Businesses carry out various transactions every single day and have to keep track of each transaction. To do this, they record the transactions by making journal entries. These journal entries serve as the bedrock of a company’s operation as they provide the management, external and internal auditors, and the accounting team with vital information about how much money is coming in or going out of a company.

The information from the journal entries made further impacts all the company’s financial statements which include its income statement, statement of cash flows, and statement of financial position.

Here, we shall look at various journal entries in accounting examples but before then, let us have a basic understanding of what journal entries are.

See also: Deferred revenue journal entry with examples

What are journal entries in accounting?

Journal entries in accounting are ways of recording the transactions that occur in a company. These journal entries are the foundation of the double-entry accounting system and are the most common accounting system used by businesses to track daily operational and non-operational transactions. When preparing tax reports or financial statements, the various journal entries made serve as a reference point that has tracked revenues and expenses or the assets, liabilities, and equity of the company.

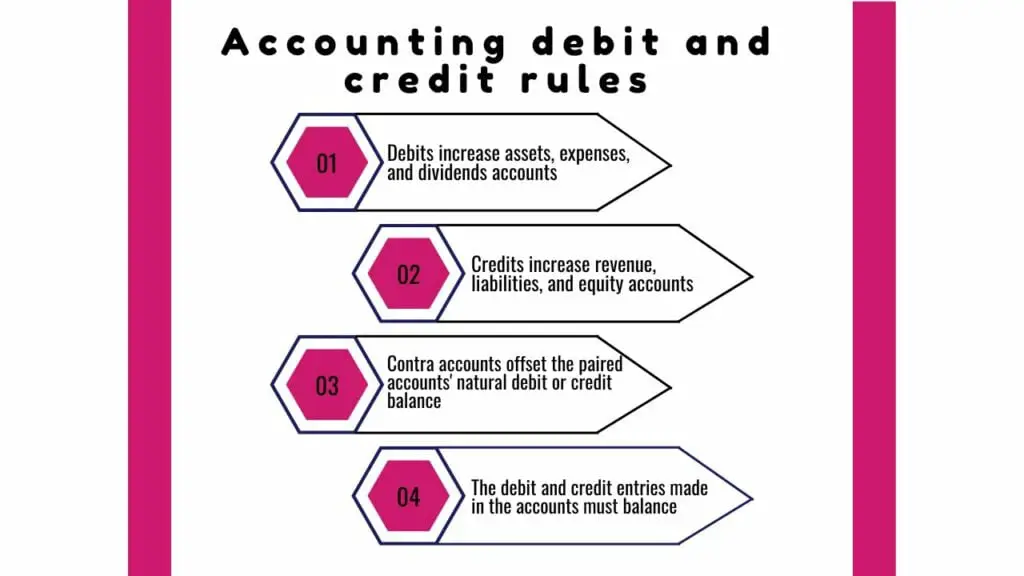

In accounting, journal entries are made based on the principles guiding debits and credits. These principles stipulate that for every transaction made, a debit and a credit must be recorded; this follows the double-entry accounting system.

For every debit made, an equal but opposite credit has to be made to ensure the balance at the end of every transaction is equal to zero. That is if a debit of $10 is made an equal but opposite credit of $10 has to be made too. No matter the number of accounts involved in a transaction, the rule of having equal but opposite entries applies. Otherwise, the journal entries wind up being inaccurate and sloppy.

Journal entries are usually recorded in a general ledger or specialty ledger. Depending on the company and its method of accounting, all transactions made may be recorded in the general ledger or the specialty ledger depending on which kind of transaction it is.

Transactions that do not fall within any of the specialty journals are then recorded in the general ledger. The specialty journal includes cash disbursement, sales, purchases, and cash receipts journals. Some companies may have additional specialty journals but the aforementioned represent the four most common specialty journals used by most companies.

