted for on a balance sheet using other entries, like cash, sales, and accounts receivable. This is usually done through a double entry system which uses debits and credits.

A double-entry system records a debit on the left side of the balance sheet and a credit on the right side of the balance sheet. The two sides need to be in balance, hence the term balance sheet.

If a company makes sales or renders services and the resulting revenue has not yet been collected, then the amount to be collected will fall under Accounts receivable on a company’s balance sheet. Accounts receivable accounts for funds that clients or customers owe a company for receiving a good or service. When the company creates an invoice for this transaction, it should be accounted for through a debit entry to the Accounts receivable account and a credit to the Sales account or Service revenue.

Then, when the invoice is paid, a credit entry will be made to accounts receivable and a debit entry to the Cash account. Though the revenue is not an asset, the accounts receivable and cash generated by the sales revenue are recorded as a current asset on the balance sheet.

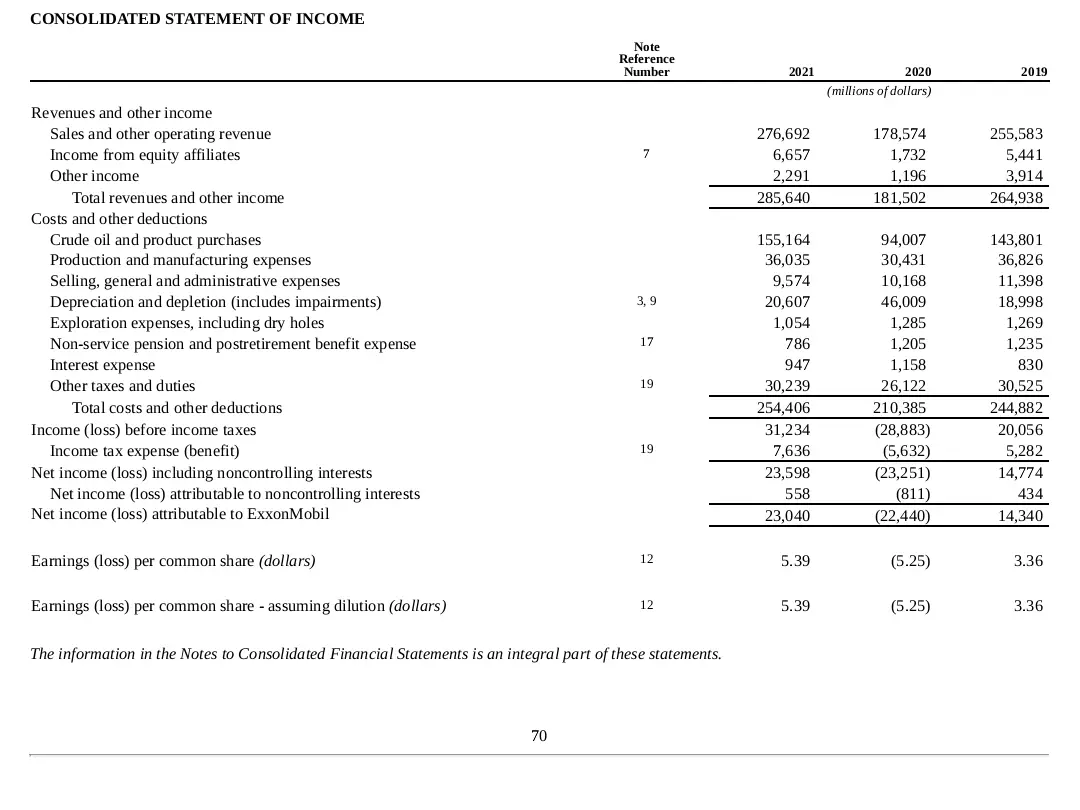

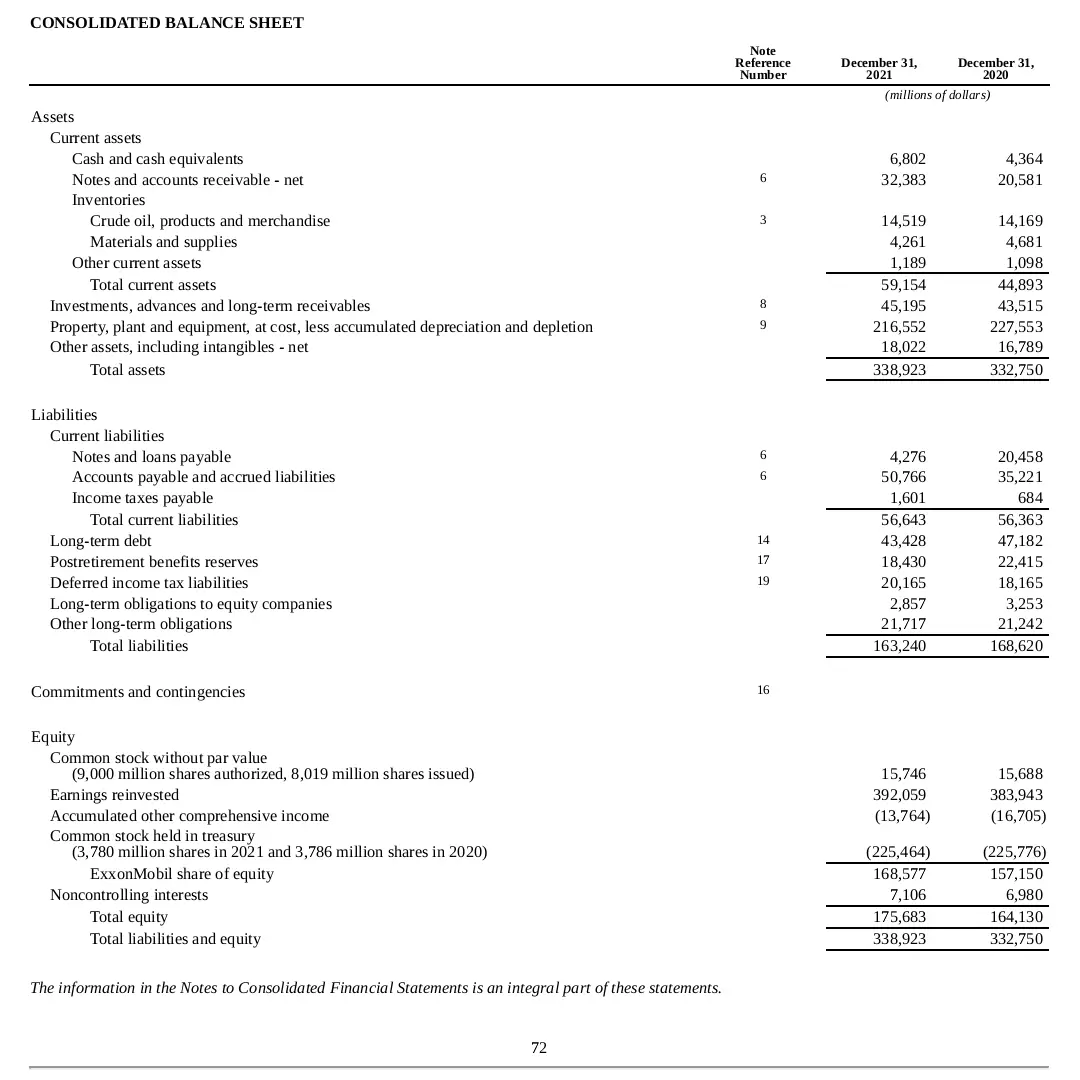

Let’s look at how revenue, assets, and equity are accounted for in a company’s financial statements. Using the Exxon Mobil Corporation (XOM) as an example, below is an excerpt of Exxon’s income statement and balance sheet from its 10K statement (pages 72 & 74) for 2019, 2020 and 2021:

As seen in the image above, revenue usually appears at the top of the income statement and is normally known as the top-line figure. We can see that revenue appears in the company’s income statement and not on the balance sheet below where assets, equity and liabilities appear:

As seen in the image above revenue will appear on a completely different part of a company’s financial statements compared to the asset and equity that are listed on the company’s balance sheet. Nevertheless, even though revenue usually appears on the income statement, it also has an impact on the balance sheet.

Revenue has an impact on Cash in the asset account in the sense that, if the payment terms of a company are cash only, then revenue also creates a corresponding amount of cash on the balance sheet. Likewise, it also has an impact on the asset- Accounts Receivable, if the payment terms of the company allow credit to customers. In such cases, revenue will create a corresponding amount of accounts receivable on the balance sheet.

Alternatively, if the company makes a sale in exchange for some other asset then some other asset on the balance sheet might increase.

Conclusively, revenue not only has an impact on the asset on the balance sheet but also has an impact on stockholders’ equity. As revenue cause an increase in assets, it also creates an offsetting increase in the stockholders’ equity part of the balance sheet, where retained earnings will increase. Therefore, the impact of revenue on the balance sheet is an increase in an asset account and a corresponding increase in an equity account.