Using debits and credits to make journal entries in accounting

When making journal entries, debiting and crediting the right account for the transaction that has been carried out is key to having a balanced report at the end of the accounting period. Debits and credits affect the balance of accounts differently, while a debit might reduce one account, it might increase another account. Below is a table that shows the five broad classifications of the various accounts for which journal entries are commonly made and how debit and credit affect the account balance.

| Account | Debit | Credit |

|---|---|---|

| Assets | Increase | Decrease |

| Equity | Decrease | Increase |

| Expenses | Increase | Decrease |

| Liabilities | Decrease | Increase |

| Revenue | Decrease | Increase |

Assets are resources both physical and non-physical that are owned by companies and bring economic value to them. Some asset accounts include cash, goodwill, accounts receivable, merchandise inventory, land, equipment, and notes receivable.

Equity is the income companies make from the sale of preferred and common stock as well as the money it has retained from their profits. Equity accounts include capital stock and retained earnings.

Expenses are the monies spent by companies during operations. Some expense accounts include salaries, cost of goods sold (COGS), rent, depreciation, utilities, and supplies.

Liabilities are what the companies owe to creditors. Some liabilities accounts include accounts payable, taxes, unearned service revenue, notes payable, and unearned revenue.

Revenue is the income realized from the operations of companies. This can be the sale of goods or provision of services or both. Some revenue accounts include service revenue, sales, and revenue.

In addition to these five aforementioned account types, there are four other broad accounts known as contra accounts. These accounts have a contrary balance to the natural balance of the account with which they are paired. For instance, the contra asset account will decrease with a debit and increase with a credit. The table below outlines how debit and credit affect the contra accounts.

| Account | Debit | Credit | Examples |

|---|---|---|---|

| Contra assets | Decrease | Increase | Allowance for doubtful accounts and accumulated depreciation |

| Contra equity | Increase | Decrease | Treasury stock |

| Contra liability | Increase | Decrease | Discount on notes and bond discount |

| Contra revenue | Increase | Decrease | Sales discounts, sales returns, and sales allowances |

How to make journal entries in accounting

- Identify the transaction accounts

- Sort the transaction

- Determine debits and credits

- Make the journal entry

Before we look at the various journal entries in accounting examples, we need to understand how journal entries are made. Making accurate journal entries is pertinent to having accurate financial statements. Companies that use various accounting software generally make fewer entries since most of this software embeds some level of automation.

Companies that mainly do their bookkeeping manually or use manual bookkeeping as a backup for the software have to make quite a number of journal entries daily. For these journal entries to be accurate the following steps will serve as a guide.

Identify the transaction accounts

When transactions occur, they affect specific accounts; identifying which account will be included in a particular transaction is therefore important. As a guide to making the right journal entry, know which account will gain from the transaction and the corresponding account that will lose.

Sort the transaction

The aim here is to identify what kind of transaction has just occurred clearly. Determining whether it is an asset, revenue, expense, liability, or equity account is pertinent. This will aid you in knowing how to make the entry with ease and accuracy. It also tells which accounts will be involved in the transaction alongside each other since journal entries generally involve two or more accounts.

Determine debits and credits

We have seen earlier that debits and credits work differently in the various types of accounts, hence determining which account will be debited or credited is a major determining factor in making the right journal entries. To make accurate debits and credits, trace where the money came from and where it is going. The accounting debit and credit rules will be an important guide here.

Make the journal entry

Now that the previous steps have been completed, it is time to make the journal entry. Every journal entry must have a date, this serves to ensure that it is accounted for in the right accounting period. The particular accounts involved in the transaction as well as the exact amounts debited and credited are also recorded. Make a table with four columns; starting from the first column to the fourth, they will contain; the date of the transaction, the accounts involved in the transaction, the amount debited, and the amount credited.

Some journal entries might have two additional columns to record the transaction number and a description of the narration. But in order not to complicate things, the examples of journal entries in accounting that we will look at here will use the four-column entry. Hence a typical journal entry example will look like the following table:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Name of account to debit | $$ | |

| Name of account to credit | $$ |

Now that we understand what a typical journal entry will look like, let us have a look at the various examples of journal entries in accounting for assets, expenses, equity, liabilities, revenue, and contra accounts.

See also: Sale of Assets journal entry examples

Types and Examples of Accounts for Journal Entries

- Assets and contra assets

- Equity and contra-equity

- Expenses

- Liabilities and contra liability

- Revenue and contra-revenue

Although all journal entries made in accounting for various transactions typically involve debit and credit, the accounts being debited or credited vary. This variation is based on what transaction was carried out and whether it reflects an increase or a decrease in an account. Let us take a look at the various journal entries when dealing with any of the account types listed above.

Examples of assets and contra assets accounts and their journal entries

- Accounts receivable

- Accumulated depreciation

- Cash

- Equipment

- Investment

- Land

- Merchandise inventory

- Notes receivable

Assets accounts are accounts that record resources that are a source of positive economic gains to the companies that own them. Contra assets accounts are associated with the various assets accounts; they have a balance that is contrary to that of the assets accounts.

Accounts receivable

When companies provide goods or services to customers on credit, the amount that the customer owes the company for the good or service received is recorded in the accounts receivable (AR). Hence the accounts receivable balance is equivalent to the outstanding invoices of the company.

When recording a transaction that involves the account receivable, a debit is made to the accounts receivable and a credit to the revenue account. The journal entry will look like the table below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accounts receivable | $$ | |

| Revenue | $$ |

When the amount owed by the customer is paid up, the company will record the transaction as a debit to the cash account and a credit to the accounts receivable. This signifies that there has been an increase in the company’s cash and a decrease in the amount owed to it by customers. The journal entry will be similar to the table below:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Account receivable | $$ |

There are instances however where customers that owe the company are unable to pay mostly due to bankruptcy or some other challenges; when this occurs, the amount owed will be considered as a bad debt by the company. Bad debt is debt that is deemed unrecoverable. In such situations, the company can write off the bad debt directly or create an account known as the allowance for doubtful accounts.

Hence, the exact amount of receivables or net receivables that the company actually expects to retrieve is the difference between the sum of all the receivables minus the sum of the bad debt and doubtful accounts.

If the company writes off the bad debt directly, the amount written off impacts the profit and loss account by reducing the net profit that will be reported by the company. The journal entry for the bad debt will be as follows:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Bad debt | $$ | |

| Account receivable | $$ |

If on the other hand, the company creates an allowance for doubtful accounts, it shows that the company is unsure if the amount owed will become bad debt or will be eventually paid up. Hence the amount recorded in the allowance for doubtful accounts will not impact the profit and loss account of the company. The allowance for doubtful accounts is sometimes called a bad debt reserve. An allowance for doubtful accounts will be recorded as shown below:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Bad debts expense | $$ | |

| Allowance for doubtful accounts | $$ |

If the transaction recorded above turns out to be bad debt, it will be recorded as a debit to the allowance for doubtful accounts and a credit to the accounts receivable. The journal entry to record such transaction will be as follows:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Allowance for doubtful account | $$ | |

| Account receivable | $$ |

If peradventure the doubtful account gets paid, it is recorded as a debit to the accounts receivable and a credit to the allowance for the doubtful accounts. The journal entry will be as follows:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Account receivable | $$ | |

| Allowance for doubtful account | $$ |

Accumulated depreciation

Accumulated depreciation is an account that records the decrease in value of an asset over its useful lifespan. It is the total amount of depreciation expense for an asset that has been recognized from the time of the asset’s purchase until the period under review. On the balance sheet, accumulated depreciation is reported as a contra asset, this reduces the book value of assets that depreciate with use.

To make a journal entry for the accumulated depreciation of assets, the depreciation expense account is debited with the estimated amount of either monthly or yearly depreciation while the accumulated depreciation account gets credited as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Depreciation expense | $$ | |

| Accumulated depreciation | $$ |

Cash

Cash is one of the most used assets of companies, it is used for the purchase of assets, settling of liabilities, and other operational expenses. Companies also get to receive cash for the goods or services they offer customers. Generally, when companies use cash for purchases or repayments, it is recorded as a credit to the cash account and a debit to the account for the item purchased. The journal entry for this transaction will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Supplies | $$ |

When companies receive cash for the goods or services they offer, it is recorded as a debit to the cash account and a credit to the corresponding account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Revenue | $$ |

Equipment

Equipment is tools used by companies for the achievement of various objectives; this includes computers, tractors, cars, drills, etc. The type of equipment used by companies varies from one company to the next based on the industry in which they are operating as well as the period of the company’s existence. The journal entries in accounting examples for equipment are different for when the equipment is bought, depreciated, or sold.