See also: What are equity stocks?

Why revenue is not an asset or equity

Revenue is not an asset or equity because it has a separate account of its own in accounting. In accounting, revenue is the total amount of income gotten from the sale of goods and services about the primary operations of a business. At the accounting year’s end, all revenue account credit balances have to be closed and then transferred to the capital account, hence increasing the business owner’s equity. Therefore, revenue in business is responsible for an increase in equity. Moreso, since credit balance is the normal balance for a business’s equity, revenue is recorded as a credit.

Also, revenue is not an asset or equity because it is used to invest in assets, pay off liabilities, and pay dividends to shareholders. Hence, revenue itself is not an asset or equity. Also, assets can be used to generate revenue. When it comes to bookkeeping, revenue has a separate account of its own from the asset and equity accounts. The table below shows the 5 major accounts in a company’s Charts of Accounts (COA):

| Types of account | Definition | Examples (sub-accounts) | Debit | Credit | |

|---|---|---|---|---|---|

| 1 | Revenue account | The revenue account is the financial account that contains the receipts of the income or interest from investments that the company receives through its business transactions | Sales revenue, service revenue, interest income, investment Income | Decrease | Increase |

| 2 | Asset account | Assets are items of economic value that provide future economic benefits to a company | Cash, accounts receivable, inventory, prepaid expenses, savings account, petty cash balance, vehicles, buildings, undeposited funds, property and equipment | Increase | Decrease |

| 3 | Equity account | The equity account is an account recording the owners’ or shareholders’ stake in the company which is calculated as the company’s total assets minus its total liabilities | Available-for-sale securities, stocks (common stock and preferred stock, treasury stock), bonds, mutual funds, real estate, pension and retirement plans, derivative instruments, debt security | Decrease | Increase |

| 4 | Liability account | Liabilities are the debts and obligations that a company has to pay | Accounts payable, income tax payable, loans payable, bank fees, accrued liabilities, payroll liabilities, notes payable | Decrease | Increase |

| 5 | Expense Account | These are monetary charges needed for the day-to-day operation of a business | Advertising, utilities, rent, travel, salaries | Increase | Decrease |

Obotu has 2+years of professional experience in the business and finance sector. Her expertise lies in marketing, economics, finance, biology, and literature. She enjoys writing in these fields to educate and share her wealth of knowledge and experience.