The journal entry to record the purchase of equipment involves the cash account and the account for the particular equipment that was bought. The cash account is usually credited while the account for the particular equipment is debited. Here, we shall use computers as the equipment in question. The journal entry made when the equipment has been purchased is similar to the one shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Computers | $$ | |

| Cash | $$ |

As the equipment gets used by the company and depreciates, its depreciation is recognized and recorded as a debit to depreciation expense and a credit to accumulated depreciation as shown in the following table.

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Depreciation expense | $$ | |

| Accumulated depreciation | $$ |

When companies decide to sell off any of their equipment, the journal entry made to record the transaction will vary based on whether the equipment is fully depreciated or not. It additionally varies based on whether the company will give out the equipment or sell it off. The tables below will show the example journal entries that can be made in different instances.

If the equipment is fully depreciated and the company chooses to give it out to another company or individual, the company will record the transaction as fol

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accumulated depreciation | $$ | |

| Computers | $$ |

In an instance where the company chooses to give out equipment that is not yet fully depreciated, it will result in a loss and the transaction will be recorded as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Loss on equipment disposal | $$ | |

| Accumulated depreciation | $$ | ||

| Computers | $$ |

If the equipment sold by the company sells equipment that is not fully depreciated and makes a profit on the sale, its journal entry will involve four accounts. The cash and accumulated depreciation accounts will be debited while the gain on asset disposal and equipment account will be credited as seen in the following table:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Accumulated depreciation | $$ | ||

| Gains on asset disposal | $$ | ||

| Towing vans | $$ |

Investment

When companies make investments, they do so with the hope of deriving economic benefits. Investments are the creation or purchasing of assets that would yield profits either as rent or interest earnings, get paid dividends, appreciate in capital over the years, or have a combination of any of the aforementioned benefits. The journal entry for investment looks like the one below;

| Date | Account | Debit | Credit |

|---|---|---|---|

| MM/DD/YYYY | Investment | $$ | |

| Cash | $$ |

Land

Companies consider land as a very valuable asset; this is because instead of depreciating as time passes like other assets, it appreciates in value instead. For land, three different journal entries can be made to record its purchase and sale either at a profit or at a loss. Selling land at a profit is however the most common phenomenon.

When companies purchase land, the journal entry made to record the purchase differs based on how they made they made the land purchase. If the land was purchased using cash, the journal entry will be as follows:

| Account | Debit | Credit |

|---|---|---|

| Land | $$ | |

| Cash | $$ |

If the company purchases the land using a loan, the transaction will be recorded as shown below:

| Account | Debit | Credit |

|---|---|---|

| Land | $$ | |

| Loans payable | $$ |

In an instance where a company sells a piece of land, the transaction will either result in a gain or a loss. The sale of land generally results in a gain and can be recorded as shown below:

| Account | Debit | Credit |

|---|---|---|

| Cash | $$ | |

| Gain on land sale | $$ | |

| Land | $$ |

In a case where the land owned by a company is located in a place that is prone to natural disasters or a neighborhood that is considered dangerous, it may sell such land at a price that is lower than the land’s initial purchase price. The journal entry to record the loss on land sale will be as follows:

| Account | Debit | Credit |

|---|---|---|

| Cash | $$ | |

| Loss on land sale | $$ | |

| Land | $$ |

Merchandise inventory

Companies that buy goods either from manufacturers or retailers with the aim of selling such goods to make a profit will have an account in their books known as the merchandise inventory account. The merchandise inventory records all the goods that a company has in stock for sale. It additionally includes the expenses associated with the good purchase such as the cost of shipping and all other related expenses made when the goods were purchased. The journal entry for merchandise inventory is as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Merchandise inventory | $$ | |

| Cash | $$ |

If the company purchases the merchandise on credit, the journal entry will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Merchandise inventory | $$ | |

| Accounts payable | $$ |

Notes receivable

Notes receivable is an account that records the amount owed by customers to the company. Unlike accounts receivable which have a short payment time frame, a note receivable has a higher time frame of payment. A note receivable is a written promise by a customer to a company stating a specified amount due to be paid by the customer to the company in the future. It is usually made for the payment of goods or services received on credit and is recorded in the company’s journal as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Notes receivable | $$ | |

| Sales | $$ |

Since notes receivable usually have an interest associated with them, at the time of paying the note receivable, the client makes an additional interest payment to the company. The transaction for the payment of a note receivable will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Notes Receivable | $$ | ||

| Interest Revenue | $$ |

Examples of equity and contra-equity accounts and their journal entries

Capital stock

The capital stock is an account on the company’s balance sheet that records the total amount realized by a company from the sale of shares, these shares can be either common stock or preferred stock. The issuing of these shares can either be at par value or above par value. When a company issues preferred or common stock at par value, it is recorded as a credit to the capital stock account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Preferred stock or common stock | $$ |

In an instance when the company sells shares above par value, the additional amount received is recorded in a different account known as the additional paid-in capital account. The journal entry for the sale of shares above par value is as shown in the following table:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Preferred stock or common stock | $$ | ||

| Paid-in capital | $$ |

When companies want to increase the number of outstanding shares they have and maintain their working capital, they can choose to pay service providers with shares. The number of shares issued to the service providers is usually equivalent to the cash amount that they would have been paid. The journal entry to record that payment of service providers in shares will be as shown below:

| Account | Debit | Credit |

|---|---|---|

| Organizational cost | $$ | |

| Preferred or common stock | $$ |

Retained earnings

The retained earnings account records the company’s earnings since its establishment after the subtraction of all dividend payments to shareholders. They are the portion of the company’s earnings that have been kept instead of being distributed as dividends. It is recorded under the equity section of the balance sheet along with share capital. The journal entries for retained earnings are made whenever dividend payments are made to shareholders and whenever the company transfers its net income to the income summary account. The income summary account temporarily closes the income and expenses of a company at the end of each accounting period.

When the records of the net income of a company is a profit, it translates to a credit to the retained earnings account whereas a loss results in a debit to the retained earnings account. For profits, the retained earnings journal entry will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Income summary | $$ | |

| Retained earnings | $$ |

In a situation where the company experiences losses instead of profits at the end of the accounting period, the journal entry will be a debit to the retained earnings account and a credit to the income summary account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Retained earnings | $$ | |

| Income summary | $$ |

When companies declare distributions, the amount that will be paid as dividends to their shareholders is usually deducted from the retained earnings account on the date of the declaration. The journal entry to record the payment of dividends will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Retained earnings | $$ | |

| Dividends payable | $$ |

Treasury stock

Treasury stock is the number of shares that have been bought back by the issuing company. Companies generally buy back their shares to reduce the number of outstanding shares that are available to investors and to increase the value of their shares. The maximum amount of shares that may be bought back by companies in the United States is determined by the Securities and Exchange Commission (SEC). Treasury stock is a contra-equity account on the balance sheet of companies and is also referred to as treasury shares or reacquired shares.

When companies buy back their shares, the journal entry to record the transaction involves a credit to the cash account and a debit to the treasury stock account as follows:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Treasury stock | $$ |

Examples of expense accounts and their journal entries

- Cost of goods sold(COGS)

- Depreciation expense

- Notes payable

- Purchase

- Rent expense

- Salaries expense

- Supplies expense

- Utilities expense

Cost of goods sold (COGS)

The cost of goods sold (COGS) is an account on the income statement of companies that comprises the cost of raw materials and the direct labor used in the creation of goods. In order to make a journal entry for the cost of goods sold, it has to be first calculated using the formula COGS = Beginning inventory + Purchases during the period – Ending inventory

The cost of goods sold account increases with debits and decreases with credits; therefore, the journal entry to record the purchase of goods will be recorded as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cost of goods sold | $$ | |

| Purchases | $$ | ||

| Inventory | $$ |

Depreciation expense

Depreciation expense is an account that records the decrease in value of an asset for a single period. It is the portion of a fixed asset that is calculated to have been used in the period under review. Depreciation expense is a non-cash expense, this is because it gradually reduces the carrying amount of the fixed assets as they depreciate in value with use. When making a journal entry for depreciation expense, the depreciation expense account is debited while the accumulated depreciation account is credited as shown below:

| Date | Account name | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Depreciation expense | $$ | |

| Accumulated depreciation | $$ |

Notes payable

When companies make purchases on credit, they could issue a written promise to the supplier of the goods stating their intention to pay up the debt within a stipulated time frame. This written promise is called a promissory note and it indicates that the company that issued it owes the company it made the promissory note for. Upon issuing a promissory note, a journal entry is made to record the transaction with a debit to the cash account and a credit to the notes payable account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Notes payable | $$ |

When the company that issued the promissory note pays up what they owe, the journal entry becomes reversed with a debit to the notes payable and credit to the cash account as shown in the table below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Notes payable | $$ | |

| Cash | $$ |

Since the issued note payable includes an interest payment, an additional journal entry for the accrued interest will be made as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Interest expense | $$ | |

| Interest payable | $$ |

When the accrued interest for the notes payable is paid, another journal entry is made to indicate the payment as seen below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Interest payable | $$ | |

| Cash | $$ |

Purchase

A purchase is the buying of goods or services either in cash or on credit payment. It is a big part of the manufacturing process as raw materials that are processed into finished goods must be purchased and some steps in the manufacturing process are sometimes outsourced. Assets are also purchased by companies to ease various operations. The journal entry for purchase varies depending on whether the purchase was made in cash or credit.

For the purchase of an asset such as computers, the journal entry to record the transaction will be a debit to the computers account and a credit to the cash account as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Computers | $$ | |

| Cash | $$ |

If the purchase was made on credit, the journal entry will be a debit to the computers account and a credit to the accounts payable as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Computers | $$ | |

| Accounts payable | $$ |

Rent expense

The rent expense account records the amount companies pay for the offices, warehouses, production plants, etc. that they use for their business operation. It is a typical expense for all companies that do not own the buildings in which they operate. The payment of rent is made either monthly, quarterly, or annually depending on the payment agreement between the company and the owner of the property.

The journal entry for rent expense involves the rent expense and the cash account. Although the cash account is used, the rent payment could be by bank transfers, cheques, or card payments. The journal entry for the transaction is as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Rent expense | $$ | |

| Cash | $$ |

Salaries expense

Salary refers to the non-hourly payment made by companies to their employees. This amount is usually specified at the time of employment and is paid either weekly or monthly. The salaries expense of a company is usually unchanged from one accounting period to the other unless some employees are laid off or resign or there is a pay reduction which will lead to a decrease in the amount; If some employees get promoted, it will conversely lead to an increase in the overall amount paid to employees by the company.

When recording salaries expense, companies may use the cash accounting method or the accrual accounting method. Companies that use the cash accounting method record salaries expense when they have made payments to employees as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Salaries expense | $$ | |

| Cash | $$ |

Companies that use the accrual accounting method to record their salaries expense make a journal entry once the employees have earned the salary even before it gets paid. Hence, they make two different journal entries for the salaries expense. First when the employees earn the salary and second when the company makes payment.

The first journal entry made when the salary is earned involves a debit to the salaries expense account and a credit to the salary payable account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Salaries expense | $$ | |

| Salary payable | $$ |

The second journal entry is made when the employees receive their salaries; thus clearing the salary payable account as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Salary payable | $$ | |

| Cash | $$ |

Supplies expense

The supplies expense account records the cost of consumables that are used by a company within a particular accounting period. These consumables include items that are regularly used in the day to day business operations such as coffee, pens, paper towels, papers, light bulbs, ink, etc. Since most companies purchase these consumables in large quantities, the supplies are considered an asset before it is consumed and recorded as supplies on hand.

The journal entry for such a large purchase of supplies will involve the supplies on hand account and the accounts payable if the purchase is made on a credit or the cash account if the purchase was paid for immediately. The journal entry will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Supplies on hand | $$ | |

| Accounts payable or cash | $$ |

Since most companies purchase supplies in large quantities, adjusting entries are made at the end of each accounting period to ensure that the supplies account accurately reflects the supplies on hand and the supplies used during the accounting period. The supplies that have been used up get recorded as supplies expense and the journal entry will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Supplies expense | $$ | |

| Supplies on hand | $$ |

If the supplies the company purchases are presumed to be used within one accounting period, they will be recorded as a debit to the supplies expense account and a credit to the cash account or the accounts payable depending on whether the supplies were paid for in cash or gotten on the account. The journal entry for such a transaction is as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Supplies expense | $$ | |

| Accounts payable or cash | $$ |

Utilities expense

Utility expense is the cost incurred by companies for their use of various utilities such as electricity, water supply, natural gas, telephone services, waste management, internet, etc. These utilities are usually consumed before they are paid for and vary from one accounting period to the next based on the amount of utility consumed. Upon receipt of the utility bill, the company makes a journal entry similar to the one below to record it.

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Utilities expense | $$ | |

| Utilities payable | $$ |

When the company clears the utility bill, it makes a new journal entry to record the payment as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Utilities payable | $$ | |

| Cash | $$ |

See also: Gain on Sale journal entry examples

Examples of liabilities and contra liability accounts and their journal entries

Accounts payable

There are instances when companies buy goods or services on credit, in such an instance, they record such transactions to the accounts payable if it needs to be settled within 30 to 90 days. Hence, the accounts payable record short-term liabilities. Accurately recording accounts payable aids companies in tracking the amount owed to suppliers and service providers. It also aids in timely and correct payments to creditors.

The journal entries in accounting made for accounts payable indicate an increase or a decrease in the accounts payable balance. There is an increase in the accounts payable when companies make purchases on credit and a decrease when they pay part or all of the amount owed. The journal entry to record the purchase of goods on credit will be a debit to the goods bought such as furniture and a credit to the accounts payable as seen below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Furniture | $$ | |

| Accounts payable | $$ |

When the company makes payment to settle what they owe, the journal entry to record the transaction will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accounts payable | $$ | |

| Cash | $$ |

Capital

Capital is the amount invested into a business by the business owner, its partners, or shareholders. The capital is raised through direct investment into the business or through the purchase of the different types of stocks or bonds that the company has issued. Capital is considered a liability because it usually has to be paid back to the investor in the future.

When making a journal entry for capital, the cash account is debited while the capital account is credited as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Capital | $$ |

Unearned revenue

The unearned revenue account records the revenue received by companies for goods or services that have not yet been delivered. It is therefore a prepayment to the company. This amount is recorded as a liability on the balance sheet of companies since they have not yet earned it.

For such unearned revenue, two different journal entries are made to record the transaction; first when the company receives the payment and second when they render the service or provide the good. The first journal entry will be as shown below:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Unearned Revenue | $$ |

When the unearned revenue is earned either by delivering the goods or rendering the services to the customer, the company then records the earned revenue as a debit to the unearned revenue account and a credit to the revenue account as follows:

| ACCOUNT | DEBIT | CREDIT |

|---|---|---|

| Unearned revenue | $$ | |

| Revenue | $$ |

Utilities payable

The utilities payable account records the amount owed to service providers for services received monthly, quarterly or yearly; depending on the payment system. Since this amount owed to service providers is mostly due for payment within one month, the utilities payable are considered a current liability. Utilities payable should not be confused with the utility expense because, while the utility expense records the amount spent on services that have already been received and paid for, the utilities payable records the amount owed service providers for services that have not yet been paid for.

Thus, all utilities payable become utilities expense once their bill is settled. The journal entries for utilities payable are the same as the journal entries for the utilities expense. The first journal entry involves a debit to the utilities expense account and a credit to the utilities payable account. The second journal entry is made when the utility bill has been paid; it involves a debit to the utilities payable account and a credit to the cash account. These two journal entries will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Utilities expense | $$ | |

| Utilities payable | $$ |

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Utilities payable | $$ | |

| Cash | $$ |

Examples of revenue and contra revenue accounts and their journal entries

Sales revenue

Sales revenue is the amount a company earns from the sale of goods within a particular accounting period. Although companies may also sell their assets that have already been depreciated or that are not yet fully depreciated, the money earned from the sale of these assets is not considered sales revenue. It is rather recorded as a gain or loss on asset disposal depending on whether the asset sale resulted in a profit or a loss.

When a company sells goods to a customer who pays in cash, a journal entry debiting the cash account and crediting the sales revenue account is made to reflect the increase in cash and business revenue. The journal entry will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Sales revenue | $$ |

If the goods sold are liable to taxation, then the journal entry will also include the sales tax payable account. This account records the amount that will be paid to the government as tax. The journal entry for such a transaction will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Sales tax payable | $$ | ||

| Sales revenue | $$ |

In a situation where the sale of goods was made on credit, the journal entry will be a debit to the accounts receivable and a credit to sales revenue as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accounts receivable | $$ | |

| Sales revenue | $$ |

Furthermore, if the sale is tax liable it will include the sale tax payable account as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accounts receivable | $$ | |

| Sales tax payable | $$ | ||

| Sales revenue | $$ |

When the customer makes payment to clear up their debt, the journal entry will be a debit to cash and a credit to the accounts receivable as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Accounts receivable | $$ |

Sales discount

A sales discount is a reduction in the amount a customer is supposed to pay a company for goods or services received on credit. This sales discount is dependent on the credit terms that the company offers the customers which allows them to pay a certain percentage less than the total amount they are supposed to pay. The sales discounts usually come with a predetermined date for the customer to make the payment and if the customer does not pay for the goods or services within the stipulated discount time frame, the price reduction becomes forfeited.

The sales discount is normally indicated on the goods or services invoice. For instance, an invoice with 5/10 net 30 indicates that the customer is eligible to receive a 5% discount on the total invoice amount if they pay within 10 days. Otherwise, the customer is expected to pay the full invoice amount 30 days from the time of the transaction. When sales that carry a sales discount are made, the company does not record the sales discount immediately, instead, it is recorded as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Accounts receivable | $$ | |

| Sales | $$ |

When a customer pays for the purchase made and it meets the sales discount terms, the journal entry to record the payment will then include the sales discount account as shown below:

| Account | Debit | Credit |

|---|---|---|

| Cash | $$ | |

| Sales discount | $$ | |

| Accounts receivable | $$ |

If the customer fails to make payment within the time frame in which the sales discount is applicable, then the customer will have to pay the full invoice amount, and the journal entry to record the payment will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Accounts receivable | $$ |

Service revenue

The service revenue account records the income that a company makes from rendering a service. Similar to goods, services can be rendered on credit or be paid for in cash. When the service rendered is paid for immediately after the service is completed, it will be recorded as a debit to the cash account and a credit to the service revenue account as shown below:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Cash | $$ | |

| Service Revenue | $$ |

If the service was rendered on credit, then the journal entry will be a debit to the accounts receivable and a credit to the service revenue earned account as shown below:

| Date | ACCOUNT | DEBIT | CREDIT |

|---|---|---|---|

| DD/MM/YYYY | Account receivable | $$ | |

| Service revenue earned | $$ |

Revenue

The revenue account is also known as the sales account. It records the revenue generated from the sales of goods (sales revenue) and from the services rendered (service revenue). The revenue account is often used to record these revenues by companies who do not differentiate between service and sales revenue and those who are engaged in only one business activity, that is, those companies who are only involved in only sales of goods or provision of services.

The journal entry for revenue is as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash or accounts receivable | $$ | |

| Revenue | $$ |

If the revenue generated has a tax liability, then the journal entry will be as shown below:

| Date | Account | Debit | Credit |

|---|---|---|---|

| DD/MM/YYYY | Cash or accounts receivable | $$ | |

| Sales tax payable | $$ | ||

| Sales revenue | $$ |

When the goods or service is paid for in cash, it will be debited to the cash account whereas if it was taken on credit, then it will be debited to the accounts receivable.

See also: Unearned revenue examples and journal entries

Conclusion

Companies make journal entries for various transactions to keep a concise, accurate, and timely record of the organization’s business transactions. They are a fundamental bedrock that provides answers to cogent questions such as how much revenue is the company making. What is the extent of the company’s liabilities? How large are the company’s expenses? And many other questions that need the information provided by the various journal entries of the company.

Furthermore, the validity and accuracy of the company’s financial statements depend on the information obtained from its journal entries. Although a lot of companies now use accounting software to record various transactions, keeping manual records of journal entries is often used as backup files for business transactions.

Last Updated on November 4, 2023 by Nansel Nanzip Bongdap

Blessing's experience lies in business, finance, literature, and marketing. She enjoys writing or editing in these fields, reflecting her experiences and expertise in all the content that she writes.